HHC - Howard Hughes Corp.: Examining The Bear Case

Summary

- Howard Hughes shares have bounced 15% since it was announced that Bill Ackman's Pershing Square would tender for another 12.7% of the shares at $60.

- Howard Hughes shares have significantly underperformed the Vanguard REIT Index/ETF for over a decade.

- Reasons for underperformance include outsized Houston exposure, outsized office exposure, ongoing losses at its Seaport project, and high cash overhead expenses.

- The bulk of Howard Hughes value comes from land for future development. Higher interest rates and an economic downturn will.

- While shares trade at a large discount to Howard Hughes published estimate of its Net Asset Value, I am avoiding the stock as I believe shares are cheap for a reason.

After falling nearly 50% since the start of the year, Howard Hughes ( HHC ) shares have bounced 15% since it was announced that Bill Ackman's Pershing Square would tender for another 12.7% of the shares at $60. Should the tender succeed, this would bring Pershing's interest in HHC to 40%. Many investors are wondering whether they should follow Ackman's lead and initiate or increase their stake in HHC shares.

While I understand the merits of the bull case (recapped below), I do not have confidence that this time is different - HHC share have traded at a large discount to theoretical NAV for years and I lack conviction that this will change any time soon.

Recap of the Bull Case

The bull case for owning HHC shares includes:

1/ HHC is comprised of a unique collection of master planned community ((MPC)) assets in sunbelt markets which are experiencing a population boom. Here is a video of Bill Ackman describing HHC's MPC business. In a MPC, one entity owns a contiguous parcel of land where it is the de facto municipality (real life Sim City). MPC have the potential for significant value creation for investors with long time horizons as:

A) Because all the land is owned by one entity, project construction can be coordinated to optimize land use/get the optimal mix of retail, office, residential, industrial, etc.

B) While oversupply can depress CRE markets/submarkets, through a controlled development program - to an extent (within the submarket) the MPC owner can limit development and reduce the risk of excess supply which should bolster rents and property prices - even in downturns.

C) MPCs can focus on creating upscale single family residential communities with high household incomes that increase the value of surrounding retail, office, and multifamily rents and property values.

2/ HHC trades at a deep (65%) discount to the company's published NAV estimate. SA Contributor Noor Darwish does a great job of walking through HHC's NAV estimate and discussing adjustments investors may want to consider.

3/ Bill Ackman has a strong investing track record as head of Pershing Square and as Chairman he will ensure value creation for HHC shareholders.

What has gone wrong?

Despite the aforementioned positives, an investor who purchased HHC shares 10 years ago would be down 14% on his purchase while having received zero dividends over the past decade. By comparison, an investor in the Vanguard REIT Index/ETF ( VNQ ) would have earned just over 6% total annualized return over the past decade. It is important to understand that Bill Ackman has been Chairman of the Board the entire time (since 2010).

Here's a look at some of the things which have gone wrong at Howard Hughes in the past 10 years:

1/ Rather than focus on its core MPC business, the company has made a foray into an ill-conceived speculative development project called Seaport in New York. While HHC has sunk over $1 billion into this project since 2014. Despite completion in 2019, today Seaport is generating no net operating income (it is actually still burning cash). Fair to say this project has been a total bust.

2/ The bulk of HHC's MPC assets are located in the greater Houston MSA (Bridgeland & the Woodlands). Houston's economy is heavily dependent on the energy sector which suffered a significant downturn from 2015-2020. Beyond cyclical factors, Houston is a structurally challenged commercial real estate market, largely due to a lack of zoning (supply, supply -there's always plenty of supply). While HHC's assets are somewhat insulated from supply (because HHC controls the supply within a few miles), Bridgeland and the Woodlands are competing with lower cost properties in the surrounding area. This is unlikely to change.

3/ Almost half of HHC's stabilized (income generating) assets are office properties in Houston. Office values have plummeted since the onset of the pandemic and have fallen further as interest rates have soared in 2022. HHC's NAV is based on cap rates in the 6-7% range while most office REITs are trading with implied cap rates of 8-10%.

Some of these were purchased in late 2019 (to some extent unlucky as COVID hit months after the deal closed). But it can be argued that buying existing office properties as outside the core competency of an MPC developer/operator -especially given the size of the transaction (was ~11% or so of total assets at the time).

4/ Failed sales process in 2019 - In June 2019, HHC announced it was reviewing its strategic alternatives to maximize shareholder value. While this sent the shares up 40% to ~$135 on the day of the announcement, the review concluded without a sale (no rumored bids), investors began to question the true value of HHC and its assets, and the stock price plummeted.

5/ The onset of the pandemic coincided with the large office purchase forced HHC to sell equity at $50/share in 1H20 to shore up its balance sheet.

6/ Howard Hughes has incurred ~$1.2 billion ($20+/share) in overhead expenses over the past decade. Development operations are much more costly to run than stabilized real estate operations (completed buildings).

Why I'm Not Buying the Stock today

Many of the aforementioned factors which have caused the massive underperformance over the past decade remain in place today:

1/ Bill Ackman remains Chairman. With 27+% ownership (likely going to 40%) he is firmly in control of HHC. While Ackman has been a very good investor overall, his magic has not worked at Howard Hughes and it is unclear what would cause this to change.

2/ Houston will remain a difficult market - a lack of zoning is an ongoing invitation for oversupply in surrounding areas. While HHC is somewhat insulated from this (higher income submarkets with the ability to control supply) the city remains dependent on the energy economy (which is admittedly providing a boost these days).

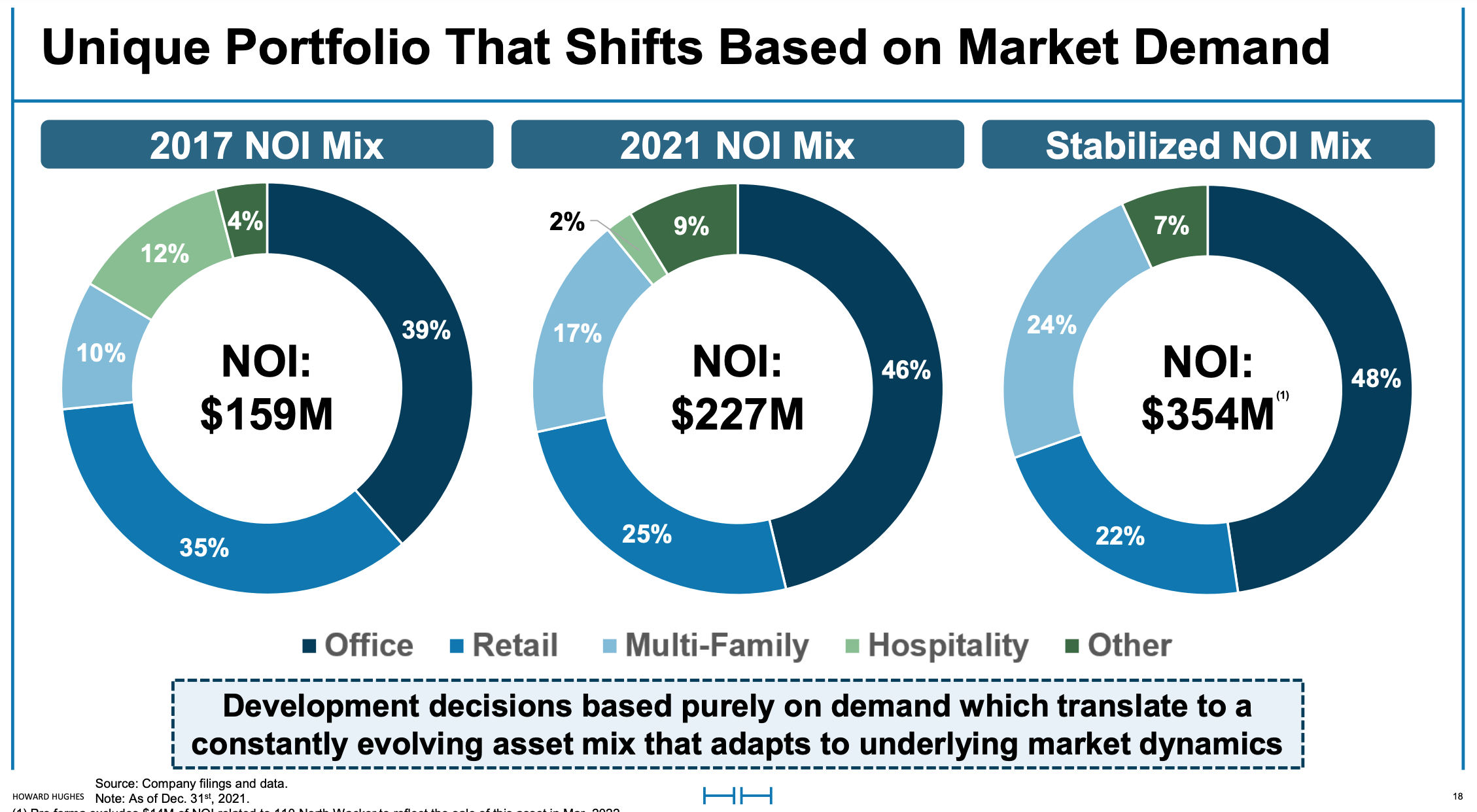

3/ Nearly half of NOI (see below) comes from office properties. This is forecast to increase - HHC has more new office properties in development. The future of office is uncertain given the double whammy of work from home pressures as well as an economic downturn.

NOI by Property Type (Howard Hughes Investor Presentation)

{kind=link}

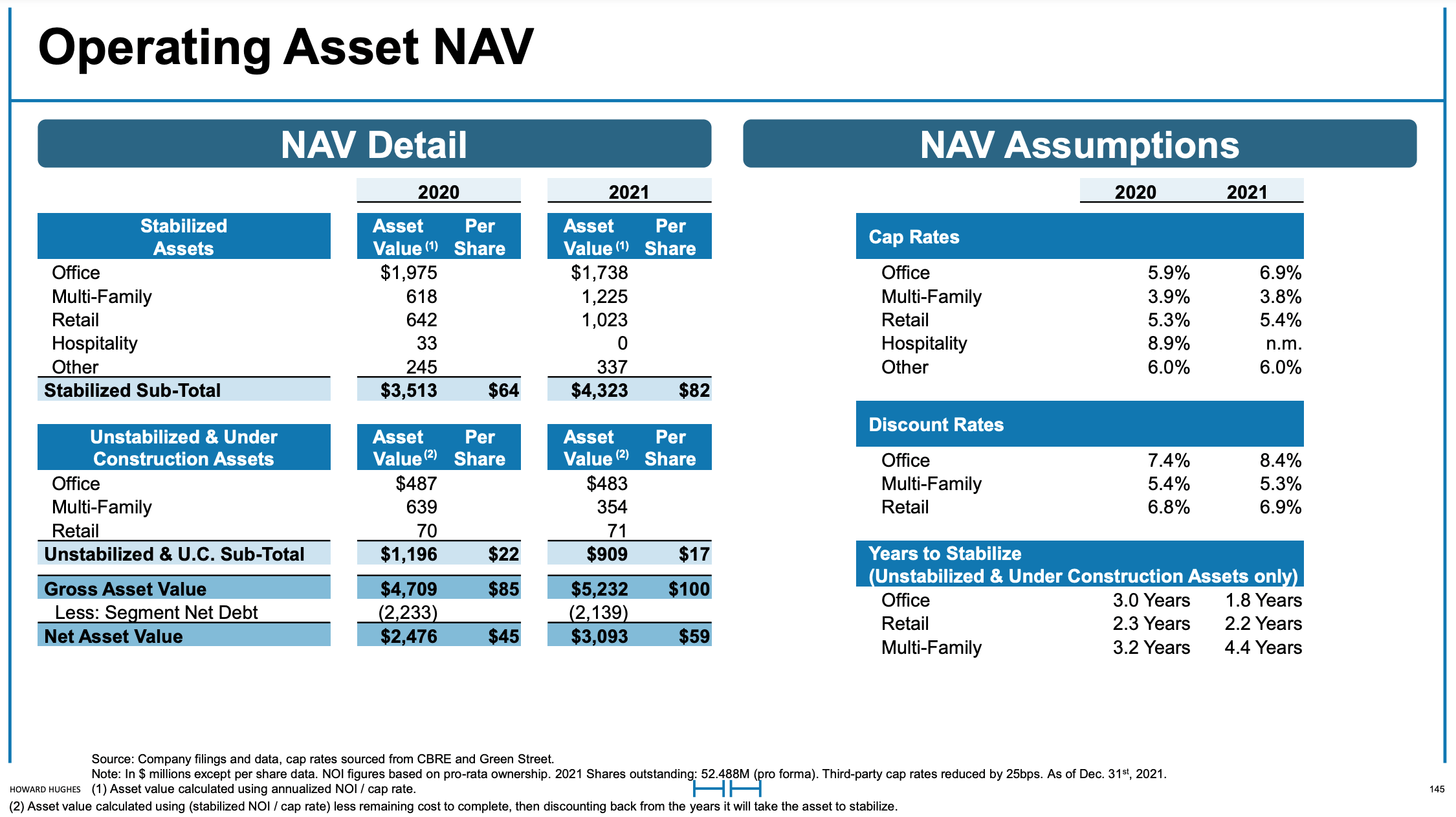

4/ Cap rates are too optimistic. Below I show cap rates assumed by HHC in its NAV estimate:

Cap rate assumptions (Investor Presentation )

{kind=link}

As I mentioned, implied office cap rates are meaningfully higher than those assumed above. The same holds true for multifamily, retail and other.

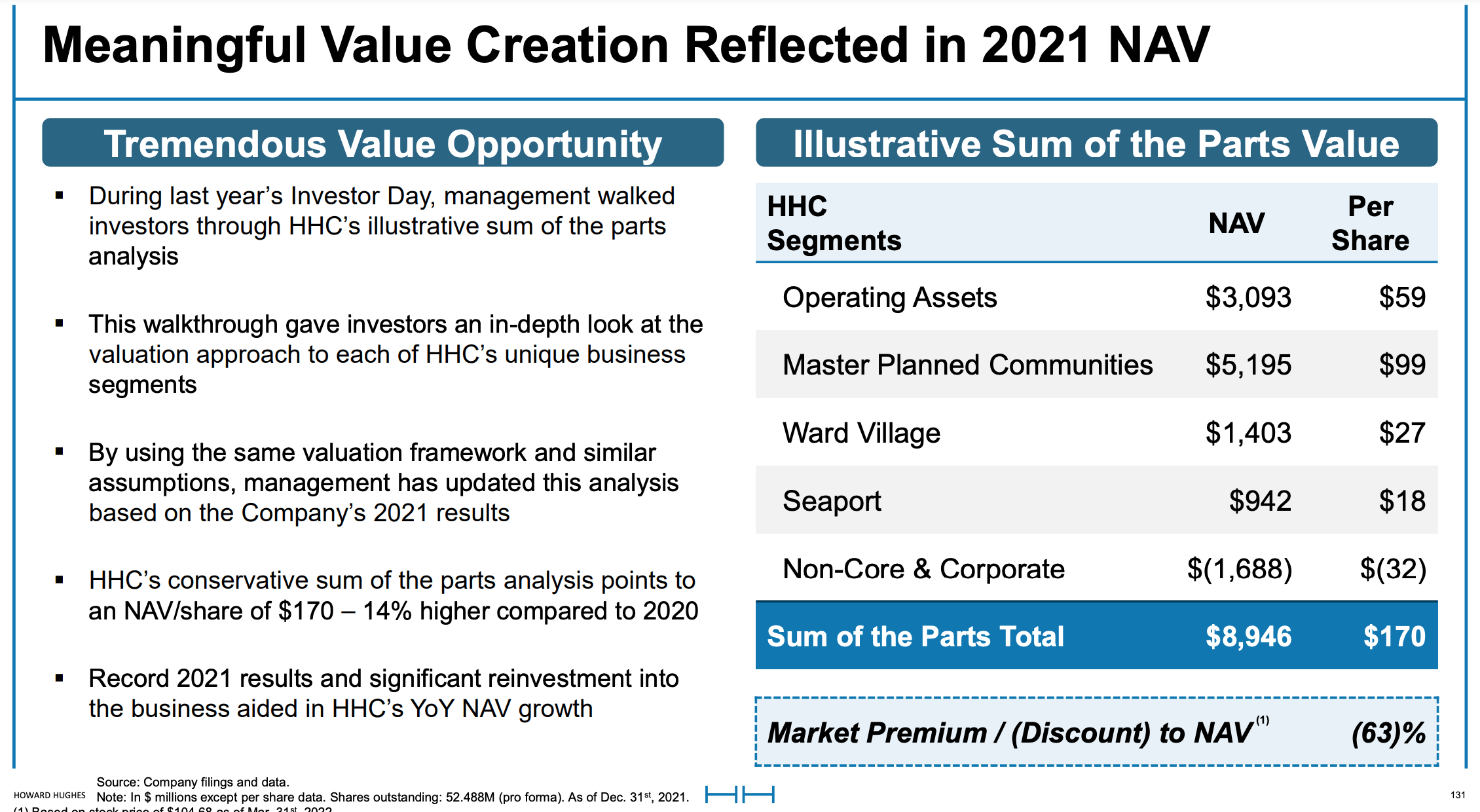

5/ Undeveloped land is a tough place to be in an economic downturn -Given the dramatic rise in interest rates, we are already seeing a dramatic slowdown in new home construction and are seeing the beginning of a slowdown in commercial real estate development. As shown below, over half of HHC's estimated NAV comes from properties for development (Master Planned Communities in the NAV slide below). Undeveloped land is generally considered the highest risk/most speculative type of property investment. The reason for this is because while leased/stabilized properties generate positive cash flows for owners, undeveloped property requires cash flow (with no certainty of payback). An economic downturn further increases this risk as it lengthens the period investors will have to put in cash and pushes out the ultimate receipt of that cash.

Howard Hughes Management's NAV Estimate (Investor Presentation)

{kind=link}

Conclusion

I am not convinced that HHC's future will be materially different from its past given the structural challenges of many of its assets and my belief that the company will fare poorly in an economic downturn. Further, with most high quality REITs trading at meaningful discounts to NAV and paying 3.5+% and growing dividend yields (I've written up a handful here on SA over the past few weeks which offer attractive upside), I see no reason to get involved with Howard Hughes. While HHC is likely undervalued, complex sum-of-the-parts NAV stories (with no dividend as land represents most of the value) tend to stay cheap.

For further details see:

Howard Hughes Corp.: Examining The Bear Case