HHC - Howard Hughes: This Is A Tricky One But I'm At 'Hold'

Summary

- A subscriber asked me to take a look at an investment of his that has yielded good RoR - The Howard Hughes Corporation.

- Howard Hughes Corp is a real estate developer out of Texas, with a 12-13 year history after spinning off from General Growth Properties.

- Most of its holdings are focused on master-planned communities. The company does not have a yield, which is rare for this type of RE.

- I'm establishing my fundamental thesis for Howard Hughes Corp here.

Dear readers/followers,

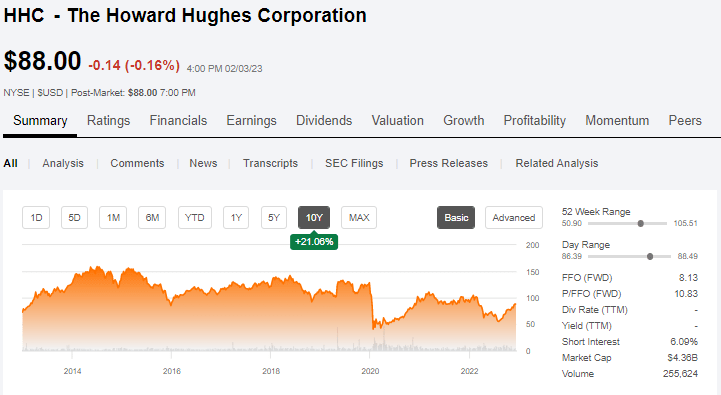

I'm happy to take subscriber and reader requests to look at companies and businesses - in this case, it's the Howard Hughes Corporation ( HHC ), a component of the Russel 1000 and a real estate developer out of Texas. Its founding came about 13 years ago, and its headquarters is in The Woodlands, Texas.

A reader of mine managed to invest substantial amounts back in October and is now sitting on a very nice gain given that the company has risen to $88/share. His question here is whether this is a company that he should hold, given the no-dividend and 6%+ short interest, or whether the time has come to sell.

Here I give you my take on the company.

Howard Hughes Corporation - From A to Z

So, HHC has annual revenues of about $700-$800M.

The company essentially runs Office, Retail, and Multi-family units in 6 attractive states and 8 communities. It manages a 10% historical yield on cost and a 24% RoE. Good numbers, from a high level.

The company was formed back in -10 after the financial crisis from General Growth properties. GGP was the second-largest shopping mall operator in the US, and it was subject to the largest real estate bankruptcy in American History back when it filed in -09. What remained of the company was acquired by Brookfield, and it ranked only behind Simon Property Group ( SPG ) at the time. At the time of filing, the company proposed a plan which included spinning off a new company that would hold those assets/properties that had long-term potential, but little or zero income.

That's essentially what Howard Hughes Corporation is, or started out as.

It's the GGP properties, that at the time of filing in '09, were determined to have a future, but had little or no cash coming in at the time. It started out holding the types of assets that you see in the company today - mixed-use developments, master-planned communities, and raw acreage of land.

The famous Hedge Fund manager Bill Ackman was the new Chairman of the company.

Now, this was far from a "smooth sailing" sort of situation. I believe it fair to say that from a long-term perspective, this company has been a truly terrible investment.

{kind=link}

Okay, so maybe "truly" might be taking it too far - but it didn't even beat your average index fund, and it hasn't paid a cent of dividends for all the years its been in operation.

Credit? B+. It's junk-rated.

Let me say straight away that evaluating the appeal of this company is extremely tricky, because it lacks usable FFO/AFFO or income metrics. It showcases earnings, but those earnings go down up and down from year to year, down 129% in 2020, up 306% in '21, and down 107% again in 2023E. For most of the last 10 years, it's had negative FFO and AFFO. More on that later in valuation.

The Howard Hughes model of developing assets works as follows.

{kind=link}

Company FCF is used to fund develop opportunities, so NOI growth means more commercial development is possible. The combination of Residential Land Free Cash flow, $317M in 2021, Operating Asset NOI, and profit from condo sales at margins of upwards of 20-30% funds equity for future developments for the company, and this is what creates the positive Yield on cost and RoE.

But when I say things haven't gone well, I mean that.

The company responded to investor disappointment in 2019 due to the valuation and share price, by reviewing its options, and this included a sale of the company. Ultimately, HHC decided to go the "transformation" path, selling off billions in non-core assets and focusing on the master-planned communities, which seem to be the major sales driver here.

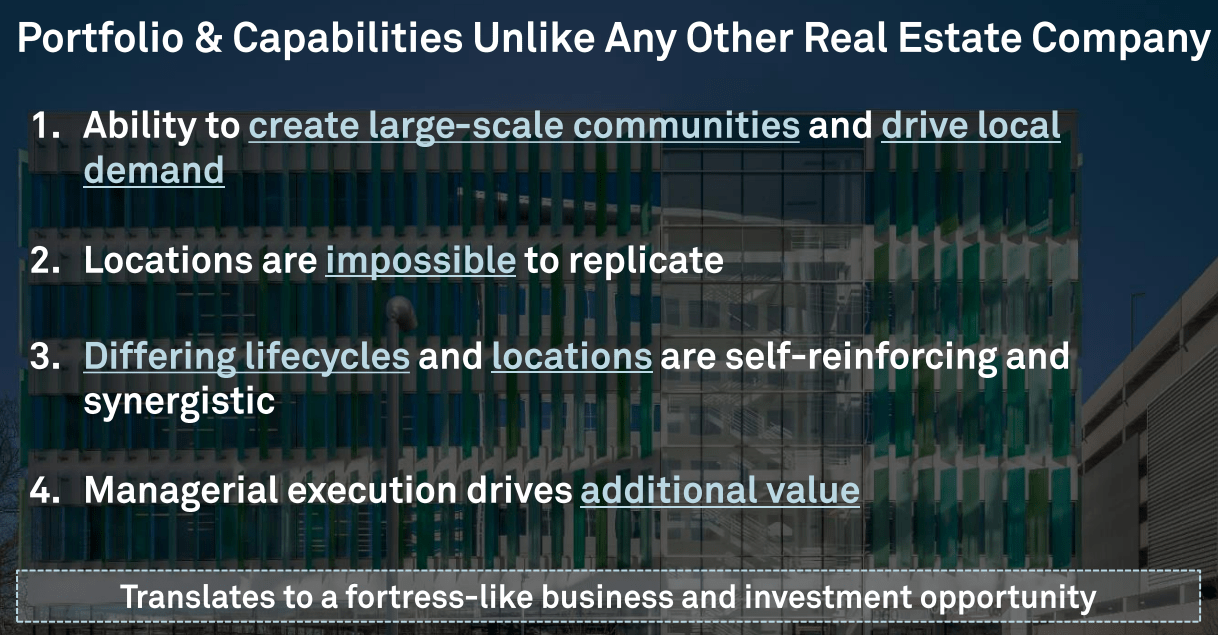

Theoretically, the opportunity for HHC to develop large-scale communities includes the ability to drive demand and control supply , which could actually insulate a business from the worst of economic cycles. HHC also claims that it's never more than "half" a building ahead of demand, which lessens the potential to get caught in the worst of a downturn.

The company reiterates the following upsides.

{kind=link}

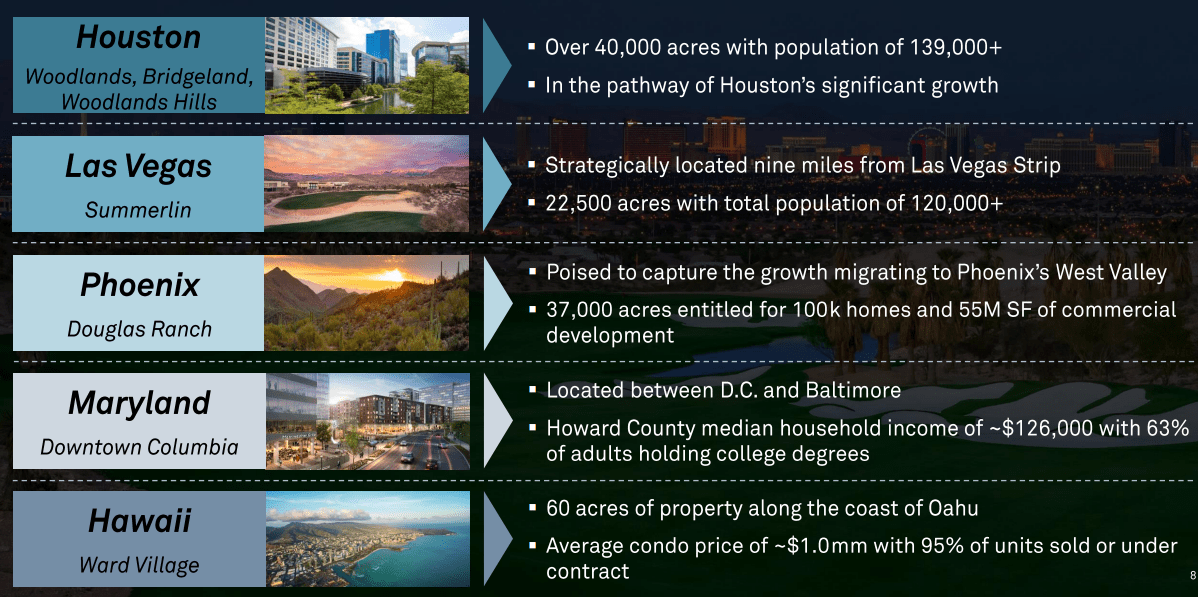

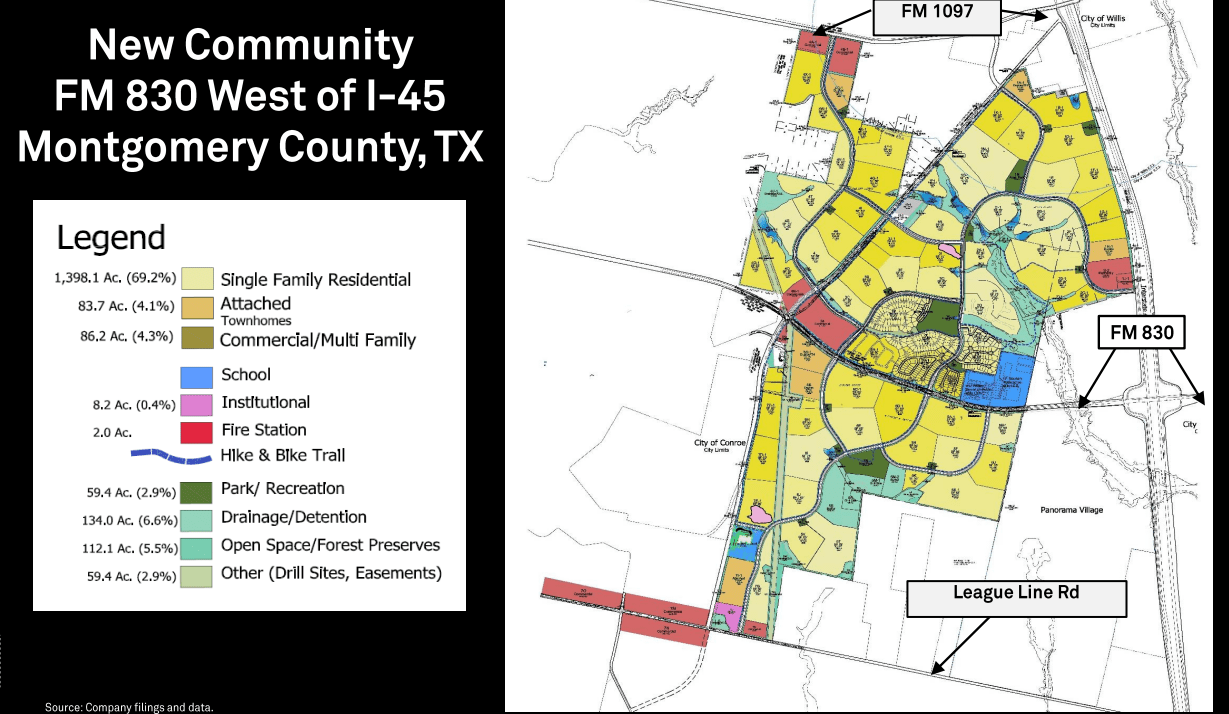

I've looked through some of the MPCs that the company speaks of - and they do look attractive, such as The Woodlands, Woodlands Hills, Sumerlin, Ward Village, and others. They're very well-situated typically, with the following examples.

{kind=link}

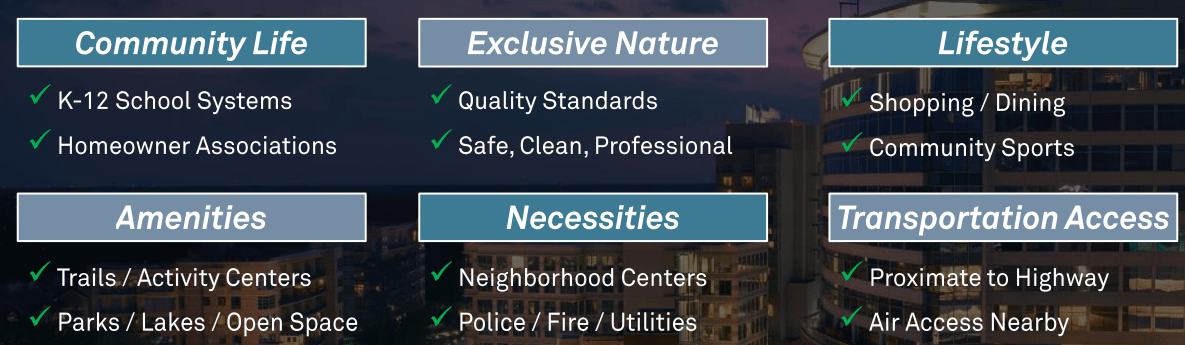

Unlike competitors, HHC has a very large land bank to access, and they use this land to turn into communities - selling residential to homebuilders, while developing the commercial, combining one-time sales with recurring NOI. HHC views every MPC as a small functioning city - large-scale, privately owned. These small cities include what families might want out of such a location.

{kind=link}

The company is able to showcase land value appreciation over time. Since 2011, the company's development land, like in Summerlin, Woodland and the like, has averaged appreciation of around 6-10% CAGR. The company targets a cycle of value creation, combining operating cash flow from NOI and developments, with land sales and equity appreciations.

Despite the B+ rating, the company has good liquidity, good debt maturities and an overall good cash situation. From a high level, this company seems quite attractive. Here is an example of how such a community that the company speaks about might be created and planned, based on the company's land bank.

{kind=link}

And overall, the company's communities are award-winning. The company has repeatedly been ranked as the best-selling MPC, landscape designer of the year, and developer of the year - especially down in Texas.

Frankly speaking, if I was looking to settle down or live somewhere in the US, this company's MPCs would be on my list to at least visit and look into. There is a lot to like here.

However, there are also risks and things not to like. The company has plenty of risks. Its absolutely outsized Houston exposure is a big reason. Another, especially in the current environment, is its office exposure - not exactly superb, or well-situated in this market. It's also wrong to call the company successful across the board because its Seaport project hasn't just been losing small amounts of money - overhead expenses that are climbing have really been a trend.

The numbers tell the real story - company presentations typically tell the company's story. It's not uninteresting, but we need to mix the two.

Part of the reason we're up as much as we are is that Ackman through Pershing square tendered another 12.7% of shares at $60/share.

Now, the upsides of HHC, or the bullish case, aren't to be dismissed. It's a superb set of MPCs, with the potential for some truly long-term value creation through a mix of land optimization, oversupply de-risking, and controlling demand. There is also the simple fact that the company is really dirt-cheap, compared to its NAV estimate - though this is the company's own published one, which needs to be examined as well.

However, this is a good example and a good "tale" of where every upside in the book, including Ackman who is experienced and capable, has not been able to deliver significant value.

Why is this?

A few reasons, but most of them centered around non-core speculative pushes, such as Seaport which is still losing money, as well as its overexposure to the office space - and this has been a net negative since the onset of COVID. Even compared to the office REITs I typically cover, I think HHC is being excessively bullish in its valuation, which I don't believe to be a good idea in this market, nor do I view it as valid.

Let's look at where HHC is in terms of valuation.

Howard Hughes Valuation

So, at a 25%+ stake, HHC is essentially in Ackman's hands to a large degree. Even if the valuation was favorable, we would need to look at what Ackman wants to do with the company, and what he wants to change in order for the ongoing trend to be broken and actually deliver shareholder value.

This is the real problem. Even with valuation facts as I will line them out below, I can't really see any change from how the company and its ambitions have been run for over 10 years - and what really hasn't worked, given where the share price has been.

The company keeps pushing its amazing MPCs, and I agree that they are great - but without any plans on how to turn the poorly-performing parts around.

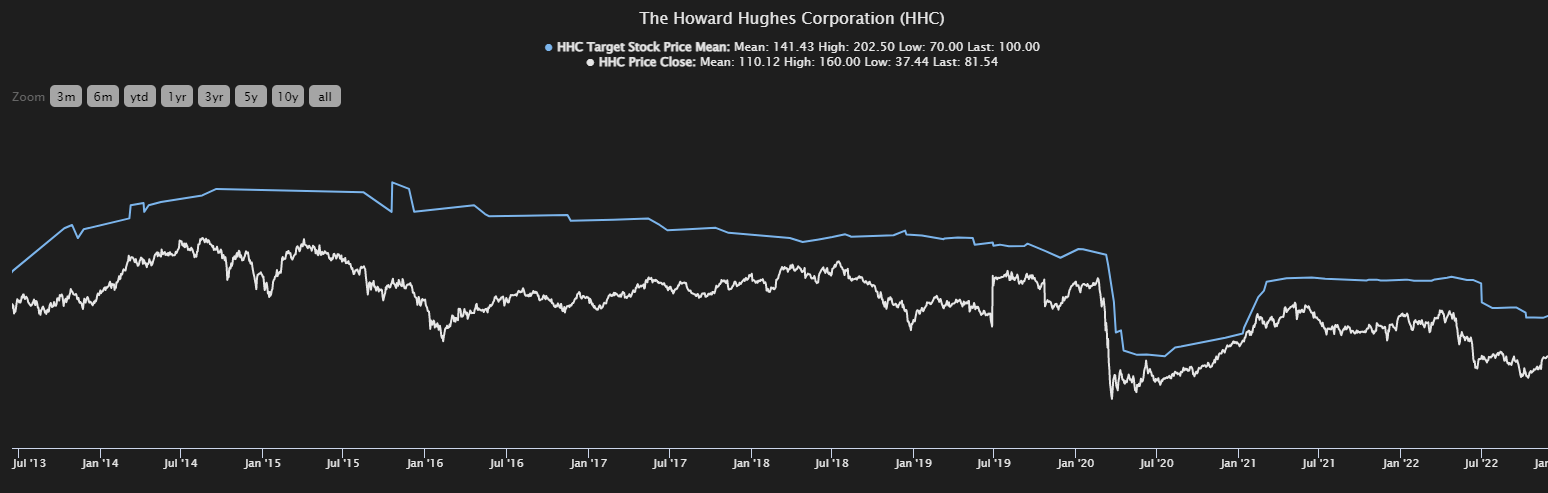

HHC has a lot of fans in the investment community. Current forecasts and price targets for the company range from an $80/share low to a $150 high, meaning out of those 5 analysts following the company, they should be frothing at the bit to buy the company at, or close to $88/share.

First off though, even if 5 out of 5 analysts are at "BUY" or "Outperform", they would have steered you extremely wrong for the past few years. Take a look at the average PT/valuation spread.

{kind=link}

The picture that I'm getting from that, aside from those analysts being happy with sub-par rates of RoR, is that we need to discount those targets at least 20-30% to get close historically to what the company could do or perform.

Now, supposedly at $88/share, the company is still only at 0.73x of NAV, less than 1.3x of book, 13x to EBITDA, and around 18x to P/E, but I feel the positives here really fail to take the company's risk ratio into account.

First, historical results. The company has been overpromising for over a decade - almost nothing has come from it. I don't see any changes in the plans in the future either.

Second , if you break down NOI, most of it is coming from Office, and this is expected to increase. This is a net risk add to me in today's environment.

Third, overexposure to Houston, to any one area, is never a good thing, and Houston as a city and place to live is highly dependent on the energy sector. When that turns around (not if), that will drag things down with it.

Fourth , by the company's own calculation of its valuation, they're using extremely bullish rates given the macro we're in - I'm not comfortable with that, given that the cap rates we're seeing in the overall REIT markets and real estate markets are meaningfully different on an implied basis.

Perhaps most importantly though, when I invest in developers, I want firms with significant expertise and that do nothing else but that. Like Skanska ( SKBSY ), HochTief ( HOCFF ) and others. There's an outsized risk in developing properties compared to managing a stable real estate property that already exists. You can only really guesstimate long-term overhead patterns, and the volatility in these segments is only offset by being able to invest in the companies, as I did with Skanska, at extreme discounts.

Howard Hughes may be at a high discount on paper, but too much of that is what I'd call sugared valuation at too-different cap rates and with not enough risk considered from development.

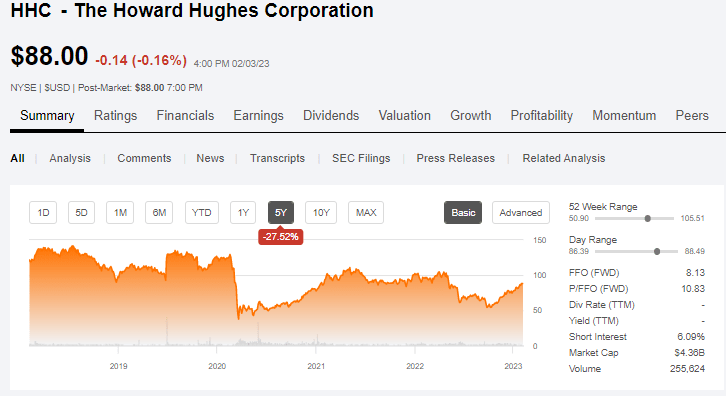

Because of the lack of a dividend and the B+ rating coupled with these risks, estimating where I would buy HHC is tricky. The company has been on an impressive run as of late, but this run was essentially just recapturing ground from the extreme low from back in October. On a 5-year basis, you're still very negative.

{kind=link}

In the end, I practice risk-averse investing whenever I can. I applaud my reader for being able to buy cheap and now hold HHC at a profit, but I would personally sell off my shares if I owned HHC at a profit. Based on where HHC values its own real estate and my own adjustments to that valuation, I would buy HHC at half of where management targets its NAV. This is to account for what I view as outsized risk, no dividend, and so forth.

That brings us to around $58/share, give or take a dollar.

Here's my thesis for Howard Hughes.

Thesis

- Howard Hughes is an interesting, MPC and office-based RE developer/company, but with a history of generating sub-par returns for over a decade. I do not see any potential clear catalysts for delivering value to its shareholders in the near term. For that reason, I'm fairly negative on the business.

- I would "BUY" this one at a severe discount to the company's own calculated NAV, coming to around $58/share, happy to hold until appreciation, all things being equal, and nothing changing.

- However, at anything beyond that, I'm at a "HOLD", and I would view this business as a clear "trim" target.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

With a B+ rating I can't call it qualitative, but it's fundamentally safe and well-run, being in Ackman's pocket (to some extent). However, it only fulfills one out of five criteria, making the company a "HOLD".

For further details see:

Howard Hughes: This Is A Tricky One, But I'm At 'Hold'