AGG - HPI: Some Good Things But High Leverage Is A Real Concern Right Now

2023-09-08 02:30:50 ET

Summary

- The John Hancock Preferred Income Fund offers a high yield of 9.84%, surpassing the fixed-income indices.

- The fund's recent performance has been disappointing, with a decline in share price and a negative total return.

- HPI's heavy weighting in the banking sector may be a concern for risk-averse investors.

- The fund has a high amount of leverage, so it could decline further if the Federal Reserve opts to increase rates again.

- The shares are currently trading at a premium to NAV, so the price seems a bit high.

The John Hancock Preferred Income Fund ( HPI ) is a fixed-income fund that has proven itself to be a very capable option for any investor who is seeking to earn a high level of income from their portfolios. This is immediately evident in the fund's current 9.84% yield, which is vastly superior to the 6.95% yield of the ICE Exchange-Listed Preferred & Hybrid Securities Index ( PFF ) as well as the 1.45% yield of the S&P 500 Index ( SPY ). In fact, the John Hancock Preferred Income Fund's current yield is sufficient to allow a $1 million investment to produce $98,400 in annual income, which is easily enough for most retirees to live a very comfortable life anywhere in the United States when combined with Social Security income.

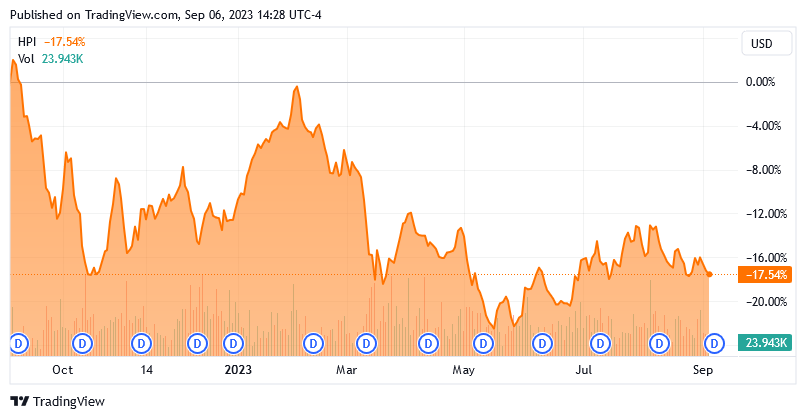

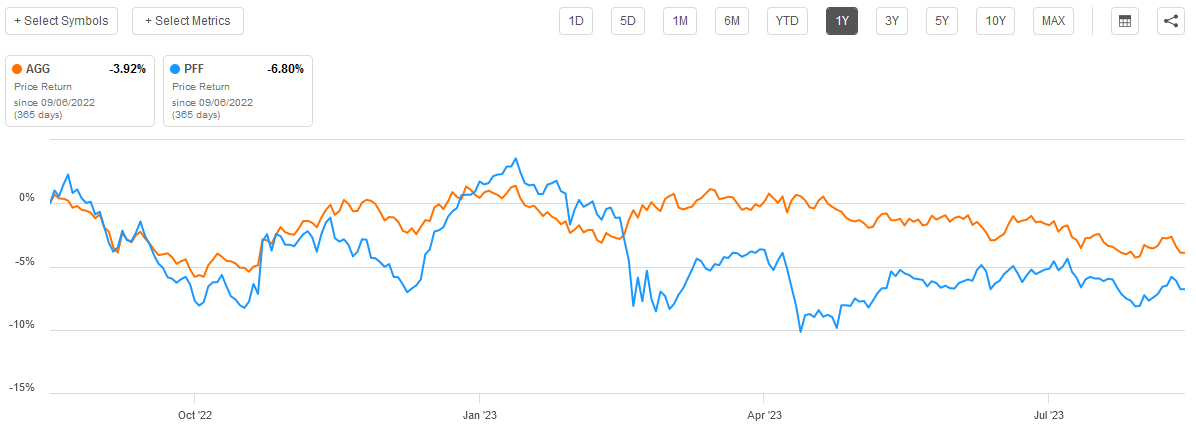

Unfortunately, the fund's recent performance leaves a lot to be desired, which explains why the yield is so much higher than in our past discussions about this fund. Over the past year, the John Hancock Preferred Income Fund has handed investors a share price decline of 17.54%:

{kind=link}

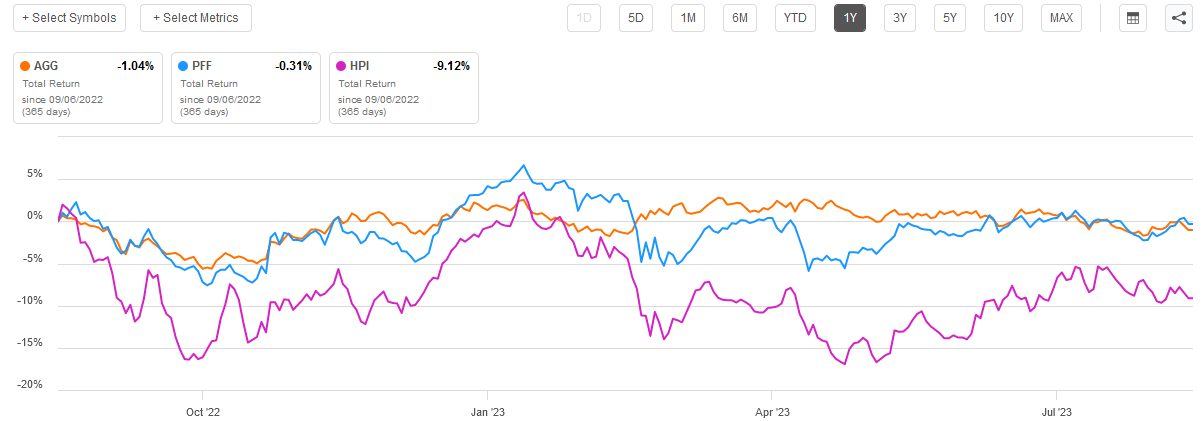

This was more than sufficient to offset the high yield, and as a result, the fund's total return was a disappointing -9.12% over the period:

{kind=link}

This does not necessarily mean that an investment in the fund does not make sense right now, but it does put things in perspective. We should not just get overly excited about the high yield and ignore other important factors. I last discussed this fund back in April, and did see some positive qualities in it but concluded that the fund was a very expensive way to obtain a high yield. The fund's price has improved somewhat since then, but it is still trading for a fairly high price so it is advisable to be cautious.

About The Fund

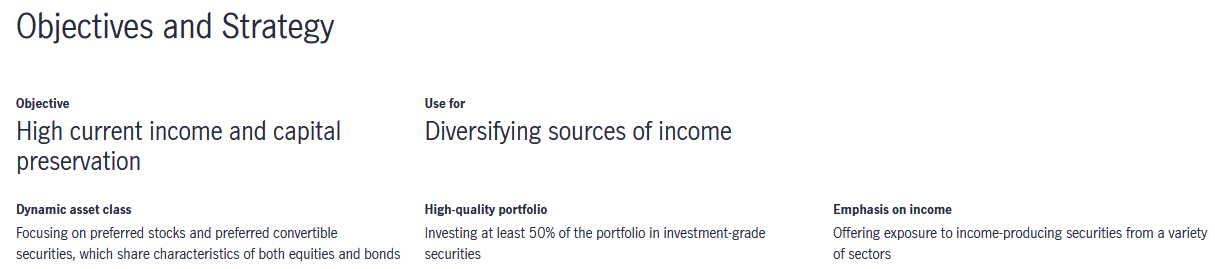

According to the fund's website , the John Hancock Preferred Income Fund has the objective of providing its investors with a very high level of current income while still preserving its principal. This is a pretty common objective that is possessed by many fixed-income funds. However, we normally see such an objective with bond funds. As the name of this fund suggests, the John Hancock Preferred Income Fund is not a bond fund. In fact, its portfolio consists of 76.71% preferred stocks:

CEF Connect

We do still see some exposure to bonds and even common stocks, but the overwhelming majority of the fund's assets are invested in preferred securities. This does fit pretty well with the website's description of the fund's objectives and strategy:

{kind=link}

It is somewhat surprising that the fund is placing an emphasis on the preservation of capital with a preferred stock portfolio. A bond fund can generally make such a claim, as anyone who holds a bond to maturity will receive the face value of the bond at that time. Thus, unless an investor purchases a bond with a negative yield-to-maturity, the investor is guaranteed not to lose money unless the bond issuer defaults. This is not the case with preferred stocks though, as preferred stocks do not have maturity dates. Thus, depending on the price that the investor paid to purchase the preferred stock, it might not be possible to preserve the value of the principal. However, it is certainly not common to lose money on preferred stock if the security is held for long enough.

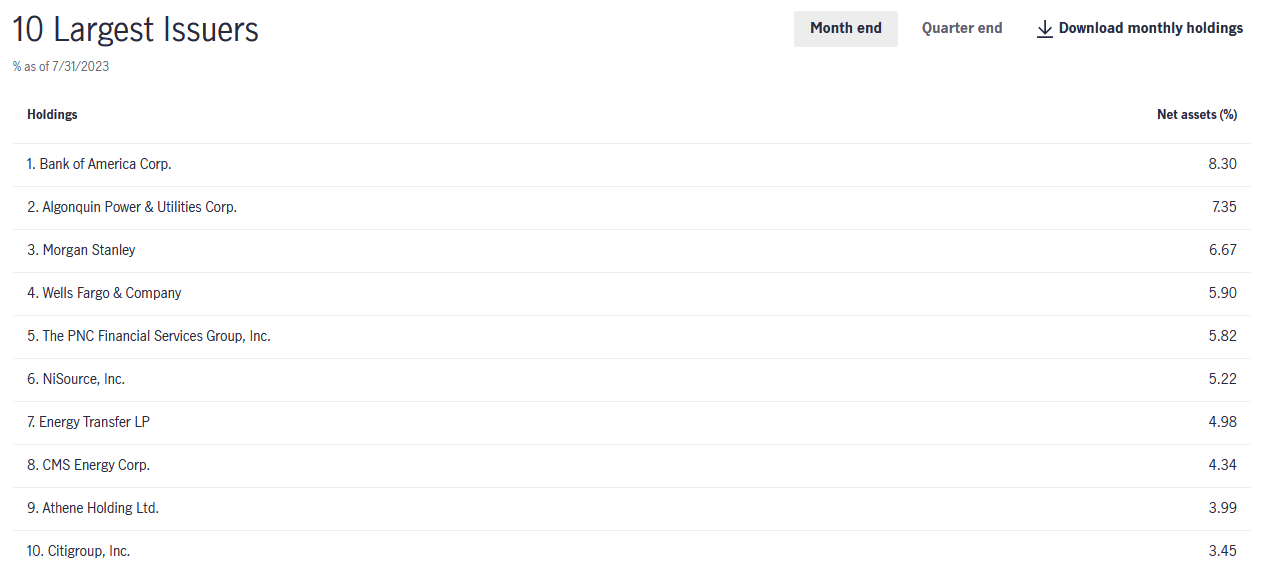

In my last article on this fund, I noted that the fund was heavily weighted to the banking sector. This continues to be the case today. We can see this by looking at the largest holdings in the fund's portfolio:

{kind=link}

Curiously, the fund sponsor does not actually provide a chart detailing its holdings by sector. The most that can be found on either the website or the fact sheet is the above chart which lists a number of major banks among the fund's largest positions. However, the fund's semiannual report does include such a chart, reproduced here:

John Hancock Investments

However, this chart is as of January 31, 2023, which is much older than the largest positions list. As such, we do not know the exact weighting of the financial sector, but it is probably still more than half of the fund.

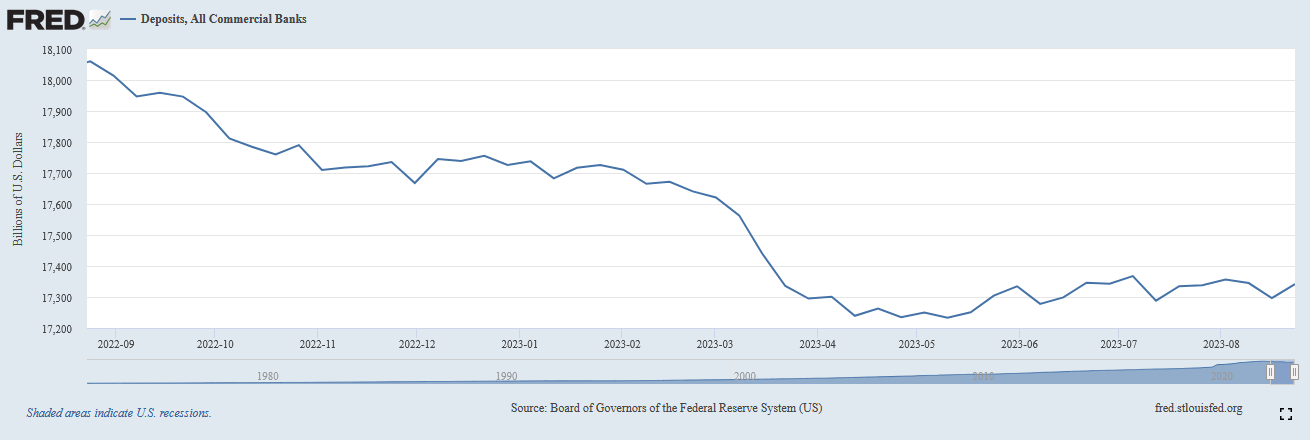

The fact that the fund's portfolio is heavily weighted to the financial sector could be concerning to some risk-averse investors. After all, we did see three of the largest bank collapses in American history earlier this year. The news with respect to the sector has generally calmed down since the Federal Government and the Federal Reserve took some actions to improve its overall stability, but deposits at commercial banks have been declining over the past twelve months:

{kind=link}

That is certainly not the best position for the sector to be in as deposits are a source of low-cost funding for banks and the steep reduction in deposits could make it harder for them to weather additional runs or similar events. Nonetheless, the banking industry tends to be the beneficiary of enormous amounts of government support when it runs into trouble, and it seems highly unlikely that all of the banks listed in the fund's largest positions listed above will suffer severe enough problems to cause significant losses to the preferred stockholders. It would take an event similar to the Great Financial Crisis back in 2008 to cause such severe losses, and while this might be possible, I do not know of any analyst who is predicting such an event in the near future. Overall, this fund is probably reasonably safe from default risk.

Interest-Rate Risk

The biggest risk faced by this fund is interest rates. I mentioned this in my previous article on the fund:

The market prices of these securities (preferred stocks and bonds, per the fund's largest holdings) vary with interest rates. It is an inverse relationship, so when interest rates increase, fixed-income prices decrease, and vice versa."

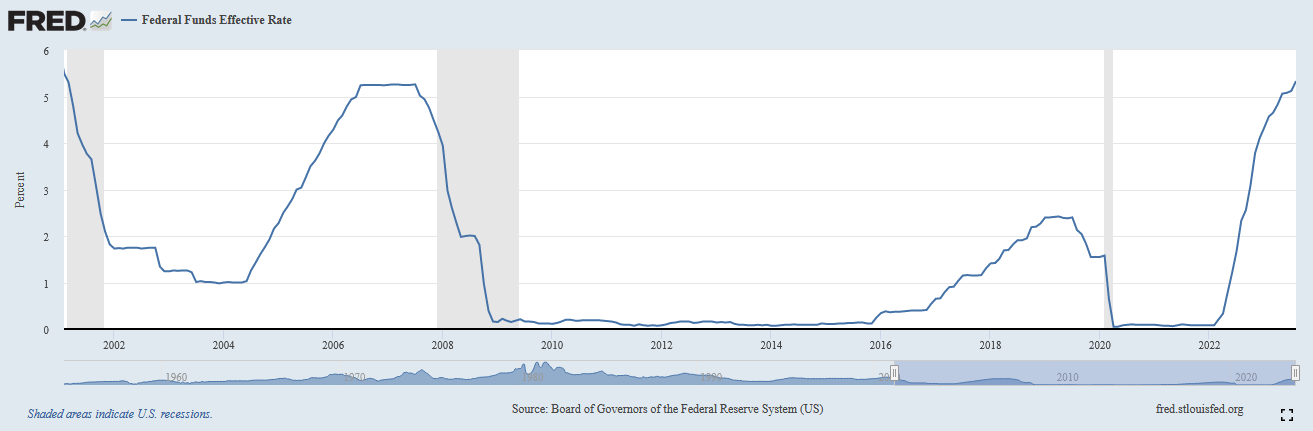

The Federal Reserve has been aggressively raising interest rates since March of 2022, although it has slowed down recently. Nevertheless, the effective federal funds rate is now at 5.33%, which is the highest level that has been seen since 2001:

{kind=link}

This aggressive series of rate hikes over the past year is the event that has been devastating the fixed-income markets for a good portion of the past year. As we saw in the introduction to this article, the John Hancock Preferred Income Fund's share price is down by 17.54% over the past year. It is hardly alone here, as the Bloomberg U.S. Aggregate Bond Index ( AGG ) and the ICE Exchange-Listed Preferred & Hybrid Securities Index were also both down over the period:

{kind=link}

In fact, it is now being projected that the ten-year Treasury bond may end 2023 at a lower level than it began the year. If that happens, it would be the first time since the American Revolution that the ten-year Treasury delivered three straight years of losses.

There is a real chance that this will happen. Chairman Powell suggested in his Jackson Hole speech that the Federal Reserve may hike rates further this year, and some analysts are projecting a 25-basis point hike later this month. That is a significant change from the market's belief that the Federal Reserve would start cutting rates this year, which was the prevailing belief the last time that we discussed this fund. If the central bank does indeed raise rates further, it can be expected to push down the fund's share price further.

Total Performance

As noted in the introduction, the John Hancock Preferred Income Fund has a much higher distribution yield than either the preferred stock or the U.S. aggregate bond indices. That is very important as it has a significant impact on overall returns. After all, a large enough distribution can offset losses due to a share price decline. I have pointed this out in numerous previous articles on other fixed-income closed-end funds. The most important thing is the total return that an investor will receive.

Unfortunately, the John Hancock Preferred Income Fund fell too much over the past twelve months for its high yield to work to its advantage. As we can see here, the fund had a much worse total return than either of the two major fixed-income indices:

{kind=link}

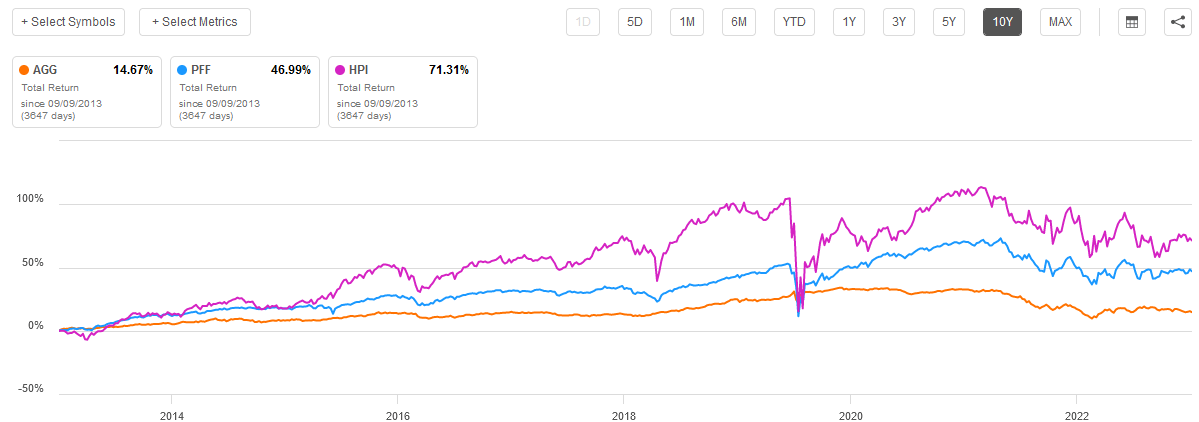

This problem does correct itself over the long-term though, as the fund manages to substantially outperform both funds over the trailing ten-year period:

{kind=link}

During both the trailing three-year period and the trailing five-year period, the John Hancock Preferred Income Fund managed to outperform the bond index but failed to match the performance of the preferred stock index. This is mostly because the preferred stock index has a higher yield than the bond index, so it took the John Hancock Preferred Income Fund much longer to compound sufficiently to overtake it.

It is important to note that the above does assume that distributions are being reinvested, which many income-focused investors may not want to do. After all, it is hard to reinvest a distribution if you want to spend it to support your lifestyle. For the most part, the above order should generally be true though. The preferred stock index will probably be the best bet over anything but an extremely long time frame, especially because rising interest rates will probably cause the John Hancock Preferred Income Fund to fall much more than indices in such an event. The reason for this is that the closed-end fund is employing leverage.

Leverage

As just mentioned, the John Hancock Preferred Income Fund employs leverage as a strategy intended to boost its effective yield. I described how this works in my last article on the fund:

Basically, the fund borrows money and then uses that borrowed money to purchase preferred stocks and bonds. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses."

Notice the final sentence in that description and consider the fund's market performance over the past year. The fund's use of leverage was probably a big reason why this fund declined so much more than the indices over the trailing twelve-month period. It is also why we should have some concerns that further interest rate hikes will cause this fund to decline more rapidly than the indices. As of the time of writing, the John Hancock Preferred Income Fund has a leverage ratio of 39.43%, which is a bit higher than we really want to see from a risk-reward standpoint, too.

Distribution Analysis

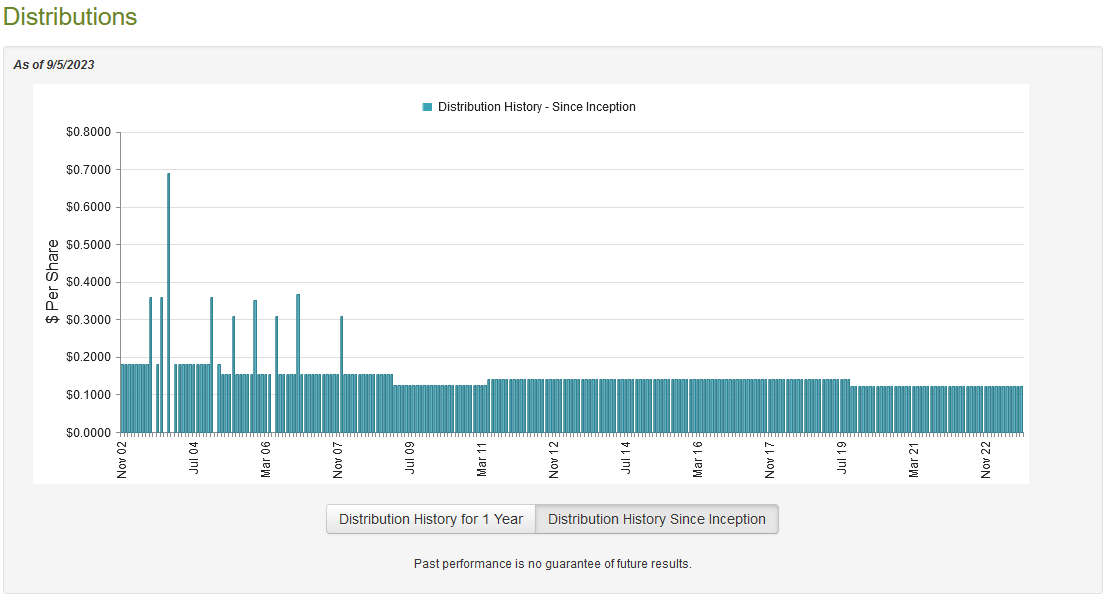

As mentioned earlier in this article, the John Hancock Preferred Income Fund has the objective of providing its investors with a very high level of current income. In order to accomplish this, the fund has assembled a portfolio that consists mostly of preferred stocks, which tend to have fairly respectable yields. The fund then applies a layer of leverage to boost the effective yield of the portfolio. As is the case with all closed-end funds, the John Hancock Preferred Income Fund then pays out all of its investment returns net of expenses to the shareholders. As such, we might expect that this results in the fund having a fairly high yield itself. That is certainly the case, as the fund pays a monthly distribution of $0.1235 per share ($1.482 per share annually), which gives it a 9.84% yield at the current price. This fund has been quite consistent with its distribution over the years, although it has changed it from time to time:

{kind=link}

As we can see, the fund's distribution has been stable since October 2019. That makes this one of the only fixed-income funds that has not been forced to cut its distribution over the past year. However, that could be a point of concern since it does not make a lot of sense for this fund to have far more consistency than its peers. It is possible that the fund is paying out more than it is actually generating off of its portfolio. We do not want that to be the case since that will almost certainly result in a distribution cut at some point in the future. A distribution cut will naturally reduce our incomes and probably cause the fund's share price to decline. Let us investigate this.

Unfortunately, we do not have an especially recent document to use for the purpose of our analysis. As already mentioned, the fund's most recent financial report is its semiannual report that corresponds to the six-month period that ended on January 31, 2023. As such, this report will not include any information about the fund's performance over most of this year. That is a shame as this year has generally been much better for the fixed-income market than 2022 was, which is partly because the market spent half of the year expecting that the Federal Reserve would quickly get inflation under control and be able to cut rates. This has proven to not be the case, but the fund still had an opportunity to generate some capital gains from this belief. Those capital gains could have gone a long way to support the distribution, but unfortunately, we will have to wait a few more weeks until the fund releases an updated report to find out how successful it was at this task.

During the six-month period, the John Hancock Preferred Income Fund received $14,607,549 in dividends and $8,860,436 in interest from the assets in its portfolio. When we net out the money that the fund had to pay in foreign withholding taxes, we get a total investment income of $23,418,045 for the period. The fund paid its expenses out of this amount, leaving it with $14,968,310 available for shareholders. That was, unfortunately, not nearly enough to cover the $19,559,824 that the fund actually paid out in distributions. This is concerning since we usually like a fixed-income fund to be able to fully cover its distributions out of net investment income.

With that said, the fund did have some capital gains during the period that were able to make up for the difference. It reported net realized gains of $5,042,419 but this was more than offset by $18,732,287 net unrealized losses. Overall, the fund's net assets declined by $17,345,986 after accounting for all inflows and outflows during the period. The fund did manage to cover its distributions out of net investment income and net realized gains, which is a good sign. The fact that its net assets declined is not ideal, but overall, it did manage to cover the distribution. Hopefully, the fund was able to deliver a better performance so far in 2023 as the decline in net assets will make it harder for the fund to sustain its distribution going forward if it does not manage to undo some of those net unrealized losses.

Valuation

As of September 5, 2023 (the most recent date for which data is available as of the time of writing), the John Hancock Preferred Income Fund has a net asset value of $14.94 per share but the shares trade for $15.01 each. This gives the fund's shares a 0.47% premium on net asset value at the current price. This is quite a bit better than the 3.40% premium that the fund's shares have averaged over the past month, but it is still a premium. I generally do not like to buy any fund at a premium, especially one that is highly exposed to interest rate risk like this one. It might be best to wait until the shares trade at a discount before buying in.

Conclusion

In conclusion, the John Hancock Preferred Income Fund appears to have some things going for it. In particular, the fund's yield is very attractive right now and the portfolio is invested in fixed-income assets, which tend to be less volatile than common stocks. Unfortunately, its high leverage exposes it to a high risk of losses in the event of another interest rate hike and such an event cannot be ruled out. In addition, the fund is trading at a premium to the intrinsic value of its shares. At least it did manage to cover its distribution during the second half of 2022, which is more than many fixed-income funds can claim. There are certainly worse funds out there.

For further details see:

HPI: Some Good Things, But High Leverage Is A Real Concern Right Now