HQH - HQH: Deep Discount Presents An Opportunity

2023-07-03 15:45:45 ET

Summary

- Tekla Healthcare Investors, a closed-end fund, focuses on the biotech subsector of healthcare, leading to potential volatility but also potential for high returns.

- The fund's deep discount presents an opportunity for investors after a down year for biotech, but a dollar-cost averaging approach could be a better approach due to volatility.

- HQH's managed distribution plan provides investors with a distribution yield while waiting through biotech cycles, with long-term capital gains making up the bulk of the distribution classification.

Written by Nick Ackerman, co-produced by Stanford Chemist. A version of this article was originally published to members of the CEF/ETF Income Laboratory on June 19th, 2023.

Tekla Healthcare Investors ( HQH ) is a closed-end fund focused on investing in the healthcare space. However, it isn't investing in the more traditional healthcare names that most people might be familiar with. Instead, they invest in the more exciting area of the market, the biotech subsector of healthcare. That can lead to more general volatility but also more potential for upside reward.

It has been quite some time since we've touched on HQH. During this time, the fund hasn't performed well.

HQH Performance Since Prior Update (Seeking Alpha)

Biotech hadn't been too hot of a performer through most of this time, and that has much to do with it. However, the fund's discount widening significantly during this time was also a major factor. The last time we covered this fund nearly two years ago, the fund was trading almost at par with its NAV. Today, a 15%+ discount presents a much better valuation to consider investing in this name.

In 2021, CEFs were at historically tight valuation levels, with shallow discounts seen across the space. That's the opposite today as we are now seeing historically wide discounts. So it wasn't necessarily specific to HQH what we've seen in the CEF market.

More recently, it was announced that abrdn intends to acquire Tekla Capital Management to start its own healthcare division. With that would come HQH and the other three Tekla funds. The proposal needs to be approved by the Boards and shareholders for abrdn to become the new investment manager; the actual current managers are expected to stay the same, as well as the investment policies of each fund stay the same. For that reason, I don't see it being too much of a change overall. If anything, being a part of a larger organization might allow the Tekla managers access to more tools and connections. abrdn is the third-largest closed-end fund manager in the world.

The Basics

- 1-Year Z-score: -1.52

- Discount: -15.41%

- Distribution Yield: 9.22%

- Expense Ratio: 1.19%

- Leverage: N/A

- Managed Assets: $985.9 million

- Structure: Perpetual

HQH's investment objective is "to provide long-term capital appreciation." They will attempt to achieve this through "investments in companies in the healthcare industry believed to have significant potential for above-average long-term growth. Selection will emphasize the smaller, emerging companies with a maximum of 40% of the Fund's assets in restricted securities of both public and private companies."

While they have the flexibility to invest in restricted private investments, it hasn't been an overly emphasized area of their portfolio. At least it hasn't been an emphasis since I've been looking at HQH. The latest report puts the weighting at 8.58% of their portfolio being allocated to investments classified as restricted, with level 3 security classifications at 7.72% of total assets. Level 3 security holdings can often add some skepticism to valuations, but with a minor allocation, it wouldn't appear to be a significant factor for this fund.

Additionally, this fund doesn't employ leverage. With interest rates rising, that's been positive that HQH is non-leveraged, as borrowings for other CEFs are now reaching the level where they don't really make sense. Between the cost of the borrowings and expected returns, there is no or very limited expected upside in most cases. For HQH, we don't have to worry about that. Given the biotech industry can be volatile on its own and HQH has to deal with discounts/premiums, that will leave HQH volatile enough without adding leverage to exacerbate it.

Performance - Attractive Discount, Generally Volatile In Nature

Biotech goes through cycles of booms and busts. 2021 was definitely one of those boom years, but that was followed by a big bust through 2022.

YCharts

These sorts of volatile moves in the underlying portfolio can be seen with HQH, as it, too, carries some significant volatility. The performance can be somewhat dampened by its more traditional healthcare names. In looking at HQH's price alone, we can see that it is down, but when including the fund's distribution, we get positive returns in the last decade.

YCharts

However, the main takeaway is that when to enter into the biotech space can be important. It will do a lot to determine whether HQH is a successful investment or not. On the chart below, there are several places one could invest, and it would have resulted in a loss or minimal results.

Helping to make HQH a more interesting pick for biotech exposure in one's portfolio, the fund's deep discount also presents an opportunity after biotech hit its bust cycle. HQH's discount seems to similarly go through cycles, and right now, it is out of favor. This has historically presented the best opportunity to invest in the fund while it's in a trough. However, we can also see that the fund has dropped to even wider discounts during recessions. So being cautious and dollar-cost averaging could prove to be a smart move as well.

YCharts

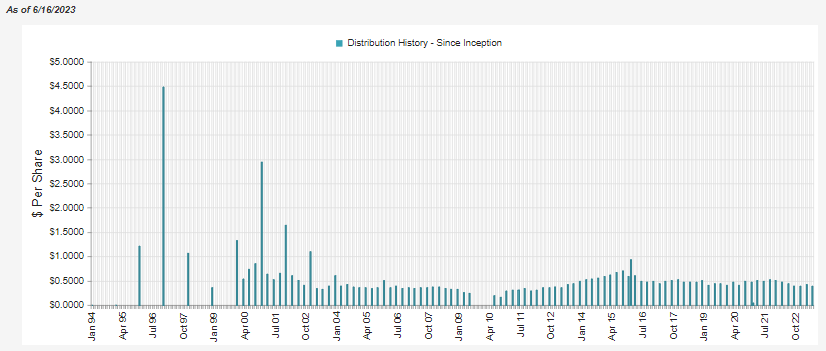

Distributions - Managed Plan

Smaller biotech companies don't generally offer yields. This is generally because they can be unprofitable or are just focused on growth only. The larger, more established biotech companies can offer yields, but they have relatively short-lived dividend histories.

Another reason why biotech companies can have relatively short-lived histories and not make it to mature dividend-paying phases of their lives is that they get acquired. As a recent example, Pfizer ( PFE ) is currently looking to acquire Seagen ( SGEN ). However, that merger is currently up in the air on potential antitrust concerns.

The main point is that biotech companies aren't necessarily what investors would look for as a yield play. With HQH, there is a focus on its distribution. So one can get paid to wait through the cycles. This distribution is based on the fund's NAV per share on the previous distribution payment date, and it works out to 2% of the NAV.

This creates a variable distribution that changes from quarter to quarter. This can be a positive as when times are bad; they are distributing less. Reducing the fund's distribution means less capital destruction relative to if they just maintained a flat distribution no matter what. Conversely, when times are good, investors receive more of that upside.

{kind=link}

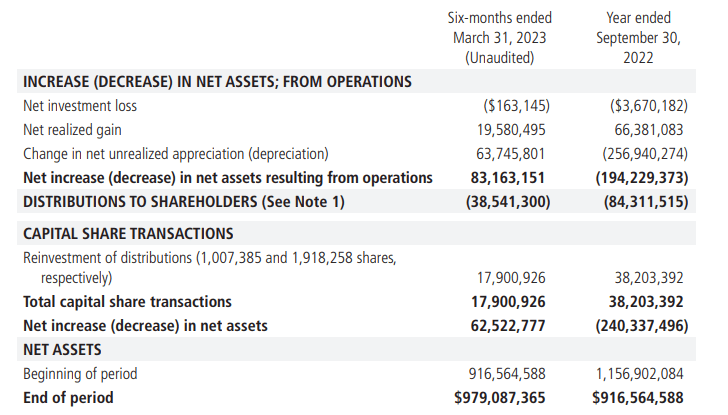

To fund that distribution, HQH will require significant capital gains. Of course, as discussed, the underlying portfolio pays out very little in the way of yield. That leaves net investment income for HQH at a loss.

{kind=link}

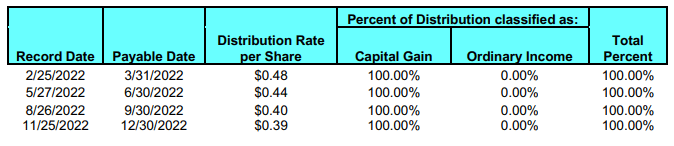

For 2022 tax purposes , the entire distribution was classified as long-term capital gains. That reflects what would be expected and has generally been the case for years, with long-term capital gains making up the bulk of the classification for the distribution. That could make it appropriate for a taxable account as LTCG are taxed more favorably than ordinary income rates.

{kind=link}

This is one of those funds that will show return of capital classifications in their section 19a, but then it gets reclassified. As an example, their September 2022 notice showed that ROC was 56% of the distribution classification for the fiscal year, which we can see all came out actually to be classified as LTCG. HQH is a good reminder of why I don't generally pay attention to the section 19a reports. It's more important to watch the NAV over time.

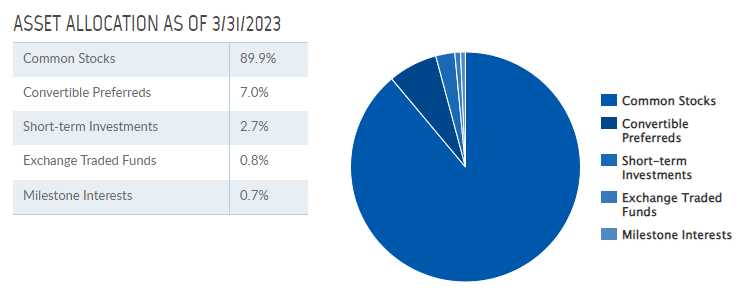

HQH's Portfolio

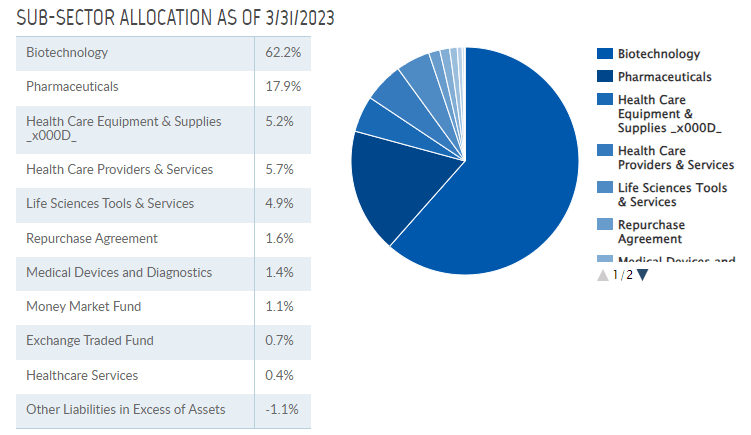

Just over 62% of the portfolio is invested in the biotechnology sub-sector of healthcare. Pharmaceuticals are the next largest allocation at a meaningful ~18%. From there, sub-sector allocations greatly diminish in weightings for HQH to fairly insignificant amounts.

{kind=link}

The fund is largely invested in the equity positions of the companies they invest in, but they also carry some convertible preferred exposure.

{kind=link}

Turnover in the fund for the last couple of years was fairly active. In the latest six-month report, we have a turnover rate of 19.99%. However, in fiscal 2022 and 2021, we see turnover at 41.21 and 69.19%, respectively. Despite this, the overall general positioning of the fund is the same as it was when we last visited this fund two years ago. At that time, biotech made up 60.9%, with pharma making a 14% weighting. Equity positions comprised 93.8% of the portfolio at that time.

Even when looking at the top ten holdings on the fund, we see plenty of the same names we saw two years ago. However, potentially worth noting is that the top ten weightings have seen an overall increase in their allocation. It had previously been 35.2% of the portfolio and has now shifted higher to 44.3% of the fund's invested assets.

HQH Top Ten Holdings (Tekla)

Gilead Sciences ( GILD ) was the top holding then, and it is now. It saw its weighting increase from 5.4% to command a more significant 6.9% weighting. Regeneron Pharmaceuticals ( REGN ) had also previously been a holding in the fund. It climbed significantly from its previous allocation of 3.2% to 6.8%. That took it from the 8th position in the fund to now being right behind GILD in second place.

GILD and REGN are sizeable biotech companies - as are most of the top holdings for HQH dominated by large-cap companies. GILD carries a nearly $100 billion market cap, with REGN at around an $84 billion market cap.

GILD sports an attractive and growing dividend, one of those fairly rare biotech companies that have matured.

{kind=link}

That said, we can see that the share price has essentially stagnated for GILD investors. This has taken place as earnings have essentially flatlined, though it could be positive from the rapid declines in earnings seen after 2015.

GILD Earnings History and Forward Estimates (Portfolio Insight)

{kind=link}

The share price performance between GILD and REGN has clearly favored REGN since our last update. In fact, REGN has been the best performer of this group of names during this time. Moderna ( MRNA ) had previously provided an outsized return thanks to the Covid boost, but it has since given those gains up.

YCharts

The strong performance from REGN would help show why they've been able to climb up in terms of HQH's top ten holdings. However, they've also upped their position in REGN during this time. They previously held 74,459 shares of REGN, but the latest report shows an increase to 81,285.

During this same time, HQH actually decreased its GILD position from 939,446 shares to 815,795. ILMN has been the worst performing during this time, which was previously the second-largest holding of the fund and had slipped to the 5th largest now. Helping to maintain the weighting to some degree to offset the sizeable declines was an increase in the number of shares held. They went from 137,115 shares to 155,689.

Conclusion

HQH is at an attractive discount. The heavy exposure to biotech can make HQH more volatile, as this space has traditionally gone through its own boom and bust cycles. However, after a down year for biotech combined with that deep discount, HQH looks like a much more interesting play these days. Since biotechs can be volatile, using a dollar-cost averaging approach could be more prudent for patient investors to build a position over time.

For further details see:

HQH: Deep Discount Presents An Opportunity