HQH - HQH: Discount To NAV Offers Attractive Entry Opportunity

2023-11-15 17:43:39 ET

Summary

- abrdn Healthcare Investors is a closed-ended fund focused on the global biotech & healthcare sector boasting a 10% dividend yield.

- The recent acquisition of Tekla Capital Management's funds by abrdn will not change the operations and strategies of HQH.

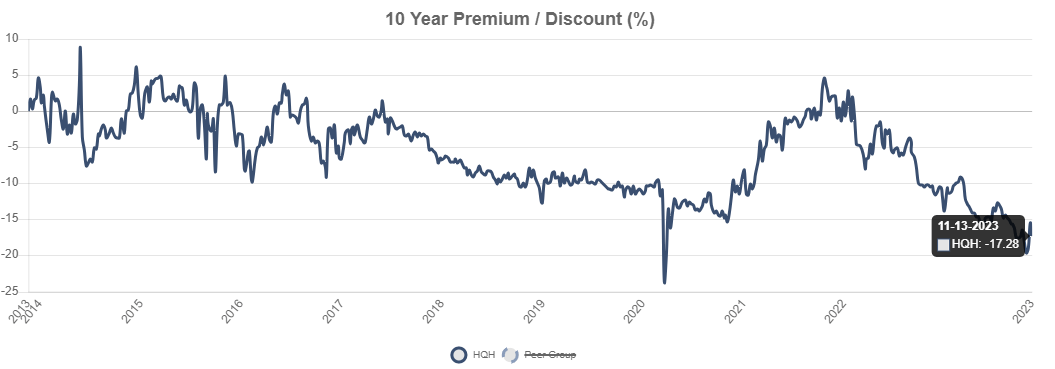

- HQH is currently trading at a 17.28% discount to NAV, indicating a potential 10% upside to historical averages, making it an attractive investment opportunity.

Overview

abrdn Healthcare Investors ( HQH ) is a closed ended fund with a focus on the global healthcare sector. The main focus here are biotechnology, medical devices, and pharmaceuticals. The fund's primary objective is to achieve long term capital appreciation by primarily investing in equity securities of U.S. and foreign companies engaged in the healthcare industries. I like HQH because it focuses on companies with potential for above average growth in revenues and earnings.

On October 27th Tekla Capital Management's funds were acquired by abrdn. Thankfully, things remain unchanged for holders of HQH and will continue to operate the same going forward. It was confirmed that the fund's objective and strategies shall remain the same. Lastly, HQH has an expense ratio of 1.19%.

All of the Tekla Funds that have been affected by the acquisition / name change are:

- abrdn Healthcare Investors ( HQH )

- abrdn Life Sciences Investors ( HQL )

- abrdn Healthcare Opportunities Fund ( THQ )

- abrdn World Healthcare Fund ( THW )

This CEF is highly attractive at the moment because of the high dividend yield of 10%, a portfolio of quality biotech and healthcare companies, and the current discount to NAV (Net Asset Value) that sits higher than the historical average.

Discount To NAV

Depending on the structure, CEFs become attractive when trading at a discount to NAV for several reasons. Firstly, purchasing the fund at a discount allows investors to acquire the underlying assets at a lower cost than their market value, providing a potential for capital appreciation if the discount narrows. With the case of HQH, the discount spread is larger than the historical average.

At the moment, HQH is trading at a 17.28% discount to NAV compared against the 3-year average discount of only 7%. This could indicate a 10% upside to get back to the levels that have been common in the past. Looking back, we can see that the price traded at a premium to NAV between 2013 and 2018. The price briefly traded at a premium in 2021 but has been slumped ever since because of the poor performance of biotech.

{kind=link}

Portfolio Structure

The top ten holdings make up 42% of the fund's portfolio and all of the holdings are within the biotech/healthcare sector. There are a total of 141 holdings and the latest portfolio turnover total sits at 41%.

The top ten holdings are as follows:

| Vertex Pharmaceuticals Incorporated ( VRTX ) |

| 7.94% |

| Regeneron Pharmaceuticals, Inc. ( REGN ) |

| 7.65% |

| Amgen, Inc. ( AMGN ) |

| 7.45% |

| Gilead Sciences, Inc. ( GILD ) |

| 5.81% |

| Biogen, Inc. ( BIIB ) |

| 3.80% |

| AstraZeneca ( AZN ) |

| 3.53% |

| Alnylam Pharmaceuticals Inc ( ALNY ) |

| 2.14% |

| AbbVie ( ABBV ) |

| 1.84% |

| Illumina Inc ( ILMN ) |

| 1.76% |

| BioMarin Pharmaceutical Inc ( BMRN ) |

| 1.62% |

Taking a quick analysis of the top holdings, Vertex Pharma ( VRTX ) recently reported strong earnings and currently has a revenue growth of 11% year over year. Regeneron Pharma ( REGN ) recently experienced a rating upgrad e from Raymond James to Outperform base d on their strong Q3 results. The price target of REGN currently predicts a 14% upside from the current level. Lastly, Amgen ( AMGN ) is a strong dividend payer with 11 years of consecutive dividend raises and an annual yield over 3%. AMGN has an excellent 5 year dividend CAGR at 10% as well. I point these examples out to reinforce that the funds in HQH's portfolio are solid and highly profitable companies.

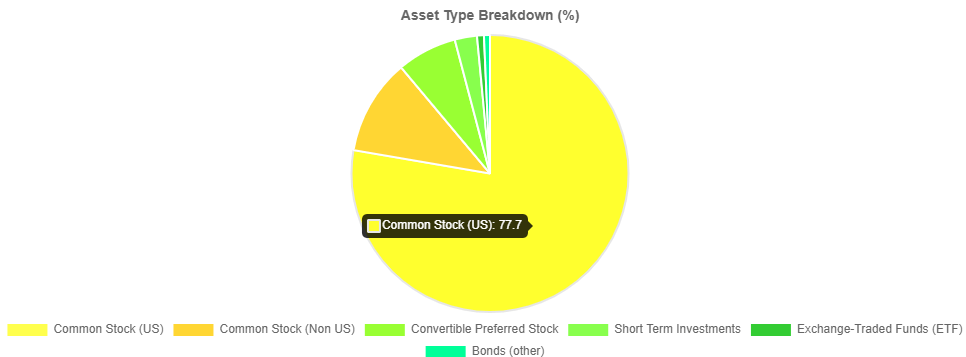

The fund is comprised of 77% US common stock, 11% non-US common stock, and 7% common preferred stock. Most of the funds exposure is to U.S related assets but you do have a small percentage of exposure to the United Kingdom (4.52%), China (0.96%), and Germany (0.71%).

{kind=link}

Forward Looking - Biotech

The recent underperformance of HQH can be attributed to the poor performance of biotech. In addition, the previous upward movement in interest rates also had an effect on the sector. We can see that HQH, as well as similar funds, have all been suppressed. The overall Biotech sector ( XBI ) is down nearly 19% while HQH has held up a bit better at only down 11%.

I believe that the biotech sector's sensitivity to interest rate changes arises from reliance on extended timelines and external financing. With operations focused on future earnings potential, rising interest rates increase discount rates, diminishing present valuations. Hence, the selloff we've been experiencing since the peak two years ago. This is why I believe the discount to NAV offers an attractive opportunity to capitalize on the disconnect here. The sector's heavy reliance on external financing makes it susceptible to elevated borrowing costs, especially as many biotech companies operate at a loss in the early stages of new developments and research.

However, I do think that we will see the tide turn very soon. We've recently seen the Fed decide to leave rates unchanged twice now. This could indicate that the lowering on interest rates are around the corner since we also see that core inflation rose at the slowest pace since Sept 2021. This shift in interest rates will create a better environment for the biotechnology sector. So, my verdict is to add to my position to capitalize on the recovery play here while the dividend yield sits at a large 10%.

Dividend

As of the latest declared dividend, the yield is slightly over 10%. Something to be aware of is that the dividend is variable and has frequently changed over the years. The dividend was raised by 7.7% at the beginning of the year in February and was subsequently cut on two different occasions shortly after that. The dividend was then cut by 4.8% in May, followed by another cut of 5% in November.

HQH employs a variable strategy, distributing 2% of its NAV on a quarterly basis. This approach ensures that payouts adjust in line with the fund's NAV, creating a safeguard against capital erosion during market downturns. In times of reduced NAV, investors experience lower distributions which is what we have been experiencing. Conversely, when NAV rises, HQH automatically increases distributions. This proactive strategy eliminates the need to anticipate market timing or hope for raises, offering a straightforward strategy.

This is why I believe entry here to capitalize on the sector's recovery would be beneficial. The beauty about this 10% yield is that it essentially means that we can get paid to wait out this cycle. I plan to hold HQH as a strong income generator for my portfolio and will be adding more at these levels to take advantage of a higher yield.

Takeaway

Abrdn Healthcare Investors ((HQH)) presents an intriguing investment opportunity in the biotech/healthcare sector following the acquisition of Tekla Capital Management. Thankfully, HQH remains unchanged in its operations and investment strategies. The current discount to NAV, trading at 17.28%, signals a potential 10% upside to historical averages.

The top holdings, dominated by solid biotech and healthcare companies, demonstrate promising financial performances, reinforcing the fund's stability. Despite recent underperformance attributed to the biotech sector's sensitivity to interest rate changes, a potential recovery is anticipated, especially with the recent decision by the Fed to keep rates unchanged.

The variable dividend strategy, distributing 2% of NAV quarterly, offers a transparent approach that adjusts to market conditions, providing a cushion against capital erosion. With a dividend yield exceeding 10%, HQH not only offers income but also positions investors to capitalize on the sector's recovery. This, combined with the anticipation of favorable interest rate shifts, makes HQH an attractive prospect for investors seeking both income and growth.

For further details see:

HQH: Discount To NAV Offers Attractive Entry Opportunity