PIAIF - HSBC: A Great Bank Investing In Uninvestable China

2023-06-10 09:00:00 ET

Summary

- HSBC's expansion into China exposes the bank to significant risks due to the country's autocratic government and fragile economic conditions.

- The bank's current financials and valuation are attractive, but its long-term performance may be negatively impacted by its China strategy.

- I think HSBC should consider selling its China and Hong Kong operations to mitigate risks and focus on growth in other Asian markets.

Thesis

HSBC ( HSBC ) ( HBCYF ), the largest European bank by assets, is attempting to (re)expand into Asia, and ride the wave of growth as economies there begin to develop and modernize. However, HSBC is pursuing growth in China, an autocratic country with a temperamental attitude towards domestic business operations and risky domestic economic conditions. HSBC's determination to expand there, combined with the Chinese government's mandates for operating in China and the risks this comes with, means that the bank will likely have a rude awakening as the consequences of its investments in China begin to be felt in the coming years.

Financials

I will dive into HSBC's financials here, but first, a breakdown of basic bank financials in general.

Basic Bank Financials

Most banks make money not by creating and selling physical products, but by collecting fees charged for their services, and from interest paid on their loans. Banks use money from the people who store their funds with them (depositors) and loan this capital out to people who want get bank loans (borrowers), and the banks in turn request that those people pay it back for a certain percentage of interest, or interest rate.

One reason banks do this is because banks also pay interest to the depositors for holding their money, so banks prefer to lend the deposited funds out as loan principle so that the deposits/loans are collecting borrowers’ interest to pay the bank, while interest is being paid by the bank to the depositors. Ideally, the bank pockets the difference in interest payments (this of course assumes that the banks are charging higher interest rates for loans they give than the rates for storing funds in its accounts, or is charging fees large enough or frequently enough to make up the difference). These are the basic dynamics at play for how banks make money.

HSBC's Financials

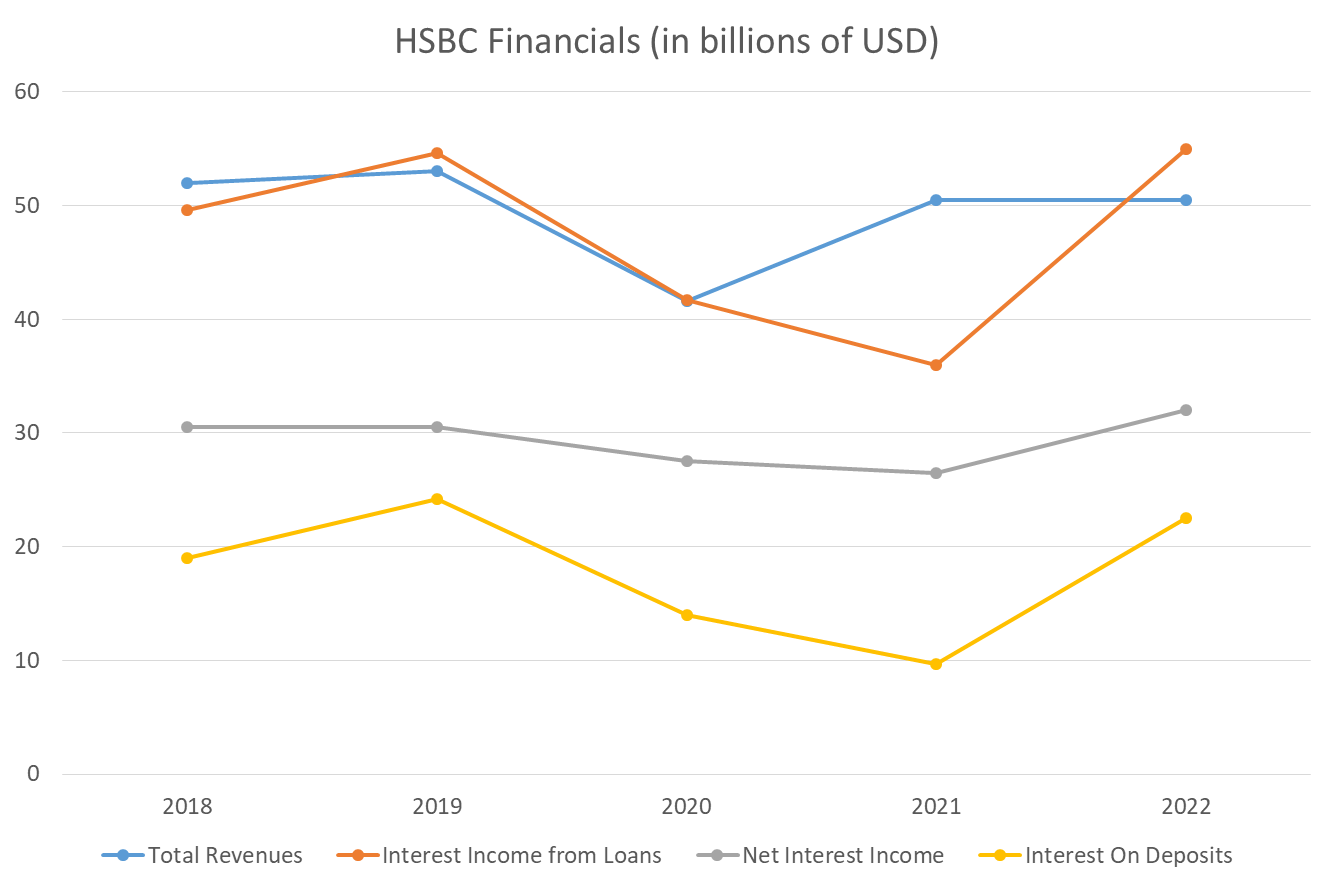

HSBC total revenues (including fees, net interest income on loans, and other income, and minus loan losses), interest income, interest on bank deposits, net interest income, and net income for the back over fiscal years of 2018-2022 were as follows:

Seeking Alpha

{kind=link}

HSBC's Financial Condition

The scale of HSBC’s financials is quite impressive. As a sprawling international bank that has expanded through Asia since the mid-1860s, and then spread across Europe and internationally during the early and mid-20 th century, this bank has been a mainstay in the finance world for several generations. Its massive numbers are thus a testament to its successful business moves over the past century and a half.

Still, many traditionally successful banks struggled during the Covid-19 pandemic, and HSBC was no exception, as shown by its dip in multiple metrics in 2020 and 2021. Still, profitability seems to have rebounded nicely, as the bank’s net income in 2021 managed to surpass its 2018 level while the bank’s income and revenue were still stabilizing.

Even more encouraging, neither the rise of fintech players like StoneCo Ltd. ( STNE ) and Block, Inc ( SQ ), nor the persistent popularity of decentralized cryptocurrencies such as Bitcoin ( BTC-USD ) and Ethereum ( ETH-USD ), have sapped HSBC’s momentum, at least not during this brief post-pandemic period.

This is at a time when many are decrying the use of traditional banks entirely, and several regional US banks , and even large international banks , are suffering from bank runs and other possible precursors of future struggles. Yet HSBC’s finances seem to be mostly unaffected by the fintech competition to traditional banking, and are also undisturbed by the turmoil in the banking industry to date, with HSBC enjoying a solid FY2022 by all metrics as it rebounds from Covid.

Overall, I am quite pleased with HSBC’s present financial situation. Based on the bank’s current financials, international reach, and long track record of success, I would find it a very attractive blue chip buy and hold. However, other information on HSBC makes me much less enthusiastic about its long term performance.

Valuation

As with the financial situation, I am fairly pleased with HSBC/HBCYF’s valuation at first glance. HSBC/HBCYF’s P/E ratio is hovering at around 6x compared to the financial sector average of 9x; HSBC/HBCYF’s Price to Sales is at about 2.5x, only a slight premium over the sector average of 2.2x; HSBC/HBCYF’s Price to Book is ~0.75x compared to the sector average of 1x; and HSBC/HBCYF has a Price to Cash flow ratio of ~5.6x, slightly discounted to the sector average of 6x.

Again, the company is quite attractive in its present state, and combined with its stellar financials, its stock would make for a good value buy. But even at this discount, the many costs and risks of doing business in China have likely not been baked in yet.

China is still viewed as investable by many in the banking industry, including Deloitte , which believes that “China’s banking sector is facing great opportunities”, and that “[g]reen transformation, digital economy[,] tech innovation … unprecedented reform in financial regulation … [i]nclusive finance [that] will focus more on poverty alleviation and rural revitalization, while reviving consumption,” and other positive developments in China's financial landscape will offset the risks threatening China’s financial industry.

I don’t believe Deloitte, or most analysts, have properly estimated the risks of investing in the Chinese banking sector; consequently, I think they, like many banking sector investors, are unwittingly assigning banks and companies investing in China an undeserved premium for assumed future stability and growth. I believe this premium likely exists even in HSBC's discounted valuation, and that it could be contributing to overvaluation if the assumption of stability and growth in China does not meet the reality.

In the next section, I explain the magnitude of China’s risks, which appear much bigger to me than its proposed fixes can manage, and why I think HSBC’s China pivot does not bode well for the bank, even at these attractive valuations.

HSBC’s Investment Push Ignores Risky Conditions in China

HSBC has begun to invest in the Chinese financial industry in the past few years. However, China is an autocratic government that demands absolute loyalty and obedience from all companies doing business within its borders, and will punish any company that raises its ire. HSBC knows this well: the bank has already provoked China once, and was punished for it as recently as 2021 in the form of lost business relationships, fines, public denigration from state media, and stymying of its business operations in China.

HSBC should have learned its lesson and pulled its business out of China, and should have pulled out of Hong Kong too when its legal system was changed to accommodate the desires of the mainland government in Beijing during the Coronavirus pandemic. Instead, as recent reports suggest, HSBC has decided to double down on investments in the country.

This seems like a questionable choice in the short term, and could be a catastrophic mistake in the long term. China has deceptively robust, but actually fragile, economic conditions in the short term, as evidenced by its more persistent post-pandemic economic sluggishness compared to other economies.

However, more important for HSBC, China’s economy is also facing severe long-term headwinds, some of which I will list and explain here.

The Long Term Economic Risks

China’s housing crisis and rapidly aging population may destroy the value of assets of Chinese citizens and reduce the possible growth rate of the Chinese economy for decades, respectively; China’s restricted access to advanced semiconductors could reduce the country’s ability to create productivity-boosting technologies to power its next generation of technological and economic advancements; and China’s looming debt crisis may create an acute but severe crash that decimates the Chinese economy, causes the liquidation of many businesses, upends the livelihoods of tens or even hundreds of millions of Chinese citizens, and drags many Chinese down into the lower middle class or poverty, essentially creating a Chinese Lost Decade not unlike that experienced by Japan .

I believe that the fallout of these long term headwinds could have a major, decades-long impact on the entirety of the Chinese economy, and I reiterate that it is not a place any foreign company or investor should put their money, time, or resources. HSBC’s significant investments in China for the long term are thus likely to end in great disappointment for these reasons alone.

The Long Term Geopolitical Risks

On top of the above issues, HSBC is subjecting itself to the risks caused by the temperamental environment and extreme self-interest that characterize autocratic governments like China's. The CCP, or Chinese Communist Party, which is the sole ruling political party that controls the Chinese government, will likely force HSBC to engage in activities that are beneficial to the CCP and the government as a whole, and the specific mandates may change on a dime. In effect, HSBC, like other banks in China, may not be able to pursue the same shareholder value-maximizing goals that those operating exclusively in liberal democracies can.

HSBC, as a foreign bank could be subject to other geopolitical risks of operating in China as well. For example, if the Chinese economy and/or financial industry starts to sag in the coming years, the CCP may do whatever is necessary to ensure that any foreign business in the country stays in the country – including forcing foreign companies to pay a hefty price to leave, so as to ensure the continued presence and investment of foreign companies. HSBC and many other firms doing business there now would subsequently be trapped.

This is exactly what Russia is doing to businesses that remained in the country as its invasion of Ukraine decimated the Russian economy; after a big chunk of foreign companies left Russia in the immediate aftermath of its invasion, Russia put up expensive roadblocks to stem the outflows of foreign capital and operations. Such may be the fate of HSBC in China if the bank continues its current course.

HSBC's Missed Opportunity to Mitigate Risks

HSBC had a recent opportunity to cut its losses in China early when a large division of the bank was almost spun off into a separate company headquartered in Hong Kong . This proposed spinoff was part of a takeover attempt led by a Chinese insurance firm that owned a not-insignificant portion of HSBC shares. However, HSBC and its investors pushed back against the deal , and beat back the takeover attempt.

Had this takeover attempt been successful, HSBC would have been forced to give up its business in much of Asia, and likely all of China. As painful as such a loss would have been, though, letting it happen may have been the better option compared to what is to come.

The Potential Consequences of HSBC’s China Strategy

As long as HSBC prioritizes growth in China, the bank is putting itself at risk for extreme and unpredictable coercion , mandates , and crackdowns by the Chinese government, acts that would rarely occur to such a degree in the West or elsewhere. This is to say nothing of the risk of sanctions that the West (i.e. both the US and Europe ) may bring down on the bank. If HSBC is forced to do China's bidding in ways that endanger the interests of Western countries, especially the US, HSBC would be at risk of fines, sanctions, prosecutions, and delisting from Western stock markets.

Geopolitical risks aside, there is also the possibility that increasing anti-China sentiment prompts customers to take money out of banks with significant Chinese dealings, including HSBC. Were this to occur, it would likely result in a deep loss of depositors for HSBC, and a possible bank run if it happens rapidly enough.

Lastly, if and when the Chinese economy starts to decline organically due to the systemic domestic issues mentioned in the previous section, HSBC's return on investment in China will be greatly reduced. This raises the possibility that its foray into China ends up being a costly endeavor that, combined with the other risks and potential fallout, was more trouble than it was worth.

The risks faced by HSBC mirror the ones I pointed out in a previous article on why companies operating in authoritarian countries are worse picks for investors than companies in liberal democracies. These risks for HSBC also mirror my concerns regarding investment in Chinese companies specifically .

Silver Lining – An Out Still Remains For HSBC

All of the above risks could have been nipped in the bud if HSBC had willingly given up its China/Asia business. However, I think these risks can still be avoided, because HSBC can still sell.

Having recently rebuffed a takeover attempt, HSBC is in a position of strength with respect to its institutional, corporate, and other large investors. From this position of strength, HSBC can carve out parts of its business it doesn’t want, i.e. operations in China and Hong Kong, and give them to a known interested buyer: Ping An Insurance Group ( PNGAY ) ( PIAIF ), the Chinese insurance giant that led the recent takeover attempt.

With Ping An as the buyer, HSBC could sell off its toxic China and Hong Kong business, but maintain its presence and growth in the rest of Asia. This would allow the bank to grow its business alongside the rising economies of other Asian nations whose citizens will use the bank’s services, but also prevent the bank’s business from suffering under the oppressive mandates of the CCP. It would also give Ping An the assets and business operations it wanted from HSBC from the beginning.

I see this as a win-win scenario for Ping An and HSBC in the long run, and HSBC would be wise to pursue such a deal regardless of any short term pain it might bring. The costs of doing business with autocratic China are insidiously high, and will only keep rising so long as China remains an authoritarian state. I believe it would be better for HSBC to cut its losses now, instead of suffering greater losses over time in China. Otherwise, I think investors should cut their losses instead, rather than suffer greater losses over time being invested in HSBC.

Risks to the Sell Thesis

The main risk to my thesis regarding HSBC is that it finds a way to cut its losses in China and Hong Kong - in essence, by following the path I laid out in the above section. I believe this would be very lucrative for the bank, and would remove most of the risks of operating in CCP-controlled China while allowing HSBC to keep the benefits of investing in growing and modernizing Asian economies, making the bank a buy.

Another risk to my thesis is that China reliably liberalizes over the next few years. Were this to occur, HSBC would be investing in a large, growing, liberal government in Asia, with all the benefits of investing in the world’s second largest economy and one of the world’s largest liberal countries, similarly improving the investment prospects of HSBC.

The latter scenario is highly unlikely, but the former is one to watch out for over the next few years. If HSBC takes advantage of its bargaining leverage and acts relatively quickly, it could engage in a sale of its China business, secure favorable terms for the deal, and strengthen the investment case.

Conclusion

As Europe's largest bank, HSBC should be a no brainer of a blue chip stock to own for the long haul, and I had considered adding it to my watchlist as a long term buy. But with its determination to expand into China and Hong Kong instead of selling its business there, the bank has committed to enduring dark times ahead. The risks that await HSBC as it pursues Chinese growth are many, and they will likely combine to worsen HSBC's overall business performance as well as trigger other consequences that depress its stocks’ performance.

Until it demonstrates the desire to sell its China and Hong Kong business operations and avoid the substantial risks of investing in autocratic China, I rate HSBC and HBCYF a sell for the long term.

For further details see:

HSBC: A Great Bank Investing In Uninvestable China