HBCYF - HSBC Holdings: Fundamentally Strong Bank Trading At An Unwarranted Discount To Book

2023-05-30 01:20:46 ET

Summary

- Having built up its global scale in previous decades, HSBC is now unlocking value by streamlining its non-core operations.

- As Q1 showed, the core business continues to be resilient as well, defying the deteriorating investor sentiment on banks this year.

- Given its wide discount to book and elevated shareholder returns, HSBC equity offers investors compelling value at these levels.

HSBC ( OTCPK:HBCYF ) kicked off the year strongly, with a solid set of Q1 results despite the banking turbulence in recent months. Instead, the bank appears to be benefiting from extended Fed and BoE rate hike expectations, with management now guiding to a 12% return on tangible equity ((ROTE)) earlier than expected. There remain plenty of growth drivers on the horizon as well. The reopening of the China/HK border is a big tailwind to its non-interest income revenue base (mainly via wealth management), while proceeds from the disposal of its non-core Canadian business add significant capital optionality. Having also rightsized its cost base in recent years, HSBC is one of the better-positioned UK banks to navigate an eventual transition into lower rates. Beyond costs, the successful execution of its strategic initiatives (e.g., the pending disposal of HSBC France) presents an additional lever to further profitability and capital return upside. At a >20% discount to book, HSBC seems too cheaply priced and should re-rate as sentiment on EU banks improves over time. In the meantime, investors can look forward to a well-covered mid-single-digit % yield.

Resilient Operational Results Defy Investor Sentiment

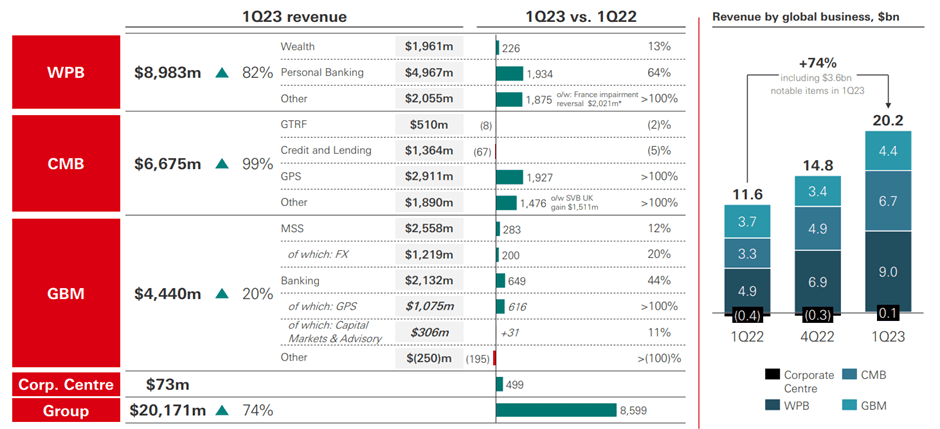

With Q1 representing the first quarter of IFRS 17 restatements for HSBC, the quarterly results were always going to be muddled. There were also ~$4bn of notable items that skewed the headline numbers, most notably one-off gains from the SVB UK acquisition and an accounting treatment change for the French banking operation (~$3.6bn gain), as well as a tax provision release of ~$0.4bn. Still, the reported Q1 net interest margin of 1.69% represented a slight QoQ acceleration (+50bps YoY) on an IFRS 17 basis, led by higher rate tailwinds in the UK business. With management maintaining a below-consensus >$34bn net interest income ((NII)) guidance for the year despite the strong quarterly beat, there remains ample room for an upgrade at the Q2 2023 review. Further reopening-driven strength in China presents additional upside to the non-NII side, particularly the wealth management business (revenue up ~13% YoY in Q1).

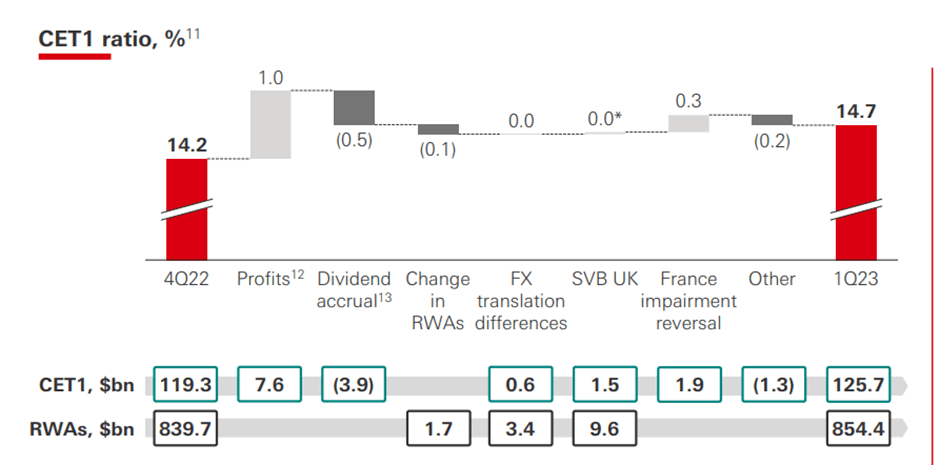

{kind=link}

HSBC

HSBC has been making steady progress on the expense side as well, with the Q1 cost base down ~2% YoY (FX-neutral basis). Excluding the one-off ‘cost to achieve’ expenses booked last year, costs would still only be up ~2% YoY (well below top-line growth). The Q1 expense run-rate is guided to extend through the rest of the year, with incremental SVB UK costs pushing overall growth slightly higher to +3%. The latter is mostly ~$300m of one-off severance payments, though, so expect the cost base to shrink post-integration from FY24 onward. Also positive was the capital position, with the CET1 ratio rising +50bps QoQ to 14.7% (albeit including ~25bps from the France impairment) and remaining well on track to hit the 14-14.5% guidance range. The positive P&L trend has flowed through to a stronger-than-expected 12% ROTE base in Q1 (vs. the current >12% target), clearing the path for a sizeable upward revision here as well.

{kind=link}

HSBC

An Unfolding Capital Return Story

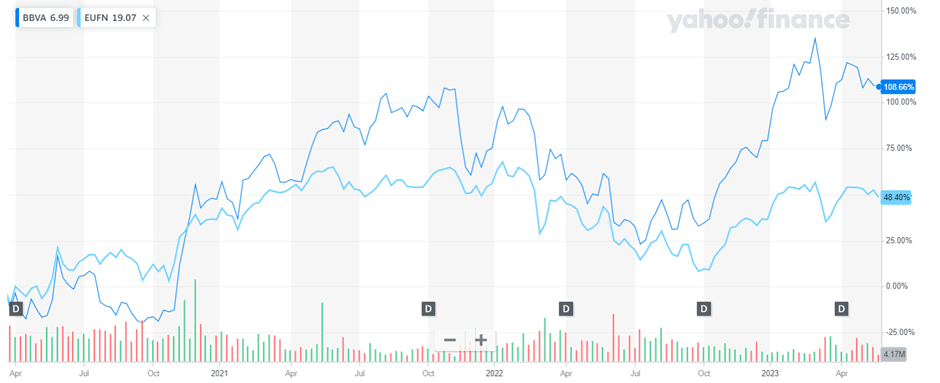

Since disposing of its non-core Canadian business for $10.1bn (implied ~3x tangible book value), a transaction that drove ~130bps of upside to its CET1 ratio, HSBC has further extended this momentum. In Q1, the bank’s solid capital generation was the key driver behind a +50bps sequential rise in its CET1 ratio to 14.7% (net of a front-loaded $0.18/share dividend accrual). But a one-off ~25bps impairment reversal benefit from the potential disposal of its French business also helped. And given management’s commitment to the France sale, expect a further capital impact down the line (vs. the ~25bps initial guidance in 2021). Still, a look back at comparable non-core disposal events by European banks indicates a likely net accretive outcome over the mid to long term. Along with HSBC’s fundamental and valuation uplift since the Canadian sale, Spanish bank Banco Bilbao Vizcaya Argentaria ( BBVA ) has seen a similar benefit, outperforming the sector (proxied in the chart below by the iShares MSCI Europe Financials Sector Index ETF ( EUFN ) since its 2020 sale.

{kind=link}

Yahoo Finance

A key reason for the potential upside is the massive capital optionality a disposal would provide to HSBC. The Canada business sale (now accounted for as ‘held-for-sale’ and expected to be complete in Q1 2024) has freed up significant capital, allowing for ‘up to $2bn’ of buybacks post-AGM. In turn, the planned capital return will lower the CET1 ratio by ~25bps in Q2. Still, there remains ample headroom for even more returns down the line, given the CET1 is already well above the 14-14.5% mid-term target and management’s stated plan to ‘manage range down further longer term.’ One option under consideration is a 2023-2025 buyback program, allowing for opportunistic repurchases throughout the cycles. Also being discussed as a ‘priority use’ of proceeds is a $0.21/share special dividend, with the remainder accruing to the CET1 balance. Along with a steady dividend payout and the potential for more shareholder return upside should the French business sale go through, HSBC’s total yield screens very attractively – even in today’s higher rate environment.

Fundamentally Strong Bank Trading at a Big Discount to Book

HSBC has sold off alongside the rest of its developed bank peers following the series of banking failures in the US and EU. But its strong Q1 numbers showed this may have been a case of the baby being thrown out with the bathwater. Its interest and non-interest income streams remain strong, supporting a low-teens % RoTE by 2023 (one year earlier than targeted). And with plenty of potential catalysts in the pipeline, including more non-core asset sales and HK/China border reopening-driven upside in wealth management, the stock seems unfairly discounted at ~0.8x P/Book. In the meantime, shareholders get paid via a ~$2bn buyback (over the next three months) and a mid-single-digit % yield to wait for the re-rating.

For further details see:

HSBC Holdings: Fundamentally Strong Bank Trading At An Unwarranted Discount To Book