HUBB - Hubbell Incorporated: Limited Upside Potential

2023-12-03 03:23:33 ET

Summary

- Hubbell Incorporated reported strong growth in net sales driven by organic growth and acquisitions in 3Q23.

- The acquisition of Northern Star Holdings is expected to enhance Hubbell's growth outlook, particularly in utility solutions.

- Despite positive performance and strategic acquisitions, the current share price is in line with the target price, leading to a recommendation of a hold rating.

Investment Action

Based on my current outlook and analysis of Hubbell Incorporated ( HUBB ), I recommend a hold rating despite its robust 3Q23 results, which show strong growth in net sales driven by both organic growth and acquisition. On top of that, it managed to expand its operating margin as well. Apart from its financial performance, I also note that the acquisition of Northern Star Holdings aligns well with its business, and I expect it to bolster its future growth outlook. However, my valuation’s target price is in line with its current traded price.

Basic Information

HUBB specializes in providing electrical and utility products and solutions, with a focus on areas like transmission and distribution and utility management.

Over the last 5 years, HUBB’s revenue growth trend has been improving significantly. In 2019, it reported a decline of 11.94%. However, over time, its revenue started to slowly improve, and by 2021, it finally reported a positive growth of 13.89%. In 2022, it reported its highest revenue growth of 17.97% throughout these 5 years.

In terms of returning value to investors, HUBB is managing it well, as it is able to grow its net income margin from 8.01% in 2018 to 10.31% in 2022, which represents an improvement of more than 2%. As a result, diluted EPS grew from 2018’s $6.54 to $10.07 in 2022, representing an improvement of ~53% over the 5-year period.

Review

HUBB reported its 3Q23 results on 31 October 2023. Its net sales grew 5%, made up by 4% organic growth and 1% through acquisition. Its operating profit margin grew 4.6% while adjusted operating profit margin grew 4.4%. Diluted EPS came in at $3.7 but adjusted diluted eps is higher at $3.95.

Organic revenue growth for the HUBB Utility segment is 6.9%, driven by a price increase of 7.5% and a decrease of approximately 0.5% in volumes. The transmission and distribution [T&D] division's components saw 3% quarterly growth, and the transmission division's shipments, backlog, and pricing are all looking great. Additionally, distribution is at a strong level, especially in areas where there were shortages, such as Metal Oxide Varistor [MOV] blocks. However, as lead times have decreased and the channel has improved its inventory management, the book and bill side of distribution has recovered.

Meanwhile, telecom experienced a temporary downturn; however, HUBB anticipates an injection of stimulus funds into this sector next year, and the outlook for the medium term is optimistic. The backlog here is still in excess of $1 billion, and communications and controls went up 28% as the supply chain eased. By the end of the year, HUBB expects the channel inventory positions to normalize, despite the elevated backlog at Utility. The inventory correction is progressing well, and HUBB is pleased due to their excellent relationships with their channel partners and end users.

At the same time, utility demand is still very high. Due to typical seasonality, HUBB anticipates a 5% quarterly drop in sales and an increase in organic sales for 4Q. As the megatrends of grid modernization and electrification continue into 2024, HUBB maintains the belief that utility markets have the potential to generate mid-single digit organic growth in the coming years. According to HUBB, the telecom markets are expected to stay sluggish in the first half of 2024. On the other hand, the transmission and substation markets are expected to see strong demand, and the results in the second half of 2024 will be helped by the deployment of infrastructure stimulus funds. Overall, I believe all these drivers will bolster its 2024 outlook.

HUBB has confirmed that it has reached an agreement to acquire Northern Star Holdings, a market leader in substation control building solutions. HUBB expects the acquisition to improve its growth and margin metrics in addition to enhancing its Utility Solutions portfolio in the areas of control, communications, and utility components. Northern Star holding’s solutions are important for grid reliability, substation infrastructure protection and control, fault detection, and electricity flow control. In addition, Turnkey Solutions provides the most cost-effective solution for safeguarding and managing T&D assets. Not just that, but it also ensures that the total and initial costs are the lowest. Engineering services, control relay panels, and equipment enclosures are all part of the offering.

Their control relay panels include a variety of options, including modular rack front panels, solid front panels, duplex panels, and rack panel plates, and can be tailored to meet the specific needs of each customer. They are the leading North American designer, manufacturer, and integrator of turnkey control panels.

When it comes to technical support, their website showcases the knowledge and experience of prominent manufacturers. In addition to a complementary product line and client base, they have witnessed a double-digit sales CAGR over the past eight years. With such robust historical sales figures and the competitive advantage of its solutions mentioned above, this acquisition seems like the right corporate decision, and I believe it will enhance HUBB’s overall business strength as well as its growth outlook.

HUBB Electrical's growth slowed to 1.2%, with prices going up a single digit and volumes going down a single digit. As channel inventory management settles down, it's encouraging to see sequential increases in volume. The most striking example is non-residential, where the volume increased sequentially due to the emergence of order patterns and the anticipation of growth in the segment in 4Q. Industrial was strong, thanks to reshoring tailwinds, while residential was down double digits on an end-market basis. Approximately 25% of Electrical's sales in 2024 came from growth verticals like data centers, renewables, and technology and development, and this trend is anticipated to continue for the foreseeable future. Industrial is doing well, and non-res is looking to remain stable. Moreover, electrical products make up approximately 40% of the segment. Despite flat sell-through, the business has been experiencing a decline in high single-digit sales due to destocking trends. However, this destocking issue may turn potentially positive in 2024.

Valuation

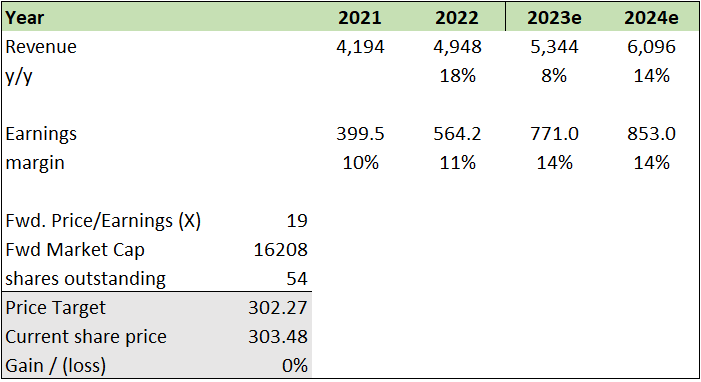

I believe HUBB can grow to 8% in 2023 and 14% in 2024 because of the following factors. Firstly, its 3Q23 results are positive, as it reported revenue growth mostly driven by organic growth. In addition, its operating profit margin also expanded, which leads me to forecast improving margins for the next two years. HUBB’s Utility segment’s robust organic revenue growth that is driven by price increases and strong demand further bolstered these assumptions.

Recently, HUBB also announced and confirmed the acquisition of Northern Star Holdings. As discussed above, I believe this acquisition fits well with HUBB, and I expect its strong market leadership to contribute positively to HUBB, thus further bolstering HUBB’s growth outlook.

In the non-residential sector, HUBB saw an increase in sales as it was getting more consistent orders and expects more growth in this area in 4Q. In addition, its industrial sector is also doing well, partly due to businesses moving back to local production. Hence, I expect its industrial sector to bolster its future quarter’s outlook as well.

{kind=link}

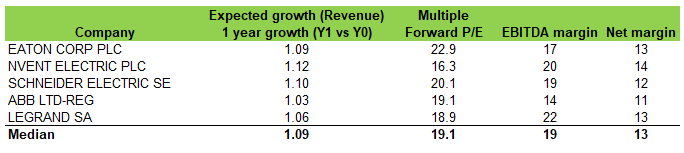

HUBB is currently trading at ~18x forward P/E. Its peers are trading at a median of 19x. Given that HUBB’s EBITDA margin, net margin, and 1-year growth outlook are in line with peers’ medians, I think HUBB should be trading at peers’ median forward P/E. HUBB’s EBITDA margin is ~18%, its net margin is ~10%, and its 1-year growth outlook is 8%. Peers’ median EBITDA margin is ~19%, net margin slightly higher at ~12%, and 1 year growth outlook is ~9%.

My price target is ~$302, which is in line with its current traded price. With no gain, I recommend a hold rating for HUBB despite its robust 3Q23 results and strategic acquisition. I believe the market has already priced HUBB’s strength in.

{kind=link}

Risk and Final Thoughts

The first risk is stronger end-market demand due to more resilient-than-feared non-residential and industrial fundamentals and sustained strength in utility spending. The second risk is that the combination of stable pricing and reduced commodity costs leads to a larger than anticipated price-cost spread, which in turn generates higher than anticipated margins. In the event that future growth outlook and margins were to beat expectations due to these factors, its share price would see upward movement.

For 3Q23, HUBB's results showed robust growth in net sales, driven by both organic growth and acquisitions. Its utility segment experienced robust organic revenue growth, supported by price increases. The acquisition of Northern Star Holdings is set to boost HUBB's portfolio and growth outlook, particularly in utility solutions. Despite a slowdown in residential sales, the non-residential and industrial sectors are performing well and is expected to have a positive growth outlook. Despite all these strengths I have discussed in detail above, its current share price is in line with my target price. With no gain potential, I am recommending a hold rating for HUBB now.

For further details see:

Hubbell Incorporated: Limited Upside Potential