HUBB - Hubbell Incorporated: Too Expensive As We Go Into The Q3 Report

2023-10-30 15:49:37 ET

Summary

- Hubbell Incorporated's share price has risen 17% in the last year, outperforming the broader market.

- The company is structured into two core segments: Electrical Solutions and Utility Solutions.

- The next report from Hubbell will be crucial to determine future prospects, but short-term headwinds and high valuation suggest a hold rating.

Investment Rundown

The share price for Hubbell Incorporated ( HUBB ) has risen quite quickly over the last 12 months, outperforming the broader markets, seeing as it's up around 17%. HUBB is included in the industrials sector, where it focuses on offering a variety of electrical and utility solutions. We are very close to the most recent quarterly report coming out for the company, that being the Q3 FY2023 report. I have not seen a strong enough recovery or momentum in the Q2 report, and higher interest rates seem to indicate that demand and capital spending may be suppressed going forward. This makes it in my opinion likely that Q3 will not be producing such strong results as to warrant a buy here. What investors can hope for is optimistic guidance and comments from the management team which would in the short term lift the share price higher, but it's a bet I am not willing to make. HUBB is already trading at a p/e of 18.4 already, which is above where a lot of the companies in the industrial sector are trading. What can be a cause for this is the higher EPS growth that the company has showcased, up 45% YoY in the Q2 report. Last year saw EPS of $3.08, and I think it is still somewhat unlikely to see a similar 45% YoY growth, as that would equate to $4.46 per share. I am rating HUBB a hold as I see short-term headwinds like rising interest rates as a means that could hurt top-line growth, and muted bottom-line growth as well. The next report will be crucial to see what the management thinks going forward, and making a bet on the positive side seems too risky right now, which underscores my reasoning behind the hold rating.

Company Segments

HUBB focuses on designing, manufacturing, and distributing innovative electrical and utility solutions, catering to both domestic and international markets. This company is structured into two core segments: Electrical Solutions and Utility Solutions.

Within the Electrical Solutions segment, HUBB offers a diverse range of wiring devices, encompassing both standard and specialized applications. Their portfolio extends to rough-in electrical products, connector and grounding solutions, state-of-the-art lighting fixtures, and a comprehensive array of electrical equipment tailored for industrial applications. In the last quarter, the fastest-growing segment in the company was the HUS segment, at 11% YoY in total.

{kind=link}

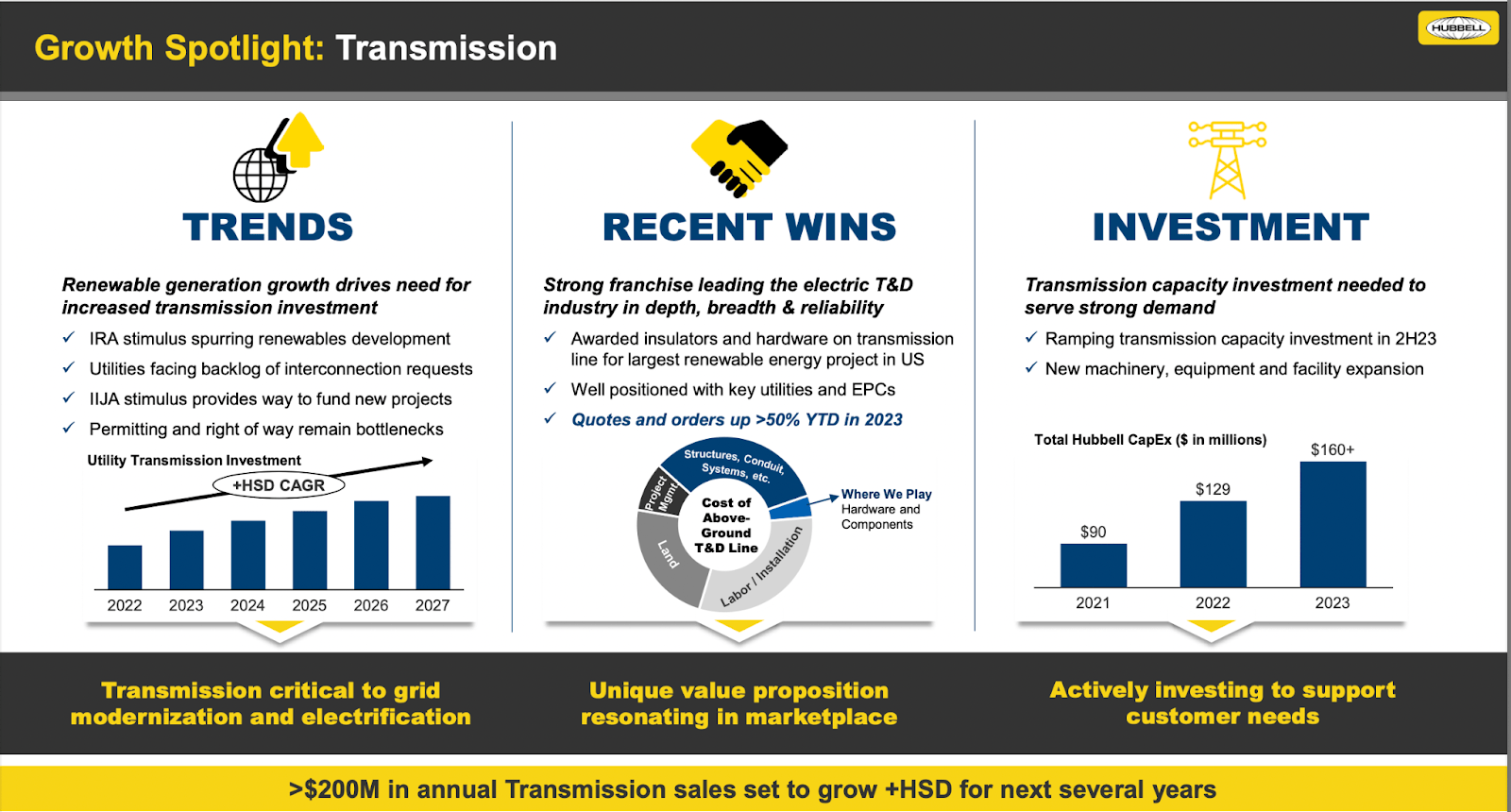

Some of the highlights for the company include their strong results in growing transmission sales, which are set to grow sales to $200 million in the next several years as per their own projections . With the last 12 months resulting in revenues of $5.1 billion, this additional 4% or so top-line growth will greatly benefit HUBB. I want to see it realized though before I rate the company any higher. Going forward for HUBB the transmission investments it is making could be a key driver for growth.

{kind=link}

The market projections right now seem to be that HUBB will be able to grow the top line at a decent single-digit rate. I mentioned the 4% or so markup the $200 million could have on the top line, which will of course as well also decline over time unless HUBB continues to make investments. They have several tailwinds behind them right now, though, like increased investments into renewables and the energy grid in the US. Increased spending in these spaces and areas is likely to result in increased demand for HUBB's products as well.

Earnings Highlights

It has been broadly mentioned already, but the last report for HUBB saw strong overall EPS growth as it reached $4.07 for the quarter. On an annualized basis, that is around $16.3, which would put HUBB at a FWD p/e of around 16. There is some seasonality to the sales and earnings of HUBB which means that perhaps expecting over $16 in EPS is unrealistic.

{kind=link}

The results from Q2 helped catapult the share price upwards as increased EPS was achieved. Currently, I think that the following report from HUBB which is set to be on October 31 won't produce the same 45% YoY EPS growth. I think something around the $4 mark is realistic, as revenues could land at $1.4 billion, and I don't see HUBB facing severe net margin losses on just a sequential basis. What is pressuring the margins is higher interest expenses, but it seems that HUBB was efficient in their debt handling, as the interest expenses have declined from a high of $72 million in 2018. Furthermore, some margin pressures caused by wage inflation seem to be present as well, and the selling general & admin expenses have risen to $800 million. Since 2020 it has grown by over 33% while revenues increased by 38% during that period. What I want to highlight is that should wage inflation continue to increase at a similar pace, it seems likely that the potential EPS that HUBB could generate could quickly diminish.

{kind=link}

Right now, the company is trading at a p/e of 18.4, which is 13.78% above the rest of the sector. I think that HUBB will over the next several years average an EPS growth rate of around 6 - 7% rather than the high double digits it has recently shown. Investments in transmission are paying off it seems, but not enough that a premium like this is justified, I think. I would be much more comfortable buying at around 14 - 15 for the p/e.

{kind=link}

Furthermore, on the p/s scale, HUBB is trading quite high as well. A 127% premium doesn't seem justified when the forward-looking top-line growth doesn't seem to breach double digits. We need a lower entry point or optimistic comments from the next report that could indicate that increased demand is projected. Until then, I think that a hold rating is far more reasonable here.

Risks

Some of the risks revolve around the possibility of raw material prices experiencing a more rapid decline than initially anticipated over the short term. Such an occurrence could trigger additional margin expansion, potentially igniting robust earnings momentum, and consequently propelling the share price to higher levels.

On the flip side, it's important to consider that this scenario can also introduce volatility and uncertainties, as fluctuating raw material prices impact the cost structure of the company and, subsequently, its profitability. Thus, maintaining a watchful eye on these potential price shifts and their ramifications is essential in sustaining a well-informed investment approach and adjusting the hold thesis as necessary to adapt to evolving market dynamics.

{kind=link}

So far HUBB has been performing very well in terms of raising the net margins, but should that momentum shift and start stagnating then the markup in the valuation against the industrial sector may be adjusted to bring the share price down. Over the long term, though, it seems that HUBB has the potential to deliver steady top and bottom-line appreciation, and short-term margin losses shouldn't indicate a lack of long-term prospects. With that said, we may see better entry prices should the margins fall, and that means a hold rating makes more sense than a buy right now too.

Final Words

The price for HUBB has appreciated very well over the last 12 months, as the EPS has grown at double-digit levels. Should the same EPS results be continued as seen in Q2 then HUBB trades at an FWD p/e of 16, but I find it realistic that some seasonality to the EPS is to be expected. This ultimately means that HUBB is trading at a premium and doesn't offer any significant value going into the third quarter in my view. Over the long-term, though, there are strong tailwinds like increased investments into renewables and the utility sectors, which should boost demand for HUBB. For the moment though, I see HUBB as a hold.

For further details see:

Hubbell Incorporated: Too Expensive As We Go Into The Q3 Report