HUBB - Hubbell: Valuation Looks To Be At Extended Levels

2023-07-26 16:42:17 ET

Summary

- I have doubts that the company's level of profitability, particularly in the utility segment, is sustainable.

- The uncertainties in FY24 should put a lid on how much valuation can further expand from here.

- Valuation should re-rate downwards along with the market eventually to historical averages.

Summary

Following my coverage on Hubbell Inc ( HUBB ), which I recommended a hold rating (close off any short positions) due to HUBB's increased profit outlook and the closure of its valuation vs. the S&P 500. This post is to provide an update on my thoughts on the business and stock. I continue to give a hold rating to HUBB as I expect valuation to re-rate back to 17x as the market trades back to its historical range.

Investment thesis

HUBB's recent quarterly results saw segment profits come in at $306 million, with Electrical profits at $93 million and Utility profits at $213 million. Both segments' margins improved compared to 2Q22. Organic growth came in particularly strong for Utility (12.8%) which offset the headwind from Electrical, resulting in overall organic growth of 5.8%. The strong growth at Utility was propelled by the expansion of both utility T&D components (13% y/y) and utility Communications and controls (16% y/y). Given the high visibility that has resulted from the strong backlog supporting the growth of T&D components and the rising availability of semiconductors in communications and controls, I anticipate the Utility's growth to continue in the near future. However, despite the encouraging outcomes, I must caution that falling order intake in the Utility sector is a clear first sign of a slowdown, reflecting normalizing lead times. On the other hand, year-over-year organic sales for the electrical sector were -4%, with commercial-facing markets still feeling the effects of channel inventory management and the residential market remaining soft.

For the results, sales were in line with consensus expectations, but margins were better than expected, driven by price, cost, and productivity. I believe the easing of raw material costs was the key driver for margin expansion this quarter. While great, I am not sure if this margin level is sustainable, as it is usually in the mid- to high-teens range. Although there might have been some improved productivity over the years, I find it hard to imagine that it has resulted in over 500 bps of structural improvements.

Nonetheless, management raised EPS guidance for the year, which bodes well for FY23 as consensus estimates become more probable. That said, I think the focus is shifting more towards FY24, particularly as the price contribution is fading and the shrinkage of the Utility backlog is shrinking. I think the stock price movement (down close to 10%) post-result is a clear sign that investors are starting to be more wary about FY24. This brings me back to my initial short post that valuation was too high, and fast forward to today: HUBB Is still trading at 22x forward PE (more on valuation below), above its 1 standard deviation range. I would think that the risk of valuation re-rating back to the historical average of 18x is much higher today as the strong FY23 is coming to an end and FY24 has more uncertainties.

Valuation

{kind=link}

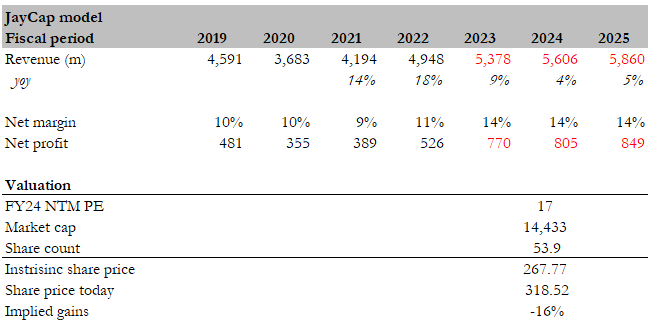

I believe the fair value for HUBB based on my model is $268. My model uses consensus figures for the next 3 years (revenue and net profit). The reason for doing so is to base my valuation on market expectations and to align my view on financials with consensus. My variant view here is that this is the multiple that HUBB should be trading at.

{kind=link}

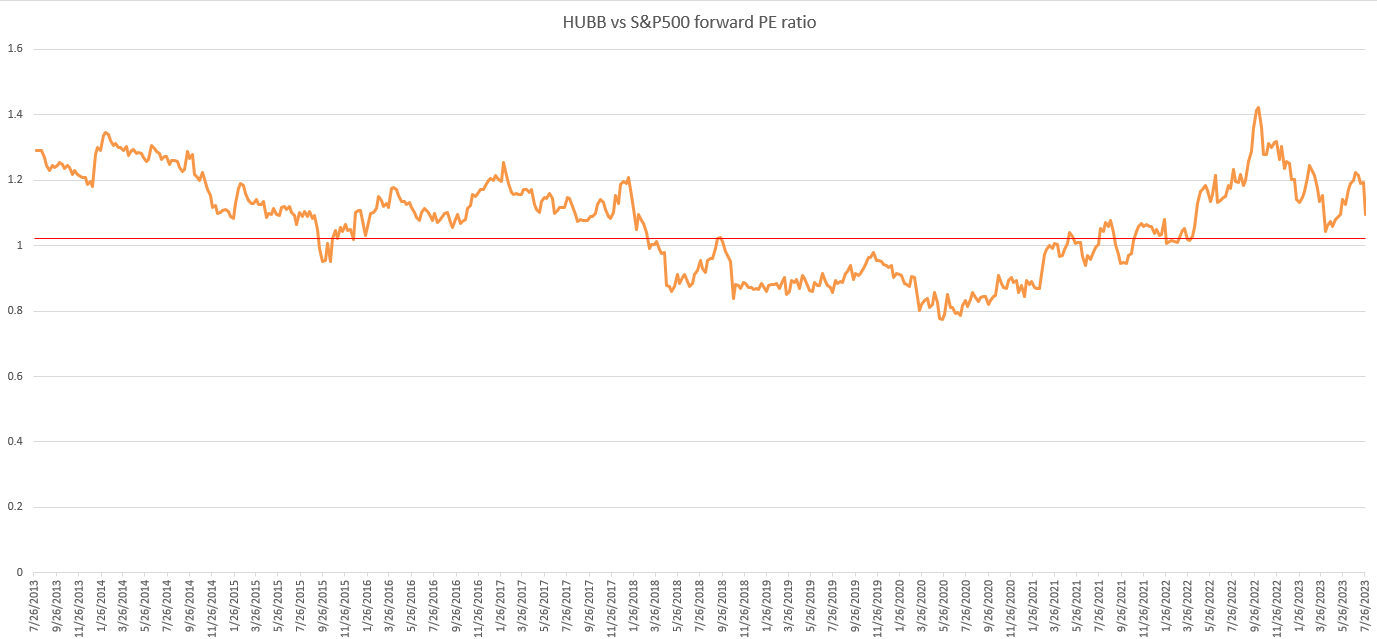

At a glance, it might seem that the HUBB is no longer trading at a premium to the market as the ratio has now tracked back to its historical average of 1x. However, this is not because valuation at HUBB has decreased; rather, it is S&P500 forward PE ratio that has increased to its 1 standard deviation range. As such, for investors to stay comfortable that HUBB will continue to trade at today's valuation of 21x forward PE, they are undertaking an assumption that the market will stay at the current multiple, which I think is hard to underwrite. Historically, the market trades at around 17x forward PE, and note that this was during years of zero interest rates. Adjusted for interest rates, the average valuation should be lower today as the equity risk premium increases. Nonetheless, I expect the market to revert back to its historical average, which means at the same 1x ratio, HUBB should be trading at 17x forward PE.

Risk

The risk to my hold thesis is that raw material prices fall faster than expected in the short term, resulting in further margin expansion that could cast strong earnings momentum, driving the share price upwards.

Conclusion

HUBB currently appears to be trading at extended valuation levels, with its forward PE ratio above historical averages and the S&P500. Despite strong segment profits and organic growth, I have concerns about potential slowdown signs and uncertainties in FY24. While there is a possibility of further margin expansion due to falling raw material prices, it is uncertain if this level of profitability is sustainable. Based on my valuation model, the fair value for HUBB is estimated at $268, suggesting that it may be overvalued at its current trading price.

For further details see:

Hubbell: Valuation Looks To Be At Extended Levels