HBM - Hudbay Minerals: Things To Consider Before Jumping On The Bandwagon

2023-03-17 05:04:23 ET

Summary

- Approximately 60% of Hudbay Minerals' revenue is attributable to copper sales, and the recent turbulence in copper prices is putting pressure on the share price.

- Strong production and cost performance during the 2023-25 period improve HBM's operating outlook but uncertainty in the metal prices steals the show.

- Moreover, HBM faces two significant debt maturities over the next 6 years and may face difficulty in managing cash flows for debt repayment, growth CAPEX, and ongoing exploration.

- The US-based projects have promising mining appeal but face certain challenges including permits, opposition from environmental groups, and CAPEX funding.

- I see HBM as a 'hold'.

Thesis

Hudbay Minerals ( HBM ) is a Canadian-based diversified metals mining company engaged in acquiring, exploring, developing, and operating copper and gold mining assets in North and South America. The company's existing production comes from its Peru and Manitoba operations.

HBM's recently reported results reveal that the company's Q4 2022 non-GAAP EPS of $0.01 missed expectations by $0.03, while revenues of $321.20 MM missed expectations by $74.4 MM (down ~24.5%, YoY.) Likewise, HBM's key financial metrics including revenues, cash position, total long-term debt, etc. all deteriorated during 2022, YoY. These numbers raise concerns about the company's financial position and performance during 2022. However, I see HBM's production and cost guidance for 2023 shows room for improvement.

Meanwhile, turbulence in copper prices is matched by the recent rally in gold prices. Nonetheless, HBM has two tranches of significant long-term debt maturing over the next 6 years, and HBM's mine plans for its existing mining operations indicate that the mining output from those operations will gradually decline after 2025. I see this whole situation as a potential concern for the company's long-term growth profile. Our article will discuss all the above areas in tandem. Let's get into the details.

Review of HBM's 2022 performance

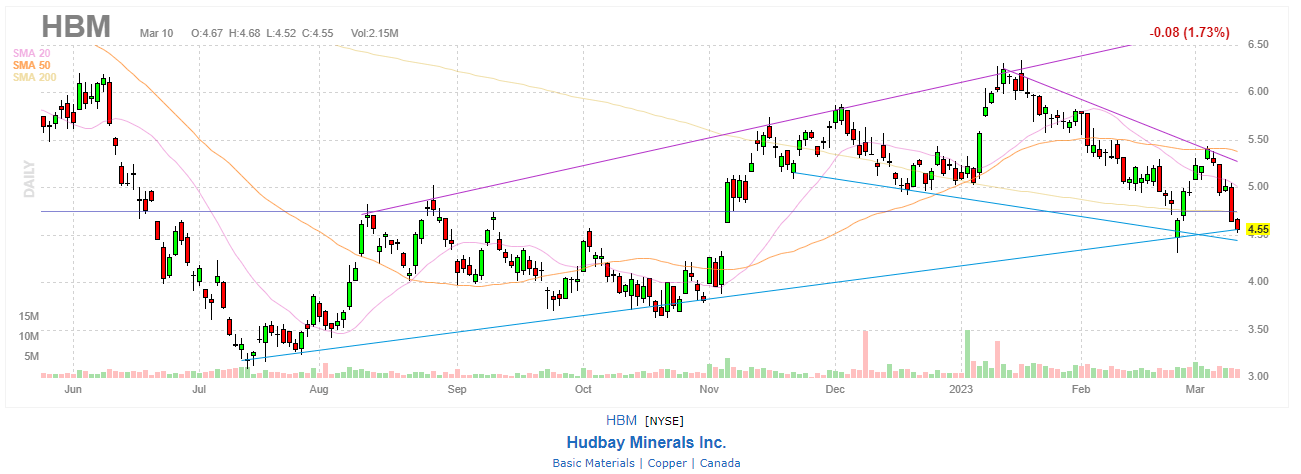

Technical Analysis

HBM's technical price chart for the past 9 months shows reveals a falling wedge pattern that could find support within the range of $4.25-4.35/share over the near term (say, the next 3 months). I believe the current momentum is partially due to concerns about Chinese copper demand and the US rate hikes. Markets are looking for stability and recovery in the Chinese copper demand, and that recovery should be sustainable to support a rebound in the share prices of copper (and gold) miners like HBM.

{kind=link}

2022 Performance Review

The following important metrics reveal a weakness in HBM's financial performance and financial position for the year ended December 31, 2022, YoY.

| Financial Performance Metric |

| December 31, 2022 |

| December 31, 2021 |

| Revenues |

| $321.20 MM |

| $425.20 MM |

| Adjusted EBITDA |

| $124.70 MM |

| $180.80 MM |

| Cash and cash equivalents |

| $225.66 MM |

| $270.99 MM |

| Total Long-Term Debt |

| $1,184.16 MM |

| $1,180.27 MM |

| Net Debt |

| $985.50 MM |

| $909.29 MM |

| Working Capital |

| $76.53 MM |

| $147.51 MM |

| Total Assets |

| $4,325.94 MM |

| $4,616.23 MM |

| Equity |

| $1,571.81 MM |

| $1,476.83 MM |

The YoY decline in revenues came despite a healthy increase in 'metal in concentrate produced' and 'payable metal sold', and the fact that All-In-Sustaining Cash Costs/pound of copper production also witnessed a YoY improvement (Figure-2).

Key Operational Metrics - 2022 vs 2021 - Source: Seeking Alpha (Figure-2)

In my view, these numbers indicate an overall weak metal price environment observed during 2022 compared with 2021. We know that the Russia-Ukraine conflict is the primary cause, as the ensuing economic slowdown triggered demand contraction for base metals like copper, zinc, molybdenum, etc. This is also evident from the fact that HBM's average realized copper price during Q1 2022 was $4.53/lb which declined to $4.28/lb during Q2 2022, following the start of the Russia-Ukraine conflict. The average price further dropped to $3.47/lb during Q3 2022, before gradually staging a recovery to $3.61/lb during Q4 2022.

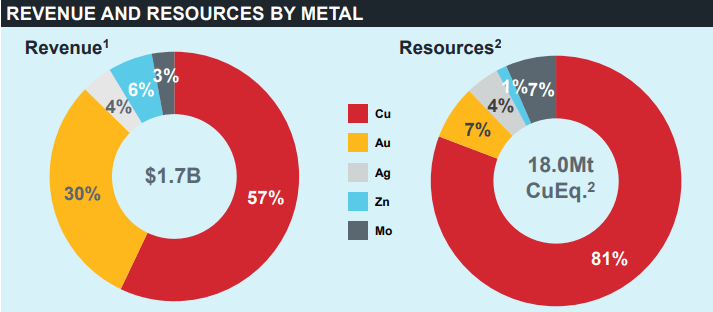

2023 Guidance: HBM's 2023 guidance reveals that ~60% of its FY 2023 revenues (amounting to ~$1.7 BB) will come from copper sales and ~30% from gold sales. It's worth noting that this guidance assumes copper price at $3.75/lb and gold at $1,750/oz. Meanwhile, spot copper trades at ~$3.9/lb while spot gold trades at ~$1,920/oz (at the time of writing). I believe this favorable increase in metal prices is likely to reflect positively on HBM's revenues. On a related note, ~81% of HBM's 18.0 Mmt (read: a million metric tons) of copper-equivalent mineral resource is comprised of copper. These numbers indicate the significance of copper in HBM's mining portfolio.

Revenues and Resources by Metal Type - Source: HBM (Figure 3)

{kind=link}

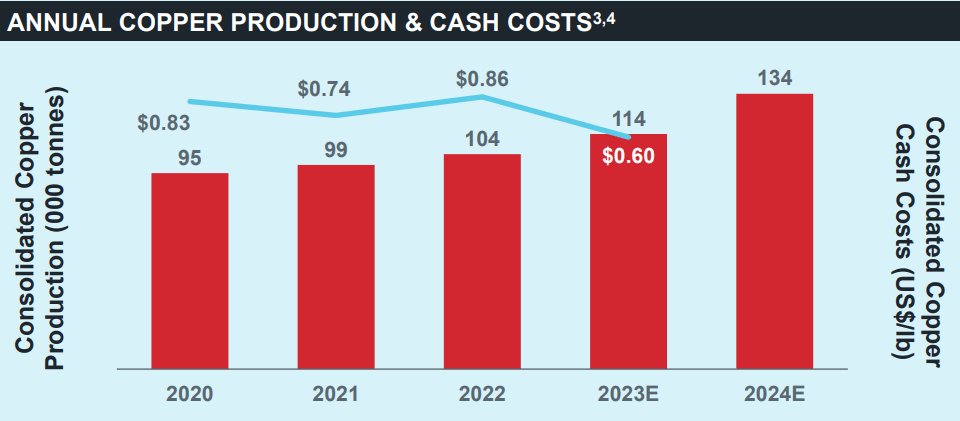

During 2023, HBM expects a ~10% and ~30% growth in YoY copper and gold production respectively. In terms of cost of production, HBM expects consolidated cash costs to decline from $0.86/lb copper in 2022 to ~$0.60/lb copper in 2023. This 30% YoY decline in unit cost is likely to reflect positively on HBM's 2023 profitability.

Expect Organic Growth From Existing Mines

HBM's copper production has gradually grown over the past 3 years, and this pattern is likely to continue during 2023 and 2024 (Figure-4).

{kind=link}

On a cumulative basis, I expect that increased YoY production together with the YoY decline in production costs will reflect favorably on the company's bottom-line profitability during 2023.

1) Peruvian operations: HBM's Peruvian mining operations comprise the Constancia mine (mine life=16 years) and the Pampacancha satellite deposits (mine life=3 years). Both these properties are 100% owned by HBM and represent open pit deposits. Ore mined at the Pampacancha deposit is transported to the Constancia mill for processing. The following table highlights that Constancia has greater underlying mineral resources in terms of resource volume while Pampacancha has higher grades.

| Deposit |

| Resource Type |

| Ore Tonnage |

| Cu Grade |

| Constancia |

| P&P Reserves |

| 483 Mmt |

| 0.28% |

| Constancia |

| M&I Resources |

| 242 Mmt |

| 0.22% |

| Pampacancha |

| P&P Reserves |

| 38 Mmt |

| 0.65% |

| Pampacancha |

| M&I Resources |

| 10.7 Mmt |

| 0.37% |

Apart from the above, HBM has three exploration properties namely Maria Reyna (historical copper grades ranged between 2-6%), Cabalitto (historical copper grades at ~2.3%), and Kusiorcco which are within trucking distance of the Constancia mine. Additionally, the company owns 100% of the Llaguen project (near Trujillo city, Peru) for which it recently released an initial resource estimate comprising ~271 Mmt ore at 0.33% copper under the Indicated resource category, and a further ~83 Mmt ore at 0.24% copper under the Inferred resource category.

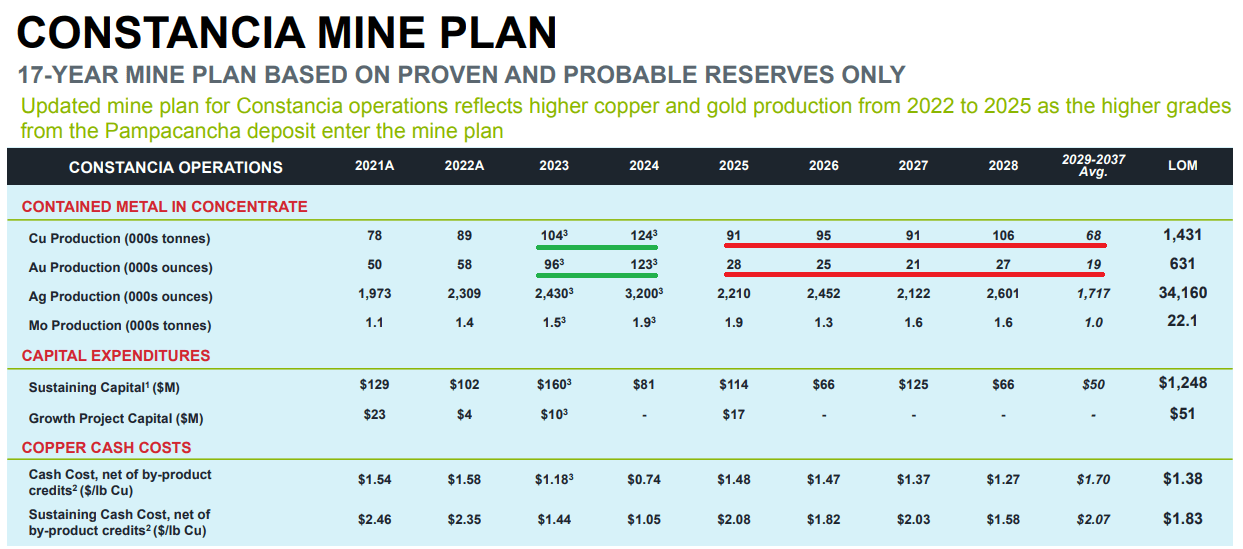

It's pertinent to note that even though HBM slashed its total exploration budget for the Peruvian assets from ~$25 MM (in 2022) to ~$15 MM (in 2023), it started early exploration activities at Maria Reyna, and Cabalitto deposits to support drill permit applications for these properties . I believe these exploration activities are important for the expansion of mineral reserves/resources in the medium term especially when HBM's existing Constancia operations are likely to witness a gradual decline in production after FY 2024 (Figure-5). Nonetheless, 2021 scoping studies at the Constancia Norte Underground revealed two high-grade skarn lenses (North Skarn and South Skarn) at this underground deposit which is expected to supplement Constancia's open-pit production from 2029.

{kind=link}

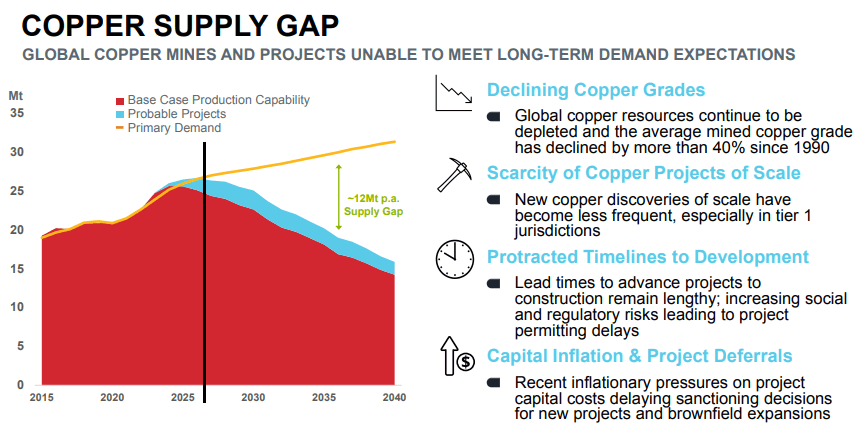

Another reason why I believe HBM should expand its copper production from these exploration properties is that over the medium term, copper's primary demand will be adequately met with copper production from existing and future copper projects worldwide (expected till 2026). Thereafter, copper demand will exceed supply to the extent that a supply gap of ~12 Mmtpa (read: Million metric tons per annum) will be created by 2035, resulting in a significant potential hike in copper prices. Since HBM's average copper production from the Constancia mine is expected to shrink to only 68 kT from the 2029-2037 period, it's easy to comprehend why fresh sources of copper production are necessary for HBM to take advantage of a potential copper supply gap over the long term.

Long-Term Copper Supply Gap - Wood Mackenzie's Report Q3 2022 - Source: HBM (Figure-6)

{kind=link}

2) Manitoba Operations: HBM's Manitoba operations refer to the Lalor underground mine (4,650 tpd processing capacity) located in Snow Lake, Manitoba which comprises gold-zinc-copper VMS (read: Volcanogenic Massive Sulfide) deposits and has a 16-year mine life. Two nearby processing mills process different types of ore feed from the mine; the Britannia Mill processes gold-rich ore, while the Stall Mill processes base metals ore.

The following two catalysts are expected to provide an operational advantage to the production from the Lalor Mine during 2023:

- During Q2 2023, HBM plans to complete the initial phase of the Stall Mill recovery improvement program to increase gold and copper recoveries.

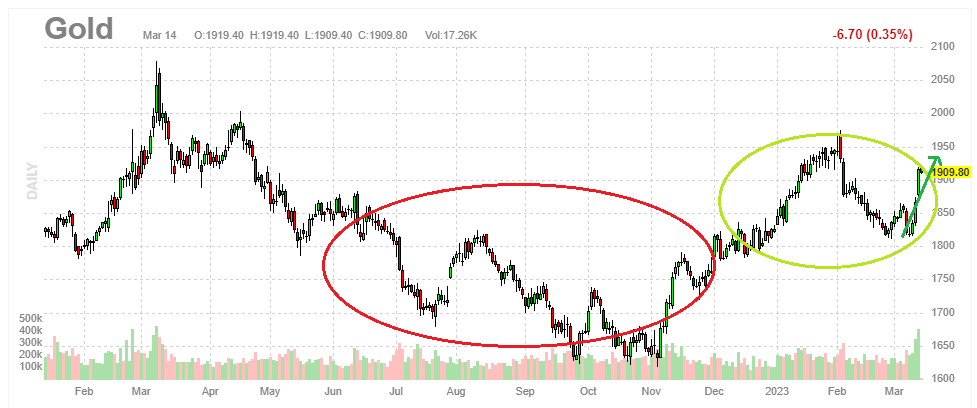

- During 2023, HBM plans to operate the new Britannia gold mill at 10% above nameplate capacity to deliver higher gold production. I think it's a good decision, particularly in light of the strong recovery in gold prices that we have recently witnessed (gold prices have had a relatively good start to 2023 compared with the second half of 2022; Figure-7).

{kind=link}

Exploration opportunities: In addition to the potential for Lalor's mine life extension (a total of 12 holes and ~20,000+ meters of drilling are planned for 2023 at the Lalor deep targets), HBM owns a couple of other exploration projects. Most of these projects are located near the Lalor Mine. These projects include the 1901 deposit, WIM & 3 Zone, New Britannia, Watts, Pen II, and the Talbot deposits.

Manitoba Exploration Projects - Source: HBM (Figure-8)

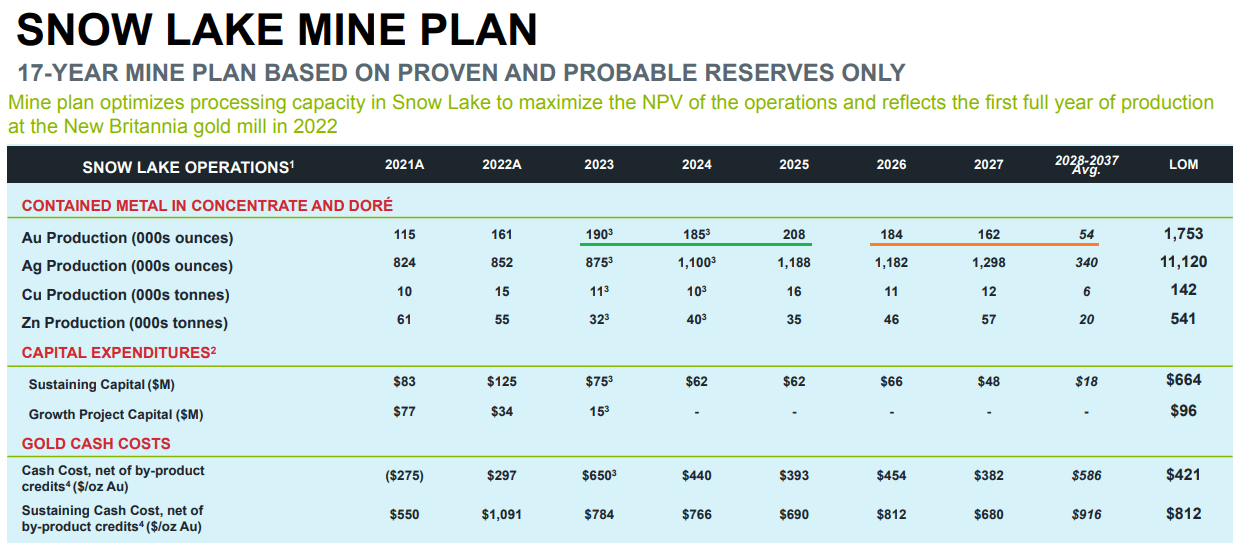

Snow Lake's 17-year mine plan (Figure-9) reveals that production will increase from 2023-2025 and will gradually decline after that. Note that the mine plan is based on P&P (read: Proven and Probable) reserves only which include ore tonnage of ~17.2 Mmt at average grades of 0.64% copper, 3.5% zinc, 3.9 g/t gold, and 28.7 g/t silver.

Besides, the property hosts Inferred resources of ~8.06 Mmt at average grades of 1.13% copper, 2.10% zinc, 3.9 g/t gold, and 28.0 g/t silver and I believe that the conversion of those inferred resources into reserves through exploration will positively impact production from Snow Lake (Lalor mine).

{kind=link}

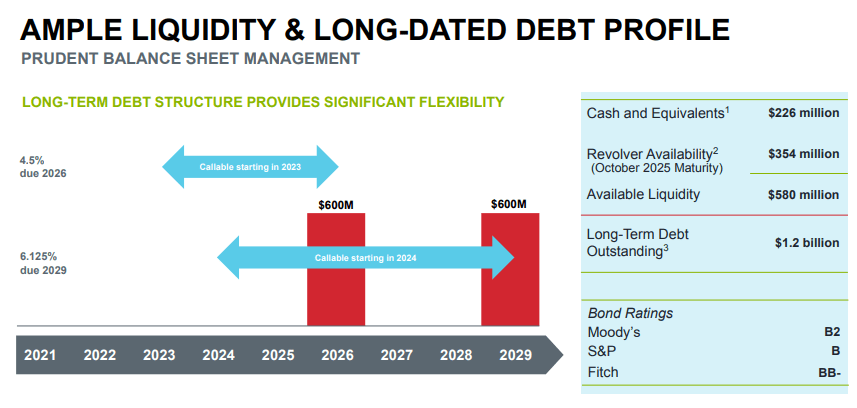

Be Wary Of The Long-Term Debt

So far it seems that HBM is a perfect investment capable of delivering suitable long-term growth. It is if we ignore that debt. However, HBM had a total LTD (read: Long-Term Debt) of ~$1.2 BB ($1,184.16 MM to be exact). At present, HBM's LTD is ~5.3x its cash position. The company's cash position declined from ~$271 MM in 2021 to ~$225 MM in 2022. Besides, the company's CFOs (read: Cash Flow from Operations) also witnessed a decline in 2022 ($391.7 MM) compared with 2021 ($483.9 MM).

{kind=link}

The ~$1.2 BB LTD is bifurcated into two series of ~$600 MM callable bonds maturing in 2026, and 2029. Besides, the company has a ~$380 MM RCF (read: Revolving Credit Facility) maturing in 2025 out of which ~$354 MM remains unutilized.

In my view, despite strong metal production anticipated during the 2023-2025 periods (refer to Figures 5 and 9) together with the recent overall positive momentum in metal prices, HBM will still find it challenging to repay the first tranche (~$600 MM) of LTD maturing in 2026.

I say so because:

- We cannot anticipate the metal price trajectory (copper and gold) over the next 3 years. Meanwhile, it would be even more challenging to repay the second tranche of the $600 MM debt that matures in 2029 because the mine plans in Figures 5 and 9 show average production to gradually decline after 2026.

- HBM has planned CAPEX of $300 MM for 2023 (2022: $343 MM) together with planned exploration expense of $20 MM (2022: $35 MM). On average, we can expect HBM's total CAPEX (sustaining and growth) plus exploration budget to vary within the range of $200-300 MM for the next 3 years. This will also impact the FCF (read: free cash flows) available to pay off the near-term maturing debt. On that note, Figure-11 shows that HBM's FCFs have grown to ~$180 MM at the end of FY 2022 but it was a rough rollercoaster ride during those past 3 years.

HBM's 3-year FCF generation (Figure-11)

Can Hudbay's US portfolio alleviate the challenges posed by LTD? Not really.

HBM's US-based portfolio comprises the Copper World Complex (or CWC) property in Arizona and the Mason property in Nevada.

Copper World Complex

Mining Attraction: CWC comprises the East and the West zones, and is planned in two phases. Phase I has a mine life of 16 years, which could be extended to 44 years under Phase II. Under Phase I, annual copper production is expected to be ~86,000 metric tons with first quartile cash costs of ~$1.15/lb and sustaining cash costs of ~$1.44/lb. Under Phase II, annual copper production is expected to extend to ~100,000 metric tons. CWC will incorporate open-pit operations.

Using a discount rate of 10%, HBM expects CWC to generate an after-tax NPV of $741 MM under Phase I, and a total after-tax NPV of $1,296 MM under Phase II.

I think the 10% discount rate is appropriate because:

- Base metal projects like CWC should typically be discounted within the range of 8-10%; the more risk in a project, the higher the rate (in contrast, precious metal projects can be discounted between 6-8%).

- The project permit is in progress, and the project is in the beginning stages and represents a significant risk element.

- Ongoing exploration activities could impact the resource definition including grades.

In terms of M&I (read: Measured and Indicated) resources, the CWC deposit has an ore tonnage of ~1,200 Mmt at an average grade of 0.41% copper. As noted earlier, HBM's existing Constancia mine has M&I tonnage of ~242 Mmt at 0.22% copper. It's easy to see that the CWC project provides a significant opportunity for growth in terms of resource volume, and ore grade compared with HBM's existing flagship copper project.

Near-Term Catalysts: I see the following near-term catalysts for CWC:

- HBM expects the project PFS (read: Pre-Feasibility Study) to be completed in Q2 2023, which will incorporate the results of exploration activities and better define the project's mining dynamics.

- For better management of liquidity, HBM seeks a minority JV partner for completing the project's final FS (read: Feasibility Study) which is targeted in 2024.

- Meanwhile, HBM expects to receive the remaining key state-level permits (Aquifer Protection Permit, and Air Quality Permit) for the project during 2023 and plans to run a bulk sampling program on the project after receipt of state permits.

In my view, at least 2 out of the 3 near-term catalysts mentioned above are beyond HBM's control and could impact the share price, going forward.

Challenges: I see the following challenges/risk factors associated with the CWC project:

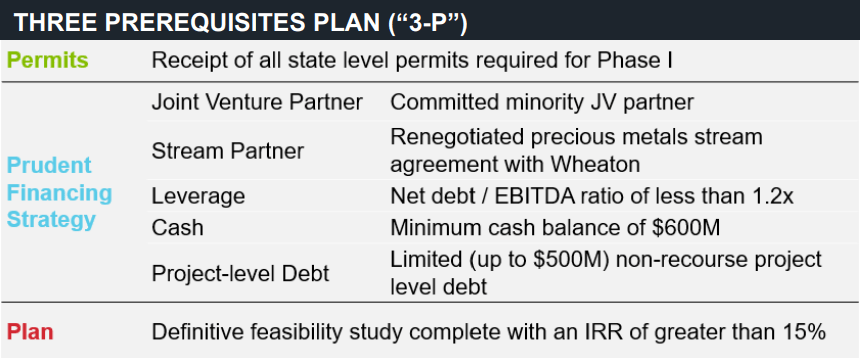

- The project development CAPEX of ~$1.917 BB (to be spent across 3 years; $338 MM in year-1, $1,007 MM in year-2, and $572 MM in year-3) is a significant number compared with HBM's existing liquidity profile (discussed earlier). It would be a challenge for HBM to successfully execute its CWC financing strategy (Figure-12) which includes arranging additional debt of up to $500 MM. The FED's recent hikes will increase borrowing costs. Further, execution of CWC Phase II will require an additional development CAPEX spend of ~$885 MM.

- Another notable challenge is to convince project opponents . This report on AZ Mirror provides a good background on the opposition to the East side (formerly called the 'Rosemont project') of HBM's CWC project. It's worth noting that HBM had recently booked a pre-tax $95 MM impairment loss on certain capitalized costs related to the Rosemont project, as these costs are determined to be no longer recoverable. HBM's focus is to obtain state permits for the West side of the CWC project which includes private land acquired for prospecting and is subject to relatively fewer environmental regulations compared with the East side.

{kind=link}

Mason Project

HBM's 100%-owned Mason project in Nevada is another interesting prospect for the future. It encompasses ore tonnage of ~2,200 Mmt at an average grade of 0.29% copper. Mason is a long-life project (LoM=27 years), with LoM sustaining cash costs expected to be ~$1.76/lb copper. The project is expected to deliver ~112,000 metric tons of copper in each full year of production. The project's base case expected after-tax NPV (at 10%) is ~$1,191 MM using a long-term copper price of $3.50/lb (spot copper=~$3.90/lb). These estimates are based on the project's 2021 PEA (read: Preliminary Economic Assessment) and are subject to revision in further prospecting studies.

While HBM's Mason strategy incorporates an analysis of the geophysical and geological data to plan a drill program to test high-grade skarn deposits, I see there's significant work to be completed (permits, CAPEX funding, results of exploration and future prospecting studies, etc.) before this project could notably influence an investment decision in the company.

Investor Takeaway

Long story short, HBM's existing mining assets in Peru and Canada do provide room for operational improvement in the near term . However, the first tranche of debt is maturing in 2026 which indicates that HBM's liquidity position will remain under pressure during the intervening period. Meanwhile, any significant or persistent decline in copper and gold prices will further deteriorate the situation for HBM.

HBM's US-based CWC project provides room for significant production growth in the long term but the outlook remains challenged by concerns such as project development CAPEX, state permits, and project opposition from environmental groups. Based on the above, I believe HBM is a 'hold'.

For further details see:

Hudbay Minerals: Things To Consider Before Jumping On The Bandwagon