HDSN - Hudson Technologies' Big Year Approaches

2023-12-12 16:45:49 ET

Summary

- Hudson Technologies is the largest independent source for refrigerants in the US, with a 35% market share.

- The AIM Act, starting in 2024, will create increased demand for reclaimed refrigerants, benefiting Hudson.

- Despite a decline in Q3 earnings, Hudson is on track to achieve its revenue target of $400 million by 2025.

Introduction

Most investors who bought Hudson Technologies ( HDSN ) stock at any time in the past few years and have held on to their shares are surely in the green. Probably, by a very significant percentage. In cases like this, some may think about locking in gains. Understood, a win is a win and if one has made a profit, hats up. However, I have shared elsewhere how I learned from Peter Lynch that it is not enough of a reason to sell a stock just because it went up. It is rather more rewarding and more profitable to assess whether that business is compounding and at what pace to see if the stock is simply following along.

So, since in March 2023 I bought the dip when Hudson was trading below $8 and am now up around 60% just on that buy, not counting the others, I want to go over my bull-case once again to see if it holds up or not.

The Company

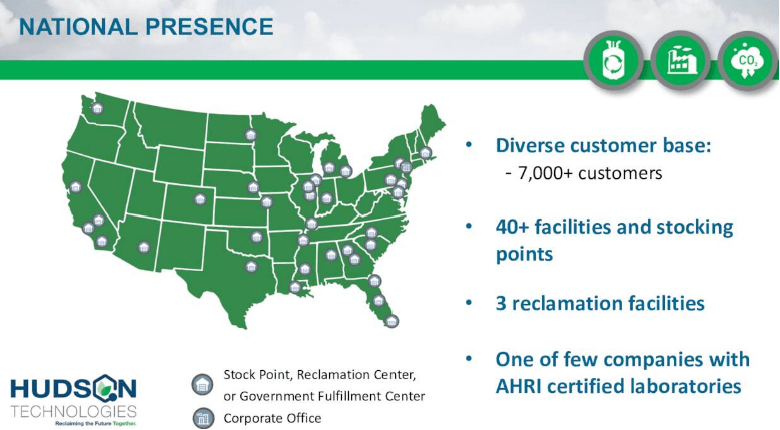

Though Hudson's market cap is around half a billion and the company can thus be considered small, its business model and its way of operating are full of surprises and interesting things to understand. In short, Hudson focuses on refrigerant gas sales and reclamation services making it the largest independent source for refrigerants (CFC, HCFC, HFC, HFOs) in the U.S. As we can see below, Hudson has a national presence with more than 40 facilities and stocking points. It also owns two of the only four AHRI certified laboratories in the country.

{kind=link}

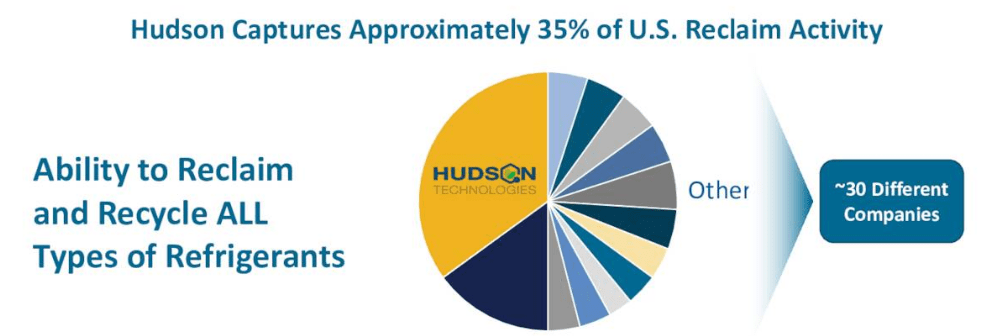

In the U.S. it has a 35% market share, making it the leader in a highly fragmented market.

{kind=link}

Hudson Technologies has developed its own chemical know-how to remove the moisture, oils and other contaminants frequently found in refrigeration circuits. Moreover, the company owns the ZugiBeast system , protected by a patent, which makes Hudson different from any other competitor. The company explains that the machine works similar to kidney dialysis in that the building chillers can continue operating while the refrigerant is diverted to the ZugiBeast cleaning process. As the company often says, its technology is "agnostic", meaning it can work with any type of refrigerant, being it legacy CFCs or today's HFCs or tomorrow's HFOs.

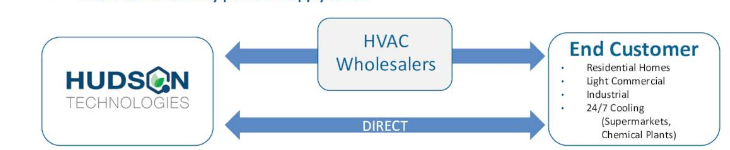

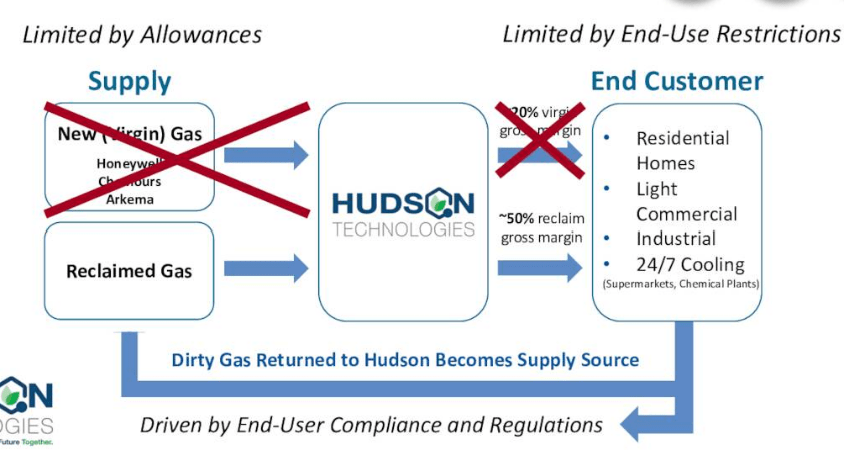

Hudson Technologies has therefore a double role in the refrigerant supply chain, as the company regularly points out in its presentation. In fact, on one hand, it is a refrigerant supplier, on the other, it is a reclaimer. In this way it is both at the beginning and at the end of the cycle. As I have written before , Hudson Technologies is able to convert every end cycle into the start of a new supply.

{kind=link}

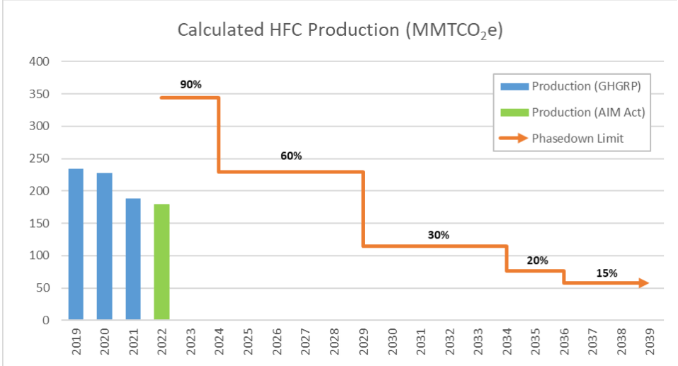

Starting in 2024, an extremely important HFC opportunity begins because of the AIM Act. As the EPA explains, in 2024 the HFC phasedown schedule mandates a 40% baseline reduction in virgin HFC production and consumption allowances.

{kind=link}

What does this mean? Since HFC and other legacy refrigerants won't be manufactured, the HVACR industry still needs them because it uses them in their equipment. Hudson becomes even more important because it is not an easy task to replace AC systems whose lifecycle is 15-20 years and that can still run effectively for several years. Hudson currently estimates the install base of HSC equipment stands at 125 million units. So, we can expect enhanced demand for reclaimed refrigerants. Moreover, several States are making the regulatory environment around refrigerants more stringent to encourage reclamation. Since 2000, Hudson has reclaimed over 72 million lbs of refrigerant, avoiding 84 million tons of CO2 equivalent GHG emissions. Therefore, Hudson can be also viewed as a green play which sees favorable market conditions due to environmental-friendly laws and policies.

Now, because of the Aim act, the supply chain sees some changes that benefit Hudson, as shown below. Since the supply will be limited by allowances, reclaimed gas will be the go-to solution and Hudson is expected to see demand increase up to the point the company said during the last earnings call it is ready to work on two shifts, if necessary. As Hudson plays a unique role it earns a larger gross margin on reclaimed gases rather than virgin HFCs.

{kind=link}

Risks

Hudson faces one major risk: refrigerant gas volatility. In 2017, it almost went bankrupt because of this. In fact, Chinese suppliers flooded the market with virgin refrigerants before they were phasedowned. This led to a collapse of reclaimed refrigerant prices and Hudson had to sell its reclaimed refrigerants well below the price it paid just to reclaim them. This is why it is important to understand how Hudson manages its inventory. Since the company uses FIFO which has the advantage of reporting the inventory value carried on the balance sheet as close as possible to the current market value. At the same time, FIFO has the disadvantage of matching the revenue from the sale of inventory with an old and possibly outdated cost. In case the market price of Hudson's inventory is less than the related cost, the company could need to write down its inventory.

Now, the risk of Chinese supply was a once-in-a-time risk. Refrigerant gas price volatility is still a risk, but the AIM Act should create the conditions to keep prices from falling unexpectedly.

Moreover, the company got its balance sheet in perfect shape in case of any surprise. Just a few months ago, Hudson announced it paid down all its remaining $32.5 million of loan debt well ahead of its 2027 maturity. After this news, I revised my target price upward. Needless to say, this will help the company save money on interest expense and help it grow its free cash flow. For us, as investors, this is nothing but good news.

Q3 earnings

Hudson's Q3 report was a miss, with revenue of $76.5 million, down 14.5% YoY and missing by $8 million (-10.5% vs forecast). Gross margin was 40%, compared to 49% in Q3 2022. Moreover, the company's tax rate was 26% while in 2022 the effective tax rate was 11.9% due to the release of Hudson's valuation allowance.

If we look at the first nine months of the year - the traditional cooling season - we see that the company reported revenues of $244.2 million, down 12% YoY. The decline was explained by declining selling prices for certain refrigerants and a slightly lower sales volume. This leads to a decrease in inventories, as I explained above. Moreover, the cost of sales actually increased a bit YoY to $45.9 million vs. $45.3. This means that in this past quarter, Hudson sold those reclaimed refrigerants at a lower price that were bought at a higher price compared to Q3 2022. This is why gross margin came in at 40% against 53% in the first nine months of 2022. Still, 40% is above the company's target of 35%.

The 2023 cooling season, which has now more or less ended, can be thus viewed as more challenging than 2022. On one side, refrigerant prices went down, following the general decline in price of many commodities. On the other, the late arrival of warmer weather impacted demand and volumes.

As Hudson's management explained during the earnings call:

The primary driver for the comparative decrease was a 27% decline in the sales price for certain refrigerants when compared to the third quarter of 2022. Specifically for the nine month period, we saw a decline of approximately 17% in the sale price of certain refrigerants as compared to the first nine months of last year. In addition, the late arrival of warmer weather to many parts of the U.S., which impacted demand for certain refrigerants, slightly impacted volume unfavorably for this season. Even with the significant pricing headwinds, we achieved our gross margin of 40%, which is slightly higher than our long-term targeted gross margin levels.

We may worry about prices falling even more, but this issue was addressed during the earnings call and Hudson reported it is already seeing a little rebounding in HFC pricing which may indicate what 2024 will look like:

we saw the lower pricing condition continue pretty much through most of the nine-month season going from somewhere above $10 a pound to probably a low of about $8 a pound in general for HFCs.

Recently, we've seen a little rebounding in HFC pricing as we exit in Q3 starting into Q4. We feel pretty good about where the pricing is at the moment. It's headed back towards that $10 a pound, it looks like, price that we sort of started the year at.

Nonetheless, even though Hudson is seeing a decline compared to 2022, this year will in any case be its second best of the past decade, with revenues that could be above $280 million. Considering the company is targeting to reach $400 million in revenue by 2025 with a gross margin around 35%, I see a company on track to achieve this goal, thanks to the changing market conditions we will see starting in January 2024.

One thing I don't appreciate much about Hudson, though yet it doesn't seem that meaningful, is the higher stock compensation expense: for the first nine months of 2022 it was $830,000 while now it is $2 million. What I don't like is not the amount, but the big percentage increase which brings SBC at 4.2% of the company's current net income. However, considering the company saved YoY almost $6 million of cash paid during period for interest, we can give Hudson a pass this time. But we will need to monitor SBC closely because it may be a way of taking advantage of Hudson's stock appreciation and make Hudson's shareholders pay the extra compensation for some of Hudson's employees. Per se, if the company performs well, it is not a problem. But we have seen how SBC can get out of control through lessons learned from other companies.

Valuation and conclusion

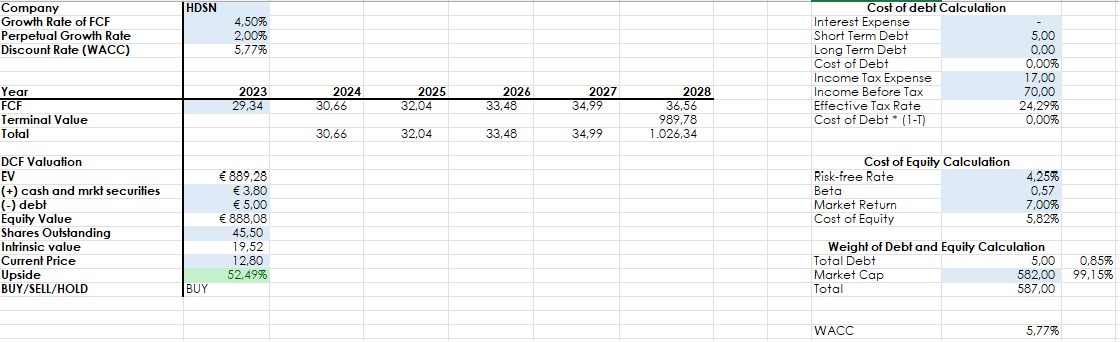

Hudson is still a very alluring buy with a 50+% potential upside. By plugging in my discounted cash flow model the new financial data available after the report, we can see what Hudson's cash flows over the next five years could look like. The company should make over $30 million in FCF every year considering a moderate FCF growth rate assumption of 4.5%. Considering the new environment for refrigerant supply should support higher selling prices, I think it is reasonable to expect a higher growth rate. But let's keep it moderate for the time being. As a perpetual growth rate, I used a traditional 2%. The other metrics come from Hudson's financials directly. To calculate its WACC, I also used 7% as the average expected market return and thus calculate the cost of equity.

{kind=link}

With the company's market cap being still below $600 million, we are looking at a business whose future prospects seem bright and whose cash generation should be reliable and protected from potential competitors stepping in. This is why I think Hudson is not a short-term play, though it offers interesting rewards over the short-term as well, but rather a play to hold until the whole AIM Act unfolds its requirements. Buy rating confirmed for me.

For further details see:

Hudson Technologies' Big Year Approaches