E - Huge Dividends From These 3 REITs

2023-10-16 08:05:00 ET

Summary

- REITs have crashed and are now heavily discounted.

- REITs now offer up to 12% dividend yields in some cases.

- We highlight 3 high yielding REITs that we are buying.

Over the 2 years, REITs (VNQ) have seen their share prices crash by nearly 40% even as most of them kept hiking their dividend payments:

As a result, there are now many REITs that offer 8-12% dividend yields.

Typically, such high yields are only offered by REITs that present significant risks due to overleverage or poor management.

But today is the exception.

The REIT market has just gotten so cheap that you can now earn such high yields even from high-quality REITs that enjoy good prospects.

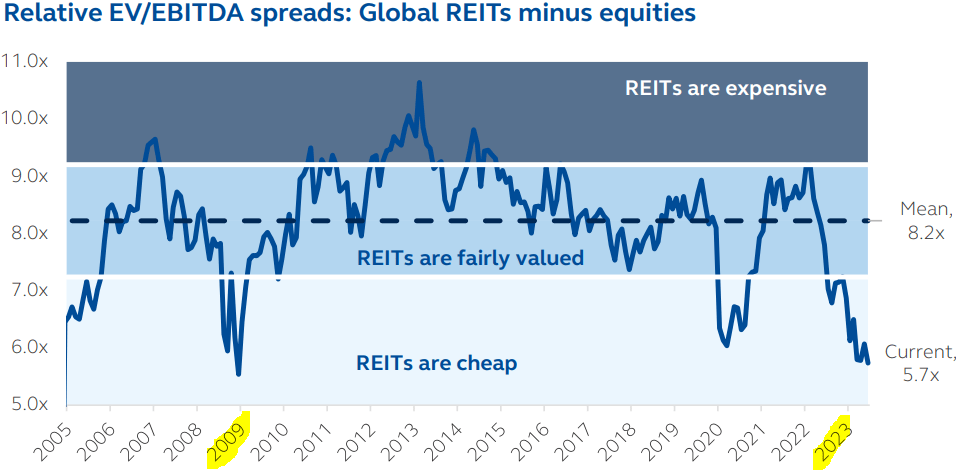

According to Principal Asset Management, REIT valuations are today the lowest since the great financial crisis so if you are looking to build a passive income stream, now is the time to take an interest in REITs:

{kind=link}

In what follows, we will highlight 3 REITs that offer huge dividends that are sustainable and set for growth:

NewLake Captial Partners (NLCP)

NLCP is one of just a few REITs that specialize in Cannabis cultivation facilities. The other two are Innovative Industrial Properties (IIPR) and Power REIT (PW).

NewLake Captial Partners

Its share price has dropped by over 50% even as it kept hiking its dividend, and as a result, its dividend yield has now reached 12%:

{kind=link}

The shocker here is that NLCP is one of a few REITs that has zero debt. In fact, it has a large net cash position that represents about 13% of its market cap.

Despite paying such a high yield, the dividend represents only 80% of their cash flow and since they have no debt, the cash stack is piling up.

The company is now also using this cash to buy back shares while they are discounted. They recently finished their $10 million buyback plan and immediately initiated a new one. Here is what the CEO of the company said recently about their buybacks:

"We continue to believe there is compelling value in our stock and while we continue to have conviction around the cannabis sector, the opportunity to invest in our stock was particularly attractive. The authorization by our Board of an additional $10 million under our share repurchase program allows us to continue to be opportunistic in stock repurchases while working to deploy additional capital into sale leaseback transactions," stated Anthony Coniglio, NewLake's President and Chief Executive Officer.

NewLake Captial Partners

Why is it then priced at such a high yield?

The main reason is an overreaction to rising interest rates. It caused all REITs to sell off, but investors appear to have overlooked that NLCP has no debt and owns higher cap rate properties that are less sensitive to rising interest rates.

The second reason is more reasonable and it is that the cannabis sector (WEED) is today out-of-favor. Operators are facing challenges and in select cases, it has caused tenants to miss rent payments.

But this is nothing new.

The cannabis property sector has always been somewhat riskier and this is well-reflected in the higher cap rates that NLCP has been getting. It is inevitable that it will occasionally run into tenant issues.

But what the market appears to have overlooked here is that NLCP focuses on properties that are located in limited license states, which significantly reduces risks. Tenants come and go, but the property should retain its value since these licenses are limited and the demand for cannabis is rising rapidly.

The public market doesn't like the occasional bumpiness, but the business model is more resilient than what the company is getting credit for, especially considering that they have zero debt and a large cash position.

Offering a 12% dividend yield and buying back stock, this is a Strong Buy for high-yield-seeking investors. If you want some cannabis exposure, you will have a hard time finding a more compelling opportunity.

EPR Properties (EPR)

EPR is a net lease REIT just like Realty Income (O).

But instead of focusing on traditional net lease properties such as CVS (CVS) pharmacies and Dollar General (DG) grocery stores, EPR is buying experiential net lease properties such as:

- TopGolf golf complexes

- AMC movie theaters (AMC)

- Water parks

- Ski resorts

- Etc.

EPR Properties

Its share price crashed at the onset of the pandemic and it has failed to recover since then:

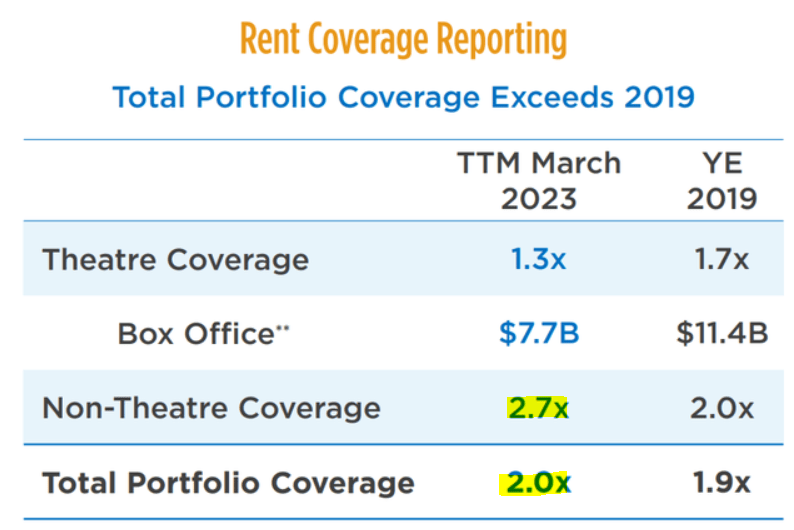

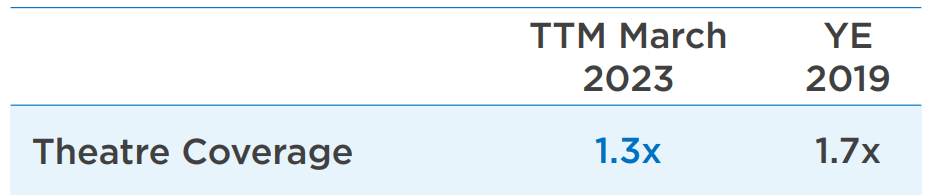

But its business has! In fact, most of its tenants are today earning far more profits than they did prior to the pandemic and this is well-reflected in EPR's high rent coverage ratios:

{kind=link}

The only property sector still lagging behind is movie theaters, and this is the main reason why EPR is still discounted.

About 25% of its properties (as measured by NAV) are invested in movie theaters and the market fears that these assets will never recover.

I disagree.

The recovery is actually well underway. EPR owns some of the most productive theaters in the nation and those are already profitable at the property level, and the recovery is likely to continue given the huge recent successes of Barbie and Oppenheimer.

EPR Properties

If anything, the pandemic proved that high-quality movie theaters are here to stay. Major studios like Disney (DIS) and Warner Bros (WBD) got to experiment with digital strategies and they all came back to theaters with the conclusion that they remain the best platform to monetize new blockbusters.

That's because digital strategies lead to pirating, people are not willing to pay as much to watch at home, and even if one pays, the rest of the family/friends watch for free.

Therefore, if you like new blockbusters (most of us do), then theaters remain needed. Even Amazon (AMZN) and Apple (AAPL) recently guided to invest billions into new movie releases for theaters.

Besides, EPR is the landlord, not the operator. EPR earns steady rental income from 10+ year-long leases that include annual rent hikes. Therefore, you don't need to be ultra-bullish in theaters for EPR to do well. You just need them to do well enough to pay their rent and today, rent coverage is already positive based on depressed figures.

{kind=link}

Even then, EPR is today priced at an 8% dividend yield and this high yield is especially attractive considering that it is backed by a low 66% payout ratio and EPR has guided to grow its cash flow by 9% in 2023.

I believe that as movie theaters continue their recovery and EPR keeps diversifying away from this sector, its valuation multiple will also expand from its low levels. If it just expanded from 8x to 12x, it would still be cheap for a high-quality REIT, but that would unlock a 50% upside for investors who buy it today.

The combination of high yield, low payout ratio, strong growth, and upside potential makes EPR a very compelling choice for high-income-seeking investors.

Healthcare Realty (HR)

I will keep this one short because the thesis is pretty simple.

HR owns a portfolio of Class A medical office buildings, has a strong BBB rated balance sheet, and has attractive growth prospects.

However, its share price has crashed recently and as a result, it is now priced at an 8.7% dividend yield, which is its highest yield ever:

It has dropped so much because the market appears to put medical office buildings in the same basket as regular offices.

In reality, medical office buildings are performing far better.

HR has actually guided for an acceleration in its same property NOI growth in the coming years and expects this to result in 5%+ FFO per share growth going forward.

Its properties are more resilient than your typical office building because:

- They have unique characteristics that serve a medical use. While offices can be converted in some cases, it is typically too expensive.

- They are profit centers for their tenants, making them far more dependent on these specific properties.

- HR's properties are in medical clusters - a clear barrier to entry - and they are mostly located in rapidly growing sunbelt markets.

{kind=link}

For these reasons, we think that the sell-off has been way overdone here and the market is wrong to perceive HR as a regular office REIT. Its valuation is not dissimilar from the likes of Boston Properties (BXP), but its fundamentals are far stronger:

| BXP |

| HR |

| FFO Multiple |

| 8.5x |

| 8.9x |

| P/NAV (consensus estimates) |

| 0.66 |

| 0.67 |

We think that this is a clear mispricing, and as HR keeps growing its same property NOI, the market will likely eventually reprice HR at closer to 15x FFO, resulting in a 50%+ upside to investors who buy it today. While you wait patiently, you will earn a near 9% dividend yield.

Bottom Line

The REIT market is today more opportunistic than it has been in a decade.

Dividend yields are very high.

Growth is steady.

And the upside potential is very significant.

The time to buy is when valuations are low following a crash. That's today.

For further details see:

Huge Dividends From These 3 REITs