BOSSY - Hugo Boss: Good Performance High P/E

2023-05-07 00:03:30 ET

Summary

- The German fashion and accessories company Hugo Boss has seen impressive sales growth and margin improvement in Q1 2023. It has also upgraded its 2023 outlook.

- The company's ongoing investments programme seems to be paying off, though it could tell on margins at a time of persistent inflation and weak demand in its key markets.

- Its TTM and forward P/Es also look stretched for now, especially in comparison to affordable luxury peers. It is a Hold for now.

Fashion and accessories brand Hugo Boss AG ( OTCPK:BOSSY ) has seen a significant 26% increase in share price in 2023 so far. In fact, its price has been rising since November last year with a few hiccups but in total, it has been a fairly steep increase.

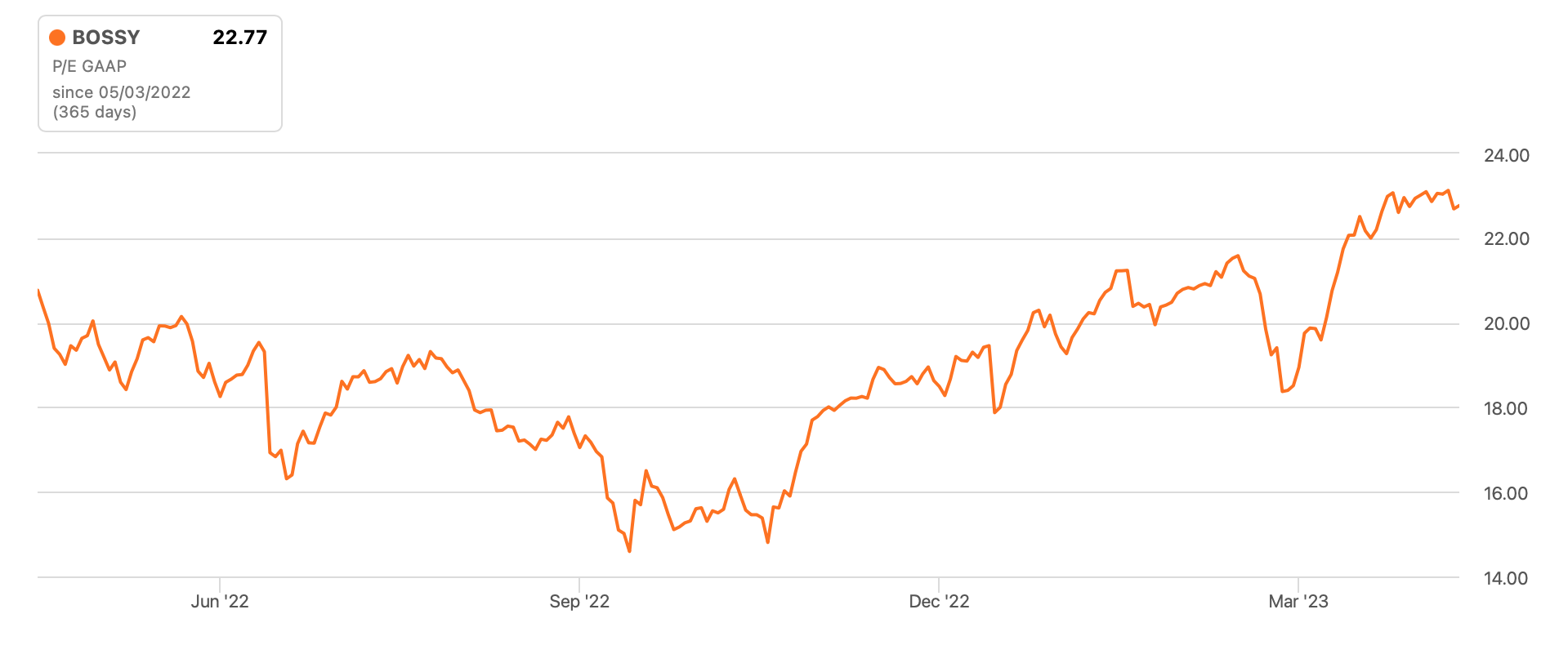

Typically such increases are matched with a corresponding rise in the price-to-earnings (P/E) ratio as well, simply because price rises are not matched with equivalent earnings growth. And that is the case here as well. Last November Hugo Boss was trading at a P/E 15.6x. It is now almost 23x, a fair bit higher than the 15.4x for the consumer discretionary sector (see chart below).

{kind=link}

Here I take a closer look at the company’s performance after its recent earnings release and how it compares to its closest peers in terms of market valuations to determine whether its price can continue to rise going forward.

Strong performance

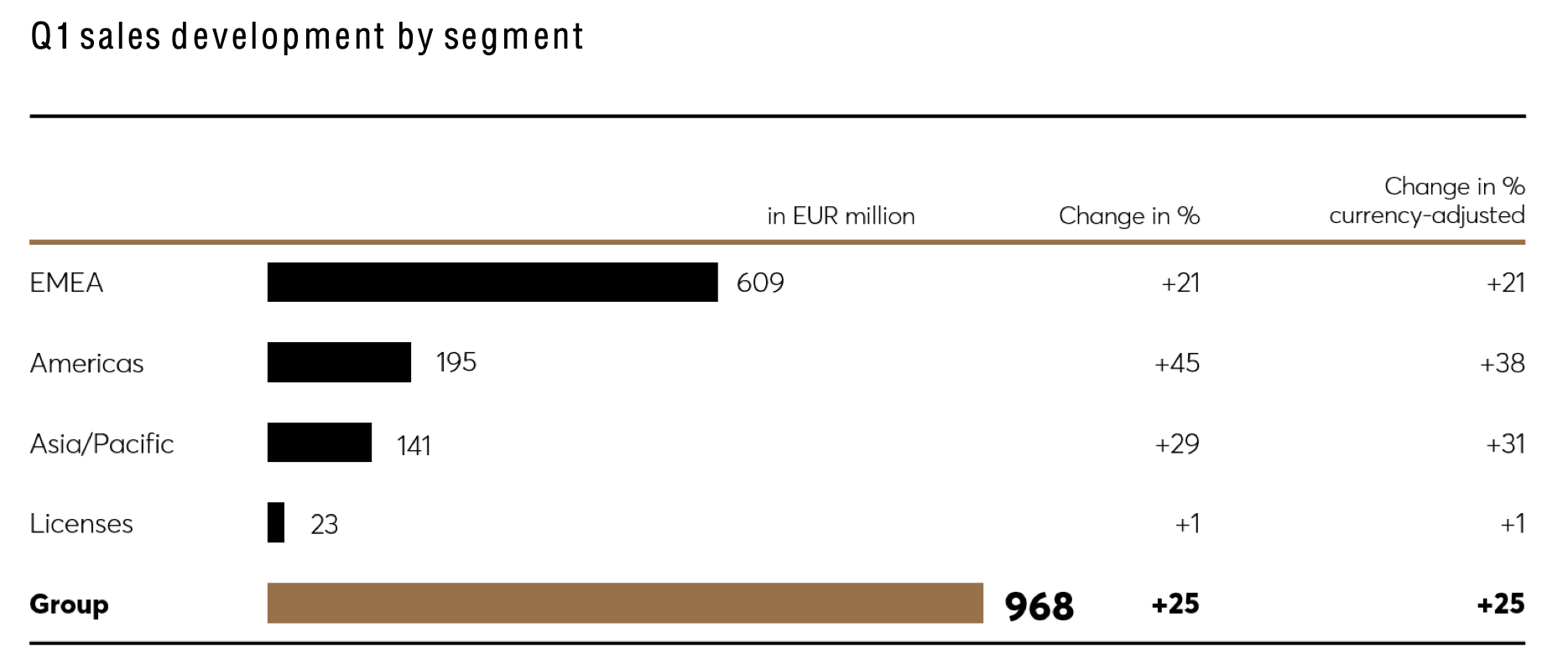

The company’s just released figures for the first quarter of 2023 (Q1 2023) continue to stay strong after a robust 2022. Both its brands, Hugo and Boss, showed double-digit growth resulting in group sales growing by 25% year-on-year (YoY). Significantly, all its geographical markets rose in double digits too, led by the Americas and followed by Asia Pacific (see chart below). EMEA showed good growth too, with notable performances from the markets in UK, Germany and France.

{kind=link}

The improvement in Asia Pacific growth was driven by the improvement in the China market, up by 25% on a currency-adjusted basis. However, unlike many other international fashion brands, the company does not have a big China market. In fact, the Germany based company’s biggest market is the EMEA, accounting for 63% of its sales.

This is important for 2023 when Germany and the UK, in particular, are flagged as likely to be mildly recessionary this year. And recessions as we know, are bad news for consumer discretionary companies. Especially those like Hugo Boss, that do not have much pricing power. The company’s operating margin, which gives a sense of this power, is at a fairly low 6.7% for Q1 2023. It has improved from the 5.2% Q1 2022, to be sure, but it is still low. Also, it is in sharp contrast with the very healthy 61.4% gross margin.

Improved margin expectations

But, after its latest results, the operating margin is expected to increase to around 9.6%, a 40bps increase from 2022. In fact, it is also a slight improvement over the 9.45% expected in its initial forecast released at the time of its full-year results. There are two points to note here.

It is worth highlighting that it expects an improvement in margins over the course of the year. The company attributes this to EBIT growth expected to come from efficiency gains as part of its ongoing investment programme . The investments have increased its operating expenses, which more than doubled to 27.9% in 2022 from the year before. They continued to rise at a fast clip, by 21% in Q1 2023 as well.

I would be less concerned about the rise in expenses if inflation were under control. But it is not. In fact, in its initial outlook for 2023 (see Page 9 of the link), the company had mentioned it as one of the factors that could dominate the global apparel industry in relation to the pressure it exerts on consumer demand. In other words, there is still a risk to the margins arising from limited pricing power.

Sales growth upgraded

That said, for now, the improved outlook is a significant positive. And frankly, sounds more in line with the performance seen in 2022 and in Q1 2023. The company’s 2022 earnings presentation started with a bang, saying “2022- A record year for Hugo Boss”. It saw a 27% increase in sales. Yet, it had forecast a very conservative “mid-single-digit percentage rate” sales growth at the time. It still sounds muted, to be sure, but significantly better at 10% (see table below).

{kind=link}

What the forward multiples say

Assuming based on its outlook, if net income rises by 15% this year, which is the midpoint of the 10-20% range it expects, and the ADR ratio of 5:1, the company’s forward earnings per share [EPS] are expected to be at $0.71 as per my calculations. This gives a forward P/E of 20.9x, which is in excess of 14x for the consumer discretionary sector.

Now, Hugo Boss is considered a luxury stock, so a closer comparison with peers would be the only fair thing to do. To compare it with peers, I exclude the best known luxury brands like LVMH ( OTCPK:LVMUY ) to Richemont ( OTCPK:CFRUY ), because they are high-end luxury as opposed to affordable luxury, which is where BOSSY comes in. The peers I believe come closest are Tapestry ( TPR ), which owns brands like Coach and Kate Spade and Ralph Lauren ( RL ). But they are trading at far lower forward P/Es of 10.2x and 14.1x respectively. There is a catch here, though. Both companies' sales growth is in no way comparable to Hugo Boss', though both have higher operating margins.

What next?

Even if some of the higher forward P/E is on account of its higher sales growth, it is worth remembering that Hugo Boss actually expects the figure to slow down considerably over the year. Maybe it is just being conservative. But we do not know. Its key markets are expected to slow down this year, and its margins are already weak, especially compared to peers.

At the same time, its price has risen quite a bit in the past few months. It is also interesting to note that since the company’s results earlier this week, its price has barely moved, despite strong growth and a forecast upgrade. I reckon that better performance is already priced in, leaving little room for increase going forward.

Over time, its investments could pay off. It has already seen much better sales growth recently. For reference, over the last decade, its revenues have grown by a CAGR of a much slower 4.5%. But the investment programme continues until 2025, in a period of high inflation and muted economic growth, which could also put further pressure on margins. I would go with a Hold rating for Hugo Boss stock for now.

For further details see:

Hugo Boss: Good Performance, High P/E