BBRYF - Hugo Boss: Tailoring A Transformation

2023-07-31 06:35:21 ET

Summary

- Hugo Boss, a German luxury fashion brand, is known for its timeless elegance and quality craftsmanship.

- Hugo Boss is experiencing a transformation, as management seeks to revitalize the brand. We do not wholly believe in it, although see near-term growth improving.

- Margins are concerning but Q1 implies the business has finally achieved an upward trajectory.

- Relative to peers, the business remains unattractive. When considering its valuation, we do not see sufficient upside.

Investment thesis

Our current investment thesis is:

- BOSSY is in the midst of a transformation project, seeking to cater to current trends under two distinct brands. Although we understand the objective and believe it will be beneficial in the near term, we are not overly bullish as it feels like trend-chasing.

- Financially, BOSSY remains unattractive due to margin dilution. This said, Q1 looks optimistic that an improvement can be made in the coming quarters.

- BOSSY's valuation does not suggest upside at its current price when factoring in its weakness relative to peers.

Company description

Hugo Boss ( OTCPK:BOSSY ) is a German luxury fashion brand that specializes in premium menswear, womenswear, and accessories. With a rich history dating back to 1924, the company is renowned for its sophisticated designs, craftsmanship, and attention to detail.

Share price

BOSSY's share price has performed poorly in the last decade, as declining financial weakness has contributed to a period of lost market share. BOSSY has faced increased competition and changing market dynamics and has been unable to adequately respond thus far.

Financial analysis

{kind=link}

Hugo Boss financials (Capital IQ)

Presented above is BOSSY's financial performance for the last decade.

Revenue & Commercial Factors

BOSSY's revenue has grown at a mild 5% over the last 10 years, a respectable level given the increased competition faced (which we will discuss later). During this period, revenue growth has been relatively consistent, with only one period of negative growth (excl. the impact of Covid-19).

Business Model

Hugo Boss offers a comprehensive range of fashion products, including tailored suits, casualwear, footwear, accessories, and fragrances. The company's focus is on "entry-level" luxury, targeting discerning customers who value quality, style, and exclusivity. This said, BOSSY also operates in the more traditional mass-market segment with more affordable products.

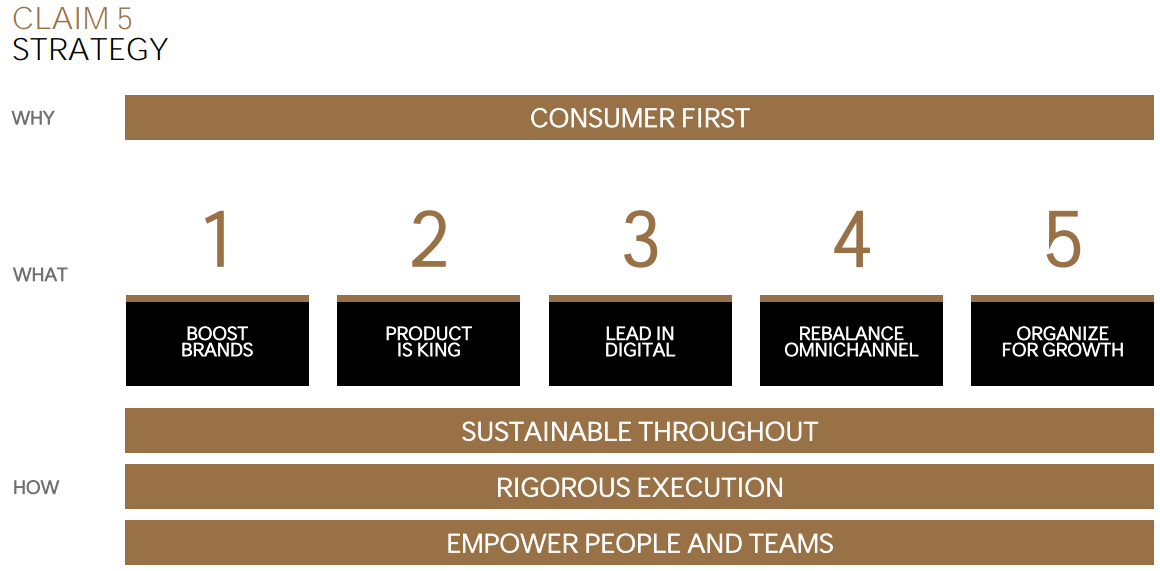

Management has been conducting a transformation exercise, seeking to better position BOSSY in the current market. This involves its "Claim 5" strategy, seeking to improve its brands, develop better products, and develop its operational capability. The goal being to set the company on a sustainable upward trajectory.

{kind=link}

Strategy (Hugo Boss)

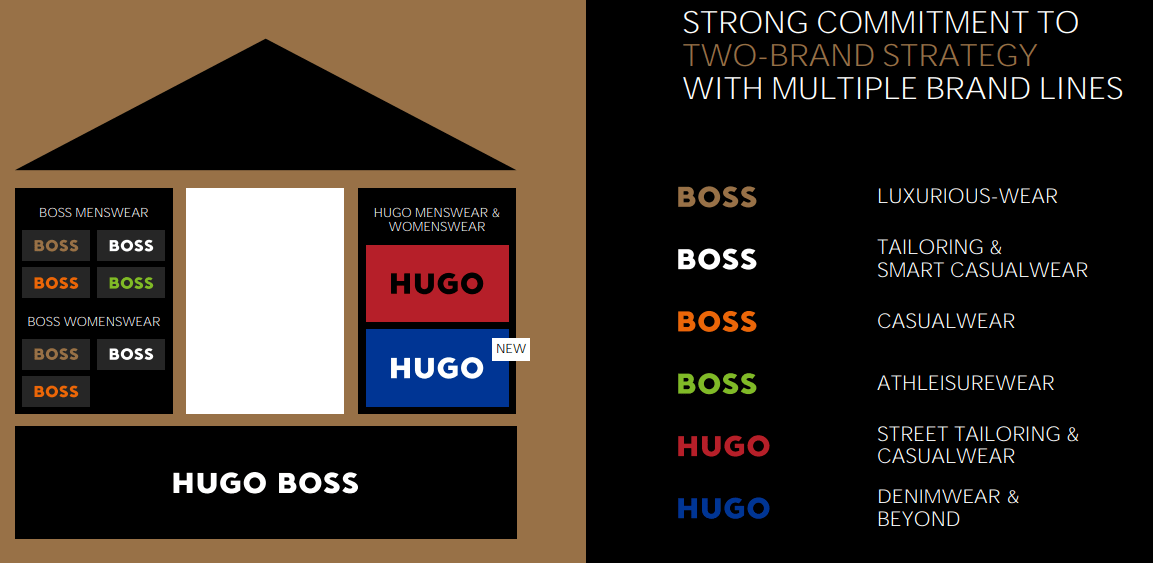

BOSSY has developed its brands into two distinct offerings (having conducted several refreshes and adjustments over the decades). Firstly, there is "BOSS", which is the broad segment but remains true to the "Hugo Boss" image. The objective here is to expand its value proposition across many growing segments, seeking to capture a larger market share of the wider fashion industry. We are not overly keen on this approach, as it feels slightly "scattergun". BOSSY is essentially attempting to capture every segment, regardless of if its brand fits.

Secondly, "HUGO", which is the more laid-back approach, targeting the streetwear, casual, and denim segments. All three have performed incredibly well in the last decade, with streetwear becoming the top-dog. This is a much-needed development for BOSSY given many of the traditional luxury brands like Louis Vuitton ( OTCPK:LVMHF ) have incorporated streetwear into their design philosophy. BOSSY has done a better job with targeting this segment, however, at its current price point, the company is facing serious competition from the traditional luxury brands.

{kind=link}

Brands (Hugo Boss)

Although the direction feels necessary, the execution is overly confusing. The idea of one brand called "Hugo" and the other called "Boss" is longstanding dating back to 1997 (although slightly confusing in itself). However, with the color scheme and product expansion for each subgroup, it feels like BOSSY is trying to do everything while losing focus on its core customers. We are struggling to see what the design philosophy is now, as it feels like each segment is seeking to replicate the most popular product on the market. Finally, there are many product designs which are overlapping in both, such as shoes and boots, blurring the differentiation.

Compounding our feeling that BOSSY seeking to follow trends is its new logo that is due to be launched. The print due to release in 2024 looks quite similar to Burberry ( OTCPK:BURBY ) monogram that was launched several years ago. This is not to suggest BOSSY copied the design but we are not seeing anything revolutionary from the business. This feels like another attempt at creating a successful monogram, but lacks the layers and complexity of the Burberry one, looking basic in comparison.

On a positive note, we believe the traditional Hugo Boss design of tailored sophistication could be on the rise. In the last year or two, there has been a quietly developing change in the luxury market, with consumers increasingly rejecting logos for well-designed, high-quality, tailored clothing, seeking silhouettes over brands. This has been referred to as "Quiet Fashion", popularized by the hit show Succession . BOSSY looks to be positioning itself to exploit this, as illustrated by the screenshot below of its ambassadors.

Further, targeting emerging markets and expanding its retail presence in these countries continues to be a growth area of the company, as an ever-growing middle class demands Western goods. We expect a bump from China, as economic conditions in the country improve following a consistent series of lockdowns in 2022.

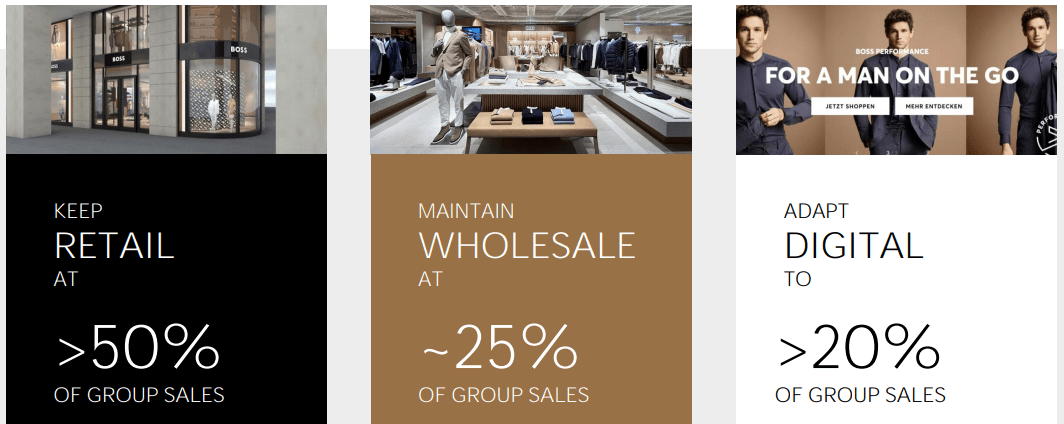

The company operates through various channels, including owned retail stores, department stores, e-commerce platforms, and wholesale partnerships. BOSSY has focused on developing its e-commerce capabilities, as increased competition has forced the business to seek new ways of capturing consumers. The value of selling to customers directly is improved margins, so it is critical from a financial perspective, also. Currently, c.75% of sales are through its own channels, a healthy level in our view. The business does not want to transition too far from wholesale, as this segment provides marketing through retail space and also certainty over demand.

{kind=link}

Distribution channel (Hugo Boss)

The company maintains control over its production processes and leverages its expertise in materials, design, and manufacturing to deliver high-quality products. This is critical for BOSSY to maintain its luxury image, as it otherwise faces dilution through the objective of cutting costs.

As part of its transformation, Management has sought to improve its social media presence. This is a vital objective they must execute, as social media increasingly drives consumer tastes and trends. Since the initiation of the current strategy, BOSSY has signed up several highly influential ambassadors, including the most followed Tik Tok'er, Khaby Lame.

This has generated 4m+ social media followers and a rapid increase in online sales. The e-commerce segment is 25% of revenue which implies further development is necessary, but this is a positive development.

Followers (Hugo Boss)

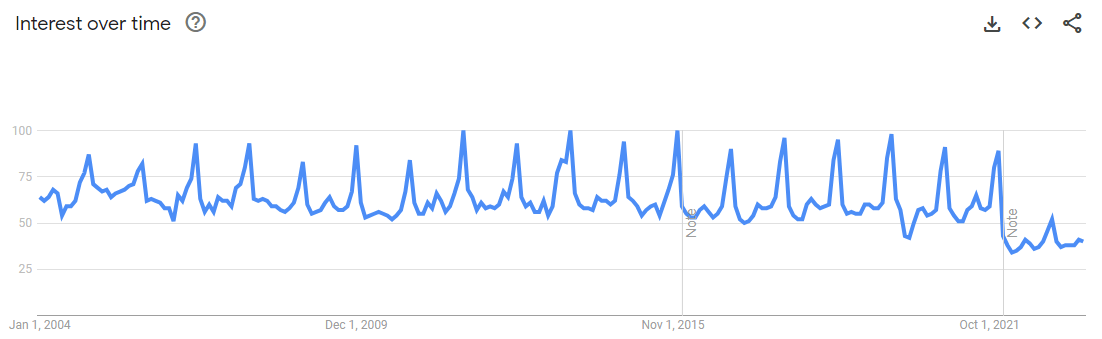

Using our own test of consumer interest below, which considers Google impressions,, there does not seem to be a material increase in interest, implying the current efforts thus far have been to maintain the status quo.

{kind=link}

Hugo Boss (Google Trends)

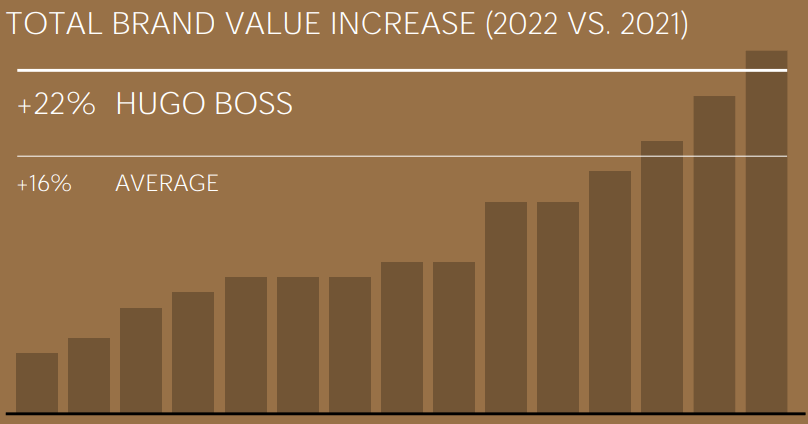

Management estimate that the Hugo Boss brand has increased 22% in value since 2021, compared to 16% in the industry.

{kind=link}

Brand valuation (Hugo Boss)

Economic & External Consideration

The current economic conditions present a potential risk to BOSSY. The combination of elevated interest rates and high inflation is a recipe for consumer spending slowdown, with discretionary purchases foregone to protect finances. However, it is important to note that the current economic weakness differs from previous downturns due to high employment and resilient spending.

In the most recent quarter, BOSSY experienced 25.4% YoY growth but from a low level a year prior. This quarter's revenue is marginally up on Q3'22, implying a continuation of the current trend, although at a slower level.

This implies economic conditions are likely weighing on the business but not to the extent that a decline is a concern. BOSSY is due to release its earnings in the coming days and we are expecting a good showing (MSD-HSD), and with many of its peers struggling for growth, this would imply market share growth. The new direction of the business and marketing push is inevitably creating some hype around the business, which is well timed to buffer the economic conditions. Analysts are guiding 12% for FY23 with the current LTM up 5%, aligning with our view.

Margins

BOSSY has faced margin erosion following the Covid-19 period, with GPM declining to 62% and EBITDA-M down to 12%.

The company has faced a number of negatively compounding factors, including inflationary pressure, increased discounting, and increased S&A investment to support its transformational efforts. In Q1-23, EBITDA-M improved to 15%, implying the business is currently experiencing a degree of improvement already, although we are yet to see the sustainability of this.

Balance sheet & Cash Flows

BOSSY's balance sheet is fairly uneventful. The company is conservatively financed, reducing any downside risk. Further, inventory turnover has returned to pre-Covid levels, implying strong stock management at a time when growth is volatile. Finally, distributions have let to return to pre-Covid level, as cash is invested in operations.

Industry analysis

{kind=link}

Fashion industry (Seeking Alpha)

Presented above is a comparison of BOSSY's growth and profitability to the average of its industry, as defined by Seeking Alpha (33 companies).

BOSSY's growth is comparable to its peers, with almost identical historical revenue growth, although the forecast period is expected to be superior. Its profitability gains have been larger, but this is a reflection of its significant weakness previously.

Profitability, however, is far worse. Even if the company was to return to its FY19 level, this would only leave the business at parity.

Based on this, we believe BOSSY should trade at a discount to its historical average and peers, reflecting the current underperformance and execution risk associated with improvement back to its FY19 levels (let alone exceeding this, which Management is targeting).

Valuation

{kind=link}

Valuation (Capital IQ)

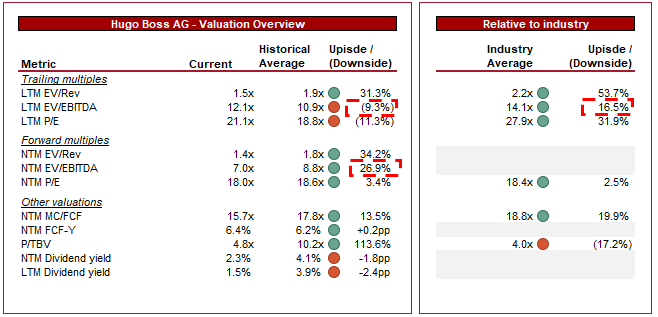

BOSSY is currently trading at 12x LTM EBITDA and 7x NTM EBITDA. This is a conflicting assessment of its current position relative to historicals.

The NTM EBITDA assessment looks optimistic, with EBITDA-M expected to improve to c.19% according to Wall St analysis ( Source: Capital IQ ). Given the Q1'23 EBITDA-M is 15%, this implies a rapid improvement in the coming quarters. Management has upgraded its guidance and is positive on the development of the business but we are not overly optimistic to this level.

From an LTM perspective, BOSSY is trading at a 17% discount to its peers. We believe this is excessive, especially when considering the margin improvement in Q1. This said, the upside is likely not substantial (<10%). Given the progress remaining, we do not believe this to be sufficient.

Final thoughts

BOSSY has arguably over-engineered its current strategy in our view. The several brand lines below the two key brands feel dilutive to its brand image. Further, the product development is not overly impressive. This said, BOSSY is doing the right thing to tap into hype, be it through its ambassadors or approach to designing products. This looks to have generated near-term improvement.

Financially, the improvements have yet to be wholly seen, although there is some evidence to be optimistic. At its current valuation, we do not believe there is sufficient upside to partake in the continuation of its transformation.

For further details see:

Hugo Boss: Tailoring A Transformation