HUM - Humana: Buy This Amazing Wealth Compounder Now You'll Be Glad You Did

2023-09-27 01:43:43 ET

Summary

- Humana's adjusted diluted EPS and free cash flow payout ratios make the dividend very secure.

- The managed care company's revenue and adjusted diluted EPS both surged in the first half of 2023.

- Humana's interest coverage ratio of over 13 is part of why it earns investment-grade credit ratings from the major rating agencies.

- My inputs into the discounted cash flows model show shares of the stock to be trading 16% below fair value.

- Humana has what it takes to keep enriching shareholders in the years ahead.

As a dividend growth investor, I put most of my emphasis on dividend growth. After all, growing streams of cash flow are what I will use to theoretically pay my bills upon achieving financial independence. Don't get me wrong: I also enjoy capital appreciation from my investments. But I know that as long as my passive income is rising, my holdings are more likely to grow in value as well.

Thanks to Humana's ( HUM ) solid track record as a dividend grower and as a growing business overall, the stock has made shareholders considerably richer in the past 10 years. A $10,000 investment made in Humana in 2013 would now be valued at $54,000 with dividends reinvested. Put into perspective, that blows away the $32,000 that the same investment amount put into the S&P 500 index 10 years ago would have been worth as of a few weeks ago with dividends reinvested.

While I don't yet own Humana, it is a business I would eventually consider owning for my dividend growth stock portfolio. Let's dive into Humana's fundamentals, valuation, and risks to learn why it is on my watch list as a dividend growth investor.

A Modest But Ultra-Safe Dividend

In every sense of the phrase, Humana is a dividend growth stock. This isn't the kind of stock that income investors are going to bother looking at twice. The stock's 0.7% dividend yield versus the healthcare sector's 1.6% median yield earns it a C grade for the dividend yield metric from Seeking Alpha's Quant system.

But if you're in my general age range as an older member of the Gen Z demographic (I'm 26 years old) or even from Gen Y, it's a wise idea to own stocks with tons of room for dividend growth. And this is where Humana truly shines.

The stock's 12.3% 10-year annual dividend growth rate compares favorably to the healthcare sector median of 8%. This is what is behind the A- dividend growth grade from SA's Quant system.

In even better news, Humana's high dividend growth should have no problem persisting for many more years. For one, the company generated $25.24 in adjusted diluted EPS in 2022. Against the $3.0625 in dividends per share paid during that time, that equates to a mere 12.1% adjusted diluted EPS payout ratio.

Humana is also skilled at minting free cash flow for its shareholders. The company posted $4.6 billion in operating cash flow during 2022. Less than the $1.1 billion in property and equipment purchases made for 2022, this is a free cash flow of approximately $3.5 billion. Compared to the $392 million in dividends paid in 2022, that works out to an 11.3% free cash flow payout ratio (details sourced from page 78 of 159 of Humana's 10-K filing ).

As if these very sustainable payout ratios weren't enough to convince you of Humana's dividend growth potential, there's more: Analysts believe that Humana's adjusted diluted EPS will rise by 12.5% annually for the next three- to five years. That is because of the underlying assumption that demand for health insurance and pharmacy services will keep growing. For context, that is better than the healthcare sector median of 10.3%. This is how Humana scores an overall growth grade of B from SA's Quant system.

So, as we can see, highly covered payout ratios and double-digit annual earnings growth are a recipe for quite a few more years of robust dividend growth from Humana.

The Business Is Performing Well

{kind=link}

Humana Q2 2023 Earnings Press Release

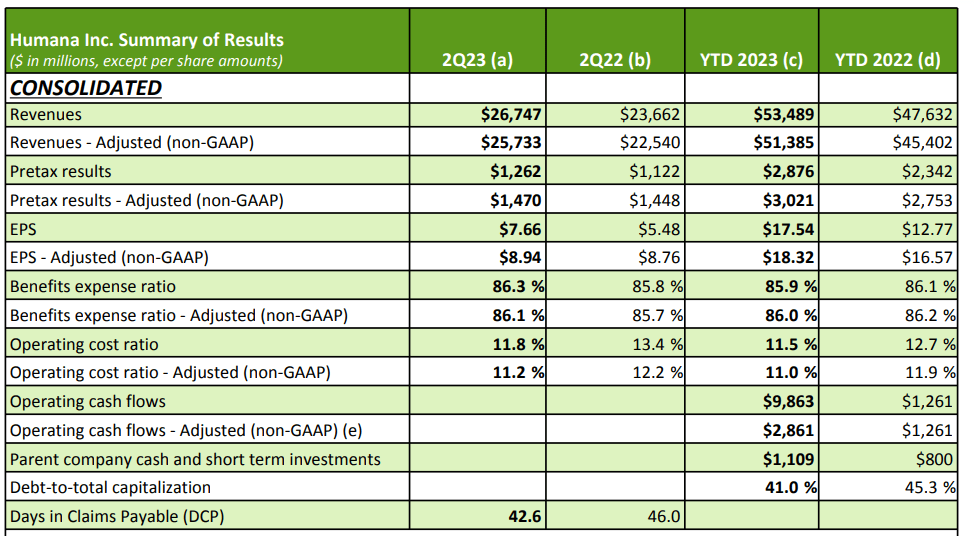

As a business, Humana continued to thrive in the first half of this year. The company's total revenue climbed 12.3% over the year-ago period to $53.5 billion for the first half of 2023.

These results were largely driven by double-digit topline growth (13.8%) in the insurance segment to $51.8 billion during the first half. Humana's total medical, dental, and vision membership was relatively flat at 22.2 million as of June 30. Premium hikes were the catalyst that powered the company's revenue higher in the first half.

Humana's CenterWell pharmacy services and provider/home solutions segment revenue edged 1.6% higher year over year to $9 billion for the first half. The company's increased scale of its capabilities in this segment contributed to its growth during the first half.

Humana's adjusted diluted EPS surged 10.6% higher over the year-ago period to $18.32 in the first half of 2023. The company's higher total revenue base and lower outstanding share count from share repurchases were the factors that led to this solid earnings growth.

Aside from being a fundamentally well business, Humana is financially secure too. The company's interest coverage ratio for the first half of 2023 was 13.3, which builds in a sizable buffer to keep Humana a going concern if profits decline temporarily. That is why the major rating agencies of S&P, Moody's, and Fitch have respectively assigned BBB+, Baa2, and BBB investment-grade credit ratings to Humana (info in section according to Humana Q2 2023 earnings press release ).

Risks To Consider

No business is completely shielded from risk, so it's important to understand at least some of the pertinent risks that apply to Humana before investing.

Deriving 88% of its total premium and services revenue in 2022 from government programs, Humana must maintain good working relationships with federal and state government health care coverage programs. These include military, Medicare, and Medicaid programs. Any breakdowns in its relationships with these programs could have a material impact on the company's fundamentals.

Another implication of being a government contractor like Humana is that the company must closely monitor changing legislation. Changes to existing laws or the implementation of new laws could result in higher expenses for the company (info in this section per the Risk Factors section of Humana's 10-K filing).

Humana Is A Blue-Chip Bargain

Humana is the type of business that younger investors can lean into to build up both the dividend income and value of their portfolios. However, the stock must be purchased at a reasonable valuation to do well. Fortunately, Humana looks to be borderline deeply discounted based on my inputs into a valuation model.

{kind=link}

Money Chimp

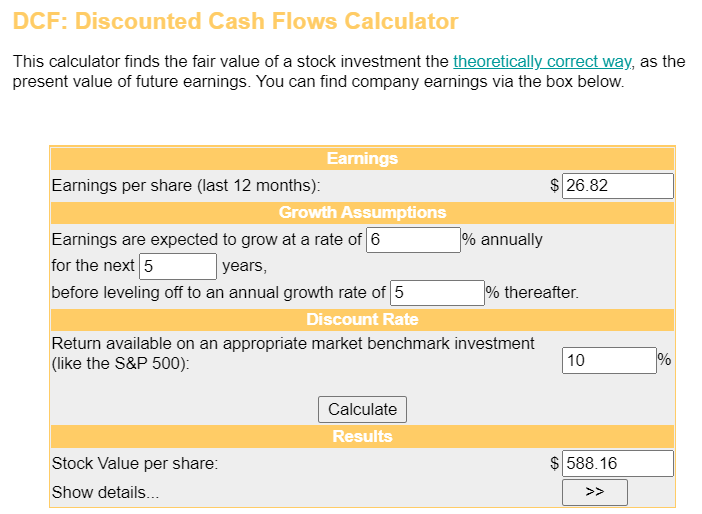

The valuation model that I will use to value shares of Humana is the discounted cash flows or DCF model. The DCF model consists of three inputs.

The first input for the DCF model is the past 12 months of adjusted diluted EPS. In the last four quarters, Humana has recorded $26.82 in adjusted diluted EPS.

The second input into the DCF model is growth predictions. Erring on the side of caution, I will use an annual adjusted diluted EPS growth rate of 6% for the next five years - - half the analyst consensus. I'll then assume a slowdown to 5% annually in the years beyond that point.

The third input for the DCF model is the discount rate, which is the annual total return rate required by investors. My personal preference is for 10% annual total returns, so that is what I'll be using.

Plugging these inputs into the DCF model, I get a fair value of $588.16 a share. This suggests that Humana's shares are priced at a 15.9% discount to fair value and have an 18.9% upside from the current price of $494.61 a share (as of September 26, 2023).

Summary: An All-Around Wonderful Investment Option

Humana has grown its dividend for 12 consecutive years, which puts it almost halfway to becoming a Dividend Aristocrat. Considering the company's very low payout ratios and healthy earnings growth potential, the probability that it ascends to dividend aristocracy is quite high in my estimation.

If these factors weren't enough, Humana looks to be 16% cheaper than its fair value based on my assumptions for the DCF model. This is why I believe shares of the stock are a buy for investors seeking a blend of dividend growth, capital appreciation, and value.

For further details see:

Humana: Buy This Amazing Wealth Compounder Now, You'll Be Glad You Did