HUM - Humana: Buy This Powerful Dividend Growth Stock In The New Year

2024-01-02 07:00:00 ET

Summary

- As always, I am looking to improve the overall quality of my portfolio in 2024.

- Humana's total revenue and adjusted EPS grew at healthy clips in the third quarter.

- The company's interest coverage ratio was above 12 through the first three quarters of 2023.

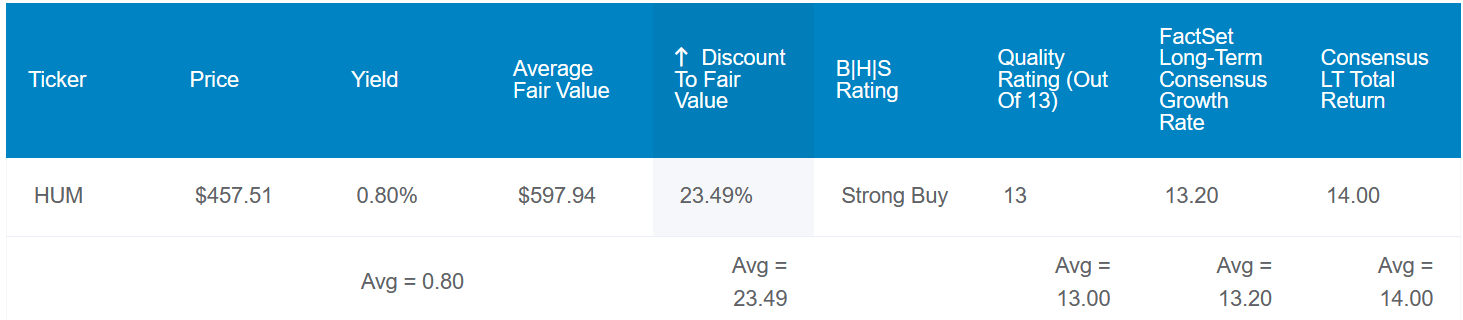

- Shares of Humana appear to be trading at a 23% discount to fair value.

- The stock's total return potential could be almost 3X the S&P in both the next two years and 10 years from its current share price.

As I'm writing this article, 2024 is just 35 hours away. In absolute terms, there were 8,760 hours this year just like any other (besides the 8,784 hours in leap years, of course).

It certainly didn't feel that long, though. I guess the adage that time flies when you're having fun rings true. Heading into 2024, I feel very blessed to be doing what I believe I was born to do covering world-class businesses here on Seeking Alpha.

The change of the calendar may bring a new year, but my core strategy of dividend growth investing will remain mostly unchanged in 2024. As my long-time readers know, I am always looking for ways to strengthen my portfolio.

The health insurer, Humana ( HUM ), is a remarkable business that I have watched for years now. As I noted in my previous article initiating coverage here on Seeking Alpha, the health insurer has a lengthy track record of crushing the S&P 500 ( SP500 ). Today, I will revisit Humana's fundamentals and valuation to unpack why I am maintaining my buy rating.

{kind=link}

Humana's 0.8% dividend yield is well below the 1.5% yield of the S&P 500. However, the dividend is remarkably safe and positioned to grow at a fast rate in the years ahead.

The company's 12% EPS payout ratio is considerably less than the 60% EPS payout ratio that rating agencies consider safe for the health insurance industry. If that itself weren't enough, Humana earns a BBB+ credit rating from S&P on a stable outlook. That implies the risk of the company going to zero in the next 30 years is just 5%.

As illustrated above, that explains how the risk of Humana cutting its dividend in the next average recession is only 0.5%. Even in a severe recession, this probability increases to just 1%.

{kind=link}

Humana is well-positioned from a fundamentals perspective. Adding to my case for it, the stock looks to be deeply undervalued. Using historical dividend yield and P/E ratio as valuation metrics, shares of Humana are worth $598 each. Against the current $458 share price, which means the stock is priced at a 23% discount to fair value.

If Humana were to grow in line with the analyst consensus and revert to its mean valuation, here are the total returns that it could produce over the coming 10 years:

- 0.8% yield + 13.2% FactSet Research annual growth consensus + a 2.7% annual valuation multiple boost = 16.7% annual total return potential or a 368% 10-year cumulative total return versus the 8.6% annual total return potential of the S&P or a 128% 10-year cumulative total return

A Solid Third Quarter

{kind=link}

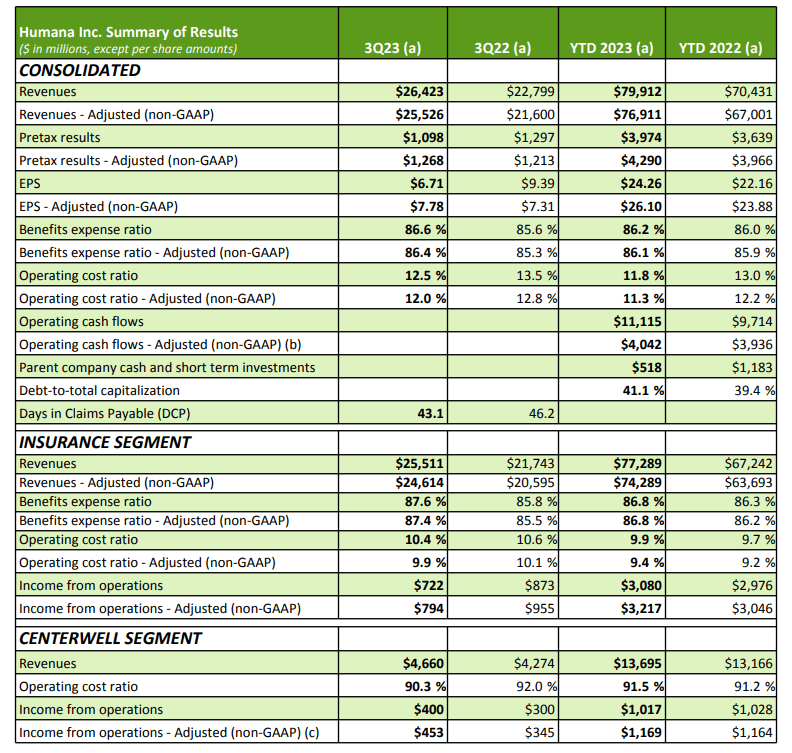

As is the case with any high-quality business, Humana tends to consistently outperform analysts' expectations. This proved to again be the case in the third quarter ended September 30 for the health insurer. Humana's revenue surged higher by 15.9% year-over-year to $26.4 billion during the quarter, which came in ahead of the consensus by $840 million .

The company's total medical, dental, and vision membership fell by 1.7% year-over-year to 21.9 million as of September 30. Double-digit growth in Medicare plan membership was more than offset by a double-digit drop in employer-sponsored medical plan membership. The good news is that this lower total membership was more than countered by premium hikes. That explains how Humana's total revenue surged higher for the third quarter.

The company's adjusted EPS grew by 6.4% over the year-ago period to $7.78 in the third quarter. For perspective, that beat the analyst consensus by $0.61. Higher claims activity during the quarter pushed the company's non-GAAP benefits expense ratio higher by 110 basis points to 86.4%. This is why Humana's adjusted EPS growth lagged revenue growth for the quarter.

Moving to solvency, the company's interest coverage ratio remained strong through the first nine months of 2023 at 12.5. This suggests that Humana can currently handily meet its financial obligations. The confidence that the company inspires with its liquidity is how it was able to issue $1.35 billion in senior notes last month at rates in the high-5% range . Considering that the 10-year U.S. treasury was yielding in the high-4% range at that time, that's a favorable spread made possible by Humana's BBB+ credit rating from S&P.

Massive Free Cash Flow Can Support Double-Digit Dividend Growth

As I pointed out in my previous article, Humana has upped its quarterly dividend per share for 12 consecutive years. This puts it well on the way to becoming a Dividend Aristocrat. More impressively, the company's quarterly dividend per share rocketed 77% higher in the last five years to the current rate of $0.885 .

This could be just the start of the amazing dividend growth as well. Humana generated $10.4 billion in free cash flow through the first nine months of 2023. Compared to the $320 million in dividends paid, the company's free cash flow payout ratio was just 3.1% (info sourced from page 8 of 61 of Humana's 10-Q filing ). This means that assuming even free cash flow throughout the year (I know that's not the case, but bear with me), Humana was able to cover three quarters of dividends in approximately 11 days! Put another way, the company threw off enough free cash flow to fund three quarters of dividends by January 12th.

Risks To Consider

Humana is an excellent business with steady growth prospects and low payout ratios. However, the company has its share of risks worth at least briefly highlighting.

Humana generated 83% of its total premium and services revenue through the first three quarters of 2023 via its Medicare products (page 26 of 61 of Humana's 10-Q filing). This revenue concentration makes the company vulnerable to certain risks. Humana's revenue is at the mercy of the U.S. government. That is why it is of utmost importance to maintain a harmonious working relationship with the federal government. In a low probability scenario, Humana's contracts may not be renewed by the Centers for Medicare and Medicaid Services. If this were to happen, it would be devastating for the business.

As an insurer, Humana is also exposed to mortality risk from catastrophes like global pandemics and natural disasters. If actual claims activity is higher than expected, the company's premiums may not be enough to turn a profit. In a worst-case scenario, Humana may not have enough of an insurance float to pay out on all insurance claims if claims activity is unusually high.

Summary: Buy This Future Dividend Aristocrat While It's On Sale

{kind=link}

{kind=link}

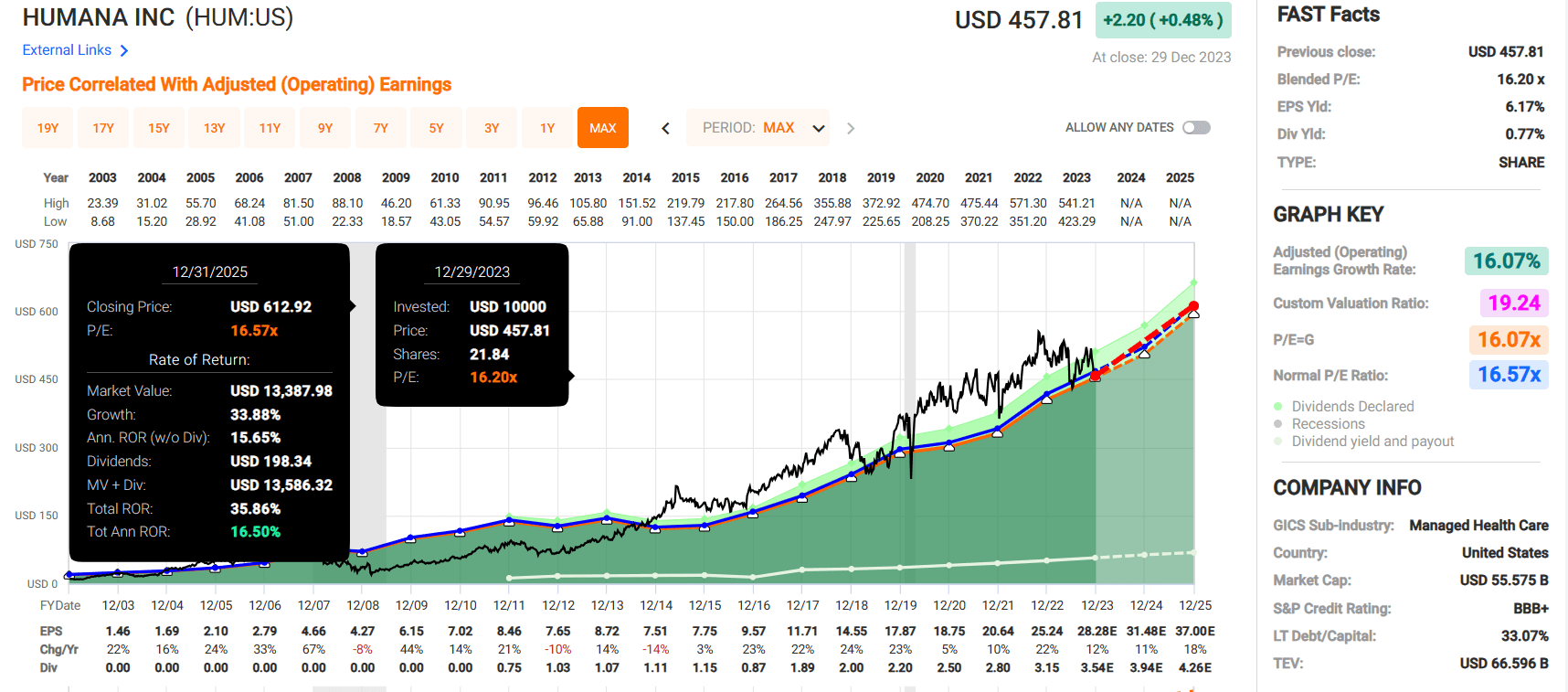

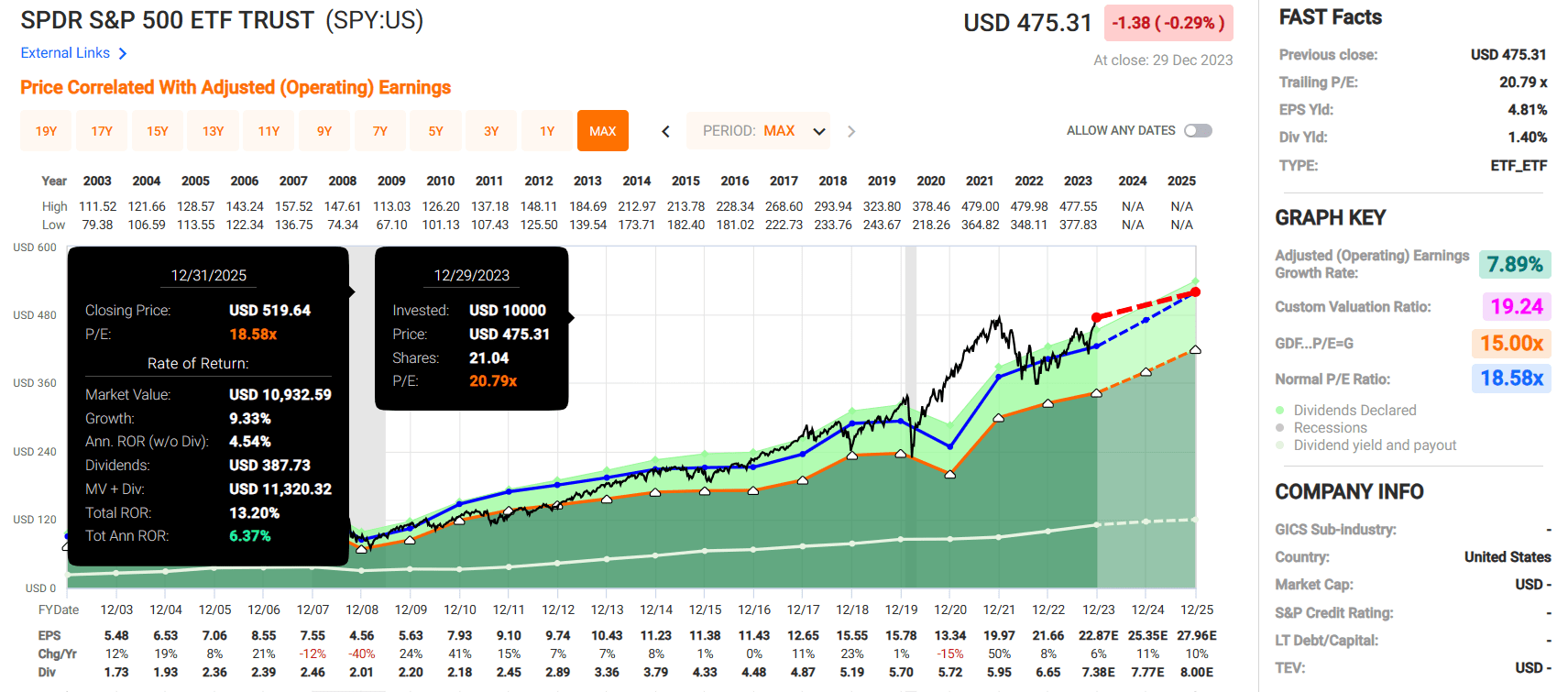

In my experience, I have found that buying great businesses on sale is a recipe for success. Humana's current blended P/E ratio of 16.2 is below its normal P/E ratio of 16.6. Assuming a reversion to its normal valuation multiple and that the company grows as anticipated, Humana could deliver 36% cumulative total returns through 2025. That clocks in at nearly triple the 13% cumulative total returns projected from the SPDR S&P 500 ETF Trust ( SPY ) at that same time. This is why I am reiterating my buy rating on Humana currently.

As a side note to conclude this article, I just want to thank my readers for their support in 2023. I'm touched that so many of you find value in the work that I do each day!

Also, I want to express my gratitude to The Dividend Kings and iREIT on Alpha Marketplace services for bringing me aboard earlier this year as a contributing analyst. Here's to a safe, healthy, and prosperous 2024 for all of us!

For further details see:

Humana: Buy This Powerful Dividend Growth Stock In The New Year