HUM - Humana: New Contract Potential But Not A Buy Yet

Summary

- A new military contract could be worth $70.85 over 9 years.

- HUM has outperformed the S&P 500 by nearly 400% over 10 years.

- Strong Revenue growth.

- Decline in Earnings.

- Technicals Suggest a Possible Retracement.

Humana Inc. ( HUM ) has recently landed a very large contract with the US military for the eastern region. The contract has a yearly option in place after year 1 and could extend for a total of 9 years. The news was released on December 22, 2022, but hasn’t had the impact on share prices I think it deserves.

If Humana gets confirmed as I believe it should, then the contract is worth $70.85 billion over the period. That would equal an extra $7.87 billion in revenue per year, which is 8.6% of the TTM total revenue.

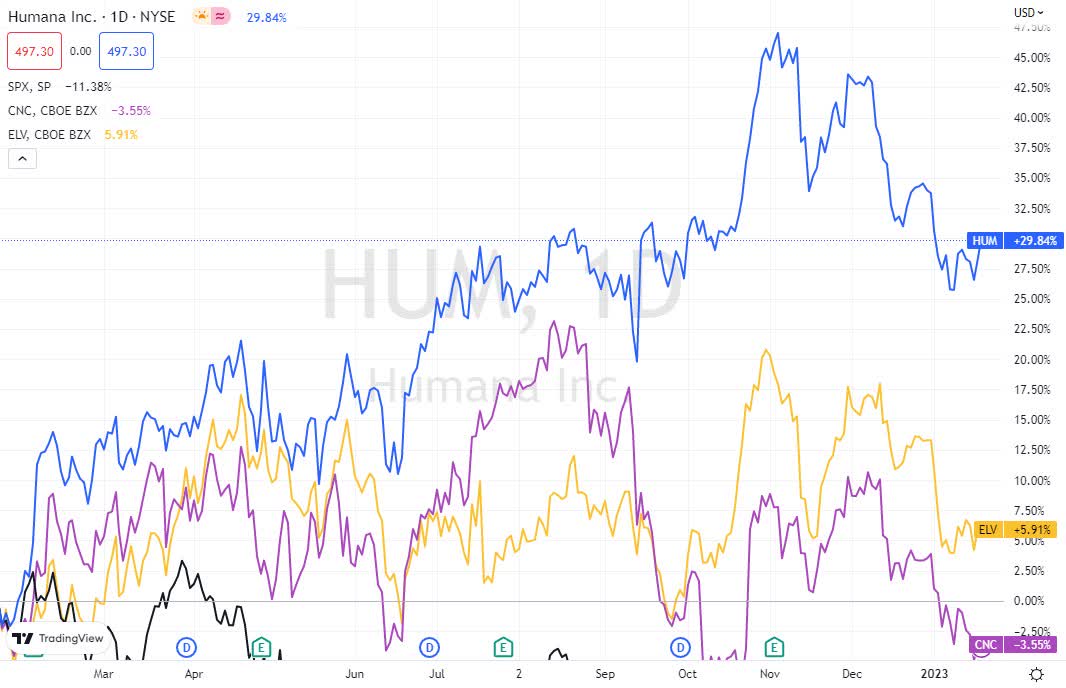

HUM’s performance has beaten the broader stock market by over 41% over the past year. And has also outperformed its closest peers, Centene Corp ( CNC ) and Elevance Health Inc. ( ELV ) by 33.39% and 41.22% respectively.

{kind=link}

TradingView

Over the past 10 years, HUM share prices have increased by 563.69% compared to 164.32% for the SP 500. That performance is slightly lower than its two peers, which achieved 624.63% ( ELV ) and 585.11% ( CNC ).

TradingView

The table above shows the share price returns for HUM and two of its closest competitors. Over the 10-year period HUM underperformed both competitors. However, as we look at more recent periods we see HUM improving, and in the last 1-year period HUM outperforms both competitors.

HUM Fundamentals

Looking at the fundamental metrics I use to evaluate a stock I see a decent progression in increased earnings since 2018. EBITDA and EPS have risen since 2018 compared to the TTM. However, they have both fallen since their 2020 high.

This is at odds with the total revenue streams which have continued to increase. Possibly most of the decline in earnings is due to operating expenses which have risen at a faster rate than revenue for 2021 and TTM.

Seeking Alpha

Cash flow has risen substantially for the TTM after declining heavily in 2021. However, the liabilities to assets ratio has been on the rise since 2019. This ratio is still not at worrying levels in absolute terms, but it has gone from 0.586 in 2019 to 0.679 TTM.

The trend in itself is of concern, although I would presume the management would try to flatten that out before it becomes a real burden. And compared to its direct peers HUM's ratio seems less concerning as both have increasing ratios and an average of 0.668 TTM.

Quant Rating

The Quant rating for HUM is a Hold with a score of 3.22. This is the same rating I would apply to this stock at the moment, given its decline in earnings despite increasing revenues. The worst grade among the 5 factors comes from the Valuation factor.

Two elements take the responsibility for this low grade, which are P/E growth and price to book ratios which get a D and D+ respectively. Bringing down the overall grade for the factor despite enterprise value to EBITDA or P/E both being above the sector average.

Seeking Alpha

Profitability, which is where I see the real concern, gets an A+. This is due to various elements of the factor getting higher than sector average ratios. However, the gross profit margin TTM is 66.51% lower than the average.

While the EBITDA margin TTM gets a B- at 4.81% as its 29.12% higher than the sector average. But to me, that's a low ratio in absolute terms and as we have seen above has been falling.

Industry Trend

The industry trend as analyzed by Mordor Intelligence puts the medical insurance industry on a CAGR of 7.95% from 2021 to 2027. That’s a substantial amount of growth. I would expect Humana to grow at the same rate at least. Possibly more as it is most likely to have the military contract renewed over the next 9 years.

Mordor Intelligence

More job creation will mean more employer-sponsored health insurance and I see the recent expansion in job data as a positive element for the growth in this market. The health insurance market has a high level of concentration and Humana is one of the bigger players in the market.

The above-mentioned report found that according to the American Medical Association, 72% of metropolitan areas lack significant competition in health care insurance.

This gives players like Humana the position to leverage their presence and outreach.

HUM Technical View

The long-term view for Humana share prices shows a very bullish trend that has been ongoing since late 2004. With price action consistently above the Ichimoku cloud and two attempts to break to the downside of the cloud failing to materialize.

Not even the 2008 financial crisis managed to send prices below the cloud. The second attempt was in 2020 where the dip lasted 3 months only. However, we are beginning to see some signs of weakness.

Not a trend reversal, but perhaps a price correction. The candle for January 2023 gapped at the open from the previous candle. This often indicates further downside momentum. Prices are relatively far away from the cloud.

As we can see in the chart below when price action moves too quickly away from the cloud, there is a tendency for the market to correct. The RSI is also showing signs of possible weakness. If the current candle for this month closes at this level we will get a break of the RSI's moving average to the downside.

{kind=link}

TradingView

Looking at the weekly chart we get a similar picture. Price action is above the cloud with the moving averages indicating bullish momentum. We also see prices are getting closer to the cloud and would place support at the top of the cloud at the $470 area.

{kind=link}

TradingView

However, on this chart we see that the RSI has broken below both its moving average and the 50 level, indicating that further price weakness is likely. Overall, the technical view I see for this stock is bullish long-term with a likely price retracement in the short to medium term.

Conclusion

I see the decline in earnings as a factor of concern, although the long-term view on this stock is positive. I’m positive long-term because of the industry trend and the consistently increasing revenues from Humana. However, the company needs to turn its profit margin higher, basically back to previous levels to gain more value in my opinion.

Adding the technical analysis to the fundamental view shows a similar story. As the market seems to be making a price correction, having a view of Hold for this stock seems to be the approach. Without giving up on the stock’s long-term performance potential.

For further details see:

Humana: New Contract Potential But Not A Buy Yet