HUM - Humana: Recent Selloff Might Present A Buying Opportunity

2023-07-13 01:32:44 ET

Summary

- Humana is close to a pure play on U.S. health insurance, especially Medicare.

- Comments from UNH's CEO in the middle of June regarding short-term challenges started an unjustified sell-off.

- Humana benefits from the growth in the elderly (65+) U.S. population and has high pricing power due to health insurance being a non-discretionary expense.

- I think Humana can generate mid-double-digit returns, while my DCF valuation indicates that there is also some valuation upside.

Introduction

This will be the first article of a planned three-part series where I want to start coverage of three big health insurance providers in the U.S.: Humana Inc. ( HUM ), UnitedHealth Group (NYSE: UNH ) and Cigna Group (NYSE: CI ). This first article will focus on Humana because it is, at its core, a pure play in the health insurance sector. This article will cover some ground regarding the health insurance market and therefore serve as the foundation for the following articles, which will be dedicated to the other two companies.

As for the structure of this article: I will start by giving an overview of Humana and why I think it is (unlike the other two) a pure play in the health insurance space. After that overview, I will go over the insurance membership structure and the benefits expense ratio while making a comparison to the aforementioned peers UnitedHealth and Cigna. I will then focus on the past financial performance and future growth prospects and finish as I usually do, with two separate chapters dedicated to valuation and risks and, lastly, a conclusion.

Company Overview

Humana describes itself as a leading health and well-being company committed to helping its millions of medical and specialty members achieve their best health. The company reports two segments: Insurance and CenterWell.

The Insurance segment is (to no surprise) the traditional health insurance business. It also includes the Pharmacy Benefit Management ((PBM)). The CenterWell segment includes all healthcare services offerings.

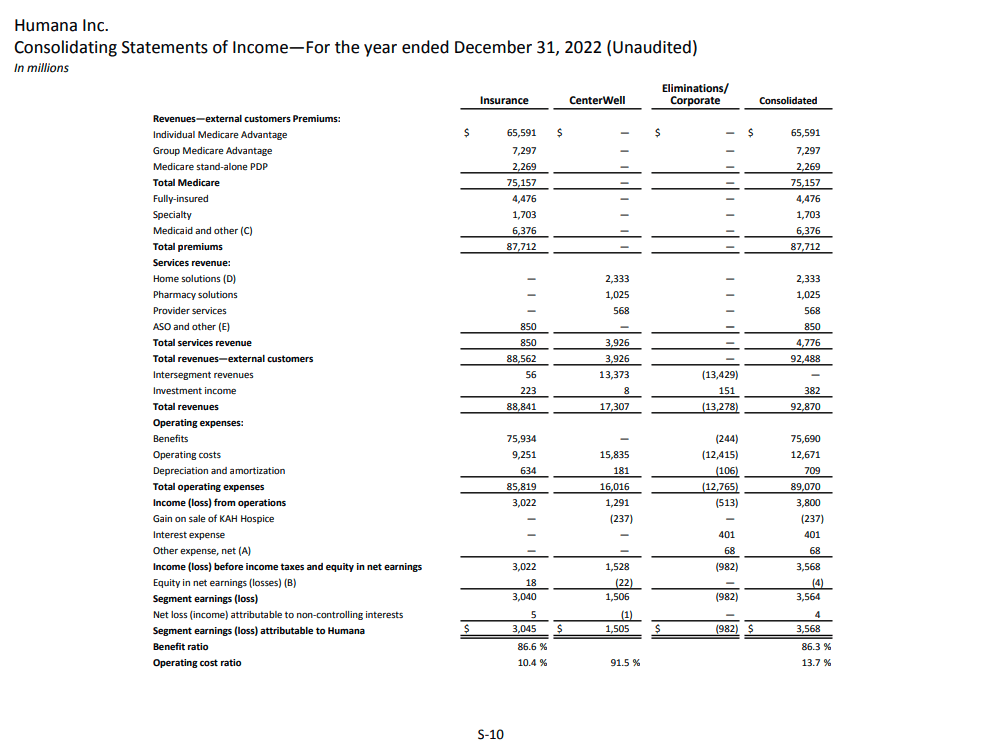

I stated in the introduction that Humana is, in my opinion, close to a pure play on health insurance. Let me show you the composition of Humana's consolidated income for FY2022 to make my point:

Humana FY2022 consolidated income statement (FY2022 earnings release - page 27)

{kind=link}

I want to turn your attention to the intersegment revenue and the "Eliminations". Total FY2022 revenue from the CenterWell segment amounted to $17,307 million (unconsolidated). $13,373 million were eliminated in the consolidation process because it is revenue billed to the insurance segment. So approximately 77% of CenterWell's revenue was internal, with only 23% ($3,926 million) being external revenue. If we assume that the Insurance segment billed close to zero revenue and caused close to zero operating costs to the CenterWell segment (which seems reasonable in my opinion), CenterWell made around $500 million in GAAP pre-tax profits off of $3,926 million in revenue. I am not saying that this isn't meaningful but it dwarfs in comparison to the $3 billion in GAAP pre-tax profits of the Insurance segment.

What does Humana get out of all these interconnections between their two business segments? I think a good comparison is what Nike (NYSE: NKE ) has been doing in the past: cutting out parts of the value chain from how a product goes until it reaches the consumer. If Nike sells shoes directly to the consumer, it cuts out the margin that an intermediary like a retail outlet would take if it were to sell these shoes in Nike's place. Humana basically does the same. By offering the needed healthcare services itself and cutting out the margins of healthcare service providers, it can either (a) lower prices for premiums, ultimately making the main insurance products more attractive to the consumer or (b) keep the premiums unchanged and improve margins.

Besides that, CenterWell's external revenues and profits can grow as well of course. Please keep in mind that I will focus on the Insurance business in this article.

Medical Memberships

The composition of the memberships is the main differentiator for the big health insurance providers. I want to start with a table showing Humana's membership composition (numbers in thousands):

Humana medical memberships (Company reports - compiled by Author)

{kind=link}

We can see that the focus has been shifting strongly toward Medicare Advantage memberships over the past few years. Please note that I summed up state-based contracts, Medicare supplement and commercial memberships under "other".

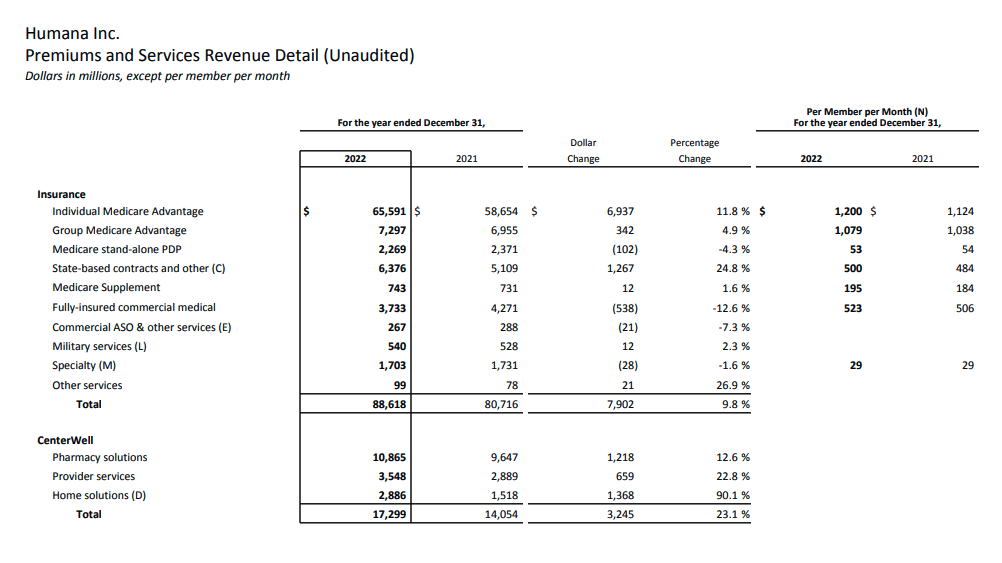

The next slide from Humana's FY2022 earnings release shows how much premiums the company gets paid for the different types of memberships:

Premiums per membership type (FY2022 earnings release - page 31)

{kind=link}

Medicare memberships have by far the highest premium per member per month. Sadly I wasn't able to find any information regarding the profits for each type of membership. This would be very valuable information to see how profitable these Medicare premiums are. I will get back to this later though.

I want to talk a bit about Medicare because it is the fastest-growing segment for Humana. Medicare is the federal health insurance program for people 65 or older or with disabilities. Medicare is split up into four parts.

Parts A and B are also called original Medicare. Part A is the hospital insurance (that covers most expenses regarding hospital visits/stays) and Part B is the medical insurance. The medical insurance covers doctor's visits/services, ambulance and preventive care (besides some other things).

Part D is a stand-alone prescription drug coverage plan. You can get prescription drug coverage by signing up for a Part D plan or by signing up for a Medicare Advantage plan. Medicare Advantage is also called Part C. Part C includes Parts A and B (Original Medicare) and additional benefits. These additional benefits can include Part D and special coverage like dental, vision or hearing. So in conclusion, Medicare Advantage (Part C) is the premium version of Medicare.

Benefits Expense Ratio

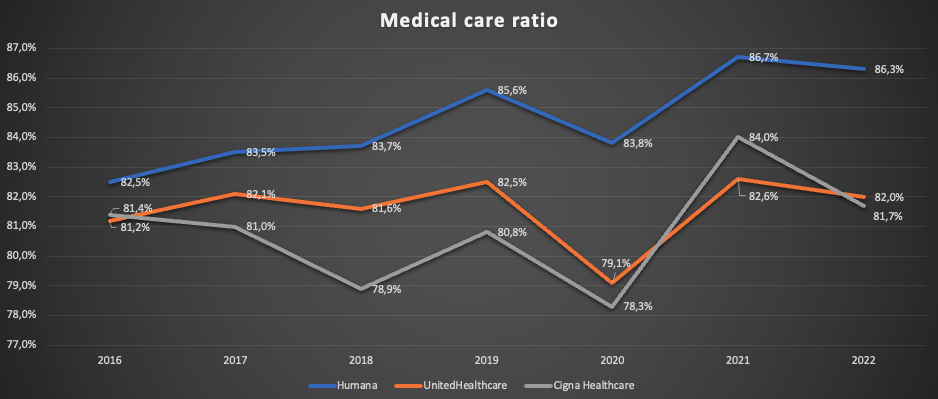

Now I want to turn to one of the more important metrics for health insurance companies. Humana calls it the "Benefits expense ratio" while UnitedHealth calls it the "medical care ratio". This ratio describes the relationship of medical costs for the insured members to the paid premiums. So the lower this ratio is, the better. I want to start with a chart showing the medical care ratio for the three companies I mentioned in the introduction:

Medical care ratios FY16-FY22 (Company reports - compiled by Author)

{kind=link}

We can see three noticeable things: (1) Humana had a higher medical care ratio than its peers in the past few years, (2) the medical care ratio got worse over the past few years and (3) there was a temporary dip in FY2020. I want to address all three points separately.

(1): According to the National Association of Insurance Commissioners (NAIC) , the Affordable Care Act of 2010 requires health insurers in the individual and small group markets to spend at least 80% of their premium revenues on clinical care and quality improvements. For the large group market, the MLR requirement is 85%. A large group health plan covers employees of an employer that has 51 or more employees. UnitedHealth and Cigna seem to sit around the sweet spot of the allowed 80-82%. Humana's higher ratio could lead to the assumption that the company isn't as good at pricing premiums or is pricing memberships lower to gain market share. I don't think that this is the case. Let's take a look at UnitedHealth's membership profile:

UnitedHealth medical memberships (Company reports - compiled by Author)

{kind=link}

In total numbers, UnitedHealth has more Medicare memberships than Humana (11,480,000 vs 8,620,500 at FY2022 end). As a percentage of total memberships (excluding Military memberships for Humana since these are services-only memberships), Medicare accounted for 53% (Humana) versus 22% (UnitedHealth) in FY2022. This is the reason for Humana's higher medical care ratio. As Medicare addresses elderly (65+) and/or disabled people, the medical expenses are higher since these groups need more care than the commercial members that comprise the bulk of UnitedHealth's membership profile. As a result, Humana's medical care ratio will naturally be higher. There is no need to worry about the higher ratio.

(2): What I described under (1) is also the reason for the increase in the medical care ratio for Humana over the past couple of years. The ratio climbed 380 basis points from FY2016 to FY2022. As I stated earlier, Humana's membership composition has shifted toward Medicare Advantage over the past few years. Total Medicare as a % of total memberships excluding Military memberships increased from 45% in FY2016 to the aforementioned 53% in FY2022. The increase in the medical care ratio naturally came along with this development. So again, nothing to worry about.

(3) The temporary dip in the medical care ratios in FY2020 was caused by the COVID pandemic and the fact that people stayed at home, couldn't visit the doctor/get treatments and that infections decreased overall because of the strict hygiene measures (social distancing, wearing masks).

On June 14, 2023 , medical care stocks sharply declined as UnitedHealth's CFO made some comments regarding a possible increase in the medical care ratio for Q2 2023. Here is what UNH's chief executive for Medicare and retirement Tim Noel had to say:

We're seeing as behaviors kind of normalize across the country in a lot of different ways and mask mandates are dropped, especially in physician offices, we're seeing that more seniors are just more comfortable accessing services for things that they might have pushed off a bit like knees and hips.

As Humana has the highest relative exposure to Medicare (as described above), Humana's share price experienced the sharpest decline of the peer group on the day of the news release (June 14, 2023), as can be seen in the following chart:

I think that this reaction to the aforementioned news doesn't add up. I understand the comments from UNH management but for Humana to see an effect as UNH described, we would need to see a significant decline in the medical care ratio in FY2020 (as a result of the pushed-back treatments mentioned) that would get reversed now. When we look at the medical care ratio chart above though, we can see that Humana's medical care ratio had the smallest drop in FY2020 (180 basis points versus 340 basis points for UNH and 250 basis points for CI). In conclusion, I think that the sell-off was exaggerated. The company reaffirmed the FY2023 EPS targets two days after the selloff. I see this as a statement that what UNH described won't affect Humana in the same way as their peers. The, in my opinion, unjustified selloff due to concerns over Humana's exposure to Medicare Advantage might present a buying opportunity.

Financials

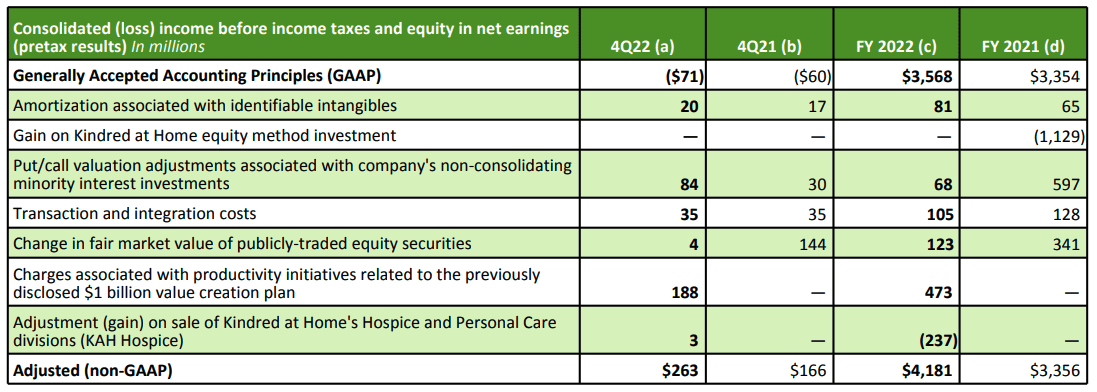

Now I want to talk a bit about past financials and I want to start with a less exciting topic: Accounting and reporting. Specifically, adjustments Humana makes to the GAAP numbers.

The table below shows Humana's reconciliation from GAAP to non-GAAP (Adjusted) pretax earnings:

{kind=link}

We need to decide if we want to accept these adjustments (and use adjusted numbers from this point) or stick with GAAP numbers. As we can see, some of the adjustments are related to changes in the fair value of various investments and the amortization of intangible assets. Both of these adjustments make perfect sense as they do not affect cash flows.

What has to be discussed are the adjustments for transaction/integration costs and the charges for the "value creation plan". Humana thinks that these are one-time costs and adds them back to GAAP numbers. As for the "value creation plan" charges, I think that this adjustment is reasonable. I looked at the adjustments from the past few years and there has never been an item like this so it does indeed look like a one-time charge (it is still debatable though and you might disagree on this).

The transaction and integration costs on the other hand should not be adjusted because they are just a part of making (M&A) business. As the adjusted numbers for these costs are insignificant compared to the earnings, I will just accept them as well and use non-GAAP numbers going forwards (if I mention pretax earnings or net income from now on I am referring to non-GAAP).

Now let's take a quick look at the current balance sheet:

10-Q Q123 Balance sheet (Form 10-Q)

Short-term debt plus long-term debt amounts to $11,610 million while cash and cash equivalents amount to $13,735 million. Furthermore, the investment securities plus receivables match the benefits payable plus the current payables at around $17 billion. The balance sheet seems to be in great shape at the moment. I have to add though that Humana's cash flows are quite volatile (unlike net earnings, I will come back to this later) so this might change pretty fast.

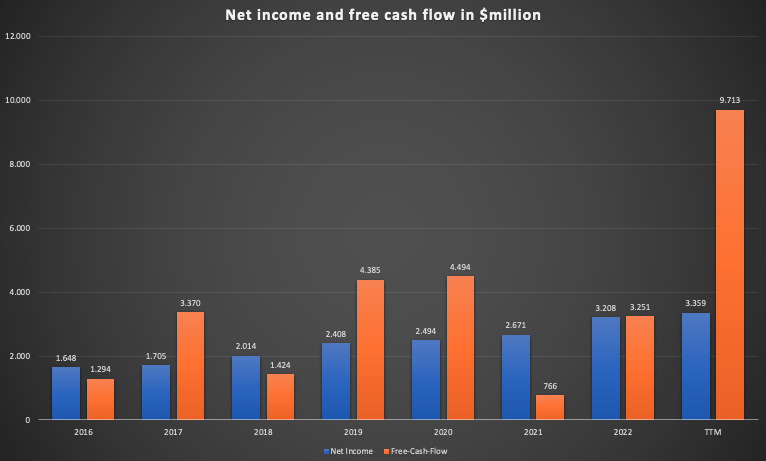

Next, let's look at the net income and free cash flow ((FCF)) over the past few years:

Humana net income and FCF since 2016 (Company reports - compiled by Author)

{kind=link}

Here we can see what I mentioned above. While net income is growing consistently, FCF is much more volatile. In cases like these, I like to look at the cash conversion over a couple of years. The sum of the FCF for the fiscal years 2016 to 2022 amounted to a total of $18,984 million. If we divide this by the sum of the net income of $16,147 million, the average cash conversion comes in at around 115%, a very good number.

As the FCF seems to follow the net income (with much more volatility) we should focus on net income from now on. From FY2016 to FY2022, Humana grew net income from $1,648 million to $3,208 million for a CAGR of 11.7%, again a very good number. As a side note, Humana also bought back shares over this timeframe, so earnings per share ((EPS)) grew from $10,92 to $25,24 for a CAGR of 15%, an outstanding number.

So the balance sheet and past financial performance (regarding earnings growth) are very good. Now I want to gauge the quality of the business and this is not as easy as it normally is. I normally use the return on capital employed (ROCE) as my metric of choice to estimate the moat and quality of a business. As an insurance business, Humana has to grow liabilities/total assets to grow earnings. This will naturally lower the company's ROCE.

Humana's ROCE hovered around 15-16% over the past few years which is good but not outstanding. This is one of the rare cases where I think we can also look at the return on equity (ROE). Humana's ROE increased from 15.4% in FY2016 to 20.8% in FY2022 (20.2% TTM), better than the ROCE but still not outstanding compared to more capital-light businesses.

I think that ROCE and ROE are just not good metrics to gauge the quality of this specific business so I will just leave it at that and rely on the excellent past financial performance as an indicator for business quality.

Growth Prospects

For this chapter, I want to focus on two growth drivers: (1) Total addressable market ((TAM)) growth in the Medicare space (Humana's most important and fastest-growing segment) and (2) pricing power. I will go over each factor separately.

1. TAM growth

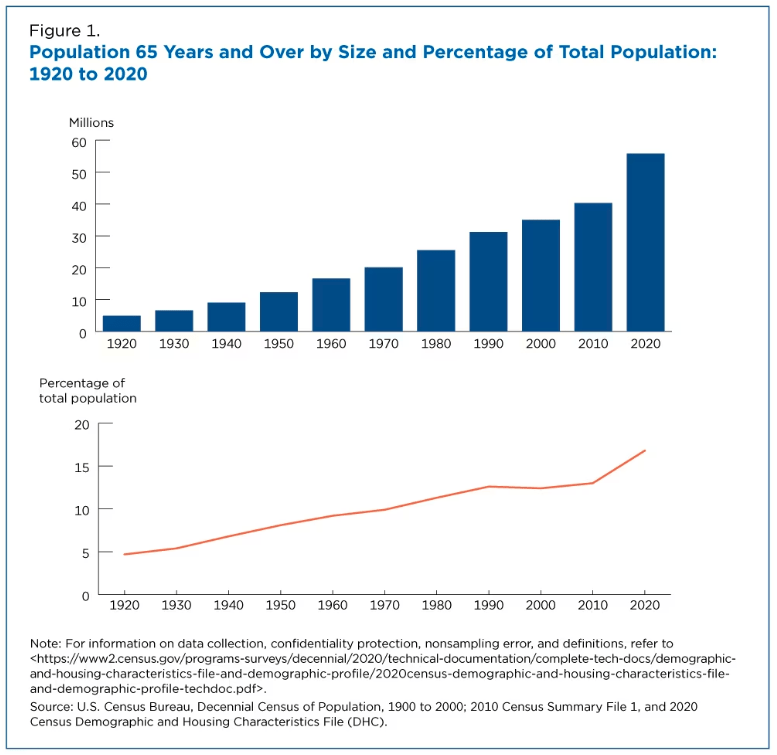

According to the United States Census Bureau , in 2020 there were 55.8 million people age 65+ in the US. These 55.8 million made up 16.8% of the population. The following chart shows the development of the population aged 65+ in millions and as a percentage of the total population:

{kind=link}

As Medicare Advantage is Humana's biggest growth driver, the TAM excluding price increases should grow in line with the growth of the population aged 65+.

According to this article from Reuters , the total number of people aged 65+ is estimated to be 74 million by 2030. Reuters estimated the U.S. population at 54 million at the time that article was published (July 12, 2021), a bit lower than the aforementioned 55.8 million (probably due to deaths because of the pandemic). This would be a CAGR of 3.6% until 2030. This means that assuming zero market share gains and an unchanged Medicare Part C/D penetration, Humana should be able to grow Medicare earnings by 3.6% per year until 2030.

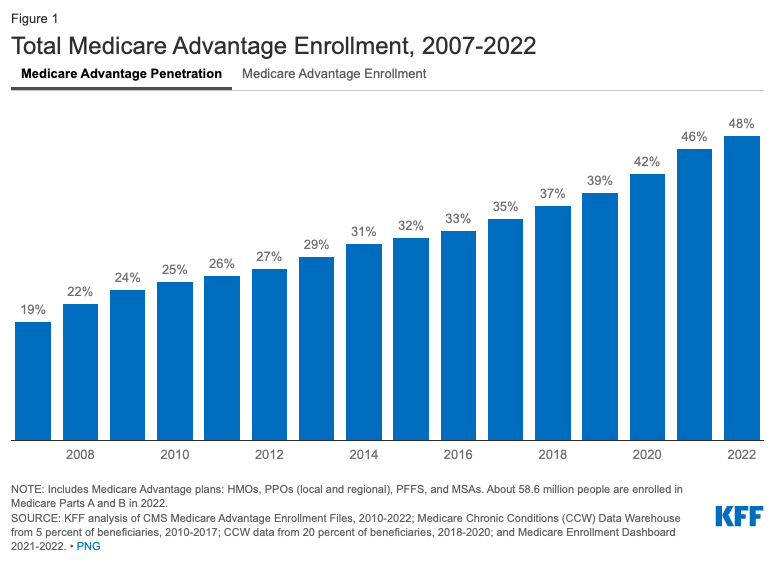

If we look at the following chart from KFF , we can see that Medicare Advantage penetration more than doubled since 2007:

{kind=link}

In conclusion, 3.6% Medicare earnings growth solely through TAM growth seems to be very conservative. Assuming Medicare Advantage penetration to keep growing at let's say 100 basis points per year, Humana should be able to grow Medicare earnings in the range of around 6% per year. Keep in mind that this assumes zero market share growth and doesn't factor in price increases.

2. Pricing power

Since health insurance is a vital expense for everyone (if you don't want to risk going bankrupt any day), it is a non-discretionary expense. Companies that offer non-discretionary services usually have very high pricing power (I highlighted the pricing power of Moody's (NYSE: MCO ) and S&P Global (NYSE: SPGI ) as the duopoly for credit ratings, another non-discretionary expense, in my article on Moody's back in April). This should also be the case here so that Humana should be able to increase prices by at least 2-3% in line with GDP growth. I think that Humana should be able to top this and increase prices by around 4% per year.

Valuation

As I am writing this, Humana trades at $424.70 per share. With 125,564,000 diluted shares outstanding as of the last report, the market capitalization stands at $53.3 billion. TTM net earnings stand at $3,359 million or $26.75 per share so Humana currently trades at 15.4 times TTM earnings.

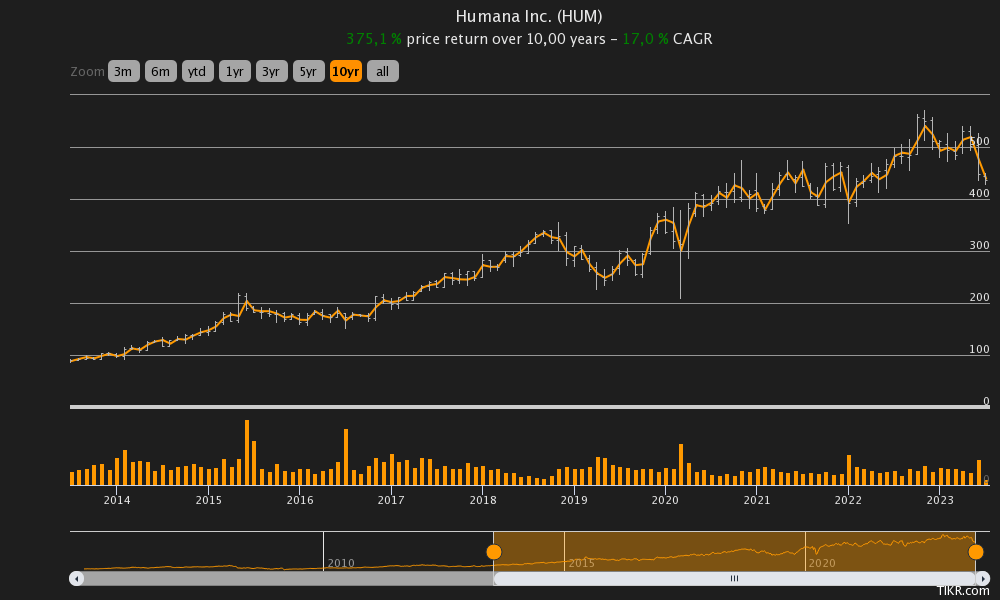

I stated earlier that over the past seven years, the total cash conversion as a sum of all years came in at around 115%. Let's be a bit conservative and calculate with exactly 100% cash conversion so that earnings per share are equal to a normalized FCF per share. In this scenario, the current normalized FCF yield stands at 6.5%. The total long-term return potential of any stock is the sum of the FCF yield and the future growth rate. I highlighted earlier that I think Humana should be able to grow 4% per year solely through pricing power so even without any other growth, we would be looking at 10.5% long-term return potential. Assuming some more growth through the Medicare Advantage TAM growth, total long-term return potential should be in the mid-double digits. This would be a bit below the returns Humana generated over the past 10 years, as can be seen in the following chart:

{kind=link}

We have to keep in mind though that this assumes no changes in valuation, so we need to perform a supplemental DCF valuation to gauge any valuation impacts.

DCF Valuation

We will use $26.75 per share as the TTM FCF per share. Now we need to make some growth assumptions. I already stated that I think Humana will be able to raise prices at around 4% per year, a bit above GDP growth. I will use this as my perpetual growth assumption. Regarding growth until 2030, I highlighted that I think Humana should be able to grow the Medicare business by 3.5% per year solely through TAM growth (no market share gains, no change in Medicare Advantage penetration). This would put growth at 7.5% per year. Let's be conservative again and assume Humana will grow earnings by 5% per year until 2030 and 4% thereafter. Here is the result of a simple DCF calculation using a 10% discount rate:

DCF calculation (moneychimp.com)

Humana shares should be worth around $497 per share, indicating a 17% valuation upside from current levels. In my opinion, my assumptions are very conservative.

Risks

Compared to past growth rates and in light of future growth prospects, Humana's valuation is cheap. The reason is that the health insurance and healthcare space is very vulnerable to regulations. Regulations may hit Humana from three angles:

(1) Drug price regulation: If prices on drug prescriptions are lowered, health insurance will be forced to lower premiums in the process (at the very least to stay in the allowed 80% benefit expenses to premiums range mentioned earlier). Since operating costs and medical care ratios would probably remain unchanged, this would automatically hit the bottom line of all health insurance providers.

(2) A change in the healthcare system: It is no secret that the U.S. healthcare system is very inefficient compared to the systems of other developed nations. According to this article from Harvard Health Publishing , the U.S. scores poorly on many key health measures despite spending far more on healthcare than other high-income nations.

The biggest threat would be a switch from the current multi-payer model to a single-payer model. Here is what Harvard Health Publishing had to say about the single-payer model in an article back in 2016:

In a single payer healthcare system, rather than multiple competing health insurance companies, a single public or quasi-public agency takes responsibility for financing healthcare for all residents. That is, everyone has health insurance under a one health insurance plan, and has access to necessary services — including doctors, hospitals, long-term care, prescription drugs, dentists and vision care. However, individuals may still choose where they receive care. It's a lot like Medicare, hence the U.S. single payer nickname "Medicare-for-all."

Source: Harvard Health Publishing

The introduction of the single-payer model wouldn't make health insurance providers obsolete, but it would hurt their business models a lot.

(3) Medical care ratio regulation: As I stated earlier, the Affordable Care Act of 2010 requires health insurers in the individual and small group markets to spend at least 80% of their premium revenues on clinical care and quality improvements. If this number would be increased to let's say 85% or 90%, it would be disastrous to the bottom line of all health insurance companies.

The big question is how likely is it that such sort of regulation takes place? In my opinion rather low. I want to cite Harvard Health publishing again here:

Stakeholders who stand to lose — such as health insurers, organized medicine, and pharmaceutical companies — represent a powerful opposition lobby. Public opinion needs to be redirected to focus on how the net benefits of a single payer system outweigh the tradeoffs discussed above. Furthermore, despite the individual level savings, behavioral economics predicts the general public will wince at the notion of transferring healthcare spending from employers to higher taxes managed by the federal government. Additionally, despite long term savings projected from moving to a single payer system, the upfront costs of the transition are also politically unpopular.

Source: Harvard Health Publishing

With all the opposing lobbies and the political requirements that have to be met to bring about these kinds of regulatory changes, the risks seem low to me.

Conclusion

Humana is close to a pure play on the health insurance sector, especially Medicare Advantage. The company has benefitted from the growth in people aged 65+ that are eligible for Medicare and an increasing Medicare Advantage penetration. Since the population aged 65+ is estimated to grow at a decent pace until 2030, there are no signs for this trend to stop. The comments from UNH's CFO in the middle of June started a sell-off in the share price that is persisting since then.

I think that TAM growth + pricing power + FCF yield should be able to generate mid-double-digit long-term returns going forward. Additionally, my DCF valuation indicated a potential valuation upside of 17%.

Risks are concentrated around several regulatory risks which I described in the risk chapter. Due to opposing lobbies and high political hurdles to bring about changes regarding any of the threatening risks, I rate the risk rather low.

In conclusion, I rate Humana a buy at the current price of $424.70.

For further details see:

Humana: Recent Selloff Might Present A Buying Opportunity