HUM - Humana: Rising Medical Costs Should Be Temporary

2023-06-28 12:21:06 ET

Summary

- Humana's share price has declined over 15% in the past two months amid the fear of rising medical costs.

- The increase in medical costs should be temporary, and will likely normalize after push-back procedures are being handled.

- The company's ongoing expansion into the healthcare services industry should expand its growth opportunities moving forward.

- The current valuation is attractive with multiples discounted compared to both peers and its own historical average.

Investment Thesis

Humana's ( HUM ) share price has slumped over 15% in the two months as investors are worried about the potential impact of rising medical costs. However, the headwind should be temporary, and the company's fundamentals remain intact. It has been actively expanding into the healthcare services segment through its new brand CenterWell, which should further increase its growth opportunities moving forward.

Rising Medical Costs

While the market seems highly concerned about the rise in medical costs, as reflected in the share price, I believe the impact should only be temporary. The increase in medical costs is largely attributed to pent-up demand and delayed surgery & procedures. As noted by HCA Healthcare ( HCA ), many hospitals faced staffing shortages during the pandemic and therefore pushed back a lot of non-emergency surgery & procedures.

Sam Hazen, HCA's CEO, on capacity constraints in Q4

Even with the progress, we continued this quarter to experience capacity constraints, creating situations where we were unable to deliver services in certain situations.

As the pandemic finally wanes and hospital capacity eases, these patients are now rushing back in all at once, which causes demand to surge. Once this wave of patients is being taken care of, demand and medical costs should normalize. On a positive note, Humana also reaffirmed its EPS guidance for FY23.

Expanding Beyond Insurance

Humana is a leading healthcare insurance provider in the US, currently serving over 17 million members. Amid the success of UnitedHealth's ( UNH ) Optum, it has also been trying to expand beyond insurance into other sectors. In 2021, the Kentucky-based company formed a subsidiary named CenterWell, which mostly focuses on healthcare services such as primary care and home health.

Primary care has been CenterWell's major priority, as it presents a massive addressable market. According to Grand View Research , the US primary care market is forecasted to grow from $271 billion in 2023 to $339.6 billion in 2030, representing a CAGR (compounded annual growth rate) of 3.3%.

In order to capture more market share, the company plans to double its staffed center from around 200 currently to 400-450 by 2025. It is also actively pursuing acquisition opportunities to expand its footprint. For instance, the company acquired 7 medical groups in the past few years,

{kind=link}

Humana is also targeting the fast-growing home health industry. The company completed the acquisition of Kindred at Home in 2021 and subsequently rebranded it into CenterWell Home Health, which was launched last year.

According to Fortune Business Insight , the US home health market is forecasted to grow from $94.2 billion in 2022 to $153.2 billion by 2029, representing an excellent CAGR of 7.2%. The expansion continues to be driven by the increase in the aging population, especially with life expectancy rising. According to the World Health Organization , the percentage of the population above 60 years old will rise from 12% in 2015 to 22% in 2050.

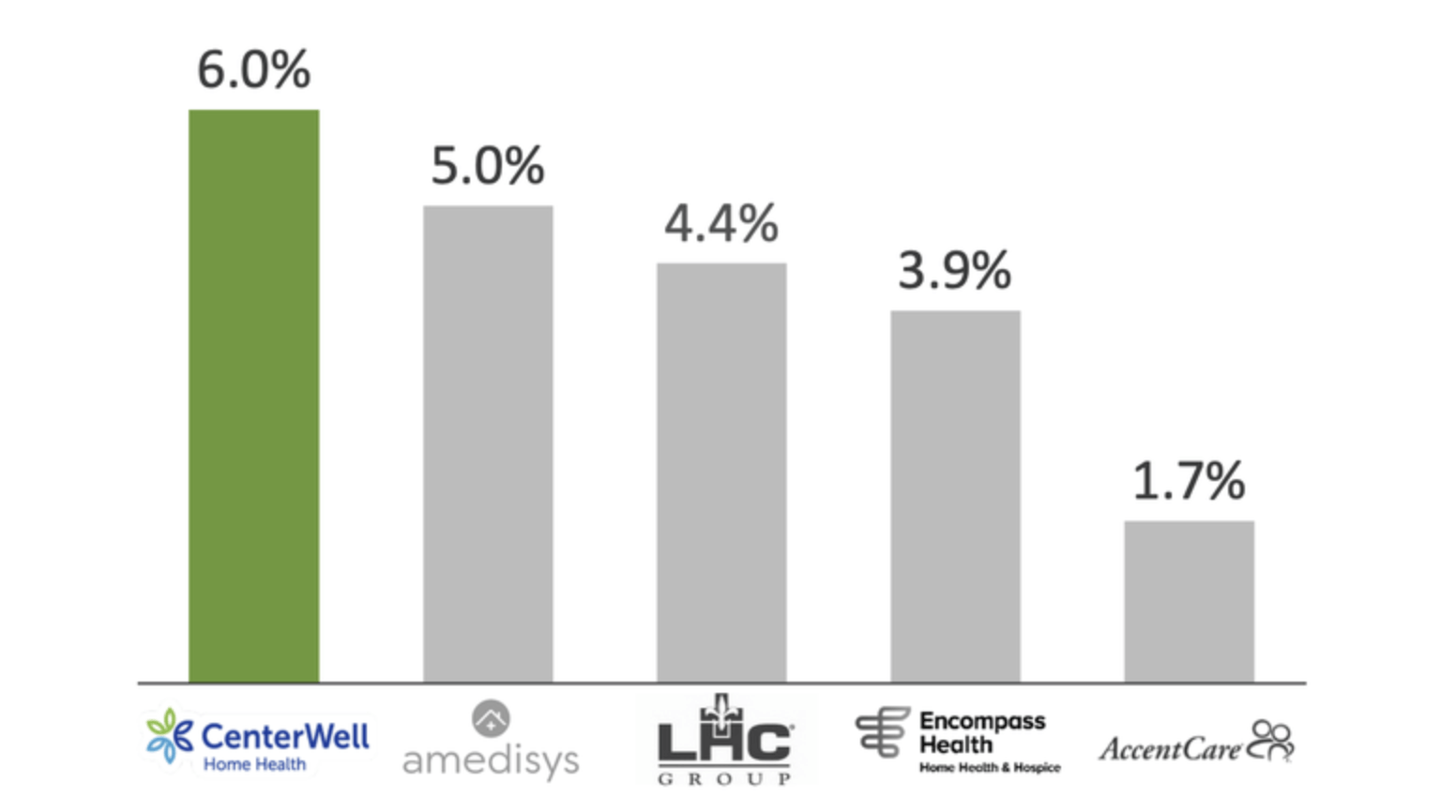

The market is also extremely fragmented, which presents ample expansion opportunities. As shown in the chart below, no company has a market share above 5% besides CenterWell. The company's leading position gives them a significant competitive advantage as their footprint is hard to match against. For instance, it currently operates 352 locations with over 9,000 clinicians.

Home Health Market Share (Humana)

{kind=link}

Valuation

After the drastic decline in share price, Humana's valuation looks attractively priced. The company is currently trading at a PE ratio of 18.1x, which is pretty modest compared to other healthcare insurance companies such as Elevance Health ( ELV ) and Centene Corp ( CNC ), as shown in the first chart below. The peer group currently has an average PE ratio of 21.5x, which represents a meaningful premium of 18.8% above Humana. The valuation is also cheap on a historical basis. As shown in the second chart below, the multiple is now back at the low end of its historical range, representing a discount of 10% compared to its 5-year average PE ratio of 20.1x.

Notable Risk

Besides rising medical costs, competition is another notable risk for Humana, especially in the home health segment. Much like Humana, UnitedHealth has also been eyeing the fragmented and fast-growing home health market.

After acquiring LHC Group for $5.4 billion last year, it is now trying to acquire Amedisys ( AMED ) for $3.3 billion. As shown in the chart above, these two companies are the second and third largest players in the industry. If the deal goes through, UnitedHealth will surpass Humana as the leader with a market share of 9.4%, which will likely meaningfully weaken its competitive advantage.

Investors Takeaway

I believe the recent drop in share price amid the fear of rising medical costs presents a compelling buying opportunity for Humana. The increase in costs will certainly have an impact in the near term but it should only be temporary. The company has also been diversifying away from healthcare insurance into the healthcare services market, which should expand its growth opportunities.

The discounted valuation seems unjustified as the company's fundamentals have been improving, as it continues to increase its presence in the healthcare services industry. For instance, UnitedHealth's valuation has risen substantially in the past decade amid the increasing presence of Optum. If Humana successfully replicates this playbook, it could see meaningful upside potential moving forward.

For further details see:

Humana: Rising Medical Costs Should Be Temporary