HURN - Huron Consulting Group: Growth May Not Be Sustainable

2023-10-19 10:51:08 ET

Summary

- Huron’s revenue has grown at a CAGR of 9% during the last decade, driven by industry tailwinds and a quality go-to-market approach by the business.

- Its specialism in particular industries has allowed the business to gain market share and expand its operations. We see healthy growth possible in the coming years.

- Huron’s expansion into the Digital segment has been successful, with strong growth and market share gains. Given the level of competition, however, we are unconvinced by the long-term growth potential.

- Huron’s performance relative to its peers is underwhelming, while its valuation appears punchy. We do not see sufficient value at today’s price.

Investment thesis

Our current investment thesis is:

- Huron (HURN) has developed a strong market presence, with its current strategy positioning the company to achieve healthy growth in the coming years (LSD/MSD). The concern we have is that its growth trajectory beyond this is not wholly convincing in our view.

- Digital is performing exceptionally well currently but this is owing to its aggressive expansion strategy and the utilization of its existing advantages. Beyond this, all we see is high competition and a pricing environment that is a race to the bottom. Further, the importance of expanding its services offering inherently implies a weakness in organic growth potential and this is not a sustainable strategy.

- With Huron's performance relative to its peers uninspiring and its valuation not glaringly suggesting value, we do not consider the company attractive today.

Company description

Huron Consulting Group, Inc. is a global professional services firm that provides consulting services to clients in various industries, including healthcare, life sciences, higher education, and business services. The company is headquartered in Chicago, Illinois, and operates internationally.

Share price

Huron's share price performance has been respectable, returning almost 100% during the last decade. Much of these gains have occurred post-2022, as the company's financial performance has accelerated.

Financial analysis

{kind=link}

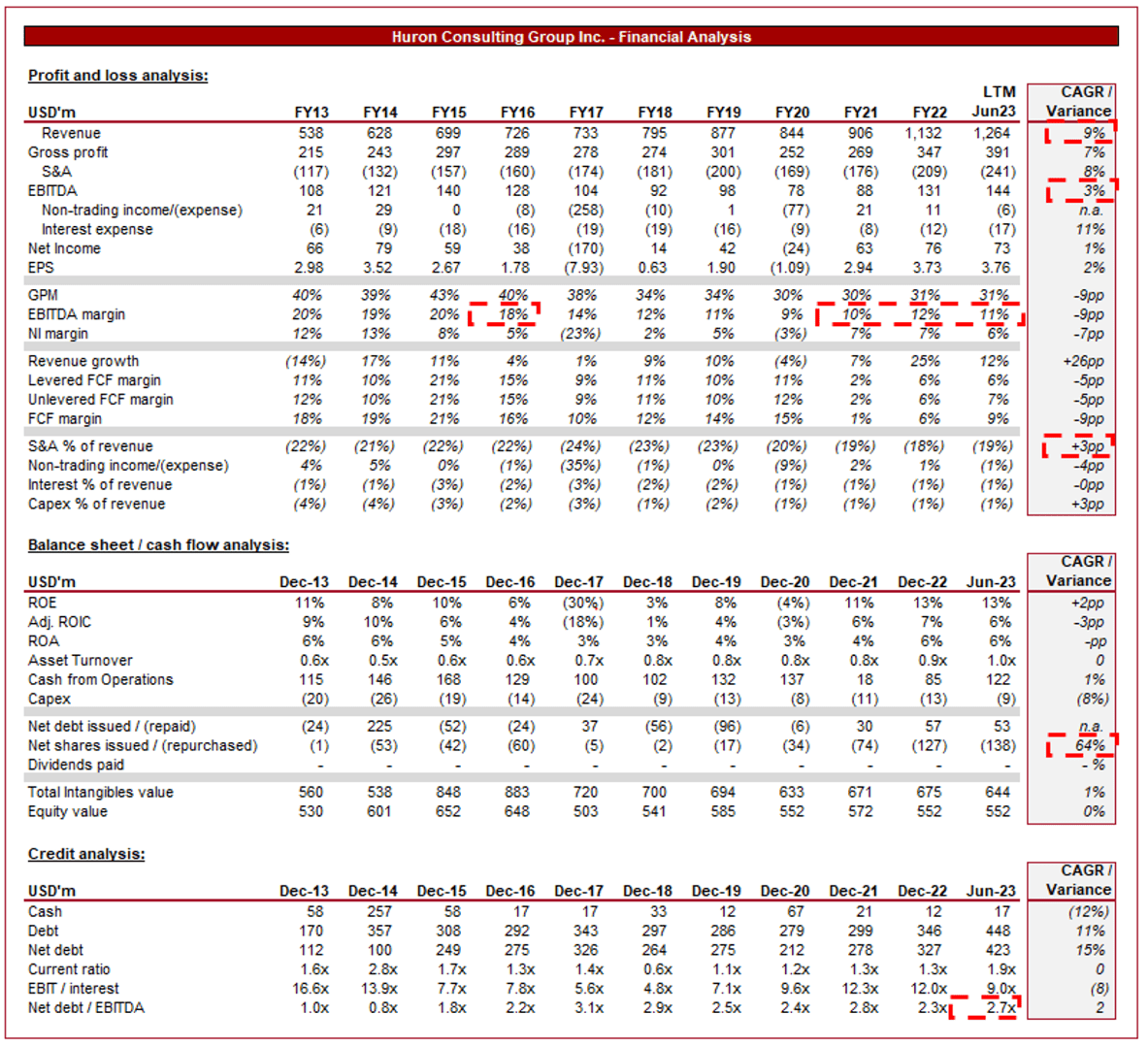

Presented above are Huron's financial results.

Revenue & Commercial Factors

Huron's revenue has grown at a CAGR of 9% during the last decade, with broadly consistent growth year-on-year. EBITDA has lagged this, however, increasing at a 3% rate as margins have contracted.

Business Model

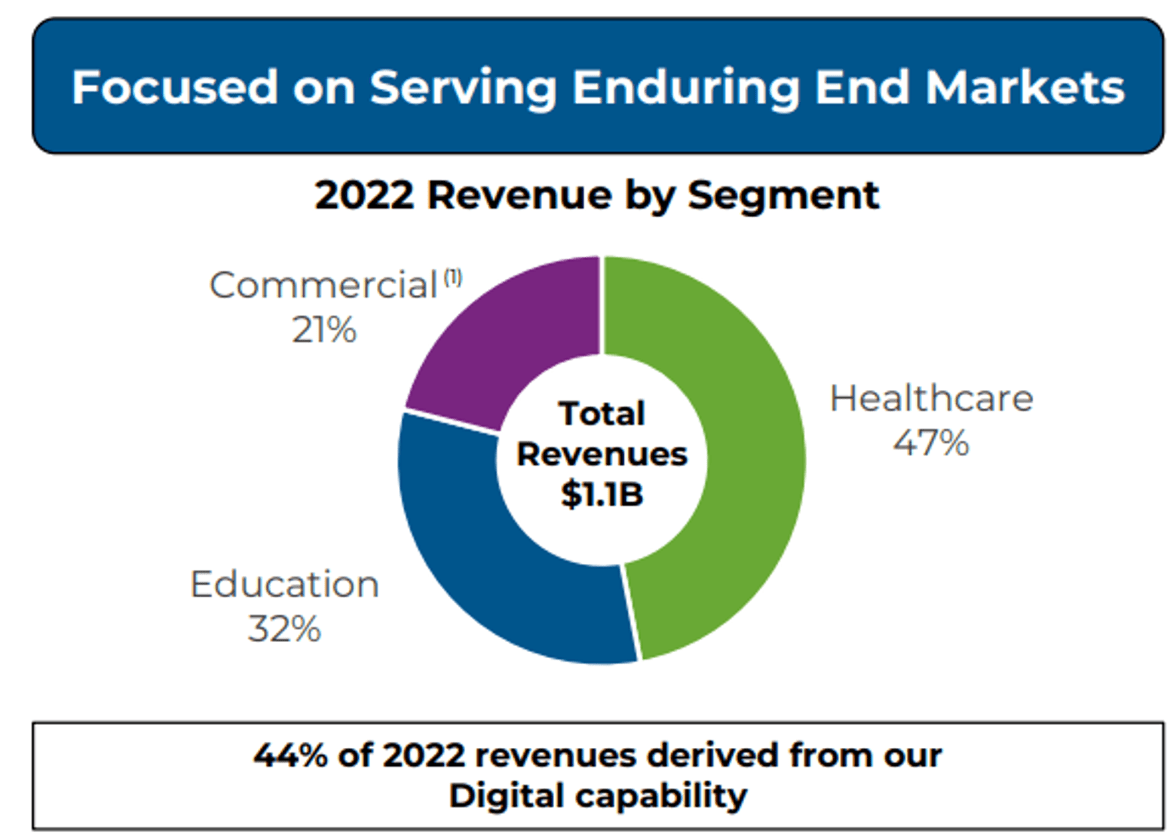

Huron is a global consulting firm that offers a wide range of services to help organizations solve complex business challenges. Huron is known for its specialized expertise in areas such as healthcare consulting, life sciences, education, financial consulting, and operational improvement. This segmentation focus has allowed them to develop deep expertise and gain market share within its niche. As the following illustrates, 47% of its revenue is derived from the Healthcare segment, with a further 32% from Education and 21% from Commercial.

{kind=link}

Huron operates globally, serving clients not only in North America but also in Europe, Asia, and other regions. This global presence allows them to address the needs of multinational organizations.

Huron provides management and strategy consulting services, helping clients optimize their operations, improve performance, and develop long-term strategies for growth. In addition to consulting, Huron offers technology solutions that help organizations streamline their processes, enhance data analytics, and make data-driven decisions. These solutions often involve the implementation of enterprise software and data management systems. Management refers to this segment as "Digital" and it represents a key growth area for the company, now comprising 44% of revenue. The development of its digital capabilities is highly lucrative in our view, as it has allowed the business to expand its relationship with its existing clients through cross-selling, and utilize its brand to gain market share quickly, while also modernizing its offering in a higher growth industry.

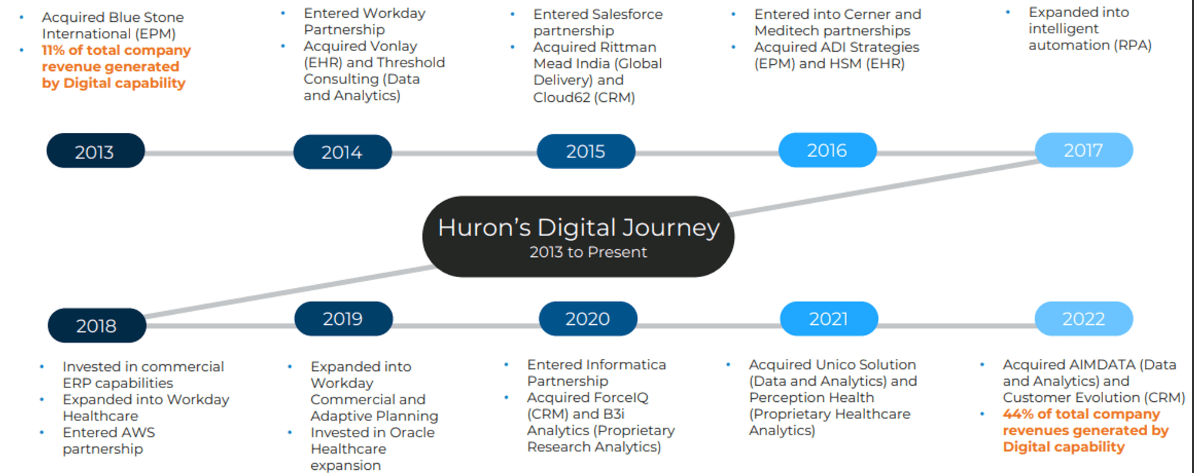

As the following timeline shows, Management has developed its expertise consistently since 2013, with both organic and inorganic growth. This continues to be the case, with Huron seeking to continually develop the complexity of the services it provides, with the benefits being greater differentiation and stickier revenue.

{kind=link}

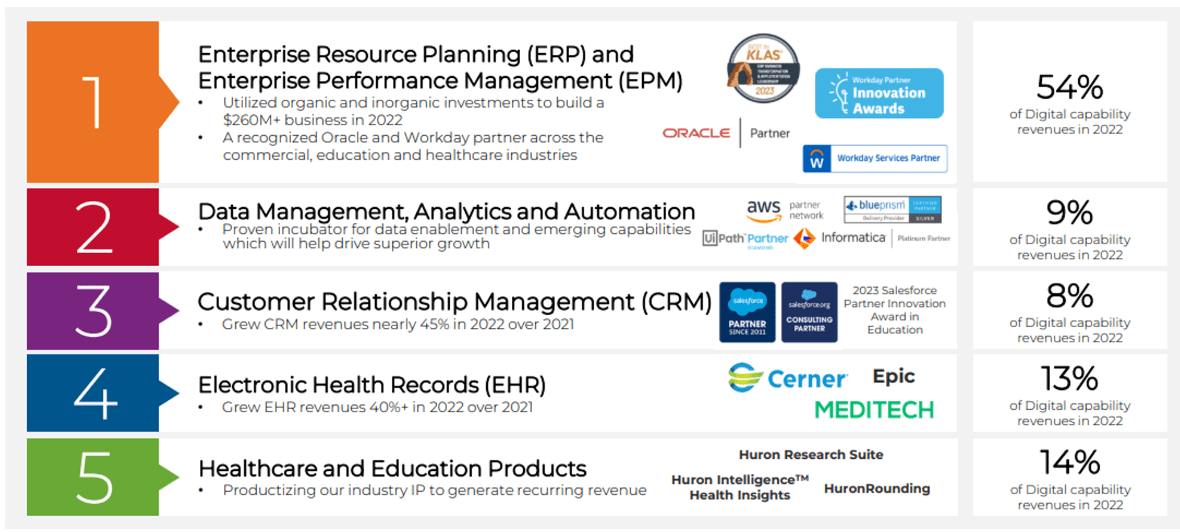

The services the Digital segment currently provides are operations-related, seeking to modernize its clients' infrastructure and improve efficiency. The concern we have with this as a growth strategy is that these services are offered by a large number of businesses, with no material way to differentiate. For this reason, there is a risk that Huron's growth from this segment is predicated on its ability to win clients in its specific niche (industry targeting), as well as through existing relationships. This may not have a long-term growth runway. This is why developing the complexity of its services is critical.

{kind=link}

Management has utilized capital to expand the business inorganically, acquiring businesses to expand its Digital offering (primarily). During the last decade, Huron has spent over $600m, allowing the business to achieve a modest foothold in a highly competitive industry. Going forward, the company's criteria for acquisitions are:

- Aligns with business strategy - Huron is seeking to expand its services offering within its area of expertise, as well as deepen its capabilities within existing segments. Given the mature nature of the consulting industry, we believe this is a critical objective.

- Enhances financial strategy - Huron is seeking to acquire growing businesses that are accretive on an EBITDA-M basis. Although it should be obvious, far too many companies make this mistake. At a minimum, investments must be margin-neutral but ideally exceed the company's existing ROE.

- Strong cultural fit - 2/3 of acquisitions are businesses Huron has already worked directly with. Given consulting is an industry of human capital, we consider this an incredibly important criterion. Working with its targets as a preference is a quality way to identify culture.

Consulting Industry

Huron competes with other consulting firms, including larger players like Deloitte, PwC, and Accenture, as well as smaller niche consulting firms specializing in specific industries.

The consulting industry has experienced consistently strong demand over the last 2 decades, although there has been a noticeable acceleration in particular segments/industries. Healthcare and Education continually face evolving regulations, financial pressures, technological advancements, and operational complexities, creating a need for expert guidance. Further, the rapid development of technological capabilities for operational improvement has required the need for third parties to support corporates with integration and utilization. Management estimates that its TAM in the Consulting segment is $32b, with a further $95b for Digital.

TAM (Huron)

Huron's specialization in key sectors, such as healthcare and education, positions them as trusted advisors with deep industry knowledge. Market observations suggest clients often prefer firms with domain expertise. As the following suggests, this specialization is not restricting the company's growth trajectory, with a substantial TAM to tap into.

TAM (Huron)

The following factors are expected to drive growth in the coming years by segment:

- Strengthening Huron's market-leading position -

- Healthcare - Broadening its Digital penetration alongside continued new client wins.

- Education - Accelerating its growth in research consulting services. Huron is well positioned, already working with all of the top 100 research Universities in the US.

- Commercial - Developing a foothold in key industries that have scope for growth, such as Oil and Gas. Further, developing its existing services to create an attractive value proposition within the industries it has initially expanded into (FS, Energy and utilities, and the Public Sector).

- Growing its Consulting offering -

- Healthcare - Expanding its services in federal health and payor offerings. Additionally, advancing its healthcare-focused financial advisory services and more broadly widening its capabilities. This will likely be achieved through M&A.

- Education - Broadening its current services offering, with substantial opportunities in what is an industry ripe for operational improvements through modernization.

- Commercial - Deepening its industry expertise to develop a reliable brand. Again, this will likely come through M&A.

- Advancing Digital capabilities -

- Healthcare - Continuing its services expansion and market penetration.

- Education - Continuing to grow its core education offerings.

- Commercial - Continuing to grow its core education offerings.

We believe this should allow Huron to exceed the Healthcare industry growth rate in the medium term, particularly due to its strong market penetration. The industry clearly has good trust in Huron's capabilities.

We also see scope for good growth in the education sector, although on an absolute basis, the rate may not be substantial. This is owing to the slow-moving nature of the industry.

Finally, it is still early days in the Commercial segment. Growth has been good thus far but it is far too early to suggest significant growth will come from this segment.

Huron's quarterly results support this aggressive expansion strategy, with a consistent >18% YoY appreciation for the last 7 quarters.

Although this implies its current growth rate is sustainable in the short-to-medium term, we are less convinced going forward. The constant need to expand its services is illustrative of the weak organic growth achievable on a LfL basis. Consulting and Digital are highly competitive and although Huron is doing well, we do not think the company is a standout.

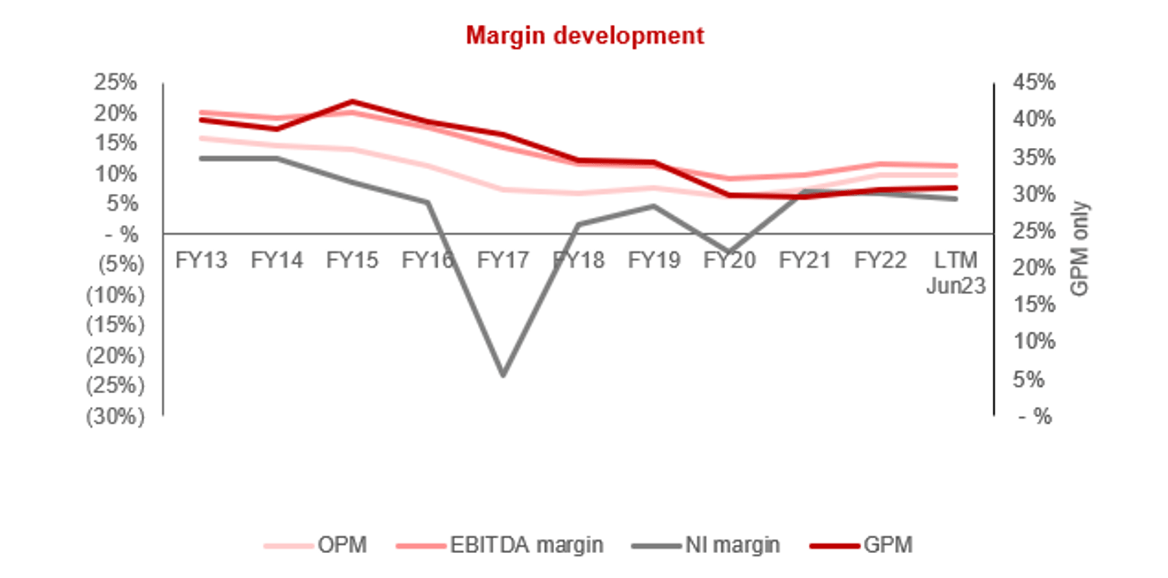

Margins

{kind=link}

Huron's margins have declined consistently during the historical period, normalizing at close to a decade-low level. This is a reflection of a change in product mix, dilution through expanding its services, and labor cost inflation.

Although we expected some erosion through growth, we are disappointed by the degree to which Huron has lost out. Management's focus on growth has been far too costly in our view. Given the level of competition in the Digital segment, we do not expect this to drive margin improvement, as many of its peers are already operating in low-cost locations to provide these services.

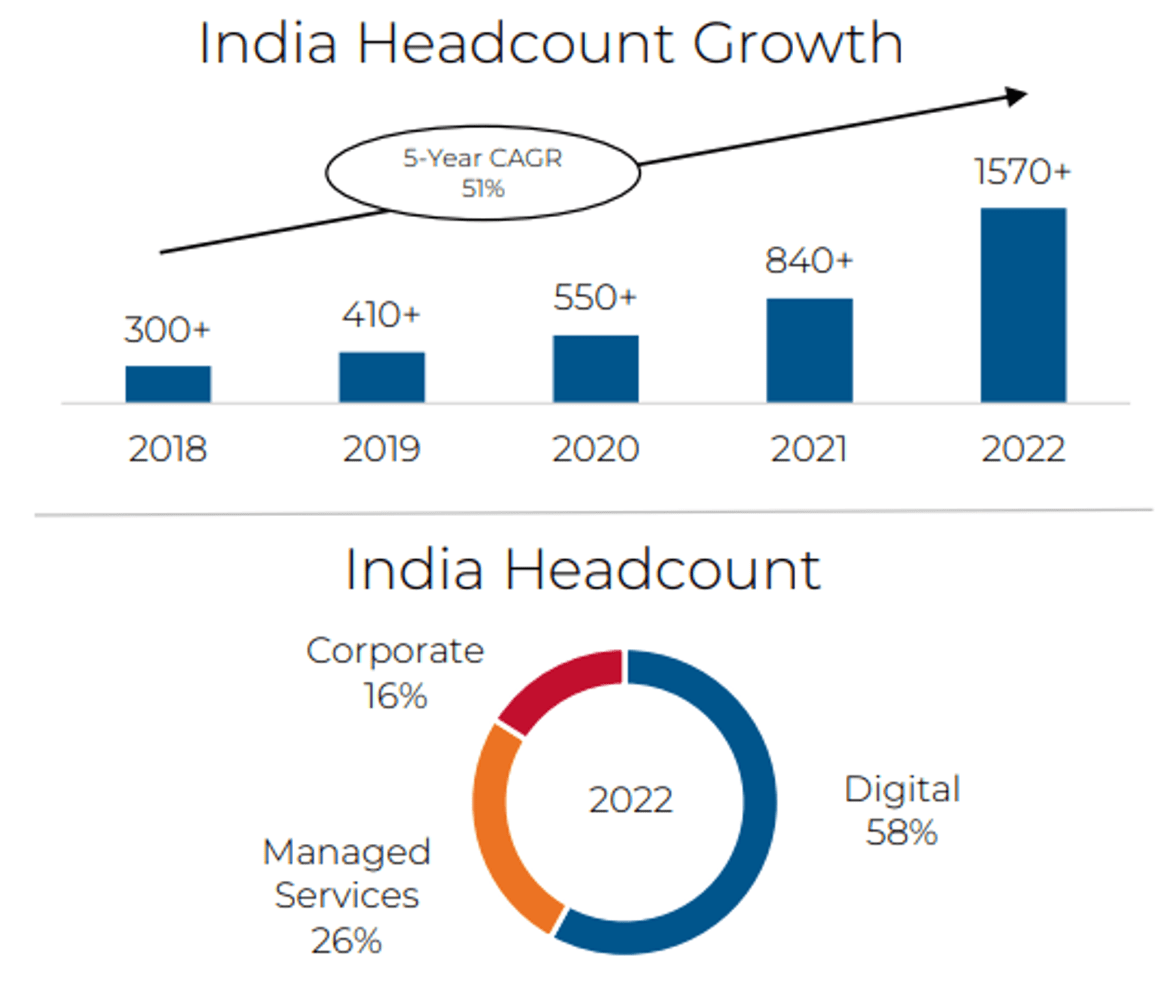

Nevertheless, Huron is catching up, investing heavily in Indian talent, which should contribute to some incremental margin improvement, although not materially so.

{kind=link}

Balance sheet & Cash Flows

Huron's balance sheet is relatively uneventful. The company is conservatively financed, with the majority of its "Debt" balance relating to long-term leases.

The company's margin deterioration is reflected in its ROE, which has struggled to exceed the low teens. Further, its FCF has equally declined alongside this, falling into the single digits. The variability of returns is quite unattractive.

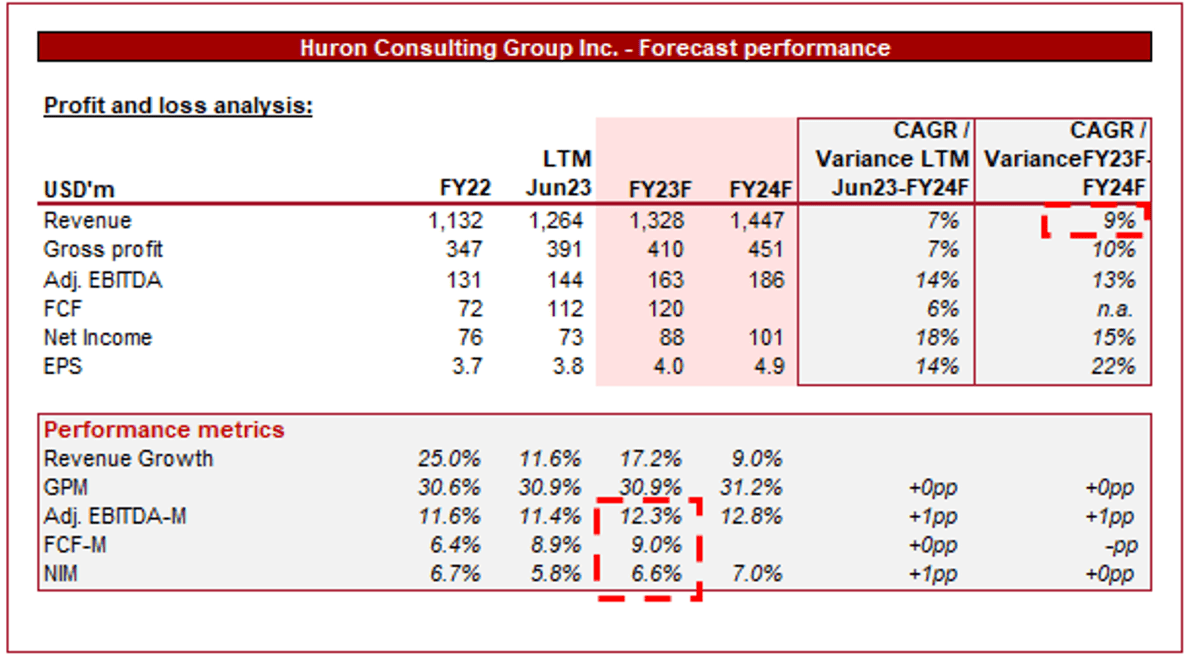

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a continuation of its current growth rate, with a CAGR of 7% into FY24F. In conjunction with this, margins are expected to slightly tick up, although not to a material level.

We believe this is broadly reasonable, as Huron continues to execute its existing strategy, which should allow for HSD growth in the medium term. Further, the lack of an increase in margins is aligned with our view that competition will restrict improvement.

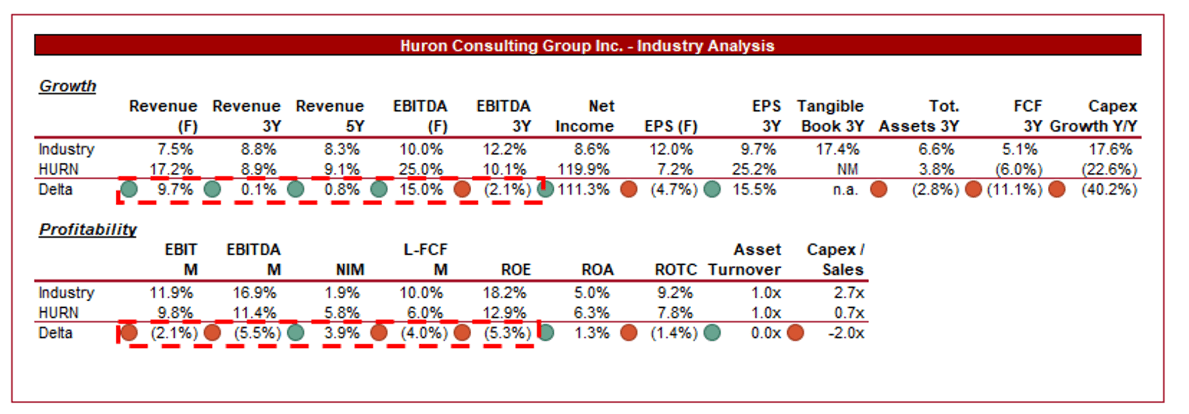

Industry analysis

{kind=link}

Presented above is a comparison of Huron's growth and profitability to the average of its industry, as defined by Seeking Alpha (29 companies).

Huron performs modestly relative to its peers. The company's growth, particularly from a revenue perspective, is strong, outperforming the average across various time periods. Not only this but its commercial improvement is expected to drive a larger delta on a forward basis.

On a margin basis, however, Huron is lacking to a significant degree. This is a reflection of the company's scale and relative competitiveness within the market, restricting its ability to price at a substantial premium.

Given the maturity of the industry, our belief is that margins are more valuable than growth and so we believe Huron should trade at a discount to its peer group.

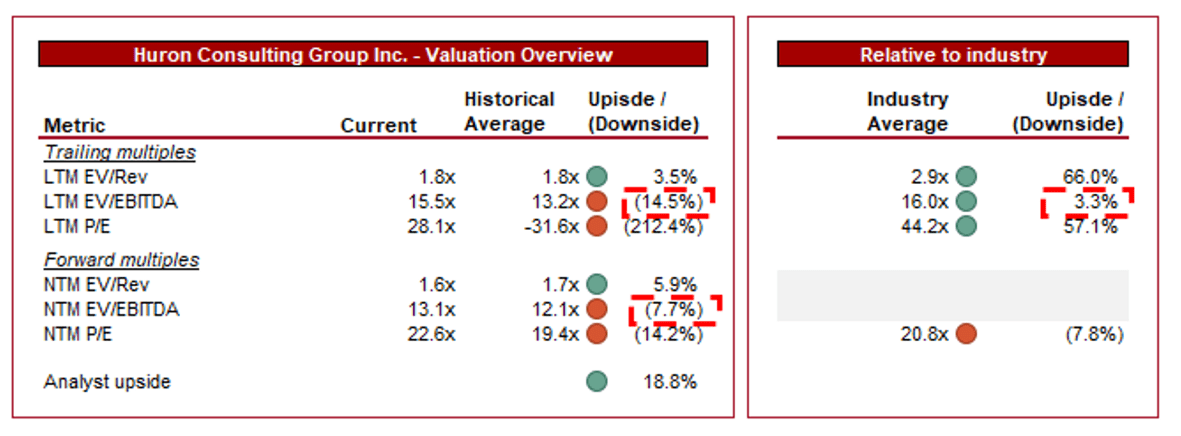

Valuation

{kind=link}

Huron is currently trading at 16x LTM EBITDA and 13x NTM EBITDA. This is a premium to its historical average.

A premium to its historical average is reasonable in our view. Although the company's margins have deteriorated, Huron was likely undervalued during this time, contributing to a low trading multiple. This has resulted in an upward-trending valuation while margins have deteriorated. We believe a low double-digit valuation is reasonable in the context of its HSD growth and c.12% EBITDA-M.

Further, Huron is trading at a discount to its industry average, although not to a substantial degree on an EBITDA basis. We consider PE less appropriate here given various outliers within the data set. Given the financial weakness, we are less convinced by this despite the HSD growth on offer.

Final thoughts

Huron is a solid company. Its focus on specific, growing industries has allowed it to achieve attractive growth in recent years. The industries are sufficiently large that Huron has a good runway to achieve LSD growth long term. Its expansion into the Digital segment is understandable and observed in many of its peers) given it has the potential to push this growth rate up further. We are not wholly convinced by it, however, given the level of competition. We do think Huron will continue to do well in the next few years, owing to its strong position within particular industries, but beyond this, it is difficult to envisage.

We think the company's valuation appears reasonable but does not suggest a substantial upside. At a comparable EBITDA multiple to its peers, investors can buy better margins/FCF, while still getting exposure to growing segments.

For further details see:

Huron Consulting Group: Growth May Not Be Sustainable