HURN - Huron Consulting Stock: The Best Play Of Its Industry

2023-03-18 06:25:42 ET

Summary

- Huron Consulting Group is a $1.3 billion market cap professional services firm that works in Healthcare, Education, and Commercial end markets.

- The company's financials look solid. I expect Huron to show further margin improvement in FY2023.

- HURN stock seems a bit expensive today, with an FCF yield of only 3.9% - well below historical levels. But it's one of the most undervalued names in its industry.

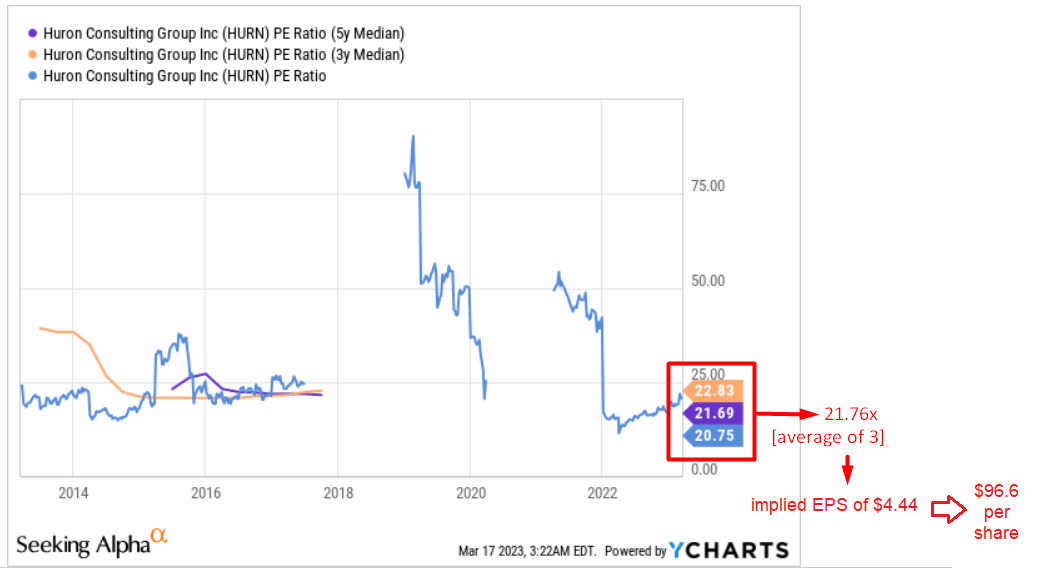

- I estimate HURN's upside potential to be about 27.9% by the end of 2023 - with a P/E multiple of 21.76x; the company should be worth ~$96.6 per share.

Intro & Thesis

Being a generalist analyst/investor by nature, I like to look at different sub-industries - Research and Consulting being one of them. In late December 2022, I wrote an article on CRA International (CRAI) and a week earlier on CBIZ (CBZ), both of which were undercovered here on Seeking Alpha to my surprise. Now my eyes are on Huron Consulting Group Inc. (HURN) - a $1.3 billion market cap professional services firm that works with clients to develop growth strategies, optimize operations, and accelerate digital transformation by leveraging a portfolio of technology, data, and analytics solutions to drive sustainable results for their businesses [description given by the company's most recent 10-K filing ].

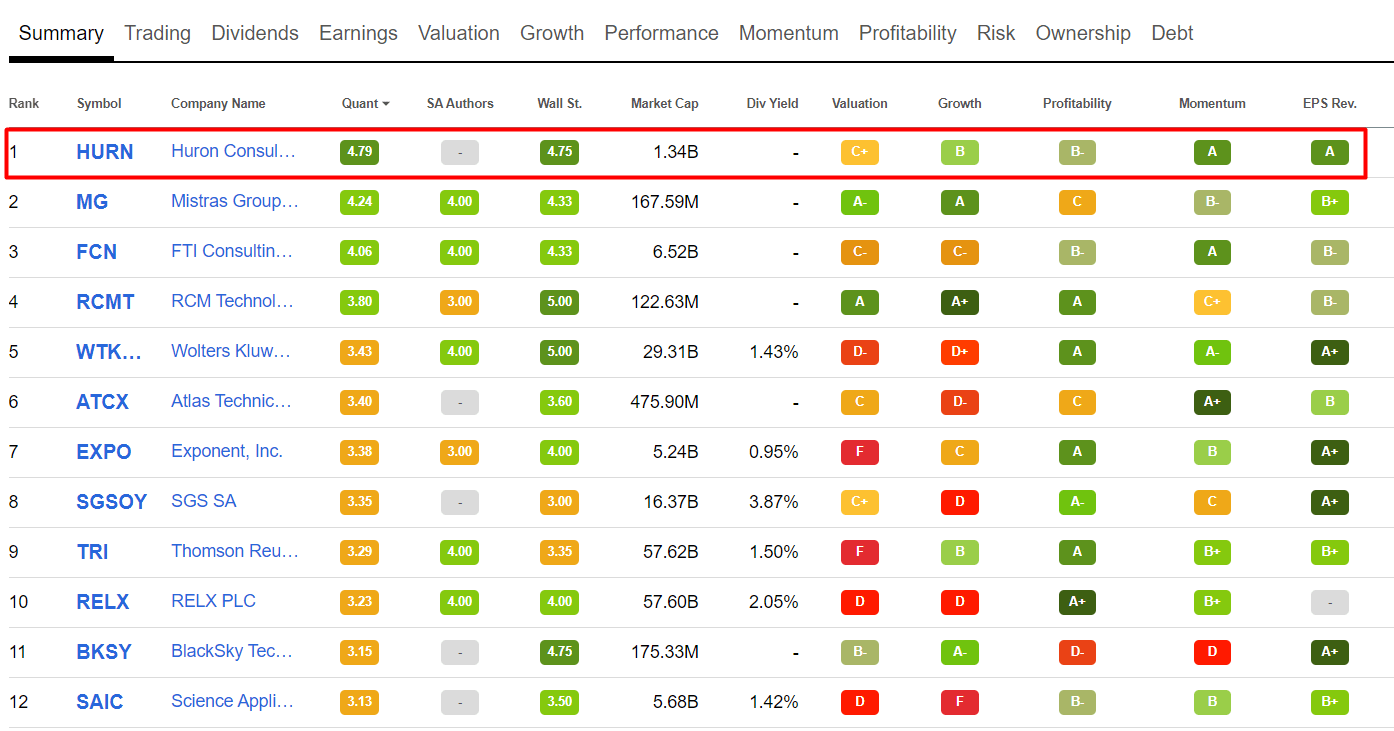

Although HURN has not received any coverage since mid-November of last year, it currently holds the highest rating among all stocks in its group according to the Quant ranking system by Seeking Alpha:

{kind=link}

I believe that among the undercovered stocks, one can find really high-quality names that are still not crowded enough. HURN seems to be just such a company - this is my conclusion after the analysis you'll find below. Although HURN seems slightly overpriced, I still believe in the continuation of last year's growth and set a price target of $90 per share, which is about 20% above today's level. Not a huge upside, but upside nonetheless. Let's dive in.

What is Huron Consulting Group?

As I briefly described above, Huron Consulting Group is a professional services firm that provides expertise in strategy, technology, operations, advisory services, & analytics through 3 operating segments:

- Healthcare - 47% of total sales and 50.42% of total EBIT - helping clients to transform and innovate the delivery model to focus on patient wellness by improving quality outcomes, minimizing care variation, and fundamentally improving patient and population health;

- Education - 31.77% of total sales and 30.33% of total EBIT - providing management consulting and technology solutions;

- Commercial - 21% of total sales and 19.23% of total EBIT - providing services to large and middle-market organizations, not-for-profit organizations, and private equity firms.

Note: Author's compilation based on 10-K filing and Morningstar Premium

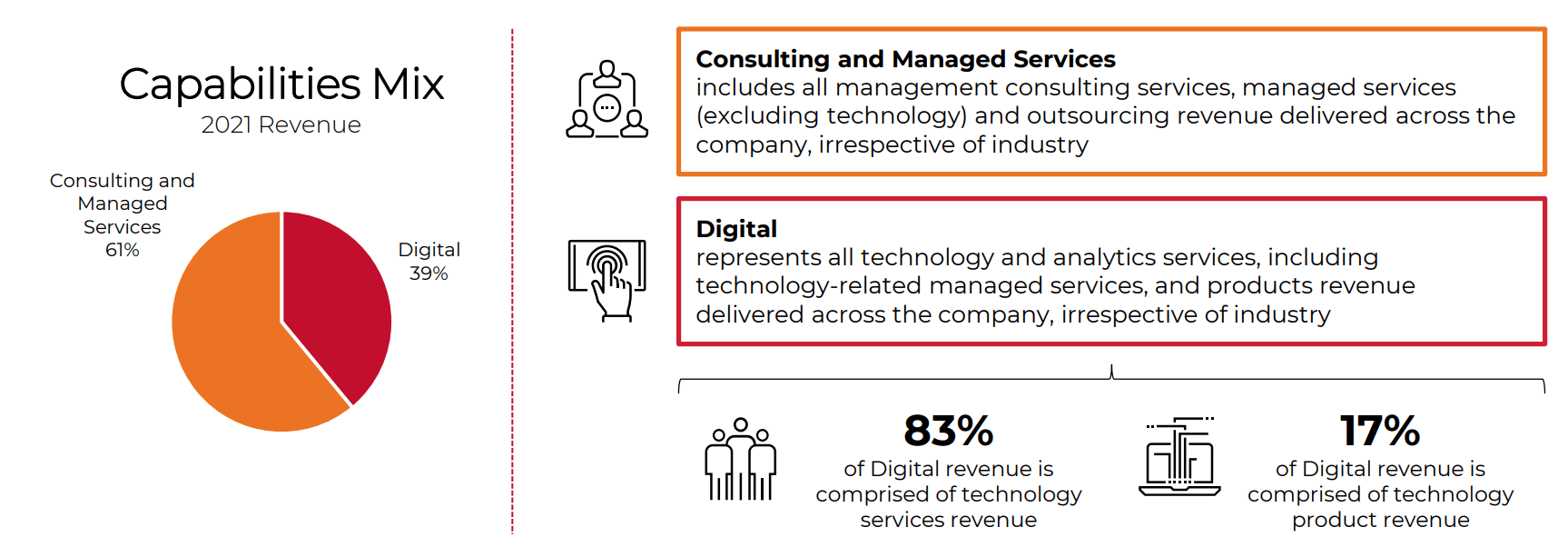

In addition to end markets, HURN's management presents the company's revenue model directly based on 2 operational activities:

- Consulting and Managed Services - 56.34% of total sales;

- Digital - 43.66% of total sales.

{kind=link}

Huron Consulting's Financials Look Solid

I suggest starting with the dynamics of the end markets since this is where the company reveals the most information.

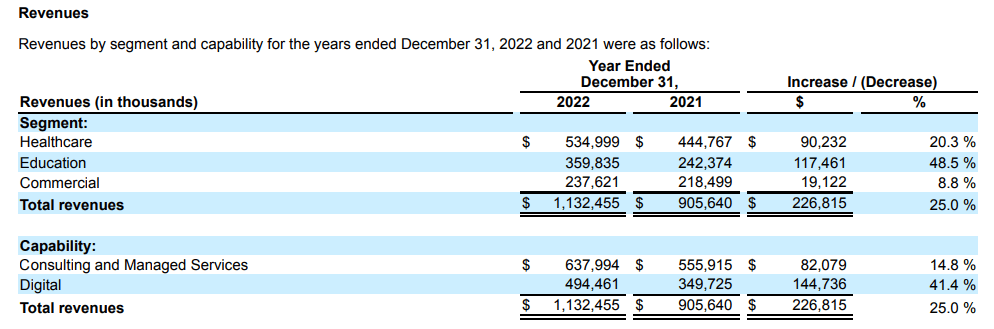

Healthcare is a sector that has been growing rapidly - HURN reported a 20.3% YoY increase in FY2022, driven by strengthened demand for their technology and analytics services and software products within the Digital capability. Additionally, there was increased demand for HURN's revenue cycle managed services and performance improvement solutions within the Consulting and Managed Services capability, the MD&A section mentions. The actual revenue growth also includes incremental revenues of $6.0 million from the acquisition of Perception Health, Inc. [closed on January 3, 2022].

In the Education sector, Huron saw a significant increase in demand across all of its services and products within the Consulting and Managed Services and Digital capabilities, the management notes. This growth resulted in a revenue increase of $117.5 million, or 48.5%, in FY2022. The Education segment's revenue growth includes incremental revenues of $8.2 million from the acquisition of Whiteboard Communications Ltd . Furthermore, HURN experienced a 50.4% increase in the number of revenue-generating professionals within its Education segment, a testament to the growing reach and impact in this sector.

The Commercial business segment experienced an 8.8% YoY increase in revenue, with a growth of $19.1 million driven by the strengthened demand for the technology and analytics services within the Digital capability, and corporate finance advisory solutions within the Consulting and Managed Services capability. This growth was partially offset by a decrease in revenue due to the divestiture of the Life Sciences business in Q4 FY2021 and a decrease in demand for the financial advisory solutions within the Consulting and Managed Services capability, based on HURN's 10-K. The Commercial segment's revenue growth includes incremental revenues of $3.0 million from the acquisitions of AIMDATA, LLC and Unico Solution, Inc. Furthermore, Huron experienced a 20.6% YoY increase in the number of revenue-generating professionals within its Commercial segment.

As a result of these changes in the business segments, consolidated revenues increased by 25% compared to the previous year, with each operating activity showing growth:

{kind=link}

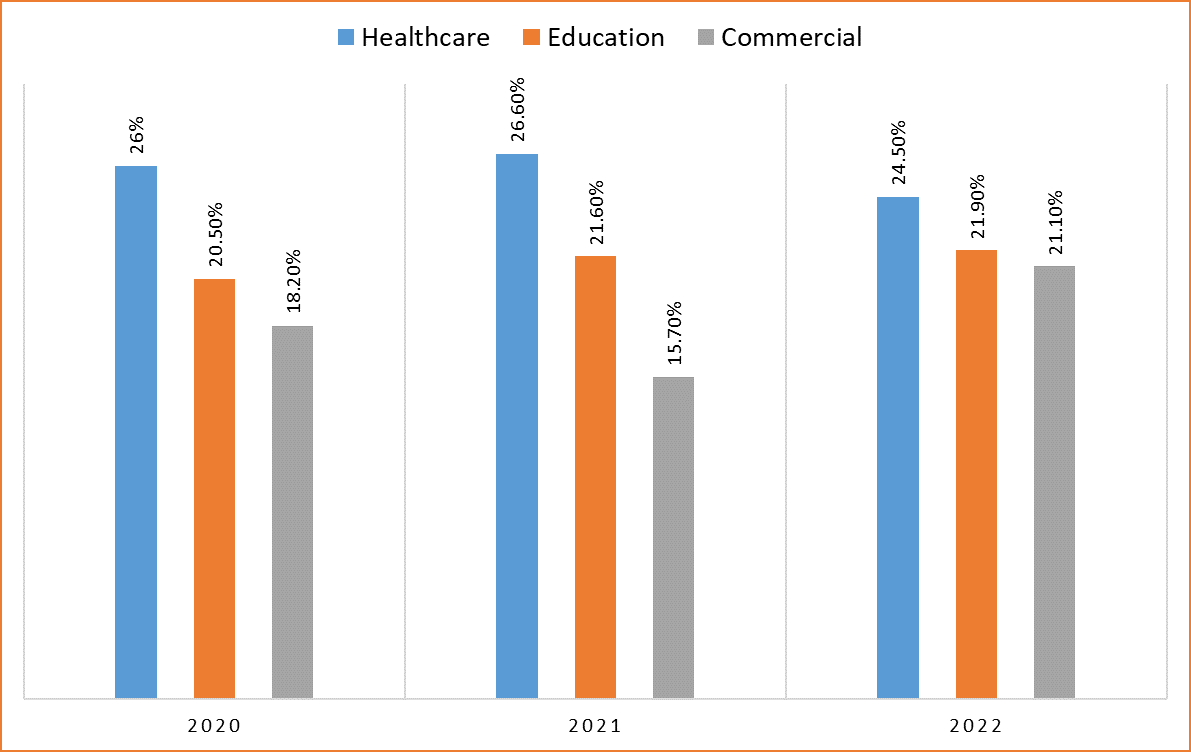

In FY2022 Huron's direct costs increased by $149.1 million, or 23.4%,[YoY]. SG&A increased by $31.3 million, or 17.6% [YoY]. The restructuring charges were $9.9 million, compared to $12.4 million in FY2021, so the company's EBIT increased by 26.9% [YoY] - the EBIT margin increased to 8.8% for 2022, compared to 5.8% for 2021. The improvement of 300 basis points for just 1 year looks compelling to me - and this is against the background of falling margins of the largest segment [Healthcare]:

Author's calculations, HURN's 10-K

{kind=link}

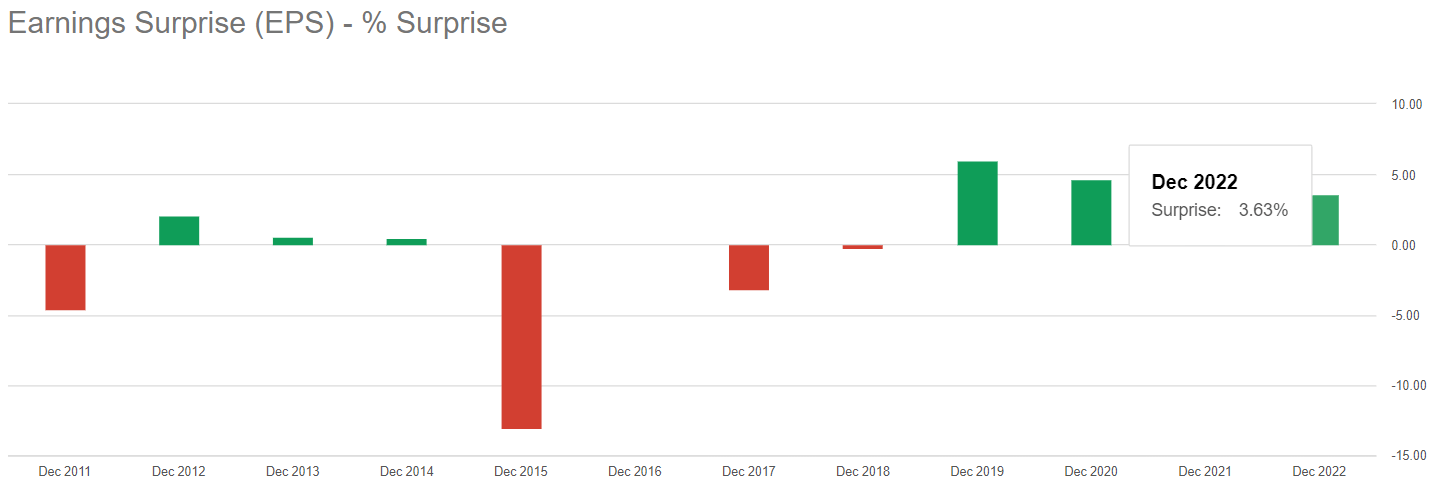

Huron's diluted EPS was $3.64, up only 26% from a year earlier. Had it not been for the nearly 2-fold increase in tax expenses in FY2023, the company would have had a much larger EPS beat than February's 3.53% :

Seeking Alpha, HURN's Earnings Surprises

{kind=link}

Now the effective tax rate equals 30.41% - I do not think that it will grow from such a high base by the end of FY2023. Most likely the opposite.

In addition, I expect Huron to show further margin improvement in FY2023 .

First, the CEO mentioned this during the earnings conference call:

In terms of margins, at the midpoint of our 2023 guidance, we expect a 65 basis point improvement over 2022 , building off the 80 basis point improvement we achieved in 2022 [meaning gross profit margin].

Source: HURN's Earnings Call , plus author's emphasis and notes

Second, these words are supported by the dynamics of the Healthcare segment. As you can see above, this segment has not yet recovered from the impact of the coronavirus, so M&A expansion as well as growing organic demand should allow the company to catch up this year. Management already has a good track record in effective cost optimization - if HURN reduces headcount a bit in this segment, which grew 18.4% last year [YoY], the chances are very high.

HURN's IR materials, author's notes

{kind=link}

So far, the company has quite a comfortable long-term debt level, and profitability, represented by return on capital employed [ROCE], is at a 5-year high:

Huron's Valuation and Market's Expectations

Huron's management anticipates a revenue range of $1.22 billion to $1.28 billion for FY2023, accompanied by an adjusted EBITDA comprising 12% to 12.5% of revenues, and adjusted diluted EPS from $3.75 to $4.25 for the year. So they expect a 10% organic revenue growth for the company as a whole , taking the midpoint of 2023 guidance.

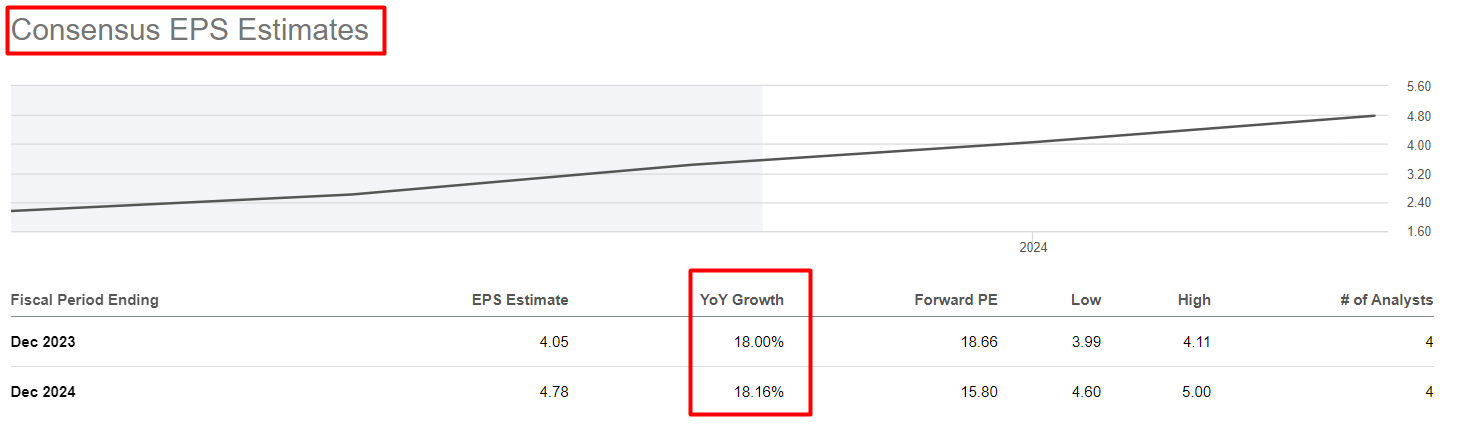

Despite HURN's management projecting a 10% YoY growth in EPS and revenue, Wall Street analysts are anticipating a higher EPS growth of 18% and a revenue growth of 10.23%, resulting in relatively small premiums for the guided numbers.

Seeking Alpha, HURN, author's notes

{kind=link}

Last year, the company spent more than $120 million on share repurchases - almost 2 times more than in FY2021 and almost 4.5 times more than in FY2020. The Board of Directors authorized an extension of the 2020 share repurchase program through the end of FY2023, and they gave another $100 million to play with; HURN had $109 million left from the previous repurchase program.

Therefore, I expect the number of outstanding shares to be significantly lower by the end of 2023 - this should have a positive impact on diluted EPS figures .

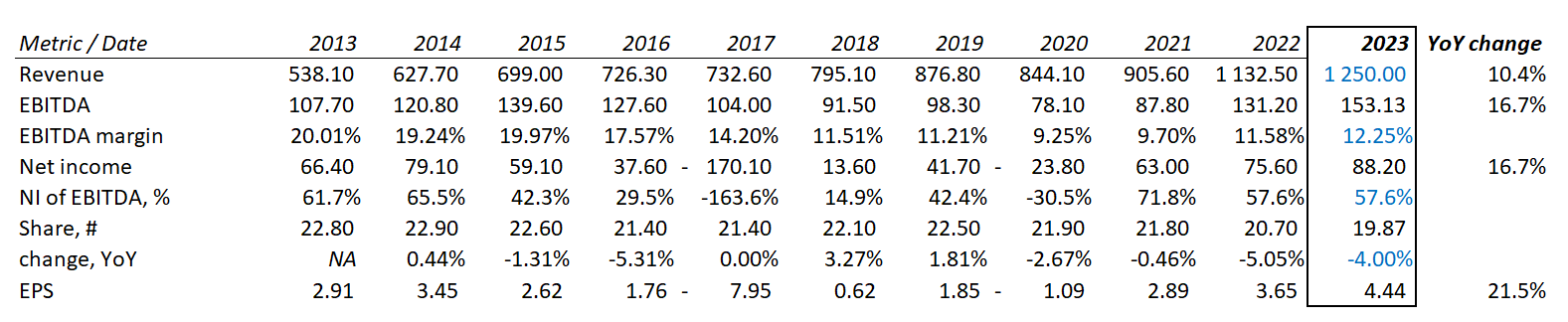

Let us do a little napkin calculation. Let's assume that management's midpoint EPS and revenue forecasts are correct. Also, the midpoint EBITDA margin forecast will be what management expects - 12.25%. Assuming net income is the same ratio to EBITDA as in FY2022, and the company buys back 4% of its shares throughout the period, implied EPS should be 21.5% higher year over year - that's 3.5% more [350 basis points] than analysts are forecasting today.

Author's calculations, Seeking Alpha data

{kind=link}

Yes, HURN stock seems a bit expensive today with an FCF yield of only 3.9% - well below historical levels:

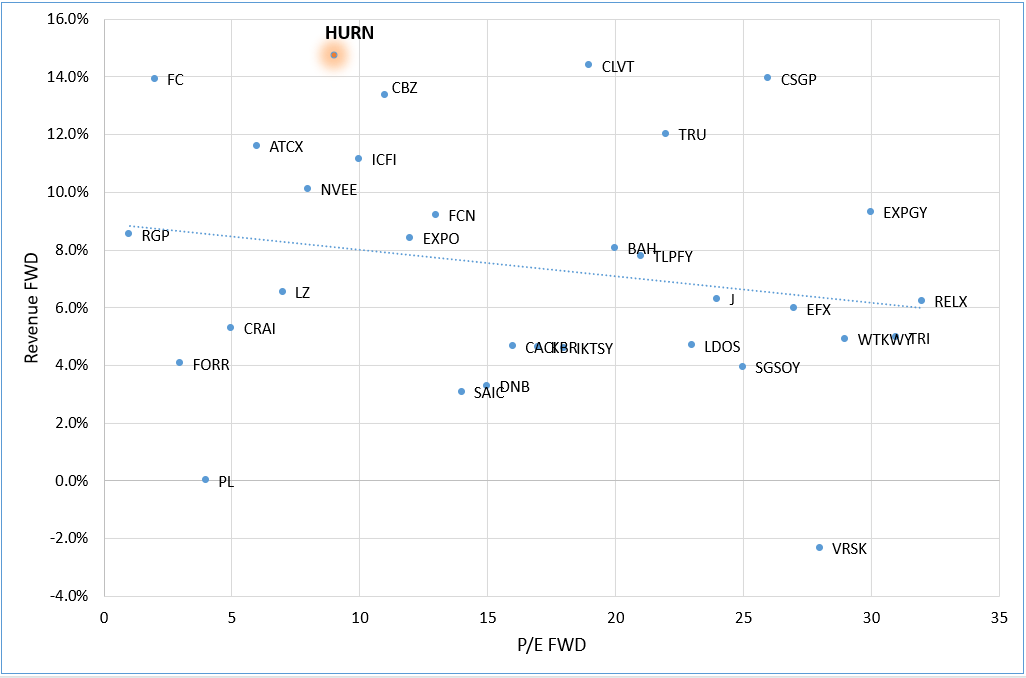

But on the other hand, as long as there is buyback support and the company's growth rates remain high, no one is stopping Huron from remaining a little overvalued. Moreover, among companies with enterprise values greater than $500 million, HURN appears to be one of the most undervalued in its industry, and that's with its current forwarding revenue growth, which we have noted may be slightly underestimated:

Author's work, Seeking Alpha data

{kind=link}

Bottom Line

Of course, I am a bit confused about what multiples the company trades at and how sensitive its business model was during the coronavirus period. There is a possibility that the current macroeconomic difficulties are putting pressure on the company's valuation and its financial metrics.

However, despite this risk, I see Huron stock as a worthy representative of the industry with an interesting and proven development strategy model ahead. For now, next year's EPS forecasts, which already include a small premium to management's words, are still below what the company is actually capable of delivering. I am waiting for a continuation of the earnings beats going forward, or an upward revision of the forecasts on the Street - both scenarios would be very positive for the price action.

I estimate HURN's upside potential to be about 27.9% by the end of 2023 - with a P/E multiple of 21.76x, the company should be worth ~$96.6 per share. That's my price target.

YCharts, author's calculations

{kind=link}

As always, your comments are welcome! Thanks for reading!

For further details see:

Huron Consulting Stock: The Best Play Of Its Industry