HURN - Huron: Less Upside But Still One Of The Best Picks In Its Industry

2023-09-21 11:08:25 ET

Summary

- Huron Consulting Group Inc., a $1.8 billion market cap firm, helps clients grow, optimize operations, and drive digital transformation for sustainable business results.

- In today's article, I review my past bullish call on Huron Consulting Group, and also analyze its latest financials as well as potential prospects.

- Huron Consulting Group compares well to other players in its industry, having some kind of reserve to the average valuation levels.

- Although I'd be more willing to buy Huron Consulting Group Inc. shares a little lower, the firm is still a "Buy" thanks to its recovery growth, expanding margins, and undervaluation.

Introduction

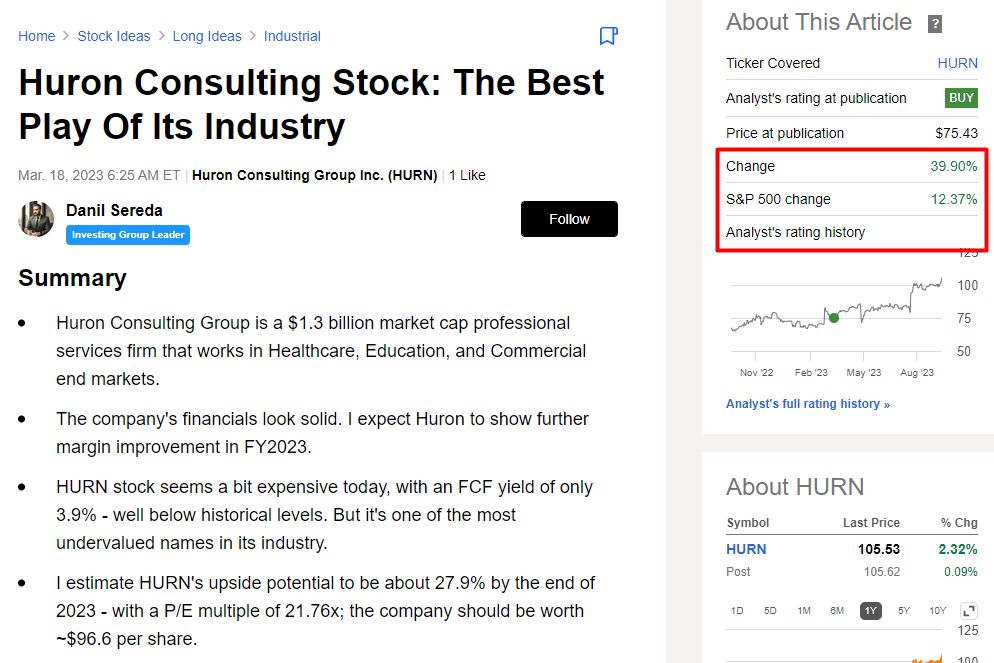

In mid-March 2023, I published a bullish article on Huron Consulting Group Inc. ( HURN ), calling it the best in its industry with a growth potential of 27.9%. A few months passed and the upside I derived came true - the stock fully achieved the target and significantly beat the broader market:

{kind=link}

I think it's time to update my thesis and try to understand how the valuation of the company has changed and what the medium-term prospects are.

The Company

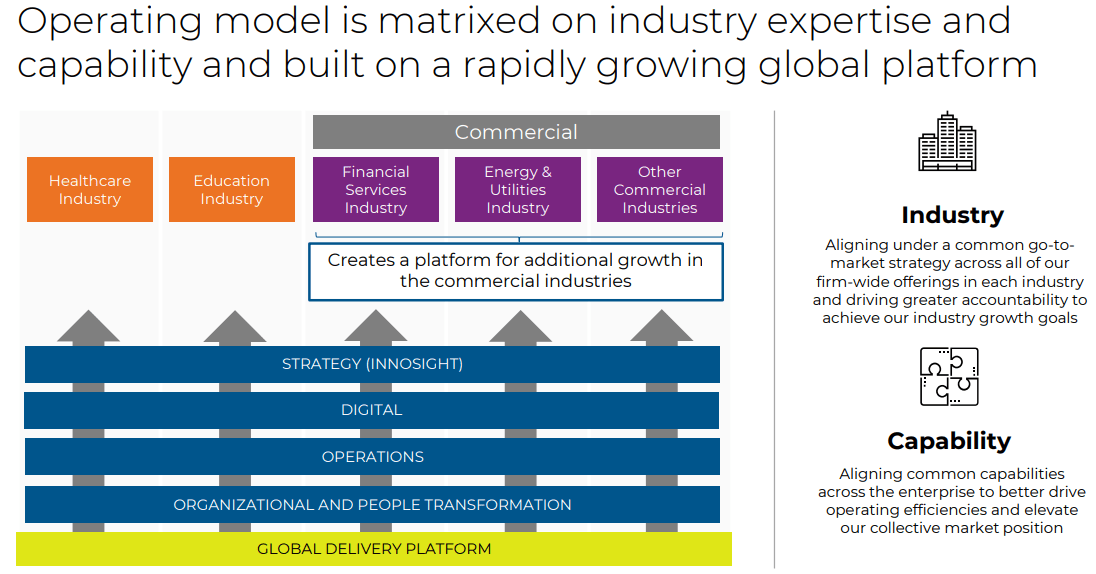

Huron Consulting Group is a $1.8 billion market cap professional services firm that works with clients to develop growth strategies, optimize operations, and accelerate digital transformation by leveraging a portfolio of technology, data, and analytics solutions to drive sustainable results for their businesses. Huron reports under 3 operating segments, tied to the end markets:

- Healthcare: 47.4% of total sales and 52% of EBIT - transforming care delivery for patient wellness and improved outcomes.

- Education: 31.5% of total sales and 32.3% of EBIT - offering consulting and tech solutions.

- Commercial: 18.6% of total sales and 15.7% of EBIT - serving large, mid-market, non-profit, and private equity clients.

{kind=link}

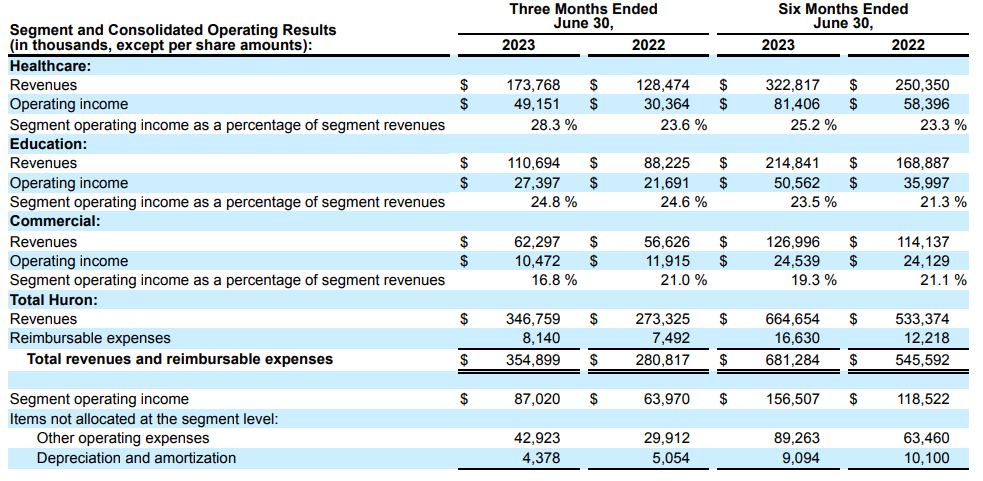

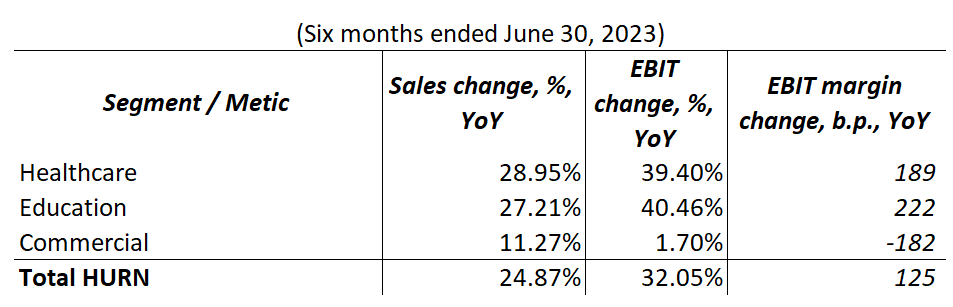

As you can see from the table in HURN's most recent 10-Q report , all of the company's operating segments are profitable, and each segment continues to grow. The commercial segment is currently a laggard because of increased spending on performance bonuses for HURN's revenue-generated professionals - that's the main reason why margins in that segment fell 182 basis points YoY in 1H FY2023. However, thanks to margin growth in the other 2 bigger segments, Huron was able to expand its overall EBIT margin by 125 basis points year-over-year, which is very solid in my opinion.

{kind=link}

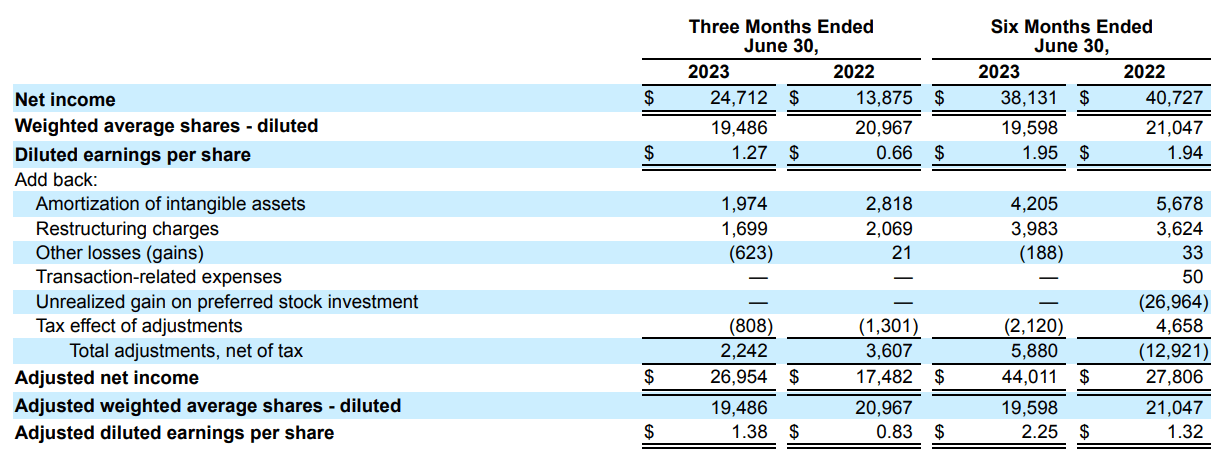

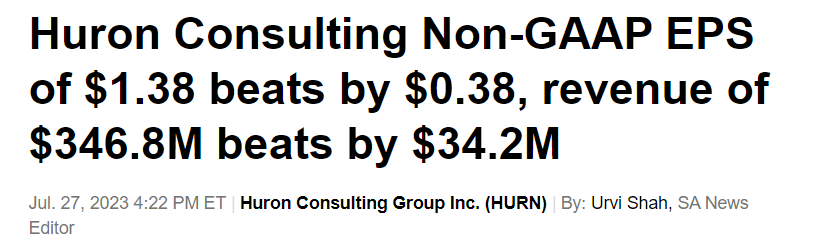

Regarding Q2 FY2023 data, the company also reported robust financial results, marked by a 26.9% YoY increase in revenues, reaching $346.8 million. Net income more than doubled, rising to $24.7 million compared to $13.9 million in Q2 FY2022. This impressive growth was underpinned by strong demand across all 3 operating segments, with the Healthcare and the Education sectors leading the way.

Adjusted EBITDA also saw a notable uptick, reaching $48.5 million, representing 14% of total revenues, compared to $33.2 million (12.2% of revenues) in Q2 2022. Adjusted net income increased to $27 million, translating to $1.38 in adjusted diluted earnings per share, marking a substantial 66% year-over-year growth.

{kind=link}

In this regard, HURN significantly outperformed Wall Street consensus estimates: EPS and revenue were 38% and ~11% higher than expected, respectively.

{kind=link}

Looking ahead to 2023, the company has raised its revenue guidance to a range of $1.3 billion to $1.34 billion, reflecting its continued strong momentum. While maintaining its adjusted EBITDA guidance at 12% to 12.5% of revenues, the company has also raised and narrowed its adjusted non-GAAP diluted EPS guidance to $4.35 to $4.65. Additionally, HURN now expects its FCF to be in the range of $100 million to $120 million for FY2023, and its effective tax rate is anticipated to fall within a range of 28% to 30%.

As I can see from the company's recent financial results, HURN's business is just picking up steam after a difficult period in 2020-2021. The current year has been challenging for margins in HURN's Commercial segment, but a look at the end industries in that segment suggests that activity should pick up in the foreseeable future.

{kind=link}

Unfortunately, the IR presentation on the company’s website has not been updated since late March 2022, but even with last year’s stated plans, we see the desire for quality growth beginning to be realized. I expect that the new talent the company has gained in the commercial sector (and not only there) in the last quarters will help it to continue to grow even in difficult times for the global economy. In fact, difficult times are the environment in which HURN's services are most needed. So Huron's multifaceted portfolio positions it as a growth leader, especially in the context of the accelerating importance of digital transformation in today's challenging business environment.

And now I want to spend a little time analyzing HURN’s valuation multiples to see how its growth potential has changed in light of its recent financial successes.

Valuation and Expectations

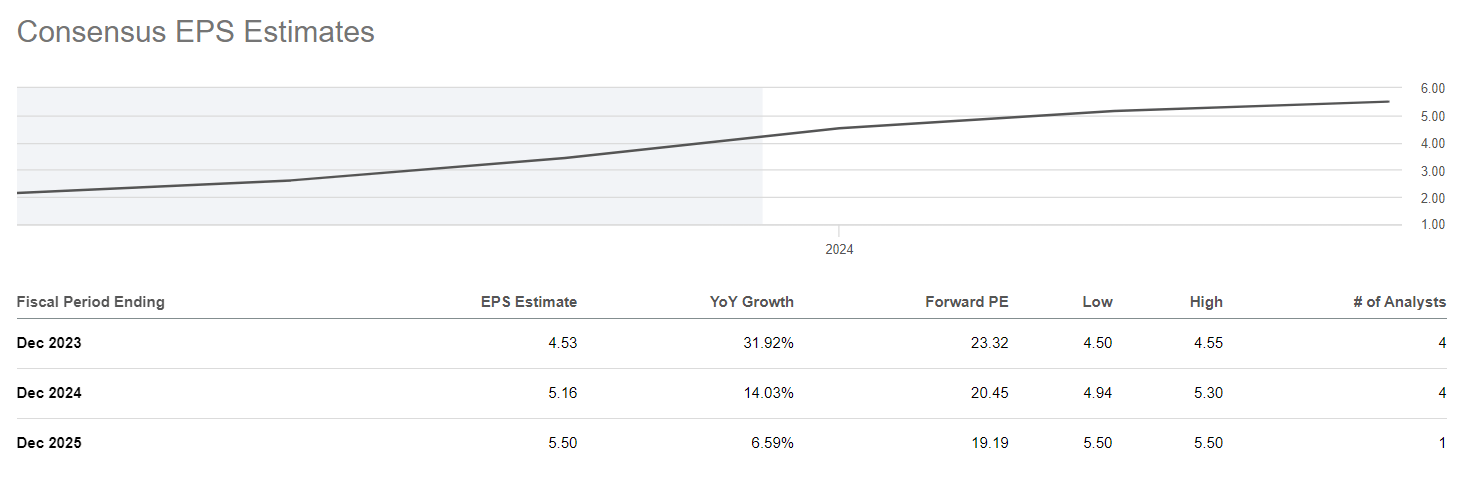

When I wrote about HURN in March 2023, Wall Street was expecting 18% EPS growth for FY2023 and FY2024. However, when HURN beat estimates by as much as we have seen for ourselves, the market revised its estimates and now expects strong EPS growth in FY2023 followed by a slowdown in FY2025:

{kind=link}

Last time we saw an implied P/E forwarding multiple [FY2024] of 15.8x, which seemed to me at the time to be an unjustifiably low metric for EPS growth of almost 20%. Today we see consensus EPS growth of 14% in FY2024 and an implied P/E of 20.45x (the multiple rose after HURN's phenomenal rally since the beginning of the year).

It should not be forgotten that if the FCF stays stable, the company is likely to continue to use the buyback program, which appears to be far from complete. During Q2 FY2023, HURN bought back only 194,000 shares ($15.4 million), so I expect the remaining repurchase program will help the stock at least maintain its current multiple for the rest of this year and early next year.

As of June 30, 2023, $49.6 million remained available for share repurchases under our share repurchase program.

Source: HURN's 10-Q

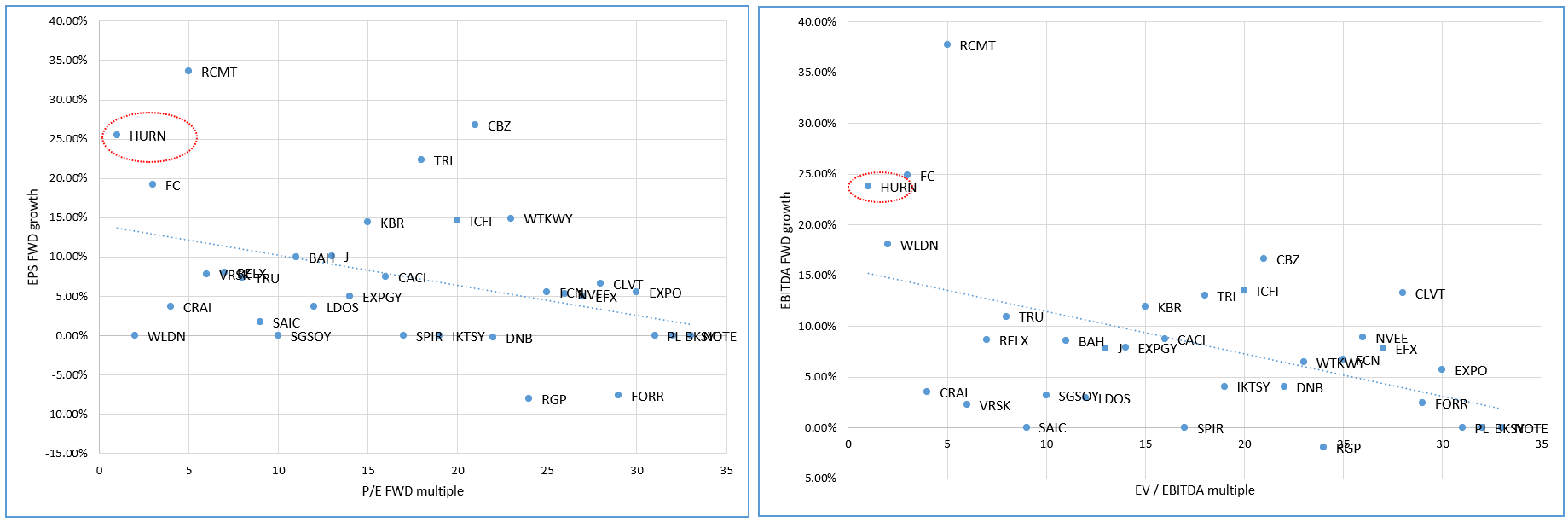

From an FCF yield perspective, today may not be the best time to buy HURN stock, but on the other hand, ROIC continues to improve relative to long-term norms, and by maintaining margins (and hopefully their continued expansion), HURN may even show some expansion in its multiples. Compared to other companies in the industry , HURN has some reserves, so to speak:

{kind=link}

Author's note: Huron is 3 times larger than Franklin Covey Co. ( FC ) and is ~ 11 times larger than RCM Technologies, Inc. ( RCMT ); so the latter 2 probably compare better because of the risk premium present .

The Bottom Line

Although HURN is now going through a rather intense recovery period after the difficult Covid period, there are some risks that I would like to mention.

First, HURN is a relatively small company with a market capitalization of less than $2 billion (still). In the event of a full-scale correction, its shares could become the leader of the decline due to its relatively low liquidity - this is the risk for all small-cap investors.

Second, I no longer see the 30% upside potential that I once did. Assuming the current multiple remains unchanged (I described why this is logical in more detail above), the growth potential for HURN in the current environment comes down to 10-15%. The margin of safety is limited, but the company may surprise everyone again with its robust growth, so who knows?

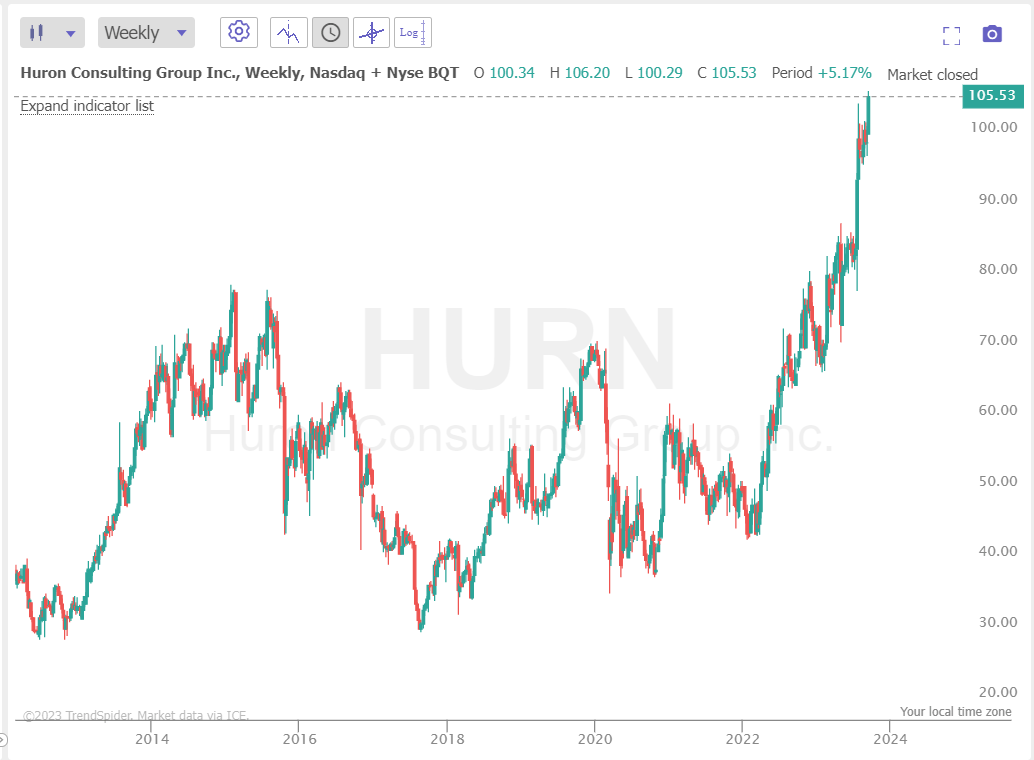

Third, from a technical perspective, the stock is already quite overheated. I expect a correction from current levels in the short term, after which HURN would be a really strong Buy.

{kind=link}

The existing growth potential compels me to issue another buy recommendation today, although I would be more willing to buy HURN a little lower. I urge everyone to do their own due diligence before making an investment decision. And don't forget to share your thoughts on Huron Consulting Group Inc. in the comments below.

Thank you for reading!

For further details see:

Huron: Less Upside, But Still One Of The Best Picks In Its Industry