SKLZ - HUYA: Waiting For The Headwinds To Blow Off Might Be The Right Choice

Summary

- HUYA is a game and e-sports live-streaming platform.

- The company is innovating and growing in the number of active users.

- 2022 showed a strong decrease in revenue and margin.

- Forecasts for Q4 and subsequent quarters appear to be under pressure.

HUYA Inc. (HUYA) is the sixth largest company in the world in terms of market capitalization in the e-sports business. The company also actively cooperates with Tencent (TCEHY) which is the market leader in e-sports. The business growth strategy is focused on investing in improving high-quality streaming content and we can recognize these efforts in the constant increase of active users on the platform.

On the other side e-sports industry seems to face some structural headwinds due to a decrease in e-sports titles and new games publications. HUYA is particularly suffering in the very thigh market context and the data of paying users is significantly worsening, bringing with it a negative trend in Revenue and above all in the EBIT Margin which fell into the negative field in 2022 (-5.9%).

Equally worrying are the prospects for Q4 and also in light of the company's downsizing of revenue estimates by 11% in 2023 and 15% for 2024, I believe it is appropriate to wait for future developments before making any decision on the matter to an investment in HUYA. My rate is 'Hold'.

General Overview

Company outlook

HUYA Inc. was born in 2014 and operates mainly in China and could be defined as a game live-streaming platform. In 2018 HUYA was listed on the NYSE. In 2020, Tencent Holdings (a public company listed on the Hong Kong stock exchange) became the controlling shareholder.

The company organizes mainly e-sport events with developer and publisher support. HUYA has managed to create a community (average monthly active users reached 86 million in Q3) of young Chinese who actively interact on the live-streaming platform. The platform diversifies its content not only on e-sports but also on other genres and also serves as a marketplace for agencies that intend to collaborate with the company. Part of the business is also located outside China via Nimo TV, a live-streaming platform born in 2018.

Revenue is generated through two main channels: the sale of products and services through the live-streaming platform and through advertising campaigns that are always present on the platform. Lately, the company is looking for further methods of monetizing its content, for example through sub-licensing of games

E-sports Market trend and HUYA active/paying users

{kind=link}

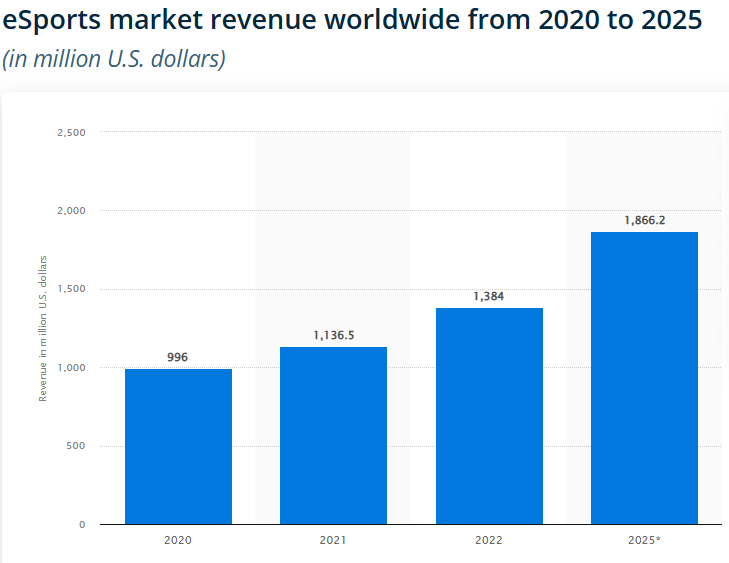

The global e-sports market has grown by 17.9% ((CAGR)) from 2020 to today to a value of $1.38 billion and is projected to grow by another 10.5% annually through 2025 ($1.86B). Although a slowdown in global growth is expected, the forecast figure is in any case double-digit and represents an investment opportunity for all the major players.

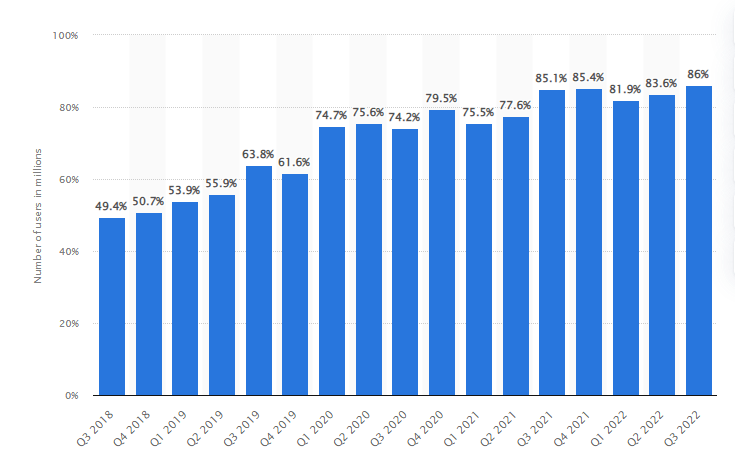

The average number of monthly active mobile users of HUYA in China from 3rd quarter of 2018 to 3rd quarter of 2022(in millions)

{kind=link}

Going into the merits of HUYA, we can see how the number of active users on the platform has been growing continuously for 4 years now and that the figure has almost doubled from 49.4 Million (Q3 -2018) to 86 Million in Q3 -22. This trend underlines how the company is implementing a policy of retention and attraction of new users thanks to increasingly better and more technologically advanced content.

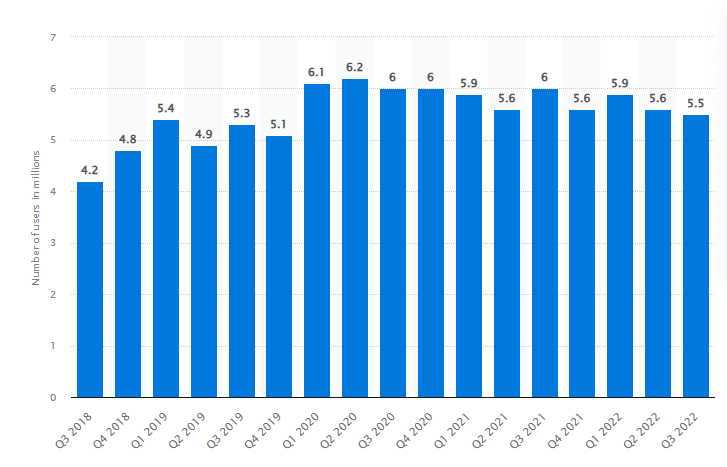

Number of paying users on the game live streaming platform HUYA in China from 3rd quarter 2018 to 3rd quarter 2022

{kind=link}

Unfortunately, the trend reverses if we analyze paying users. We can see how from Q1 of 2020 with 6.1 million paying users the trend has decreased to the value of 5.5 million in Q3 - 22. This negative trend, which has been performing for almost 3 years now, represents a source of high risk for the company's future growth.

The company management say ( last Q3 earnings call ):

The decrease was primarily due to a decline in the number of paying users and average spending per paying user of HUYA Live, as the recent micro and regulatory environment that worsely affected paying user sentiment.

It, therefore, seems that factors exogenous to the company have heavily influenced the revenue trend relating to paying users.

Revenue and Profitability

{kind=link}

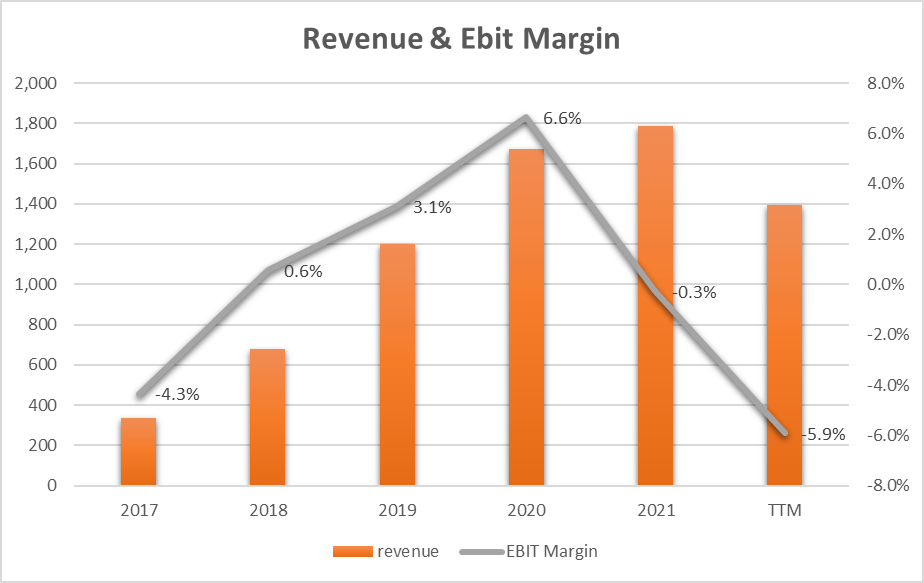

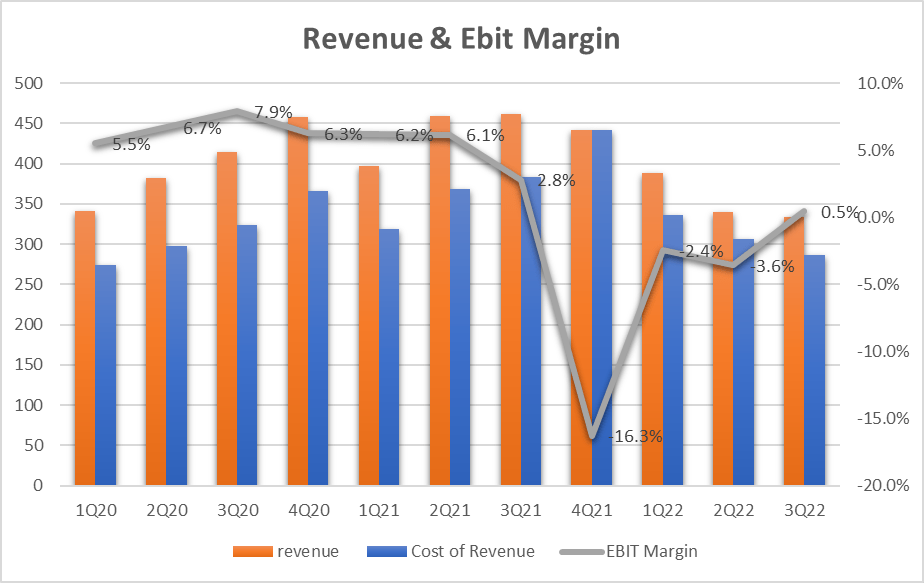

What is recorded on the data of paying users in China is also reflected in the company's global revenue trend. We can see how (orange bars) revenue grew from $335M (2017) to $1,786B (2021) but that 2022 saw a significant decrease of -21.9%, bringing revenue back to $1,395B ((TTM)). Another very important aspect is that relating to margins (EBIT Margin - gray line) which from a positive figure of 6.6% in 2020 collapsed to -5.9% ((TTM)). This trend deserves further study at the quarter level.

{kind=link}

We can see how up to Q3 - 21 the EBIT Margin (grey line) remained within positive levels while Q4 - 21 recorded a collapse of up to -16.3%. This is mainly due to the decrease in paying users on the one hand but above all to the lack of ability of the company to react promptly with the containment of operating costs (blue bars). Q4 - 21 saw the revenue cost equal to the revenue and this brought the Gross Margin to 0 causing a strong operating loss. In the following quarters of 2022, the company reacted and the blue bars became smaller than the orange ones with a consequent increase in the EBIT Margin (grey line) which in the last Q3 became positive again. This is a small sign of recovery which however contrasts with the general trend of revenue.

As we can hear from the latest earnings call:

Additionally, in the third quarter, our optimization initiative with broadcaster related costs, and bandwidth usage helped us to reduce the quarter's total costs, driven by savings from sales and marketing expenses. We are encouraged by the decline in total operating expenses in Q3, saving approximately 37% year-on-year.

The company has implemented and is proceeding with a rationalization of expenses but it remains to be understood how it can reverse the revenue trend.

One of the positive aspects can be determined by the advertising revenue which fell 'only' by 3% reaching RMB361 million from RMB374 million (quarter on quarter). Sub-licensing content also begins to produce a positive effect on revenue.

But a big unknown is represented by Q4 - 22 where the company (Q3 earnings call) expects a strong increase in costs related to the content, comparing them to Q4 - 21 where we have seen a collapse in margins:

The cost of S-12 tournaments is indeed relatively high, and the competition took place mostly in Q4, so it brought about a significant increase in our Q4 content costs. This is similar to the seasonality impact of S11 on the content cost last year. So it might also affect our overall Q4 cost and margins.

Should this scenario materialize, the EBIT Margin will reverse the trend again, going heavily into the red and placing the company in great difficulty also in the next quarters of 2023.

EPS Growth Model Valuation

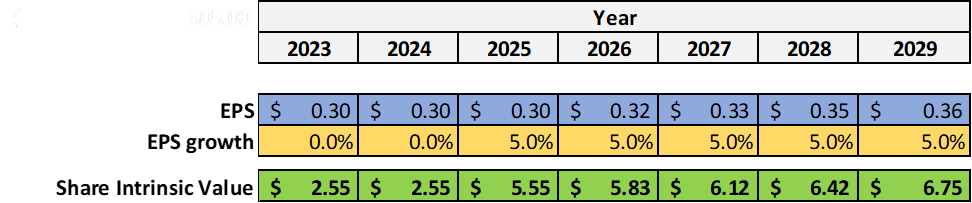

Since the company is showing headwinds in terms of Revenue and EPS growth, I decided to use a conservative estimation of the EPS growth parameter of 0% for 2023 and 2024 then I used a conservative 5% growth rate for subsequent years until 2029.

The Formula is (by popular investor Benjamin Graham):

Intrinsic value per share = EPS x (8.5 + 2 g)

Where

EPS = earnings per share (I used non-GAAP EPS)

g = EPS growth rate = 0% between 2023 - 2024 and 5% from 2025 to 2029

{kind=link}

Example of calculation for 2023:

Intrinsic value per share = EPS x (8.5 + 2 g) = 0.3x(8.5+2x0) = $2.55

The last intrinsic value of $6.75 for 2029 underlines an annualized return ((CAGR)) of 9.3% as the current share price is $3.95.

9.3% is the annualized expected return for the investment in HUYA. It's not a bad figure but it requires high risky confidence that the EPS growth rate can become 5% for the years from 2025 and above all EPS will not fall in 2023 and 2024.

Peers Comparison

To compare HUYA with similar companies in terms of market capitalization in the Interactive Home Entertainment industry I have defined the following peers:

PLAYSTUDIOS, Inc. ( MYPS )

DouYu International Holdings Limited ( DOYU )

DoubleDown Interactive Co., Ltd. ( DDI )

Skillz Inc. ( SKLZ )

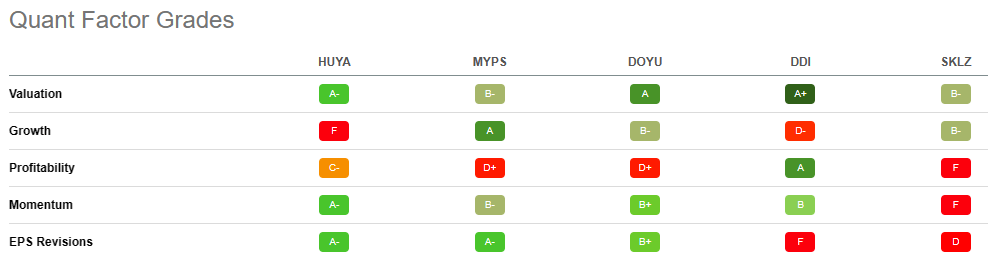

Using Seeking Alpha's Quant Ratings, we have a 'Hold' verdict related to the 'Hold' or 'Strong Sell' or 'Buy' rating of the others company. It seems that there are best opportunities to invest in the interactive home entertainment industry.

{kind=link}

{kind=link}

From the Quant Factor Grades point of view, we can see how HUYA has a good rate of 'A-' in Valuation, Momentum, and EPS Revision. In Momentum and EPS Revisions, HUYA represents also the best choice and it could be a possibility for a short-term trading opportunity.

On the other side, Growth represents the worst parameter and growth represents an Achilles' heel of the company on which management must optimize its efforts.

Revenue Growth represents the most important Risk

HUYA is investing and putting all the major efforts into the continuous optimization of the content both from a technological point of view and from a point of view of enriching the content in games or e-sports This is also thanks to the help of excellent content-creators with a great experience.

All this seems to translate into an excellent growing trend of active users on the platform but as the management says (Q3 earning call):

Recently, the monetization of our domestic live broadcast business has been affected by the overall macro environment and adjustments based on the latest industry regulations. This relative weakness of the game industry and the lack of new major game titles for a long time have also had a certain impact on the game live broadcast businesses. So Q3's live broadcast revenue declined at present due to the continuous impact of the above reasons, we will keep an eye on the trend of live streaming income changes.

HUYA's business is going through a period of general difficulty linked to the macro context. This factor, which has persisted since Q4 of 2021, could also heavily recur in Q4 - 22 and represents, in my opinion, the greatest element of risk for business growth and continuity.

Conclusion

HUYA Inc. has grown in terms of revenue by 33% annually since 2017 and this represents a respectable element. In terms of margins, 2020 was the best year with a 6.6% in EBIT Margin but the figure reversed and became -5.9% in 2022. This trend was mainly generated by a decrease in paying users and also represents an element of high risk for growth and profitability in 2023 and beyond. In terms of share price valuation, it seems that the current price could produce sufficient profitability for the next few years if there is no decrease in profits. Precisely because of this last factor, I do not deem it appropriate to open a long position but to wait for further developments before taking any position. My rate is Hold.

For further details see:

HUYA: Waiting For The Headwinds To Blow Off Might Be The Right Choice