HYGH - HYGH: Hedged High-Yield Bond ETF Growing 8.1% Yield

2023-09-26 04:34:41 ET

Summary

- HYGH invests in high yield bonds, and hedges its interest rate exposure.

- The fund has outperformed in the recent past, and yields more than its peers.

- An overview of the fund follows.

I last covered the iShares Interest Rate Hedged High Yield Bond ETF ( HYGH ), a high-yield corporate bond ETF that hedges its interest rate risk, late last year. I was bullish due to the fund's growing dividends and low interest rate risk. HYGH has since outperformed its benchmark, and most of its peers, in-line with expectations.

As inflation has mostly normalized by now, Federal Reserve rates are expected to decrease in the coming years. By my calculations, HYGH's swaps are priced in expectation of +2.0% in interest rate cuts, or Fed rates hovering around 3.5%. In my opinion, expectations are a bit dovish, although broadly rational. I rate the fund a buy, and do not believe that future rate cuts will unduly affect the fund or lead to underperformance. More dovish investors might disagree.

HYGH - Overview and Benefits

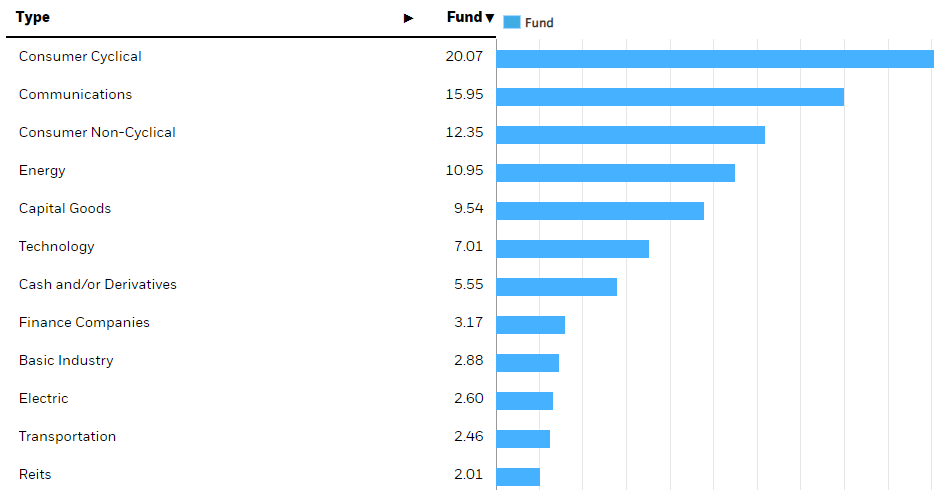

Diversified Holdings

HYGH is an interest rate hedged high yield bond ETF.

HYGH invests around 95% of its assets in high yield bonds. It does so indirectly, through an investment in the iShares iBoxx $ High Yield Corporate Bond ETF ( HYG ), the largest high yield ETF in the market. HYG's holdings are quite diversified, with investments in over 1000 bonds from all relevant industry sectors. HYG provides more than enough diversification in this market niche, as does HYGH.

{kind=link}

Both HYGH and HYG are managed by the same company: BlackRock ( BLK ). HYG's fees are waived for HYGH until 2027, so investors do not need to pay two sets of management fees right now.

HYGH

Diversification reduces risk, volatility, and the magnitude of any losses from any potential individual default or bankruptcy. HYGH's portfolio is quite bland, and does not significantly differ from the industry average in any important way.

Strong, Growing 8.1% Yield

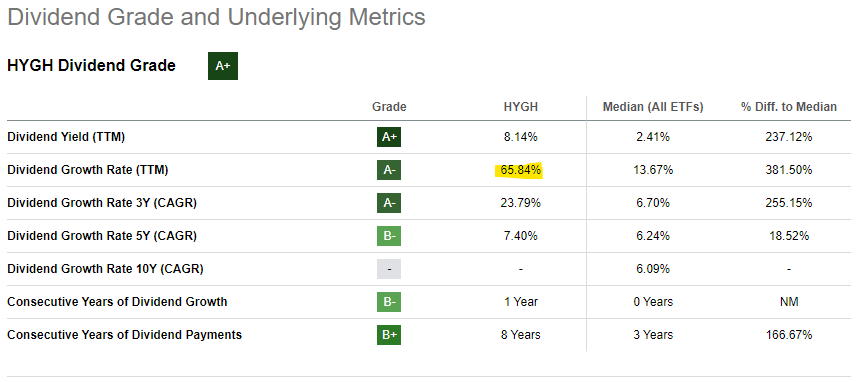

HYGH (indirectly) invests in non-investment grade securities, issued by companies with comparatively weak financials and balance sheets. Risks are higher than average, but so are coupon rates, resulting in an 8.1% dividend yield for HYGH and its shareholders. It is a strong yield on an absolute basis, and higher than that of most bonds and bond sub-asset classes. HYGH's 9.2% yield to maturity, which includes potential capital gains from bonds maturing, is quite high too.

Fund Filings - Chart by Author

HYGH's dividends have seen very strong growth in the recent past, due to Fed hikes.

{kind=link}

Importantly, HYGH's dividends are quite a bit higher than those of HYG.

Fund Filings - Chart by Author

HYGH yields more than HYG due to the latter's interest rate swaps. Let's have a closer look at these.

Interest Rate Swaps

Some context first.

Higher Fed rates only increase the coupon rates of newly-issued securities, including T-bills, with no impact to the coupons of most older, longer-term bonds. Due to this, higher Fed rates tends to lead to selling pressure for most older, lower-yielding securities, reducing their demand and prices. Recent Fed hikes have led to lower prices for most bonds and bond funds since early 2022, including for HYG.

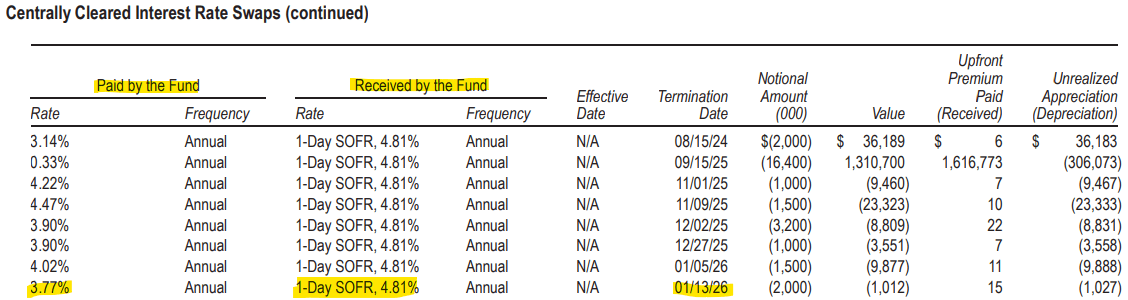

There are several ways to reduce or minimize interest rate risk / exposure. Focusing on shorter-term bonds is one way, in variable rate bonds another. Interest rate swaps are another uncommon, but effective, way to do so. To understand how these swaps work, let's have a closer look at a specific HYGH swap, in bold below.

{kind=link}

Investors in the swap above pay a fixed 3.77% to their counterparty every year. In exchange, investors receive a variable interest rate payment every year, indexed to SOFR. SOFR is an overnight financing interest rate effectively equivalent to Fed rates. So, in effect, the variable payment in the swap above is indexed to Fed rates.

Data by YCharts

Investors in the swap above receive a net payment when Fed rates are higher than 3.77%, must make a net payment when these are lower.

The swaps above can be used to hedge a portfolio's interest rate exposure in two ways.

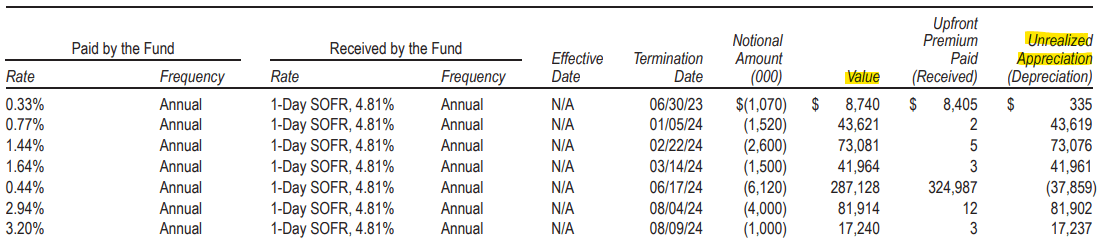

First, the swaps generate a lot in payment or income when the Fed hikes, which can be used to cover any losses from lower bond prices. HYGH's swaps have led to higher dividend growth for the fund versus HYG since the Fed started to hike, as expected.

Data by YCharts

Second, as these swaps generate a lot in income when the Fed hikes, their prices tend to increase as well, balancing any losses from lower bond prices. Looking at HYGH's swaps, it seems most of these have risen in price since the Fed started to hike, as expected.

{kind=link}

HYGH's swaps have increased in price since the Fed started to hike, significantly reducing losses for the fund itself. There were still some losses, however.

Data by YCharts

HYGH's swaps did not fully eliminate recent price losses, as credit spreads have widened these past few years, leading to excess losses.

{kind=link}

HYGH's swaps are not designed to eliminate losses from wider credit spreads, defaults, or similar, only those caused by higher rates. From what I've seen the fund has accomplished said goal, recent (small) losses notwithstanding.

HYGH - Interest Rate Expectations

HYGH's swaps have led to strong dividend growth and lower price reductions since the Fed started to hike. These same swaps should lead to dividend cuts and lower price gains when the Fed starts to cut. Depending on the magnitude of any future Fed cuts, HYGH's dividends might see very significant cuts, and the fund might end up underperforming.

Right now, the market seems to be expecting around 2.5% - 3.0% in Fed rate cuts, as per surveys and market prices. HYGH's swaps themselves are priced in expectations of rate cuts of similar magnitude. To understand why, let's have a closer look at a specific swap.

Investors in the swap above pay a fixed 3.77% coupon each year, and receive a variable payment indexed to SOFR / Fed rates in turn. In total, from inception to maturity, these payments should roughly equal each other. If fixed payments are consistently higher, the fund would not enter into these swaps, because they would lose money. If variable payments are consistently higher, the fund's counterparty would not enter into these swaps, because they would lose money. Profits or losses do occur, especially when the Fed hikes or cuts aggressively, but expectations are for these payments to be roughly equal.

Right now, the variable rate payment is higher, as Fed rates are at 5.25% - 5.50%, compared to 3.77% for the fixed rate payment. As the Fed cuts rates, variable rate payments should decrease. By my calculations, rates need to decrease to around 3.0% for this to occur, taking into consideration the fact that the swap matures in 2016. A quick table of the calculation:

HYGH - Chart by Author

Although the above calculation is a massive simplification, I think it is reasonably accurate, and broadly in-line with surveys and other market-based measures of expected interest rate cuts. In my opinion, expectations are a bit too dovish , as inflation remains above-target, and the Fed itself has indicated a somewhat slower pace of cuts . In any case, do remember that these swaps are pricing in several rate cuts already, and so should perform reasonably well if these occur.

Conclusion

HYGH is an interest rate hedged high yield bond ETF. HYGH's growing 8.1% dividend yield and low rate risk make the fund a buy.

For further details see:

HYGH: Hedged High-Yield Bond ETF, Growing 8.1% Yield