HYGH - HYGH: Not Properly Compensated For Rising Credit Defaults

2023-09-21 02:26:55 ET

Summary

- iShares Interest Rate Hedged High Yield Bond ETF allows investors to bet on the direction of credit spreads.

- Contrary to my expectations, HYGH has performed well since the regional bank crisis as policymakers prevented credit contagion through liquidity injections and deposit guarantees.

- Another technical reason for tighter credit spreads is that the all-in yield for high-yield bonds is now attractive, so investors have been buying.

- I believe credit spreads are now overly tight and do not properly compensate investors for rising credit risk.

Six months ago, shortly after the regional bank crisis, I wrote a cautious update on the iShares Interest Rate Hedged High Yield Bond ETF ( HYGH ), suggesting caution may be warranted as credit conditions were tightening due to contagion risks from regional bank failures.

However, it appears my fears were overblown, as credit markets promptly calmed down, spreads tightened, and equity markets rallied. What did I get wrong with respect to credit and how do credit spreads look now?

Brief Fund Overview

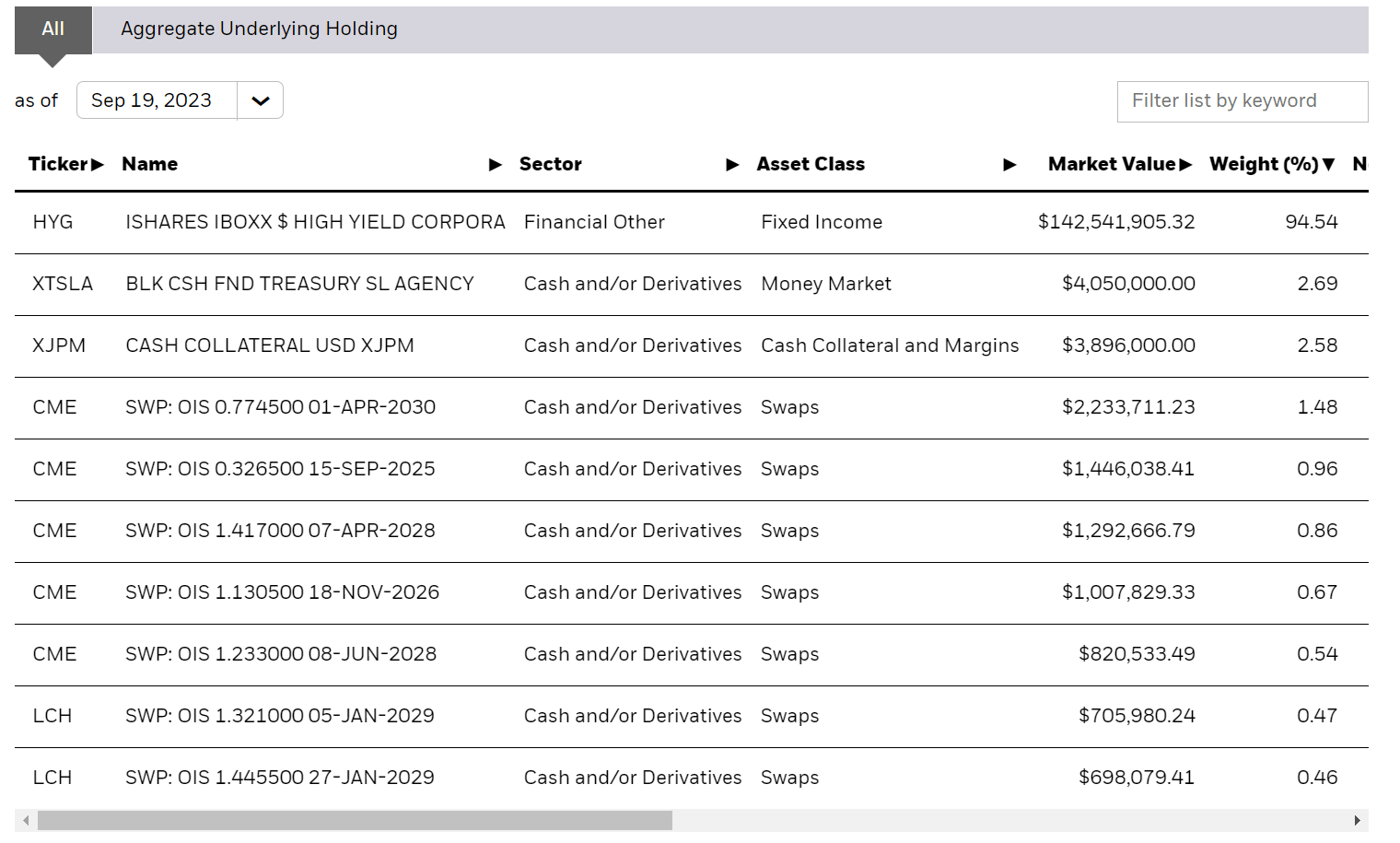

First, for those not familiar with the iShares Interest Rate Hedged High Yield Bond ETF, the HYGH ETF gives investors a quick and convenient way to express their views on the creditworthiness of high yield bonds, without the associated interest rate risk of owning the bonds themselves. Instead, the HYGH achieves this by owning units of the iShares iBoxx $ High Yield Corporate Bond ETF ( HYG ) and a portfolio of interest rate swaps to hedge away its duration exposure (Figure 1).

Figure 1 - HYGH portfolio holdings (ishares.com)

{kind=link}

Investors who want to know more about the fund mechanics of the HYGH ETF should consult my initiation article for more details.

What Happened To The Expected Credit Contagion?

To be a successful investor, one must always be humble. Even the best investors like Stanley Druckenmiller are only correct 60% of the time. It is ok to be wrong, but what is important is to review trading decisions objectively to see whether we made any analytical errors and correct them for the future.

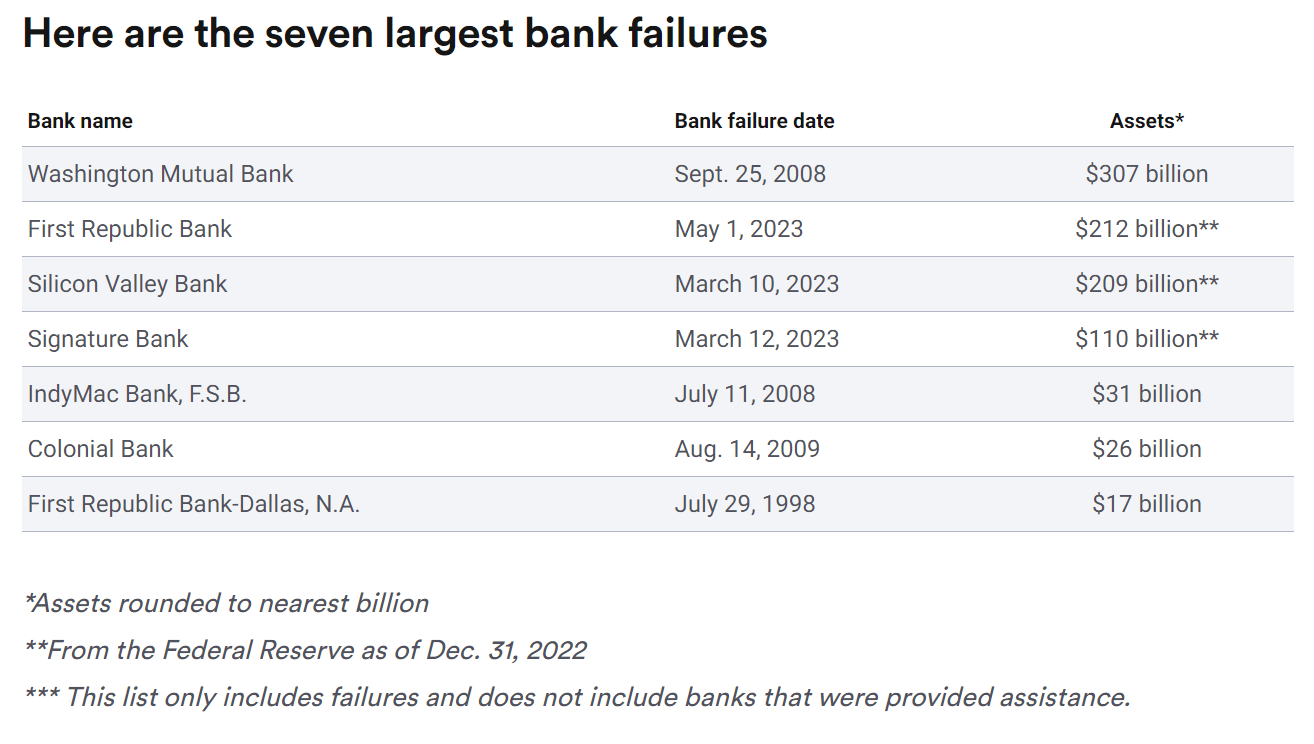

Returning to the credit landscape in late-March, Silicon Valley Bank and Signature Bank had just failed and other banks were on the verge of collapse. SVB and Signature were the 2nd and 3rd largest bank failures in U.S. history, until they were eclipsed a few months later by First Republic Bank (Figure 2).

Figure 2 - Some of the largest bank failures in history occurred in 2023 (bankrate.com)

{kind=link}

So I believe taking a cautious view in light of these bank failures was the prudent course of action back in March.

Policymakers Prevented Contagion

However, with respect to the expected credit contagion from regional bank failures, that ultimately did not play out as the Federal Reserve and other policymakers like the FDIC flooded the system with liquidity and rescued the banking sector.

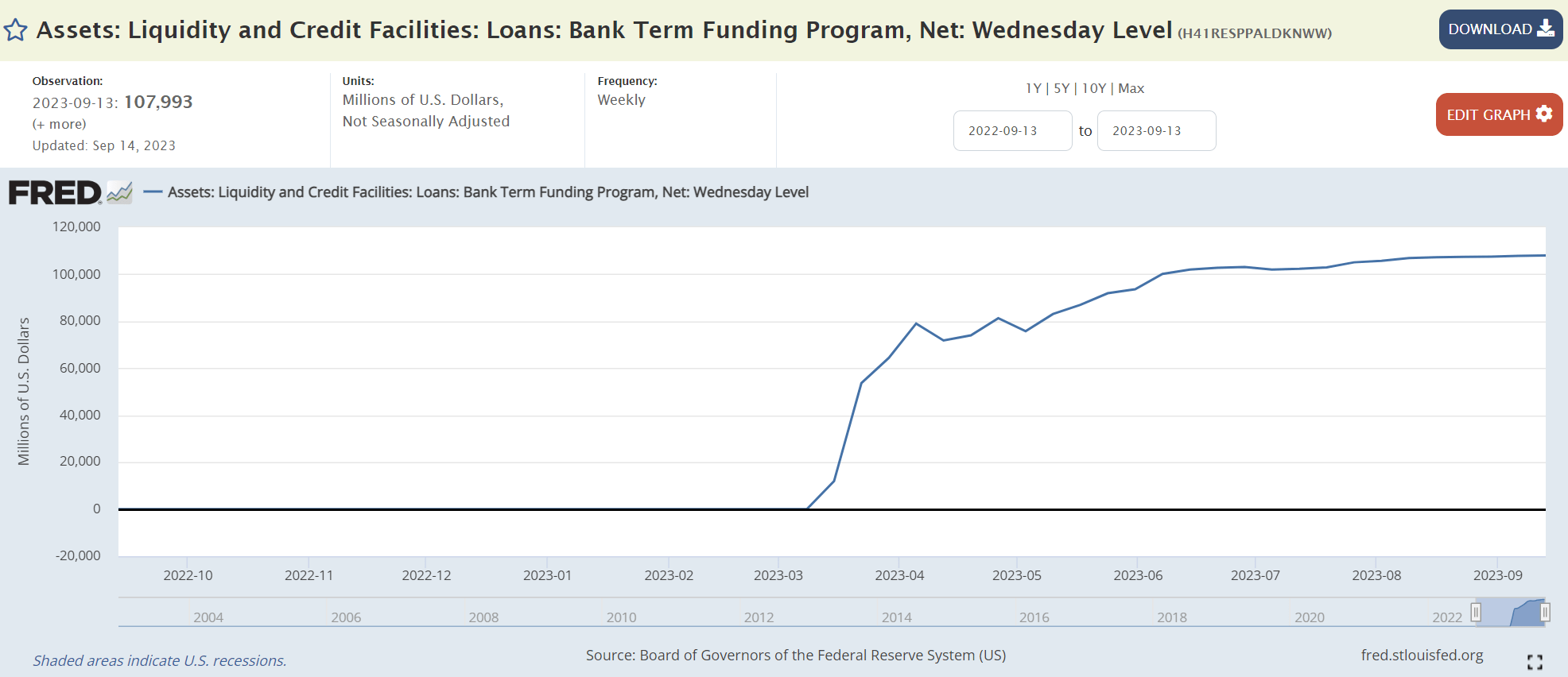

For example, the Federal Reserve set up the Bank Term Funding Program ("BTFP") which allowed banks to borrow funds against their underwater investment securities at par , effectively buying the banks time to work out their balance sheet problems (Figure 3). As of September 13, 2023, commercial banks have utilized $108 billion of this facility.

Figure 3 - Banks used $108 billion of BTFP facility (St. Louis Fed)

{kind=link}

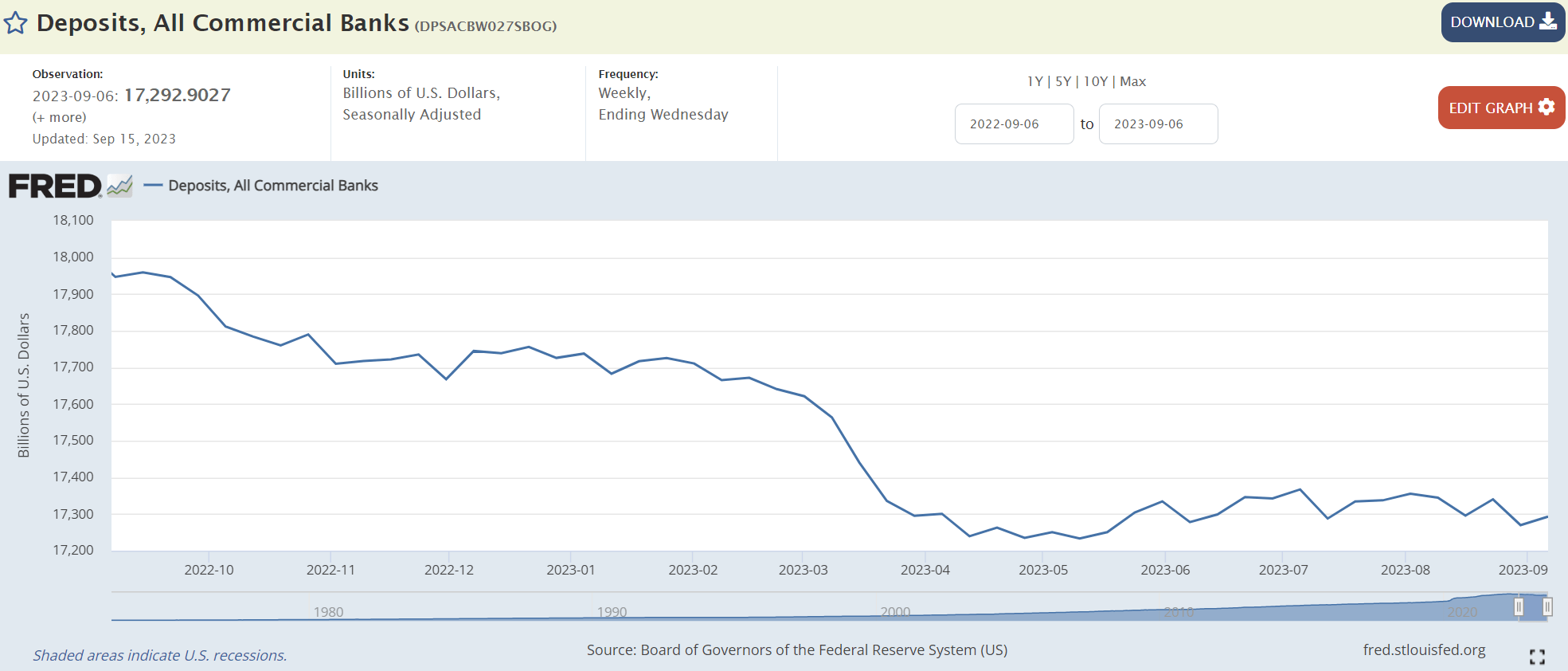

Similarly, the FDIC guaranteed the deposits of the failed banks, reducing panic withdrawals from bank deposits. This action stabilized bank deposits, with total commercial bank deposits holding relatively steady at $17.2 trillion since April, and reduced the urgency for banks to offload underwater securities portfolios (Figure 4).

Figure 4 - FDIC backstop stabilized bank deposits (St. Louis Fed)

{kind=link}

Economy Far Stronger Than Expected

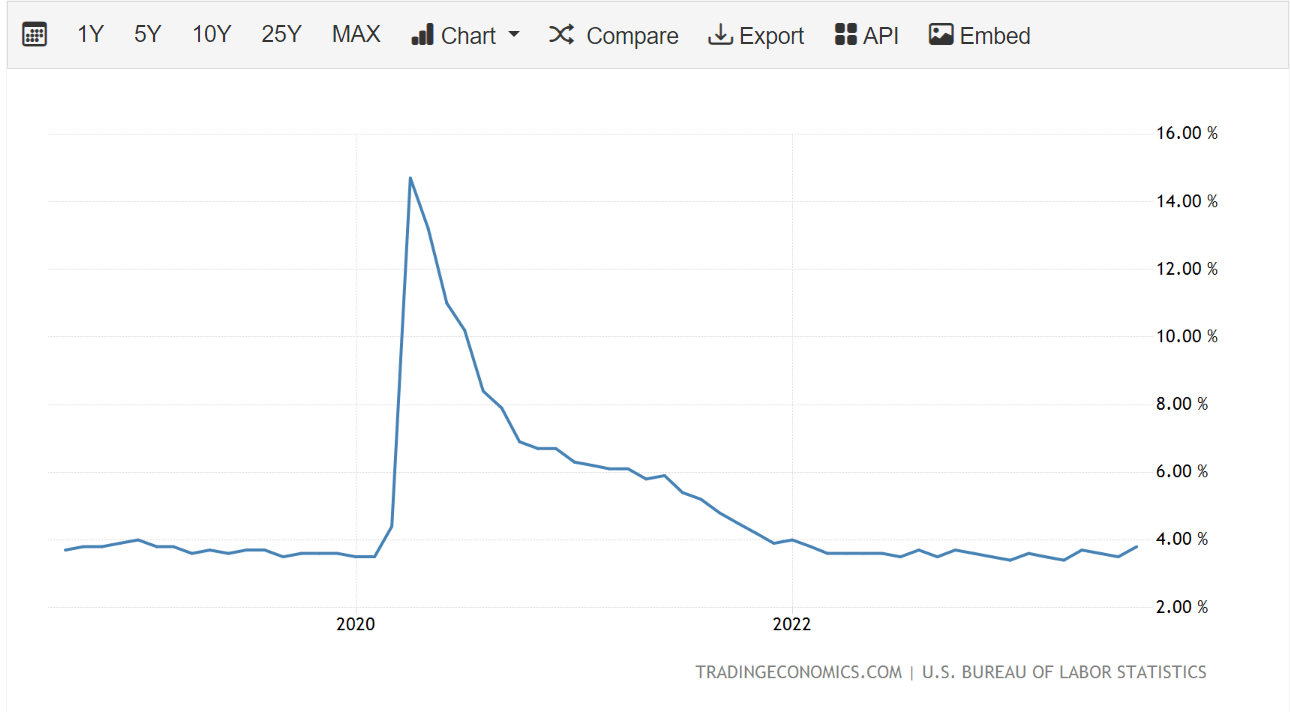

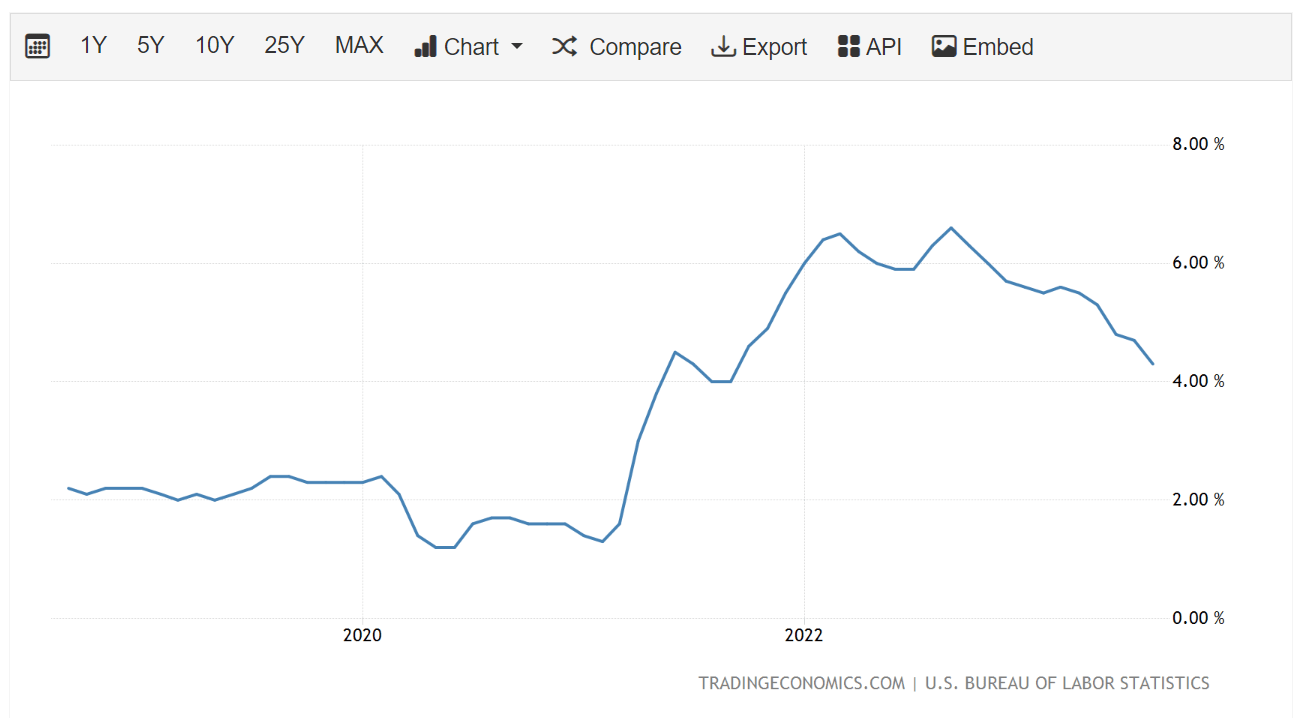

On the other hand, the American economy proved far more resilient than expected, with unemployment rate still near multi-year lows (Figure 5) and inflation moderating (Figure 6).

Figure 5 - Employment remains strong despite bank failures (tradingeconomics.com) Figure 6 - Inflation moderating (tradingeconomics.com)

{kind=link}

{kind=link}

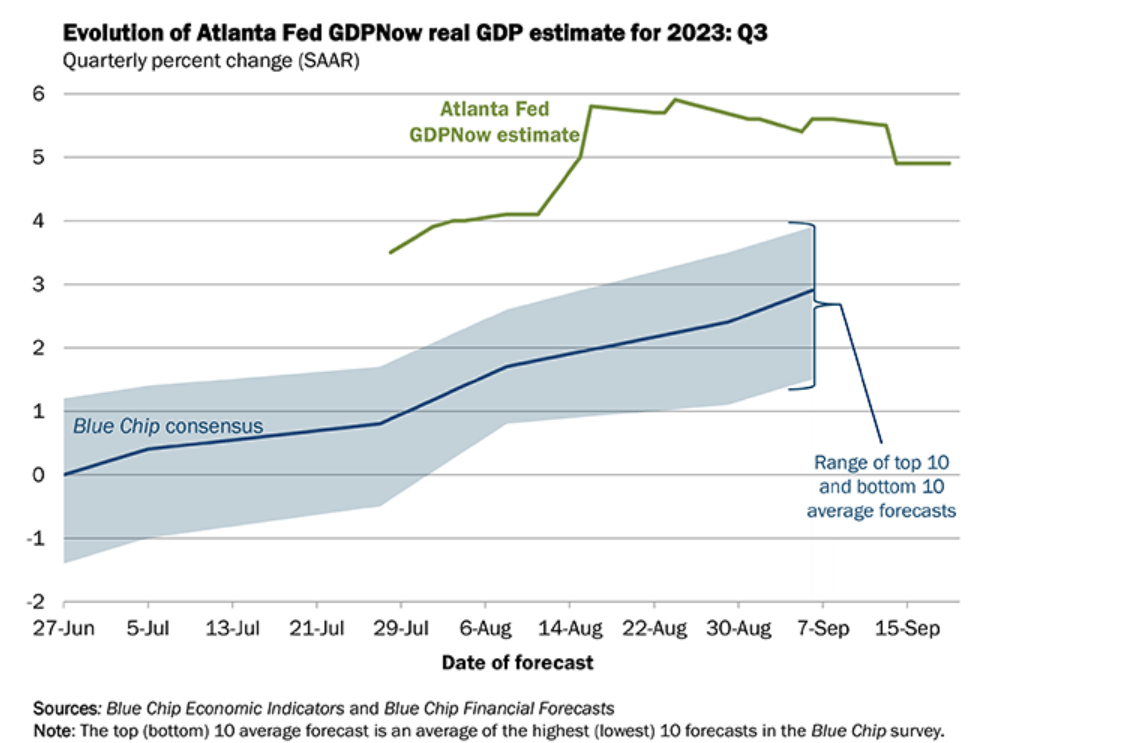

In fact, recent forecasts from the Atlanta Fed's GDPNow tool suggest the economy may be reaccelerating in recent months, as it is forecasting a Q3 GDP growth rate of 4.9% YoY, far above consensus and Q2's 2.1% growth (Figure 7).

Figure 7 - Atlanta Fed's GDPNow forecast a blistering 4.9% GDP growth rate (Atlanta Fed)

{kind=link}

The Federal Reserve appears to have engineered the fabled 'soft landing' scenario where they are able to tame inflation with minimal damage to the real economy. Mission Accomplished ?

But Defaults Are Rising

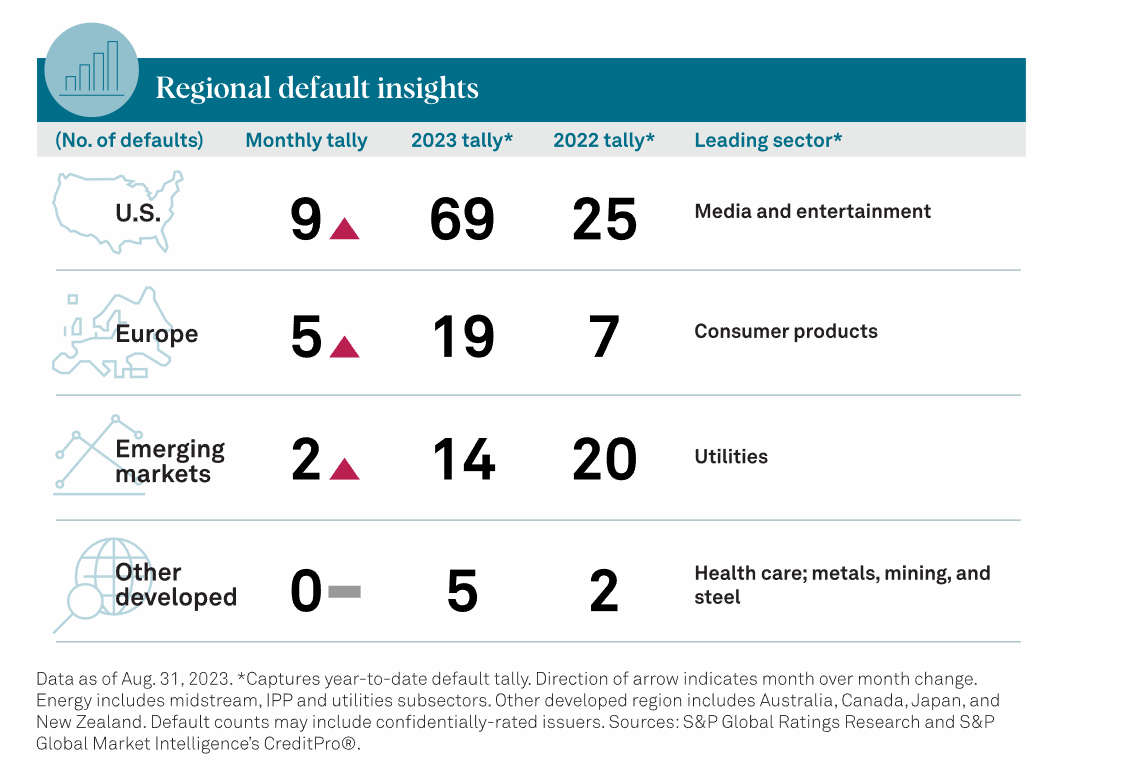

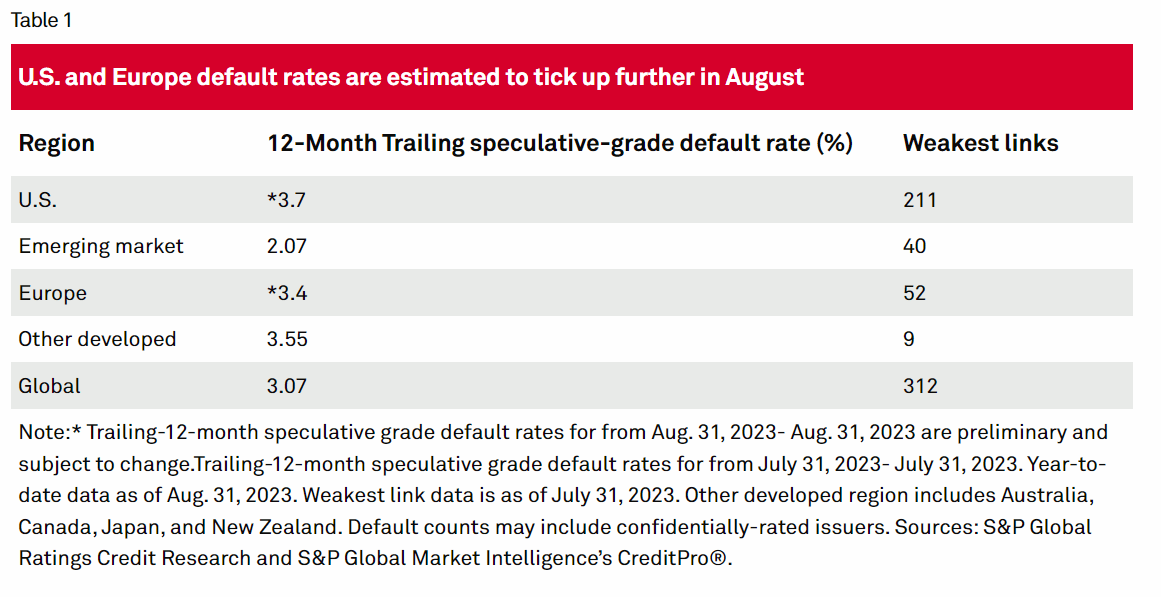

While the data has been good so far, investors are cautioned against celebrating prematurely as there are still dark clouds on the horizon. For example, according to S&P Global , a credit rating agency, the number of corporate credit defaults rose to 107 in the year to August, with 16 defaults in August alone, the highest August tally since 2009 (Figure 8).

Figure 8 - Credit defaults rising (S&P Global)

{kind=link}

Overall, S&P Global expects the U.S. corporate default rate to continue rising, hitting 4.5% in 2023 from a trailing 12 month default rate of 3.7% (Figure 9).

Figure 9 - S&P Global expect high yield default rate to hit 4.5% this year (S&P Global)

{kind=link}

Why Are Credit Spreads So Tight?

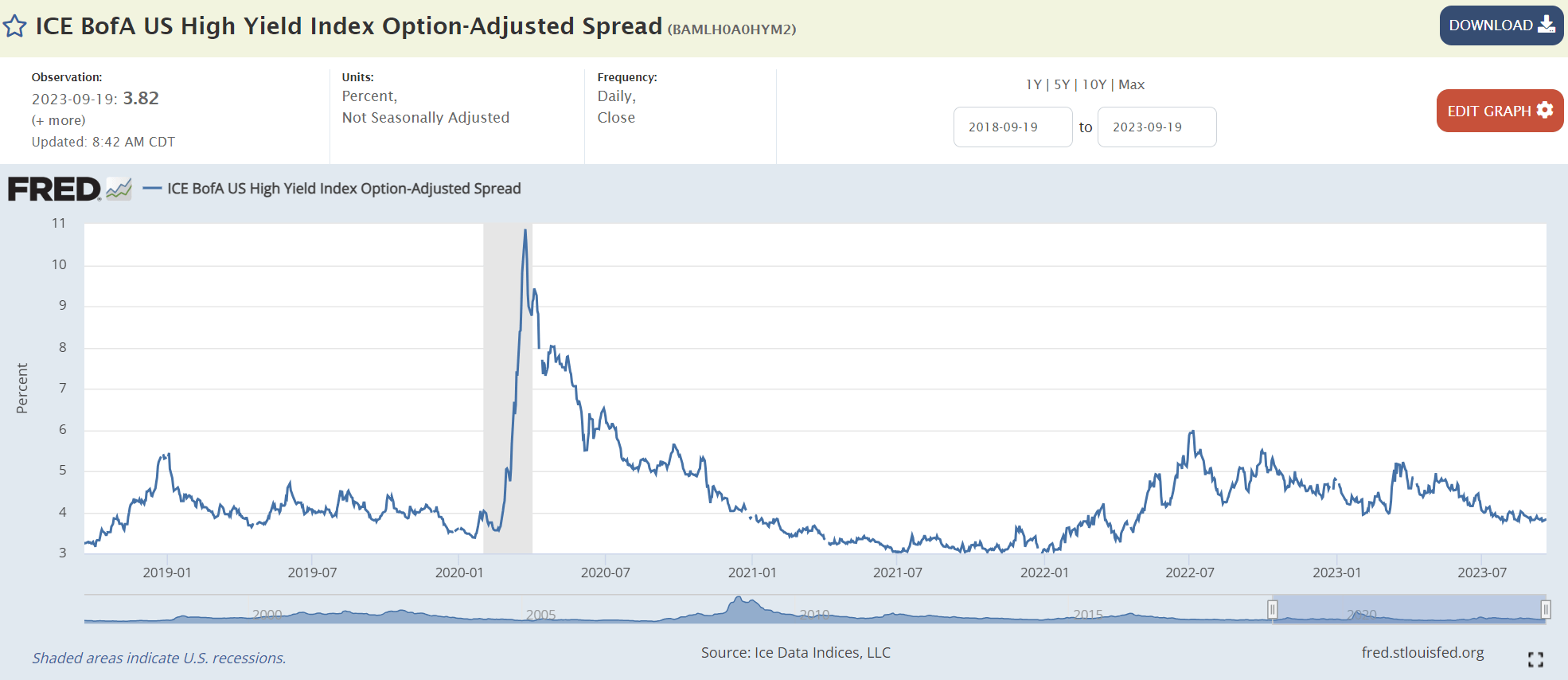

However, despite rising corporate defaults, credit markets remain extremely calm, with high yield credit spreads, on which the HYGH ETF is based, trading at only 3.8%, the tightest since early 2022 and not reflective of the outlook for rising defaults (Figure 10).

Figure 10 - Credit spreads remain extremely benign (St. Louis Fed)

{kind=link}

Are credit markets really that sanguine, or is there something else going on?

High Interest Rates Mask Low Credit Spreads

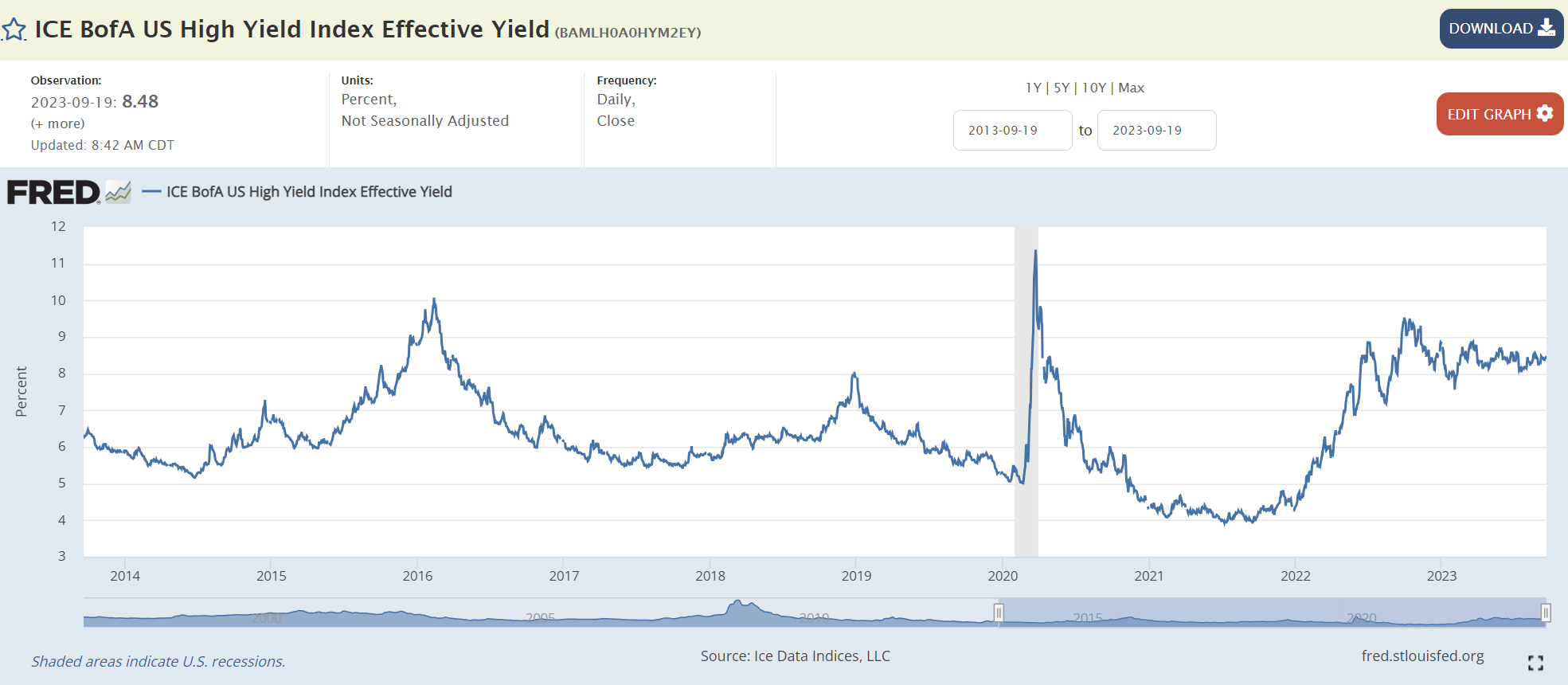

I believe what is going on is that with interest rates having risen substantially in the past year, the all-in yield for high yield bonds have become attractive to investors. For example, the effective yield of high yield bonds are now 8.5% on average, the highest in the past decade save for the 2016 global growth scare and the 2020 COVID-pandemic (Figure 11).

Figure 11 - High yield effective yields are 8.5% (St. Louis Fed)

{kind=link}

For many investors, getting equity-like returns (8%+) from fixed income investments is proving to be a very attractive proposition because they know that even in a bad recession, an 8%+ yield provides a lot of downside cushion for credit losses. For example, according to data from Insight Investment , high yield default rates only spiked to 5.3% in 2009 and 4.0% in 2020 (Figure 12).

Figure 12 - Historical high yield default rates (Insight Investment)

So even in a 2008/2009 Great Financial Crisis scenario with 5%+ high yield defaults, buying high yield bonds at 8%+ yields should still generate positive returns (8% coupon less 5% credit loss, even without recoveries, net to 3% return).

That is precisely the reason I have been recommending investors consider buying fixed-term high yield bond funds, like the Invesco BulletShares 2026 High Yield Corporate Bond ETF ( BSJQ ), because if we look at the math, as long as investors are able to hold the fund until maturity, they should generate positive returns even if credit defaults rise as S&P expects.

Caution Remains Warranted For HYGH

While the high yield bond market may appeal to investors because of the attractive all-in yield, the same cannot be said for the HYGH ETF. Since the HYGH ETF hedges away interest rate risk, investors in the HYGH ETF are essentially betting on credit spreads continuing to tighten.

Referring to Figure 10 above, high yield credit spreads are essentially trading at 2019 levels, when default rates were 1.6% (Figure 12 above). However, trailing 12 month realized and expected default rates are 3.7% and 4.5% respectively according to S&P Global, so investors are not being properly compensated for the credit risk they are assuming.

Conclusion

Contrary to my expectations, the HYGH ETF has performed well in the past few months, as contagion from the regional bank crisis was contained by officials and investors stepped in to buy high yield bonds yielding 8%+, compressing credit spreads.

However, with corporate defaults rising and expected to worsen in the coming months, I do not believe investors are currently being properly compensated for credit risk. I remain neutral on the HYGH ETF for now.

For further details see:

HYGH: Not Properly Compensated For Rising Credit Defaults