LQD - HYI: No Leverage No Problems

2023-09-24 10:56:08 ET

Summary

- Leveraged closed-end funds are facing headwinds of rising costs associated with leverage in a higher interest rate environment.

- The Western Asset High Yield Defined Opportunity Fund offers exposure to a high-yield bond portfolio with an attractive discount while being a term fund.

- HYI's income has been growing with rising yields, and the fund recently increased its distribution, making it a potentially attractive investment.

Written by Nick Ackerman, co-produced by Stanford Chemist.

The majority of closed-end funds utilize leverage through borrowings to potentially enhance returns. With a higher interest rate environment, the costs associated with those borrowings are rising. Some funds are better protected by utilizing various hedges, so that has put some funds in a better position. Additionally, while leverage can enhance returns, the opposite is also true. This makes the funds riskier as downside pressure can also be increased than what would otherwise be experienced.

However, it's important to note that not all CEFs utilize leverage, and so some funds aren't dealing with those current headwinds. The Western Asset High Yield Defined Opportunity Fund ( HYI ) is one such fund that offers exposure to a high-yield bond portfolio with exposure around the globe.

While some high-yield funds are facing pressure on their distribution coverage, HYI's income has been growing with rising yields, and that's led to the fund even making a small increase in the distribution recently. The fund is also sporting an attractive discount, offering a fairly tempting time to consider this fund. Given the fund is anticipated to liquidate in around two years, this could be a catalyst worth watching going forward.

The Basics

- 1-Year Z-score: -1.52

- Discount: -7.15%

- Distribution Yield: 9.98%

- Expense Ratio: 0.95%

- Leverage: N/A

- Managed Assets: $278.8 million

- Structure: Term (anticipated liquidation date of September 30, 2025)

HYI has an investment objective of "high income, with capital appreciation as a secondary objective." They "emphasize team management and extensive credit research expertise to identify attractively priced securities."

They are free to invest across various types of fixed-income securities. However, they primarily focus on high-yield corporate debt, "...under normal market conditions, at least 80% of its net assets in a portfolio of high-yield corporate fixed income securities..."

On the fund's expense ratio, this is one of the first places we'd see the ugly effects of a higher interest rate environment. However, for HYI, we don't have to deal with ballooning costs of leverage, so the fund's expense ratio has stayed fairly consistent.

Performance - Attractive Discount

Since the last time we covered HYI , just over a year ago, the fund has provided total returns that were basically flat. However, one of the factors at play here was the discount widening since our last update.

HYI Performance Since Prior Update (Seeking Alpha)

Besides being non-leveraged in the current uncertain environment, one of the main features that make HYI particularly attractive is the fund's limited term structure with the deep discount. This is a way for investors to realize the discount instead of letting a fund trade perpetually at a discount. With just around two years left until the fund's termination, that's one of the driving catalysts for producing alpha relative to other global high-yield bond funds. That could see the entire discount realized from this point going forward.

Additionally, the overall discount of the fund is also relatively attractive. There had been a period of time when the fund traded at wider discounts, but it is currently trading just below its inception average.

YCharts

Of course, like any investment, there are risks to be considered. With the term structure, there comes a bit more that is unique to the structure.

First, this is still a high-yield-focused fund with a global portfolio. If defaults tick up, that could create a situation where heavier than usual losses are incurred. Just because the discount can be realized doesn't mean it will produce positive returns. It only means that relatively speaking, alpha would be created compared to another fund of the exact same positioning but with a perpetual structure during this time.

Second, there is no guarantee that the fund will liquidate when it should. The Board of Directors can determine that liquidation "would not be in the best interests of stockholders" and propose an amendment to shareholders to extend the term. However, in this situation, they stipulate that it would need to gain the approval of the majority of shareholders to approve. So, at the very least, investors would have a say in how it plays out.

As an example, the Western Asset Mortgage Opportunity Fund ( DMO ) was one such fund that had previously had a termination date . However, the Board put up the amendment to eliminate the term date entirely, and shareholders approved it at the end of 2019. The Board then amended the bylaws and switched to a perpetual fund in early 2020. At the time, DMO had been trading at a significant premium. It was literally in the best interest to get rid of the term structure or face a guaranteed loss, as a liquidation at NAV would have done just that.

To me, the DMO situation seems a bit strange in that investors didn't just exit when it was at such a premium. I wouldn't have been voting for any amendment because I wouldn't have even been invested in the fund at such a pricey level anyway. That's one of the main reasons I'd be less concerned about that situation with HYI. There is no reason for investors to vote to amend to a perpetual fund if the fund continues at such a large discount.

Since HYI's inception, the discount/premium has been on quite the wild ride. We've seen a discount as low as 15%+ before, but the fund has also traded at a premium.

YCharts

In fact, in 2021, there was a spike in the premium that seemed out of nowhere. That spike has probably made this latest discount widening feel even worse for investors who potentially held on during that period.

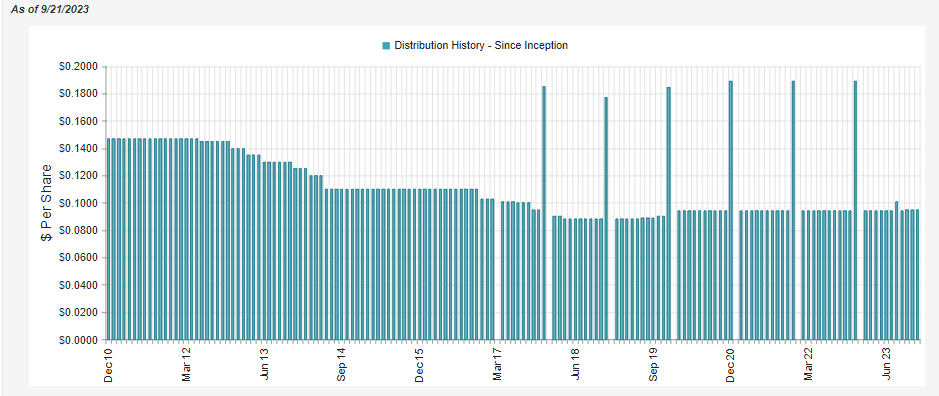

Distribution - Gets A Small Bump

HYI isn't a floating rate fund that we've seen aggressively increase their distributions through this higher rate environment. However, HYI can still benefit from higher yields over a longer period of time.

{kind=link}

This looks to be at least initially starting to take place as the fund increased the distribution to shareholders on the back of increasing net investment income. It was a small increase, and they certainly have much more history of cutting their payout during the previous zero-rate environment.

{kind=link}

In looking at their 2022 fiscal year, NII came in at $0.96. This had then increased to $1.07 at the end of fiscal 2023 , which is for the period ending May 31, 2023. The NII ratio to average net assets for the fund climbed from 6.32% to 8.38%, the highest in the last five years.

From their last quarterly financials for the period ending February 28, 2023, NII came in at $0.27. A year ago, the NII was at $0.24. For the quarter-over-quarter period ending November 30, 2022, had NII at $0.26. This shows us another way that NII has been getting progressively higher as income generation picks up.

This is a positive because, based on the annualized payout of $1.14, we'd see that it isn't being entirely covered yet despite them feeling comfortable enough to put in the small bump to the monthly distribution. Given that the Fed just signaled fewer cuts than originally anticipated in the coming years, this bodes well for HYI's chances to also grow its own income as yields stay elevated.

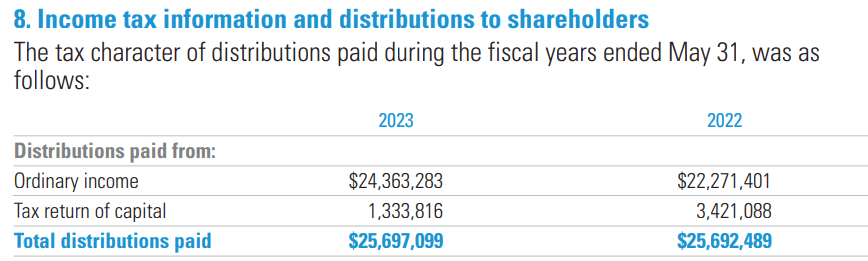

For tax purposes, the overwhelming majority of the distribution is classified as ordinary income, which is what we'd expected for a fixed-income fund. However, some return of capital has also been classified in the payout. Given that they aren't quite covering the payout at this point and weren't previously either, this also isn't too surprising.

{kind=link}

So, at this point, the NAV distribution rate of 9.27% is still quite a bit rich in terms of what the fund can earn, but it is certainly heading in the right direction. Due to not having the headwinds of growing leverage costs, I believe that puts HYI in a better position than their leveraged peers in the current environment.

HYI's Portfolio

HYI carries a portfolio of mostly BB and B rated debt. The CCC portion of its debt is also quite large, which is something to consider before investing in this fund. This does make it one of the more 'junky' below-investment-grade bonds.

HYI Credit Rating Allocation (Western Asset)

For some context, we recently covered the New America High Income Fund ( HYB ), and they had a 10.08% weighting in the CCC and below category. If we give BlackRock Corporate High Yield Fund ( HYT ) a look, we see that CCC rated debt is at a weighting of just over 13%.

The fund is also invested fairly meaningfully outside of the U.S., with U.S. exposure still being the dominant weighting. No other country allocation really commands even close to having a material weighting on its own, but in the aggregate, there is still some decent global exposure here.

HYI Geographic Allocation (Western Asset)

The fund's weighted average life comes to 5.14 years with an effective duration of 3.52 years. Given the high yield exposure, it is fairly common to have a lower duration as maturities generally come sooner, and yields are higher.

For some context, we can give HYT a look again and see its effective duration comes to 4.51 years. That would mean that the fund is anticipated to be more interest rate sensitive relative to HYI.

If we give the iShares iBoxx $ Investment Grade Corporate Bond ETF ( LQD ) a look, we get a duration of 8.22 years. Of course, that's a higher-quality portfolio with the heaviest allocation split between A and BBB rated debt. With higher credit ratings, investors would be willing to extend maturities out further and even at lower coupons with the idea that there is a good chance that the principal will be returned at the time of maturity.

Conclusion

HYI is a non-leveraged, high-yield focused fund. With having no leverage, it puts the fund in a position where it is potentially less volatile. Additionally, the fund hasn't had to deal with rising interest rate costs, and instead, they've only seen the upside of the higher rate environment leading to higher income generation. They raised their distribution a bit recently, and while it isn't entirely covered yet, management probably felt with the current trajectory that it could be covered before too long. That certainly seems probable given the new outlook of the Fed expecting only a couple of cuts next year.

For further details see:

HYI: No Leverage, No Problems