EFT - HYT: Surprisingly Strong Recent Performance And Improving Financials

2023-09-07 04:53:33 ET

Summary

- BlackRock Corporate High Yield Fund offers a 10.13% yield, providing investors with extra income in an inflationary environment.

- The fund's recent performance has been surprising, with its share price rising despite rising interest rates.

- The fund's focus on junk bonds and floating-rate assets may explain its strong recent performance as investors are fleeing into low-duration assets.

- The fund did manage to cover its distribution in the first half of the year, but it remains overly dependent on unreliable capital gains.

- The fund is trading at a discount to NAV, but it is a much smaller discount than normal.

BlackRock Corporate High Yield Fund, Inc. ( HYT ) is a 10.13% yielding closed-end fund that investors can purchase to obtain some extra income, which is sorely needed in today's inflationary environment. Indeed, the fund's potential here should be quite obvious by that yield, as it should not take very much money to obtain the higher level of income that is needed to maintain a certain lifestyle today compared to only two years ago. Unfortunately, any time a fund's yield gets into double-digits like this, it is a sign that the market expects that the fund will have to cut its distribution. I suggested this possibility as well the last time that we discussed this fund, although this fund has been one of the most reliable fixed-income securities with respect to the maintenance of its distribution.

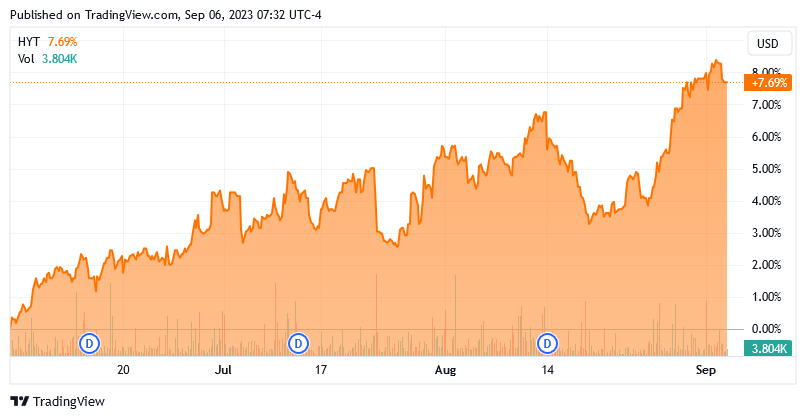

One very interesting thing here has been the recent performance of this fund in the market. Over the past three months, the fund's share price has risen by 7.69%:

{kind=link}

This is despite the fact that the Federal Reserve raised interest rates during the period and Chairman Powell has been extremely hawkish in recent speeches , even going so far as to suggest that interest rates will need to be increased further. The fund's performance has basically been the exact opposite of what we would normally expect from a bond fund in such a scenario. As such, we will want to investigate a few things here, namely the fund's ability to sustain its distribution and possibly what assets are in its portfolio to justify such a strong recent performance.

About The Fund

According to the fund's webpage , the BlackRock Corporate High Yield Fund has the objective of providing its investors with a very high level of current income. This makes a lot of sense for a fund whose assets are 96.99% invested in bonds:

CEF Connect

As I explained in my previous article on this fund,

Bonds are by their very nature an income vehicle. An investor will purchase a bond at face value at issuance, receive a steady stream of interest payments over the life of the bond, and then receive the face value of the bond back at maturity. Thus, the only investment returns that will ever be earned over the life of the bond are the coupon payments. The same is generally true for preferred stock, although there is no maturity date.

Bonds have no net capital gains over their lifetime, so the fund's focus on current income makes a great deal of sense.

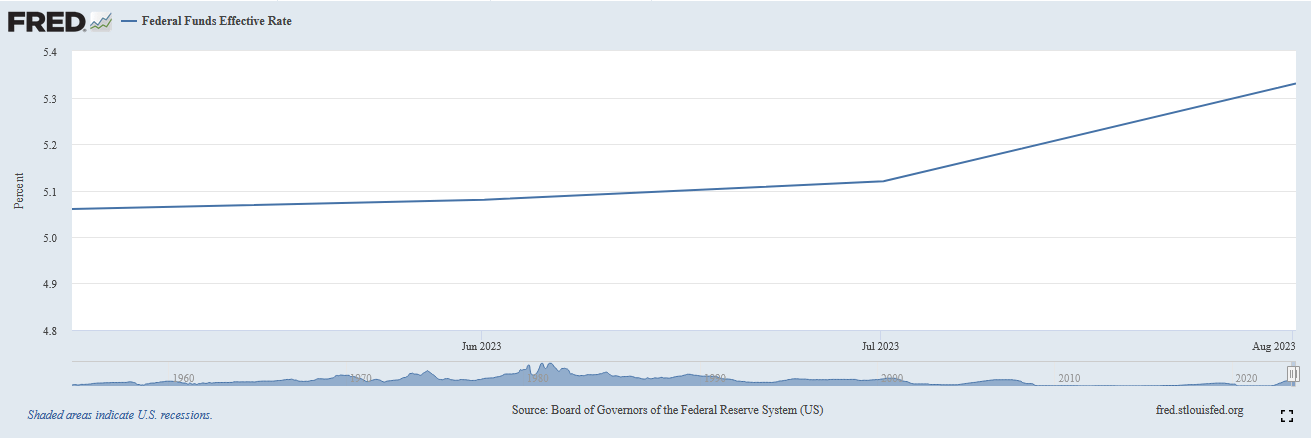

However, as everyone reading this likely knows, the price of bonds in the market does fluctuate with interest rates, which is what makes the fund's recent performance confusing. This chart shows the effective federal funds rate over the past three months:

{kind=link}

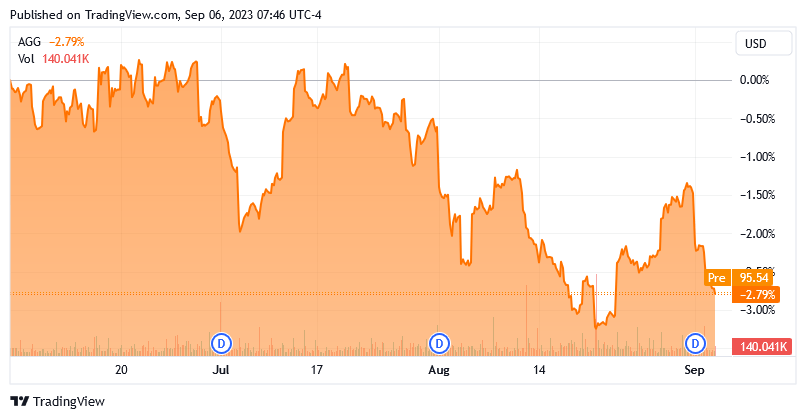

As we can clearly see, the federal funds rate has been rising over the period, which makes sense as the Federal Reserve hiked the target rate back in July. As of right now, the federal funds rate is at the highest level that we have seen since 2001, which was the tail end of the technology bubble. We would normally expect bond prices to decline in response to the rising interest rates, which actually was the case. As we can see here, the Bloomberg U.S. Aggregate Bond Index ( AGG ) is down 2.79% over the past three months:

{kind=link}

Yet, as we just saw, the BlackRock Corporate High Yield Fund is up over the same period. This is very difficult to explain with a bond portfolio.

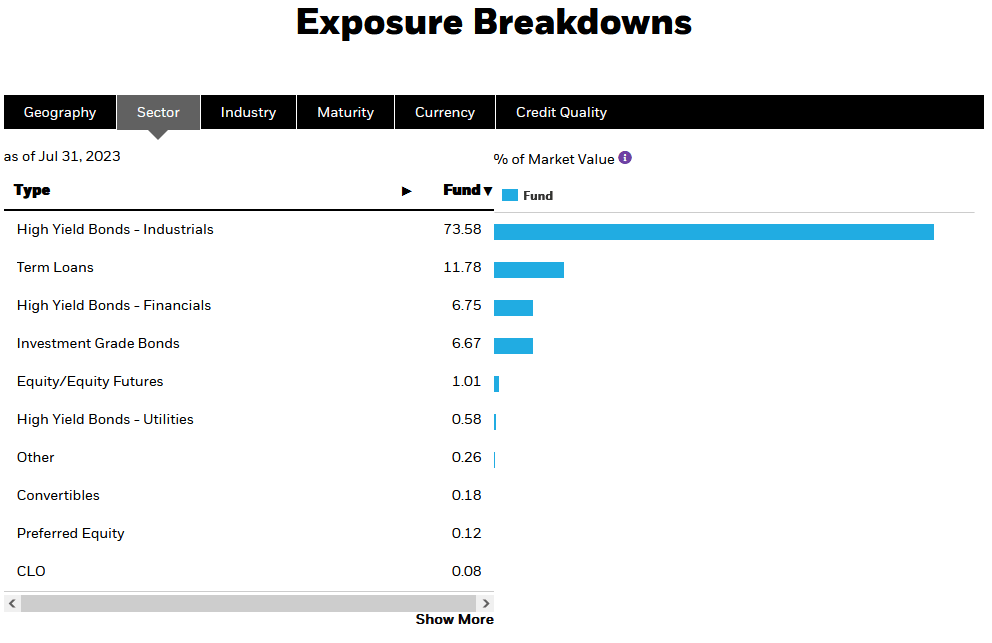

One possible explanation can be found by looking at the fund's holdings based on security type. Here they are:

{kind=link}

One thing that we note here is that 11.78% of the fund's assets are invested in term loans. These are frequently floating-rate assets, which tend to perform much better than traditional fixed-rate securities during a rising rate environment. I discussed this in a recent article focusing specifically on a floating-rate fund. We have certainly seen closed-end funds that invest in floating-rate securities deliver very strong performance recently. Here the price returns of a few of them over the past three months:

| Fund |

| Price Return |

| Apollo Tactical Income Fund ( AIF ) |

| 8.52% |

| Eaton Vance Floating Rate Income Trust ( EFT ) |

| 7.17% |

| Ares Dynamic Credit Allocation Fund ( ARDC ) |

| 7.76% |

The latter two are pretty close to what the BlackRock Fund delivered over the same period. The reason for this is that the coupon payments on these securities rise when interest rates do, so investors may be bidding them up with the expectation that interest rates will rise over the coming months. That is a very reasonable conclusion to draw, but it still cannot fully explain the performance that we see with this fund. After all, the overwhelming majority of the fund is invested in junk bonds and junk bonds are not generally floating-rate instruments. As such, traditional finance theory states that the majority of the assets in this fund will decline as interest rates rise.

In late 2021, an article in Reuters posited that some investors might be seeing the higher yield of junk bonds relative to investment-grade bonds as a buffer against rate hikes. As junk bonds have a much higher yield than investment-grade bonds, they have a lower duration. An investor might be willing to purchase these bonds, figuring that they might not sell off as much in response to rising rates due to the fact that their yields should still be relatively attractive. However, that article was written in late 2021 and interest rates went up more rapidly than anyone expected over the following two years. With that said though, we might have seen the same phenomenon over the summer. The past two months or so have seen an uptick in inflation and a change in market sentiment. The market is no longer confident in earlier predictions that interest rates would be cut later this year. Thus, bond investors may have responded by purchasing low-duration bonds, such as junk bonds, due to the perceived lower exposure to rising interest rates. This is all just speculation on my part, but it could explain why this fund has been delivering a performance comparable to floating-rate funds despite holding the majority of its assets in fixed-rate securities.

The fact that the BlackRock Corporate High Yield Fund is investing mostly in junk bonds could be a bit concerning for more risk-averse investors. Indeed, we have all heard about the high risk of losses due to defaults that these securities possess. The rapid increase in interest rates that we have seen over the past eighteen months could amplify this risk. Reuters reported on this:

Ratings firm Moody's Investors Service expects trailing 12-month default rates among speculative-grade issuers to climb nearly threefold to 4.4% in August 2023 from 1.5% in August 2022. This number could hit 13% in a worst-case scenario accompanied by high unemployment and wide spreads.

There has been a very sharp increase in defaults on floating-rate loans, however thus far junk bonds have been spared from the worst of it. This is probably because the rising interest rates do not actually increase a company's bond-servicing expenses until it has to roll over its bonds. Thus, it takes a little while for the sting of higher interest rates to actually have a noticeable effect on a company's cash flow. The rising rates have an immediate impact on the servicing expenses of a floating-rate loan though, which is the thing that is causing the increase in default losses in that sector. This is something that could be attractive to more risk-averse investors as we have not yet seen real problems related to junk bonds.

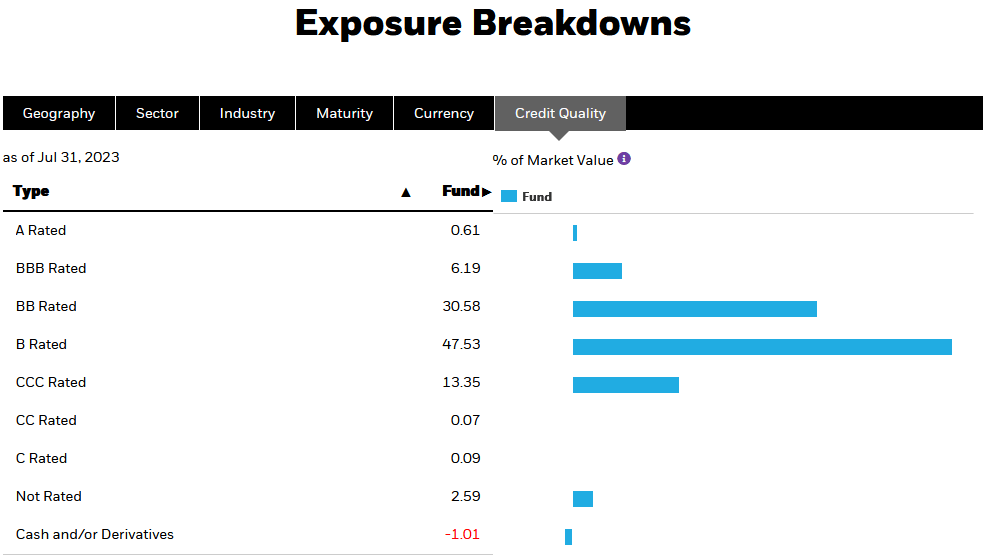

Further comfort can be found by looking at the ratings that have been assigned to the securities in the fund's portfolio. Here they are:

{kind=link}

As we can clearly see, only 6.80% of the fund's assets are rated investment-grade. Thus, the overwhelming majority of its assets are high-yield, speculative-grade securities. However, fully 78.11% of the portfolio has either a BB or a B credit rating. That is slightly lower than the 79.13% weighting to these particular securities that the fund had when we last discussed it. However, the fund's weighting to investment-grade securities increased by 0.39% over the same period. Thus, it does appear that the fund's risk is increasing but not at a very rapid rate. This could be comforting for risk-averse investors, especially considering that BB and B-rated securities are issued by companies that should be able to avoid default even if the economy hits a recession. In addition, the fund has 1,209 unique holdings so any individual issuer should only account for a very small portion of the overall portfolio. We probably do not need to worry too much about default losses at this point, but the fact that the fund's risk profile is deteriorating is something that we will want to keep an eye on.

Leverage

As is the case with most closed-end funds, the BlackRock Corporate High Yield Fund employs leverage in an attempt to boost the effective yield of its portfolio. I explained how this works in my last article on the fund:

In short, the fund borrows money and then uses that borrowed money to purchase high-yield bonds. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing at institutional rates, which are considerably lower than retail rates. As such, this will usually be the case. However, it is worth noting that the rising interest rate environment has made this strategy less effective than it was a few years ago, when leverage was basically free.

The real downside to leverage comes from the fact that it boosts both gains and losses. As such, we want to ensure that the fund does not have too much leverage, because that would expose us to too much risk. I do not typically like to see a fund's leverage exceed a third as a percentage of its assets for this reason."

As of the time of writing, the BlackRock Corporate High Yield Fund has a leverage ratio of 28.33%, which is pretty much in line with what it had the last time that we discussed it. It also fulfills our requirement for having less than a third of its assets purchased with leverage. As such, the balance between risk and reward is quite acceptable here.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the BlackRock Corporate High Yield Fund is to provide its investors with a high level of current income. In order to accomplish this objective, the fund primarily invests in junk bonds, which tend to have very high yields to compensate investors for the additional risks possessed by these securities. The fund then applies a layer of leverage to boost the effective yield of the portfolio. The fund collects all of the interest payments made by the securities in the portfolio and then pays them out to the shareholders, net of expenses. As such, we can assume that this fund will have a very high yield itself. That is certainly the case as the BlackRock Corporate High Yield Fund pays a monthly distribution of $0.0779 per share ($0.9348 per share annually), which gives it a 10.13% yield at the current price. The fund has been surprisingly consistent with its distribution over the years, as it has steadily raised it since 2015:

{kind=link}

This makes the BlackRock Corporate High Yield Fund one of the few fixed-income funds that has not cut its distribution over the past year or two. As such, it is quite likely that it will appeal to anyone who is seeking a secure and stable source of income to use to pay their bills or finance their lifestyles. However, it is curious that this fund has managed to achieve such stability when many of its peers could not. In addition, the current double-digit yield is a sign that the market expects that this fund will not be able to sustain its distribution going forward. We should therefore have a look at the fund's finances to determine how sustainable its distribution is likely to be.

Fortunately, we have a very recent document that we can consult for the purposes of our analysis. The fund's most recent financial report corresponds to the six-month period that ended on June 30, 2023. This is therefore a much newer report than the one that we had available to us the last time that we discussed this fund. That is a very good thing because this fund delivered a very disappointing performance in 2022, but it may have had an opportunity to turn things around in the first half of this year. After all, as we already discussed, the market was generally optimistic that the Federal Reserve would cut rates, so bond prices performed reasonably well. That could have given this fund the opportunity to earn some much-needed capital gains.

During the six-month period, the BlackRock Corporate High Yield Fund received $43,555 in dividends along with $67,139,088 in interest from the assets in its portfolio. When we combine this with a small amount of income that was received from other sources, we can see that the fund had a total investment income of $68,108,168 during the period. It paid its expenses out of this amount, which left it with $47,612,223 available for shareholders. This was, unfortunately, not nearly enough to cover the $66,697,943 that the fund paid out in distributions during the period. That is quite disappointing as we generally would like a fixed-income fund to be able to cover its distributions solely out of net investment income.

With that said, the fund does have other methods that can be employed to obtain the money that it needs to cover the distribution. For example, it might be able to earn capital gains that could be paid out to the shareholders. This is especially possible considering the fairly strong bond market that existed during the first half of 2023. Unfortunately, the fund only enjoyed moderate success at this task as it reported net realized losses of $69,338,743 but these were fully offset by net unrealized gains of $108,217,130 during the period. Overall, the fund's assets increased by $19,792,667 after accounting for all inflows and outflows during the period. This is a significant improvement from 2022, which is a year that saw the fund unable to fully cover its distributions.

The sustainability of the fund's distribution largely depends on how well it manages to perform going forward. The big question will be whether or not it can generate sufficient capital gains to cover the difference between net investment income and the amount paid out in distributions. This is uncertain, especially in a rising rate environment. That is one of the reasons why we like to see fixed-income funds cover their distributions fully out of net investment income. In this case, we should keep a close eye on the fund as it may not be able to sustain the payout in a weak second half of the year.

Valuation

As of September 5, 2023 (the most recent date for which data is available as of the time of writing), the BlackRock Corporate High Yield Fund had a net asset value of $9.38 per share but the shares currently trade for $9.23 each. That gives the fund's shares a 1.59% discount on net asset value at the current price. This is a lot worse than the 4.12% discount that the shares had on average over the past month, so the current price might be a bit high. It would probably be best to wait a bit and see if a better price can be obtained in the near future.

Conclusion

In conclusion, the BlackRock Corporate High Yield Fund has been delivering very interesting performance for a fixed-income fund recently. The fund's share price has been rising over the past few months despite a corresponding increase in interest rates. This could be because of its focus on junk bonds, which have lower durations than corporate bonds. The fund seems to be in much better shape financially than the last time that we looked at it, which is also fortunate and could be contributing to the strong performance. Unfortunately, the fund is a bit pricey compared to its historical levels, so it might be best to wait for a better entry price.

For further details see:

HYT: Surprisingly Strong Recent Performance And Improving Financials