TDG - HYT: Very Attractive Portfolio But Distribution May Be At Risk

Summary

- The incredibly high level of inflation has caused many investors to look for ways to increase their incomes in order to maintain their standard of living.

- BlackRock Corporate High Yield Fund, Inc invests in a portfolio of high-yield bonds in order to provide that income.

- The closed-end fund has generally performed poorly over the past year as rising interest rates have crushed the value of bonds in the market.

- The fund is struggling to maintain its distribution and may have to cut it in the near future.

- The fund is trading at a reasonably attractive valuation, but it may be best to wait until a distribution cut before buying it.

One of the biggest problems facing Americans today is the incredibly high rate of inflation that has been dominating the economy. This inflation has gotten so bad that it is forcing many people to take on second jobs or begin performing odd tasks in order to get the extra money that they need to keep themselves fed and warm.

Fortunately, as investors, we have better methods that we can use to generate the extra income that we need to maintain our standard of living. One of these methods is to purchase shares of a closed-end fund that specializes in the generation of income. These funds are quite nice as they provide easy access to a portfolio of income-producing securities that can usually provide a higher yield than any of the underlying assets. In addition, these funds enjoy remarkable diversification due to their professional management team and as such are usually less risky than the portfolio that we would get by assembling it ourselves.

In this article, we will discuss the BlackRock Corporate High Yield Fund, Inc ( HYT ), which is one closed-end fund ("CEF") that can be used for this purpose. I have discussed this fund before, but more than a year has passed since that time, so obviously a great many things have changed. This article will, therefore, focus specifically on these changes and attempt to determine if this 10.70%-yielding fund could be a reasonable addition to our portfolios today.

About The Fund

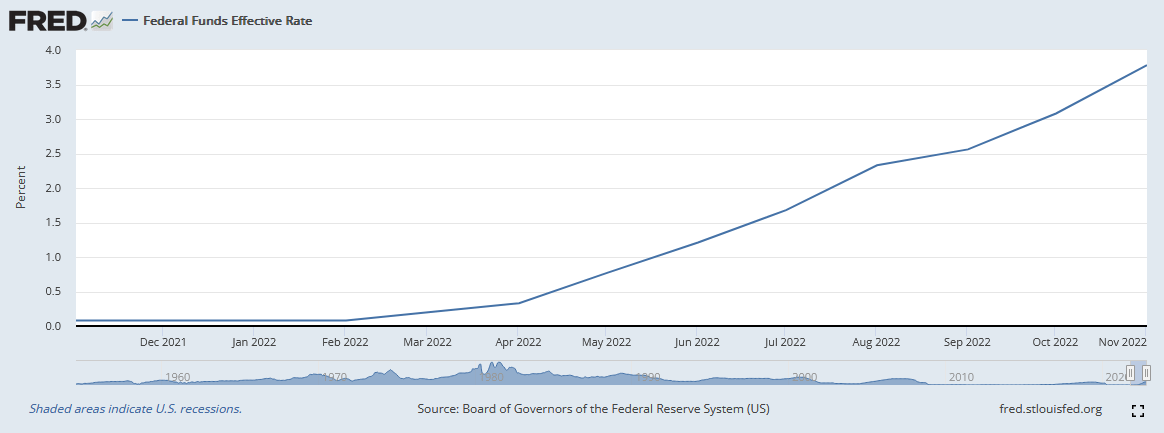

According to the fund’s webpage , the BlackRock Corporate High Yield Fund has the stated objective of providing its investors with a high level of current income. This is not surprising as a high-yield fund typically invests in fixed-income securities. These securities typically deliver the overwhelming majority of their investment return in the form of direct payments to their investors and cannot really be counted on for capital gains. This is because they have no direct link to the performance and prosperity of the issuing company. After all, a company will not increase the interest payments on its debt just because its profits increased. A fixed-income security is instead priced based on interest rates. As a rule, when interest rates go up, fixed-income security prices decline and vice versa. This is because newly issued securities will have a higher yield than existing securities when interest rates are rising. As such, the price of the already-existing securities will necessarily decline so that they have the same yield-to-maturity as similar newly-issued bonds. As everyone reading this is no doubt aware, the Federal Reserve shifted its monetary policy from loose to tight last year. In February 2022, the federal funds rate, which is the benchmark interest rate in the United States, sat at 0.08%. It had risen to 3.78% by November 2022:

{kind=link}

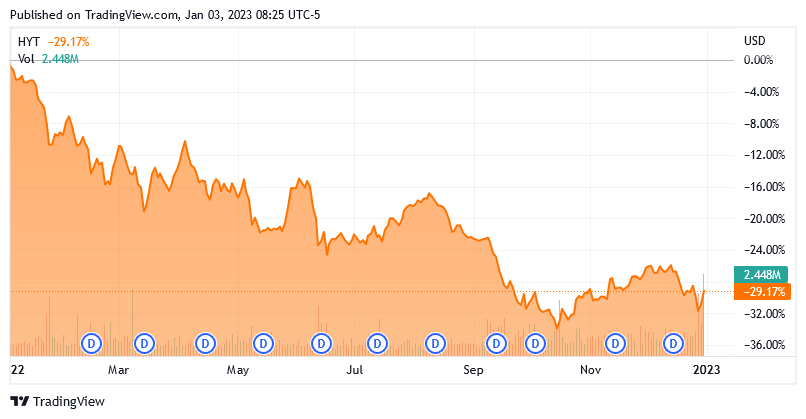

The Federal Reserve has not released data on the effective rate for December 2022 yet, but we can expect it to be somewhat higher. This is because the central bank agreed to raise the rate by 50 basis points at the meeting that it held in the middle of December. As might be expected based on the above discussion, this series of rising rates have caused the BlackRock Corporate High Yield Fund, Inc to decline in price over the past year. The fund is down 29.17% over the trailing twelve-month period:

{kind=link}

This is likely to continue in 2023, which is somewhat unfortunate for many investors. The Federal Reserve has already stated that it intends to keep raising the federal funds rate for at least through the first quarter of the year, expecting that rates will peak at 5%. That is a bit above today’s level, so we can expect that the fund will decline a bit more, although it will probably deliver a much better performance than it did in 2022.

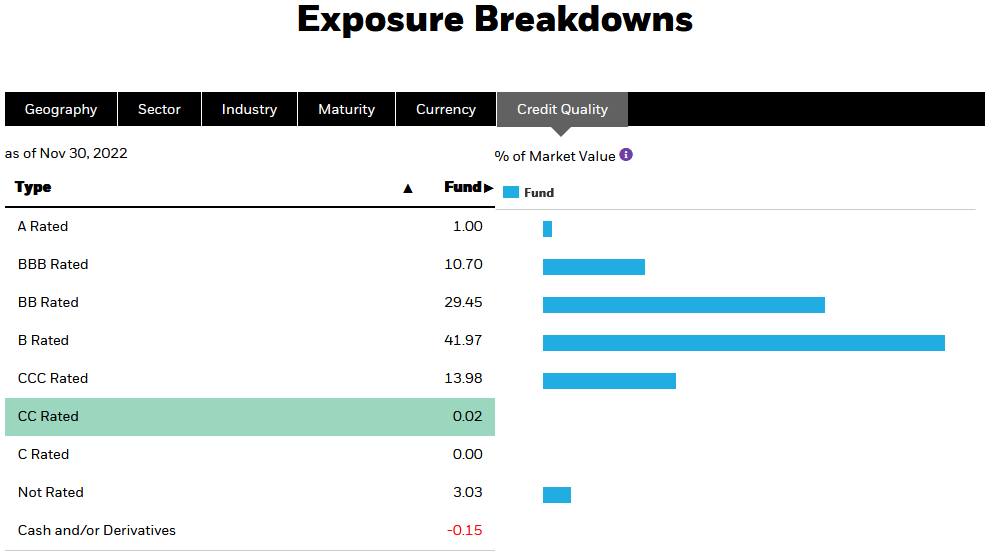

As such, current income is going to be the best that we can expect from this fund for the time being. Fortunately, this is something that it does very well. As the name of the fund implies, the BlackRock Corporate High Yield Fund primarily invests in high-yield bonds, which are colloquially known as “junk bonds.” This is something that may be concerning since these bonds are frequently considered to be at high risk of default. Naturally, when a bond defaults, our principal is at risk. However, this risk is likely overstated, at least in the case of this fund. We can see this by looking at the credit ratings of the bonds in the portfolio. Here they are:

{kind=link}

As we can see, 71.42% of the bonds in the fund’s portfolio are rated BB or B by the major rating agencies (S&P, Moody’s, and Fitch). This is something that is fairly nice because these are the highest possible ratings for high-yield bonds. According to the official bond rating scale , companies that are rated BB or B rated have the sufficient financial capacity to meet their current financial commitments. In addition, these companies have strong enough balance sheets to weather short-term economic shocks but may not have the wherewithal to handle long-term problems. However, we have not had a prolonged economic downturn since the Great Depression so this is something of minimal risk. Overall, the bonds in the portfolio should have a relatively low risk of default.

Another way that the fund can reduce the risk of investor losses due to default is to have a large number of holdings. This ensures that any default that does happen only affects such a small proportion of the portfolio that it is not noticeable enough to have any real impact on the investors. This fund certainly does that as it currently has 1,369 positions. When we combine this with the reasonably strong credit ratings of the assets in the portfolio, we can conclude that we only really need to worry about default if a large number of companies go bankrupt during a period of prolonged economic stress. In that situation, though, we will all have far more to worry about than just a few investors losing money. The odds of such an event are unlikely in the extreme. Overall, there does not appear to be anything for us to worry about here.

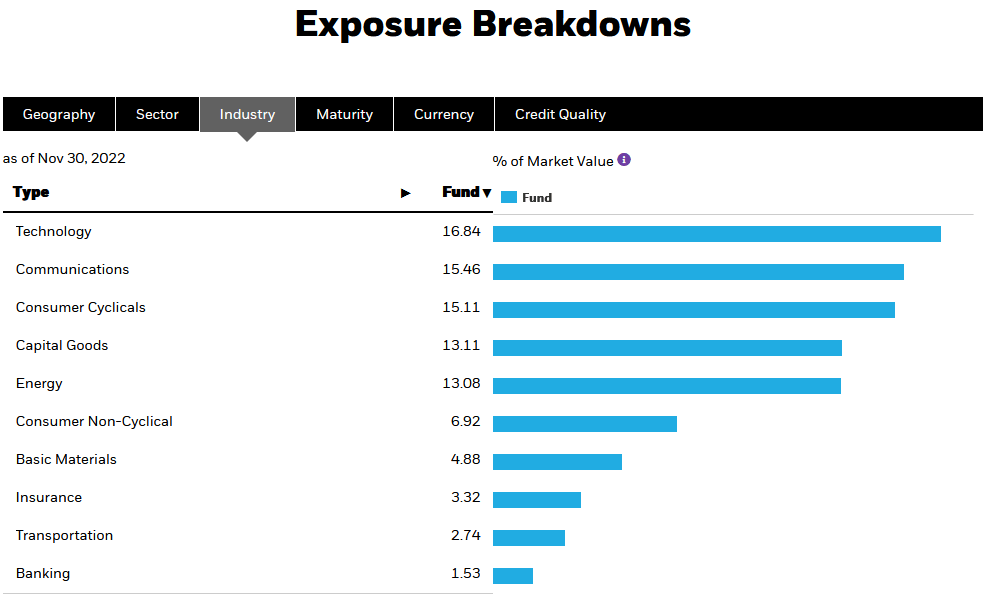

Another way that the BlackRock Corporate High Yield Fund protects us against risk is by spreading its assets around different sectors. Indeed, this fund is remarkably well-balanced in terms of the industries whose bonds comprise its portfolio:

{kind=link}

This is nice, because each of these sectors has very different fundamentals. We saw this somewhat in 2020 as the energy sector nearly collapsed but the technology sector did incredibly well. Today, the reverse is true as technology and consumer discretionary are struggling but energy and healthcare are doing just fine. The fact that the fund has reasonably balanced exposure to all of these different sectors, therefore, provides investors with exposure to those strong companies and weak ones as well as the ability to take advantage of any reversal in fortunes. Overall, investors should be quite pleased about this balanced exposure.

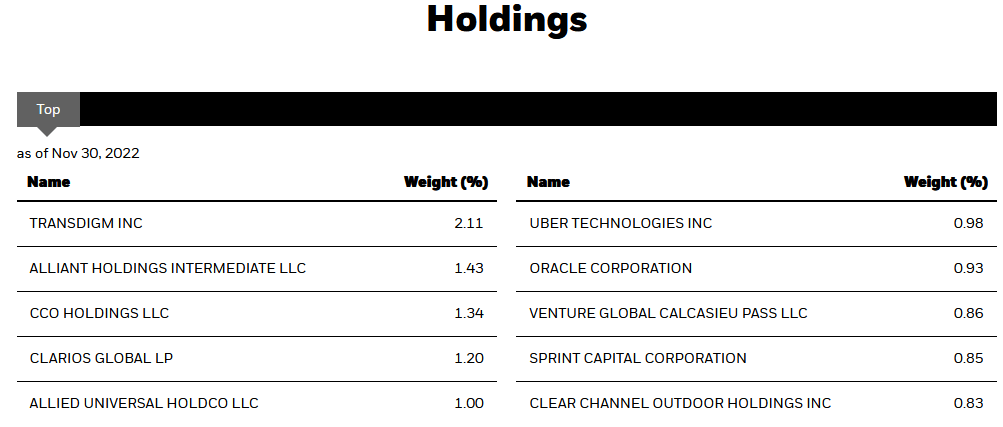

Although the BlackRock Corporate High Yield Fund, Inc has a substantial number of holdings, it is not prevented from having a high degree of exposure to a relatively small number of companies. We can see this by looking at the largest positions in the fund. Here they are:

{kind=link}

Admittedly, this is nowhere near as bad as many equity funds that frequently have single companies accounting for more than 5% of the portfolio. However, we do see a sizable amount of exposure to TransDigm Group Incorporated ( TDG ) in the fund. TransDigm is a major aerospace company so this might not be a horrible place to be considering that there is a war going on in Europe, but it still could be a risk as the economy enters into a recession and the demand for air travel almost certainly declines. However, it is important to keep in mind that these are bonds so they should hold up better than stocks. After all, TransDigm needs to make the payments on the bonds before it can give anything to the stockholders. It will almost certainly be able to make these required payments regardless of any foreseeable economic problems so there is probably nothing to worry about here.

There have been a number of changes to the largest positions in the fund since we last reviewed the fund. In fact, only TransDigm, Alliant Holdings Intermediate, Clarios Global ( BTRY ), and Allied Universal HoldCo LLC retained their positions as one of the fund’s ten largest positions over the past year. This could imply that the fund is doing a great deal of trading within its portfolio. This is somewhat true as the fund’s 54.00% annual turnover is higher than many other fixed-income funds. This is something that we should keep in mind because it costs the fund money to trade bonds and these costs are billed to the shareholders. This creates a drag on the fund’s performance because management has to generate a sufficient return to cover these costs and still deliver a return that satisfies the investors. This is a very difficult task to accomplish and usually results in actively-managed funds underperforming their benchmark indices.

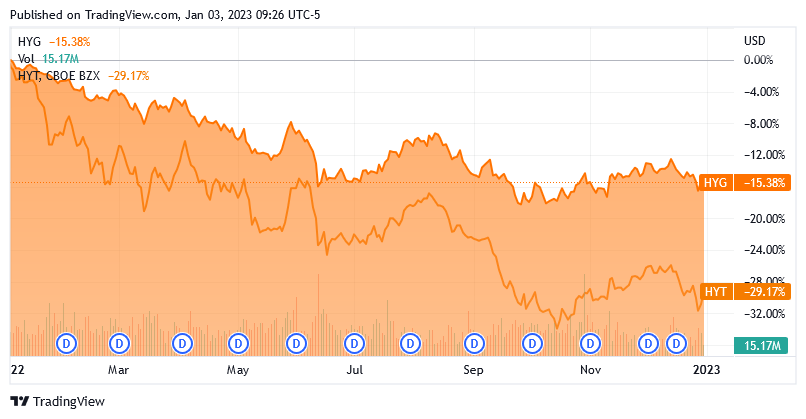

This is certainly true for this one, as the BlackRock Corporate High Yield Fund has underperformed the Markit iBoxx USD Liquid High Yield Index ( HYG ) over the past twelve months:

{kind=link}

With that said, the closed-end fund does have a significantly higher yield than the index fund so that helps to close the performance gap somewhat. However, an investor that reinvests the distributions would have still been better off with the iShares index fund. The fact that the BlackRock Corporate High Yield Fund has a substantially higher turnover is one reason for this underperformance but it is not the only one.

Leverage

As mentioned in the introduction, closed-end funds are able to use a variety of strategies that have the effect of boosting their yields beyond that of any of the underlying assets. One of the strategies that are used by the BlackRock Corporate High Yield Fund is the use of leverage. In short, the fund borrows money and uses that borrowed money to purchase junk bonds. As long as the yield on the purchased assets is higher than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the overall yield of the portfolio. As the fund can borrow at institutional rates, which are lower than retail rates, this will usually be the case.

However, the use of debt is a double-edged sword since leverage boosts both gains and losses. This is another reason why the fund has significantly underperformed the index. Naturally, we want to ensure that the fund is not employing too much leverage since this would expose us to too much risk. I do not like to see a fund’s leverage go above a third of its assets for this reason. Fortunately, the BlackRock Corporate High Yield Fund fulfills that requirement. The fund’s levered assets comprise 30.39% of the portfolio, which is a level that represents a reasonable balance between risk and return. Despite the fact that the fund will likely underperform the index as long as rates keep rising, there does not appear to be an outsized amount of risk here with respect to the fund’s use of leverage.

Distribution Analysis

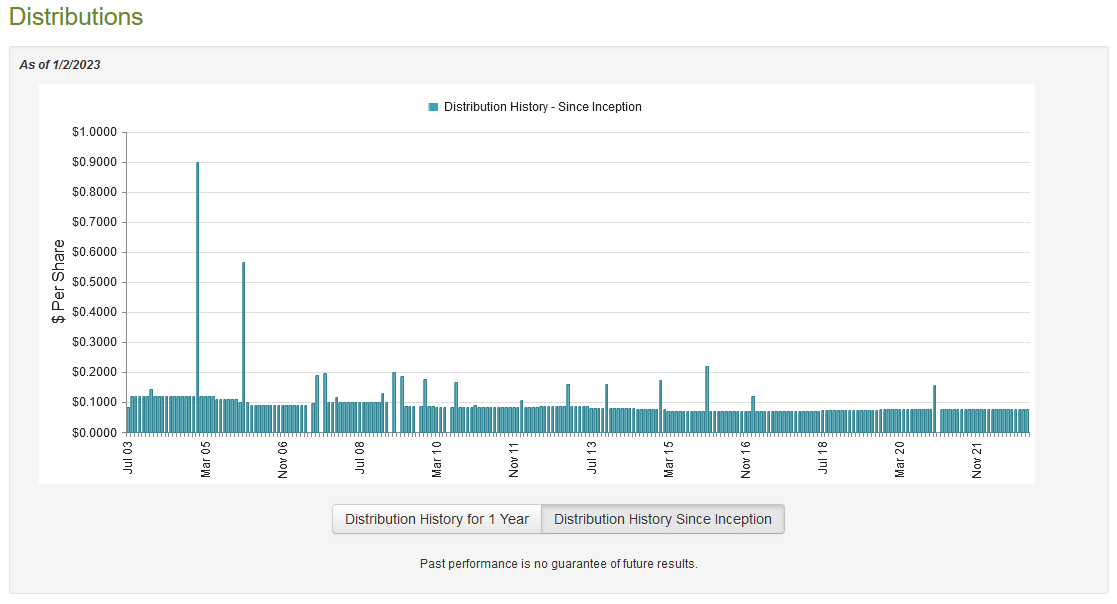

As mentioned earlier in this article, the primary objective of the BlackRock Corporate High Yield Fund is to provide its investors with a high level of current income through the distributions that it pays out. The fund seeks to accomplish this objective by maintaining a portfolio of high-yield bonds and then using leverage to boost the yield. As such, we might assume that the fund has a very high distribution yield itself. This is certainly the case as it currently pays out a monthly distribution of $0.0779 per share ($0.9348 per share annually), which gives the fund a 10.70% yield at the current price. Unfortunately, the fund’s distribution has varied quite a bit over the years, although it has maintained the current distribution since October 2019:

{kind=link}

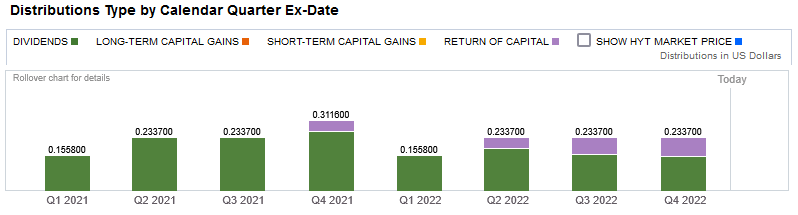

The fact that the fund’s distribution has remained stable since 2019 despite the economic issues that we have experienced since then will likely be a source of comfort for those investors that are seeking a stable and secure source of income to use to pay their bills and maintain their lifestyles. However, the fund has been paying out a growing amount of return of capital in the past few quarters, which could dampen the enthusiasm somewhat:

{kind=link}

The reason why this may be concerning is that a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them. This is something that is obviously not sustainable over any sort of extended period. However, there are other things that can cause a distribution to be classified as a return of capital. For example, the distribution of unrealized capital gains is typically classified in this way. As such, we should investigate the fund’s finances to determine where exactly it is getting the money to pay its distributions and determine how sustainable its distributions are likely to be over time.

Fortunately, we do have a somewhat recent document to consult for that task. The fund’s most recent financial report corresponds to the six-month period ending June 30, 2022. Although this document will not provide us with any insight into the second half of 2022, it will still tell us how well the fund handled the reversal of the Federal Reserve’s monetary policy that sent shockwaves through the bond markets. During the six-month period, the BlackRock Corporate High Yield Fund received a total of $1,043,568 in dividends and $52,571,290 in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, the fund brought in a total of $53,752,272 during the period. It paid its expenses out of this amount, leaving it with $43,850,623 available for investors. This was, unfortunately, not enough to cover the $47,620,136 that the fund actually paid out in distributions but it did get fairly close. However, it may still be a somewhat worrying situation for the purposes of the fund’s ability to sustain the distribution.

The fund does have other ways that it can obtain the money that it needs to maintain its distribution, however. The most common of these methods is through the generation of capital gains. As might be expected from the performance of the broader bond market, the fund generally failed at this task. It reported net realized losses of $5,864,389 and had another $300,571,470 net unrealized losses. Overall, the fund’s assets declined by $309,139,506 during the six-month period after accounting for all inflows and outflows. This is likely one of the reasons that the fund did a capital raise during the second half of 2022 as it is clearly unable to sustain its distribution at the current level without having more money. Thus, it does appear that the fund’s recent return of capital distributions was actually caused by the fund distributing money from new investors to existing ones. This is concerning and a sign that we may not want to purchase shares of it until it either cuts the distribution or manages to increase its income to make the distribution sustainable.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund, one metric that we can use to value it is the net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. That is because such a scenario implies that we are purchasing the fund’s assets for less than they are actually worth. This is, fortunately, the case right now with this fund. As of December 30, 2022 (the most recent date for which data is currently available), the BlackRock Corporate High Yield Fund had a net asset value of $9.25 per share but the shares currently trade for $8.76 each. This gives the fund’s shares a 5.30% discount to the net asset value at the current price. This is a much more attractive price than the 3.40% discount that the shares have possessed on average over the past month so the price is certainly reasonable today. This may be because the fund is struggling to maintain its yield.

Conclusion

In conclusion, the high level of inflation that continues to plague the economy has forced many investors and others to begin looking for alternative sources of income. One of the best methods available to us is owning shares of an income-focused closed-end fund. On the surface, the BlackRock Corporate High Yield Fund appears to have a lot to like as it offers a very well-diversified portfolio of high-yield bonds that appears to be relatively safe from default risk. However, a look under the surface reveals that the fund is struggling to maintain its current distribution and may be forced to cut it in the near future. Otherwise, though, there appears to be a lot to like here with BlackRock Corporate High Yield Fund, Inc, as the price is certainly attractive and the fact that the distribution has been stable since 2019 is a nice quality. I would recommend waiting until BlackRock Corporate High Yield Fund, Inc does something to make its distribution affordable before buying, however.

For further details see:

HYT: Very Attractive Portfolio But Distribution May Be At Risk