IAUX - i-80 Gold: A Transformational Year On Deck

2024-01-11 16:19:51 ET

Summary

- i-80 Gold Corp. has had a tough start to 2024 after a significant decline in 2023, but the share price performance doesn't reflect the strong progress made over the past year.

- Meanwhile, the company has a very busy 2024 on deck that I would describe as transformational, with significant resource growth, further production growth, and a possible JV deal.

- In this update, we'll dig into recent drill results, the 2024 outlook, and whether the stock is worthy of investment.

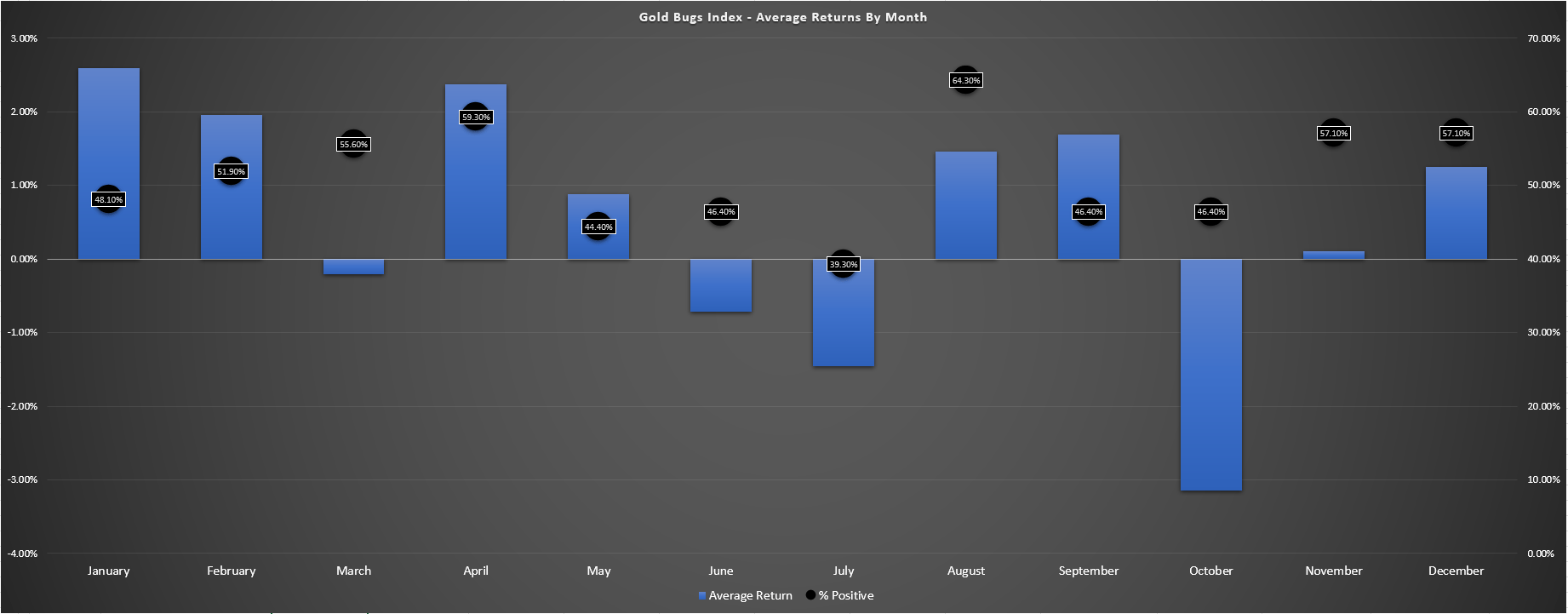

It's been a rough start to the year for the Gold Miners Index ( GDX ) in what's typically the best month of the year from a seasonal standpoint, with an average return for the sector of ~2.6% in January over the past 30 years. This is certainly disappointing for investors especially with the metal's price logging a record six weekly closes above the $2,000/oz level, but can be explained by continued negative sentiment. Unfortunately, i-80 Gold Corp. ( IAUX ) has been one of the underperformers to start the year, but this softening in the stock has occurred ahead of what's set to be a transformational year for the company as it ramps towards full production levels at its currently operating mine and potentially secures a joint-venture on its largest asset where it's made multiple new discoveries, Ruby Hill.

In this update we'll dig into recent drill results, the 2024 outlook, and whether the stock is worthy of investment.

Gold Bugs Index - Average Returns By Month & Percent of Months Positive - Author's Chart & Data

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Granite Creek Drill Results

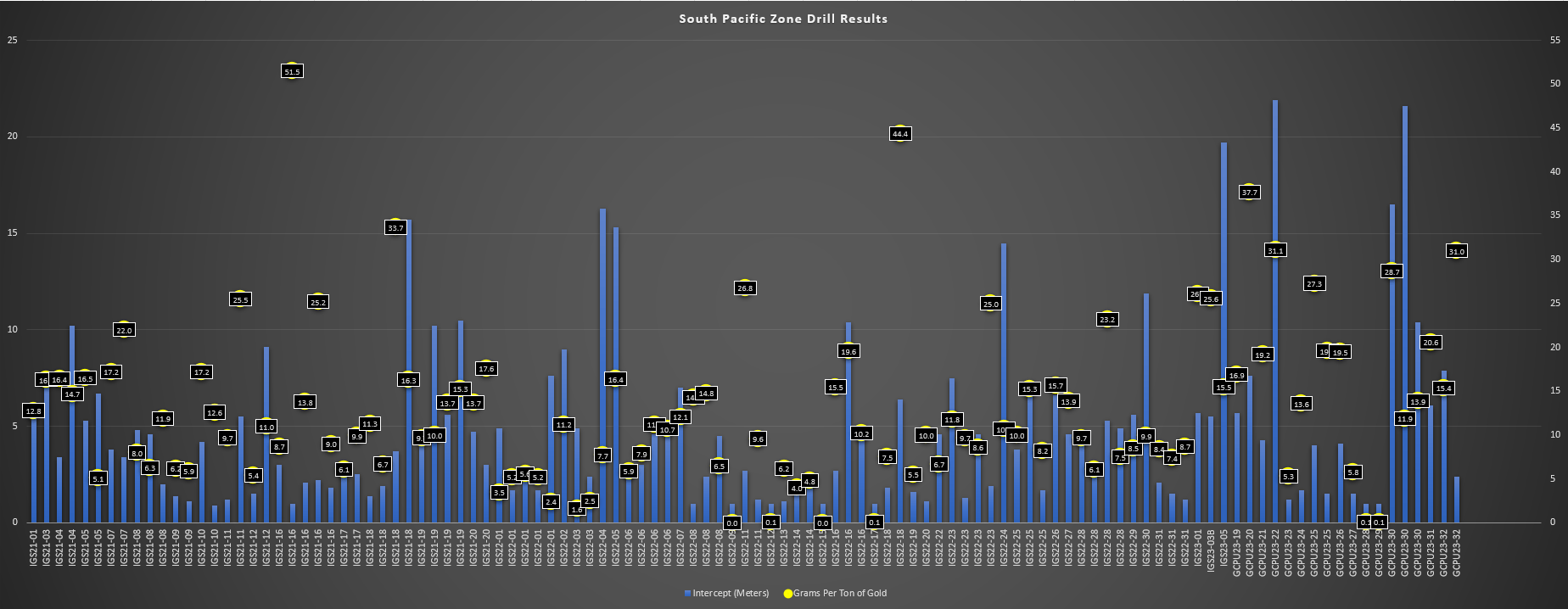

i-80 released more drill results from the South Pacific Zone at its Granite Creek Underground Mine last month. For those unfamiliar, this is a new discovery at its currently producing Granite Creek which is expected to be its main production area with it having a greater proportion of sulfide material vs. the Ogee Zone, better ground conditions, slightly better grades and a much larger strike length (up to 800 meter strike). The average intercept was 7 meters at 20+ grams per ton of gold, the best intercept was an impressive 21.9 meters at 31.1 grams per ton of gold (best gram-meter hit to date, beating out 15.3 at 16.4 grams per ton of gold in hole IGS22-05 and 19.7 meters at 15.5 grams per ton of gold in hole IGS23-05) and the average intercept drilled at South Pacific Zone since its discovery is ~5.0 meters at ~13.0 grams per ton of gold. True widths were a little lower in the most recent release at closer to 50% vs. 70% previously, but these are still very impressive intercepts even if adjusted for true widths.

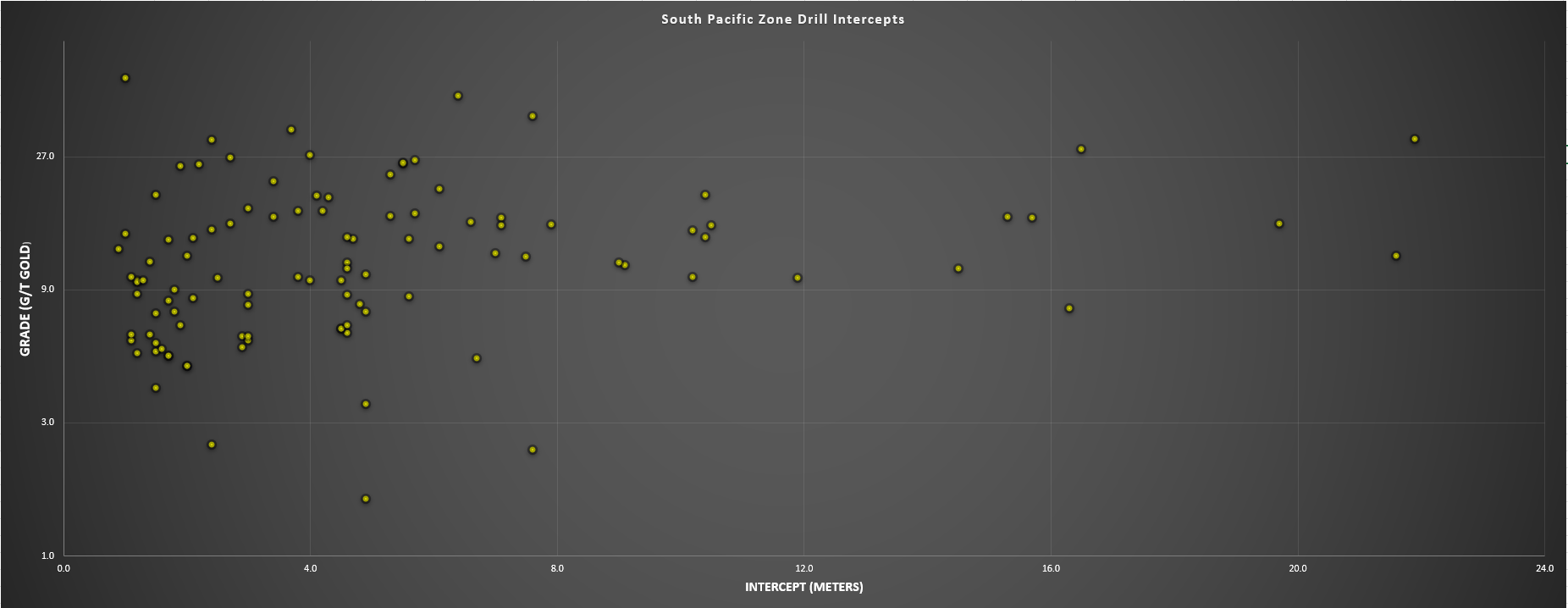

South Pacific Zone Drill Results - Company Filings, Author's Chart South Pacific Zone Drill Intercepts - Company Filings, Author's Chart

{kind=link}

{kind=link}

As the charts above show, i-80 continues to have an extremely high hit rate at the new South Pacific Zone (~96% of intercepts have hit mineralization), from what will be one of its spokes at its future autoclave (toll-milling agreements in place for meantime). If we assume an average throughput rate of 800 tons per day (Ogee + South Pacific Zone), an average grade of 10.7 grams per ton of gold and 85% recovery rates, this translates to ~80,000 ounces of gold per annum from Granite Creek Underground alone once in full production, a very productive spoke for the future Hub & Spoke Model (three gold mines feeding the Lone Tree autoclave) given its relatively low mining rates. In addition, it's encouraging to see grade control sampling outperforming expectations for four levels to date (4430, 4445, 4475, 4490), and very encouraging to see grades meeting/exceeding current underground resources which sit at ~660,000 ounces at 11.0+ grams per ton of gold (Otto, Adam, Ogee zones), which does not include the new South Pacific Zone discovery.

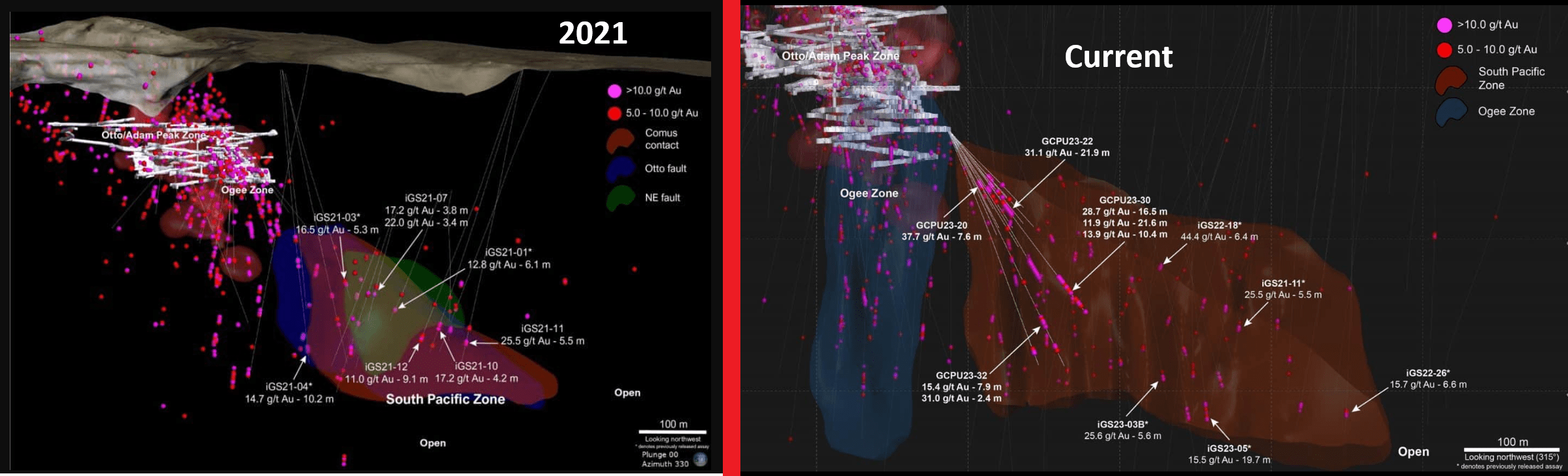

Granite Creek 2021 vs. Current - Company Filings

{kind=link}

The above image highlights what the South Pacific Zone was believed to be in 2021 with drilling at the time vs. how it's grown today to quadruple the strike of the Ogee Zone, and with the highest-grade intercepts coming at depth.

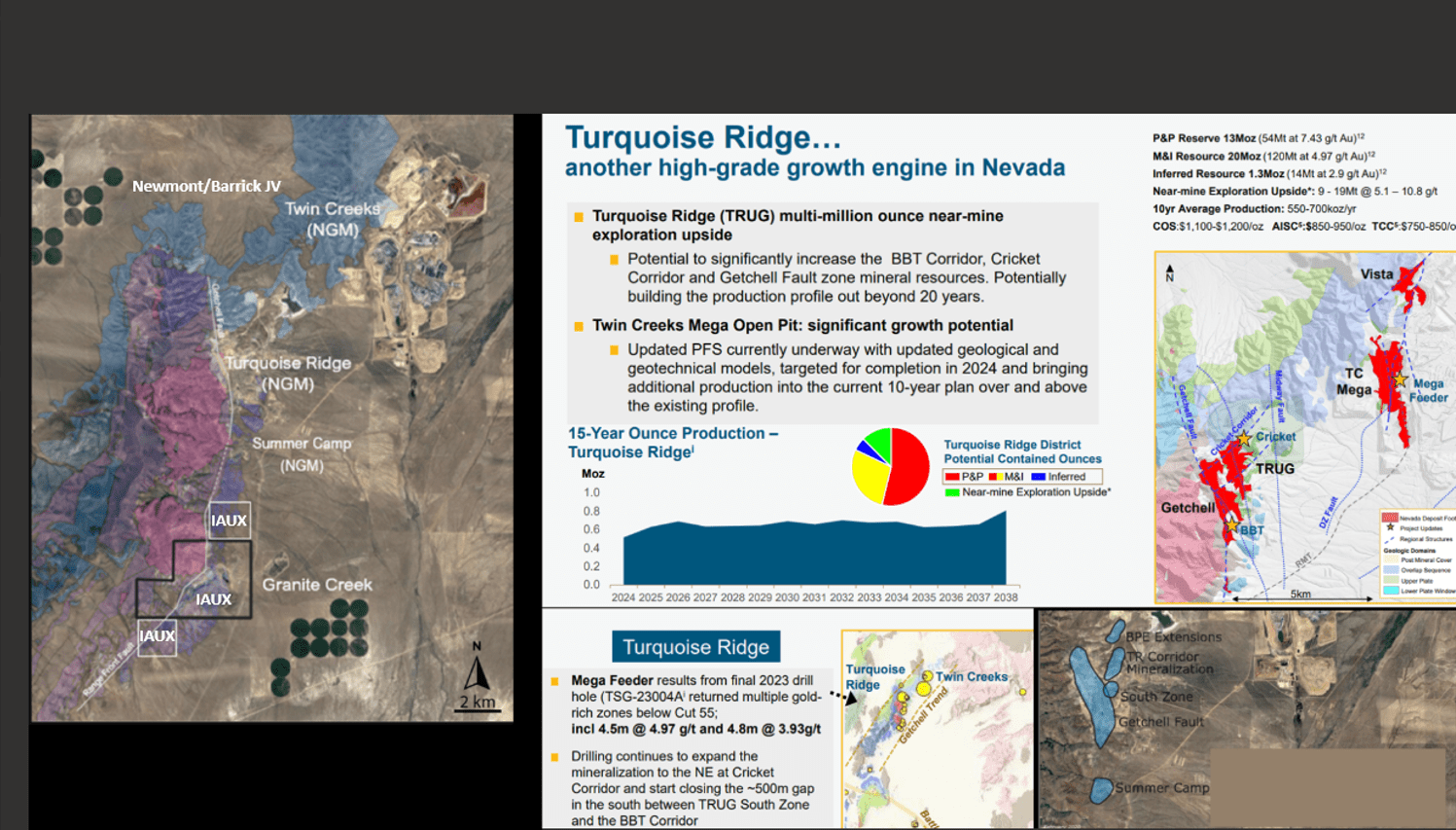

Although South Pacific will provide significant upside to the current resource at Granite Creek Underground, the South Pacific Zone remains open to the north and significant land was added in May 2022 (1.6 kilometers north of previous land package towards the Turquoise Ridge Complex that is a ~600,000 ounce per year mining complex). Plus, historic drilling in hole HPC-175 hit high-grade mineralization 400 meters north of the current South Pacific Zone footprint. Hence, there is certainly the potential that the South Pacific Zone continues north, while there's further upside at depth in the Lower Comus Zone. In fact, i-80 Gold's CEO Ewan Downie has stated the following in past interviews:

"So that deeper area is looking like it's really coming together. There's two additional major fault structures that we think will intersect the South Pacific Zone to the north and these represent to us some really big scale targets that next year we can start looking at this bigger, deeper targets. If you look at the history of the Turquoise Ridge Mine, the upper parts were quite difficult. It wasn't until they got below 600 meter depths that they found what is being mined today where the stratigraphy flattens. We're drilling to depths of only about ~450 meters, so we're still above where they found the bigger part of the Turquoise Ridge deposit.

"The geological setup is essentially identical to Turquoise Ridge, now we just have to hope we’re as big as that”

- i-80 Gold CEO, Ewan Downie.

Deep Range Front Target Drill Core - Company Website

{kind=link}

One of these targets includes the Deep Range Front Target, where historic drilling hit 4.9 meters at 49.0 grams per ton of gold and 16.8 meters at 10.5 grams per ton of gold, as well as one of i-80's best intercepts on the property of 15.3 meters at 16.3 grams per ton of gold. As highlighted in i-80's most recent presentation, ground conditions look to improve at depth with this target south of the Ogee/South Pacific deposits, so there's the certainly the possibility of a Turquoise Ridge Underground repeat with i-80 drilling directly on strike with this massive high-grade asset. Hence, given the exploration upside at depth and along strike, I would not be surprised to see Granite Creek Underground ultimately grow into a 2.2+ million ounce resource (triple its current size), and this would still place Granite Creek's total endowment at just ~3.6 million ounces, a fraction of the ~21 million ounce resource at the Turquoise Ridge Complex currently.

Granite Creek Land, Turquoise Ridge Complex & Recent Drilling Results - i-80 Gold & NGM Presentation

{kind=link}

A Busy 2024 On Deck

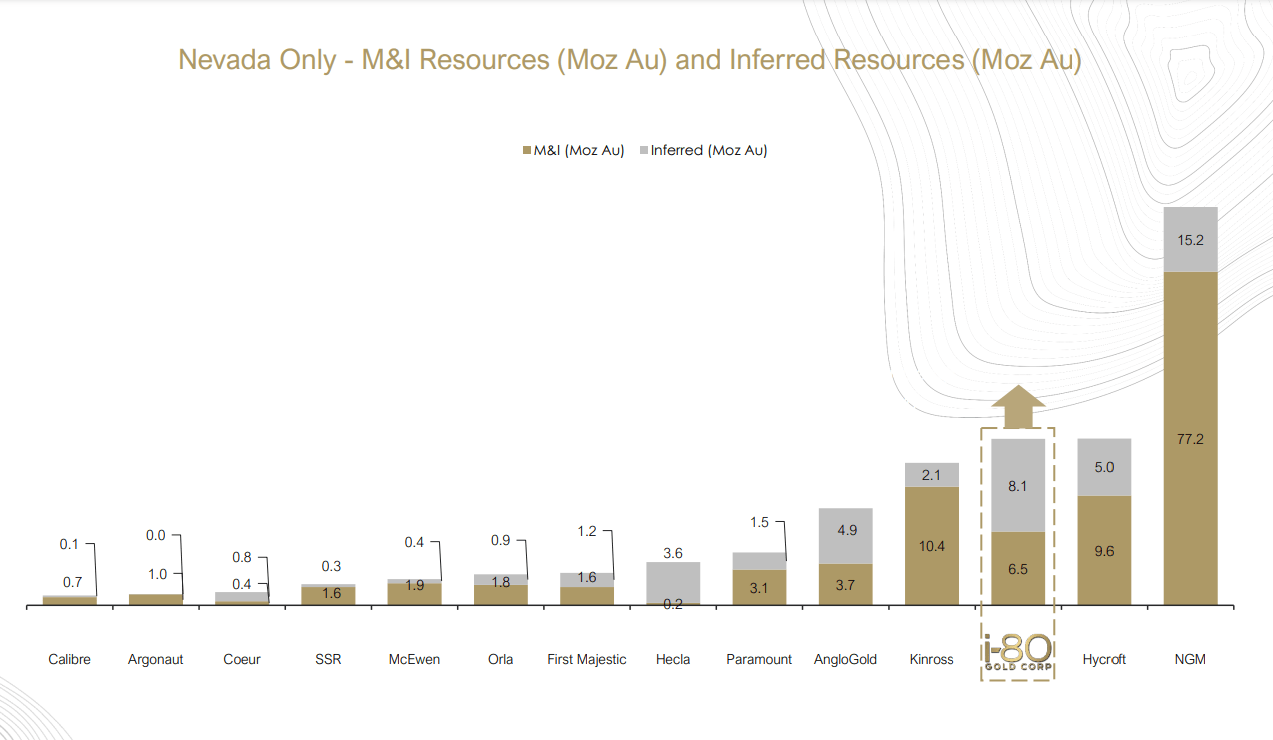

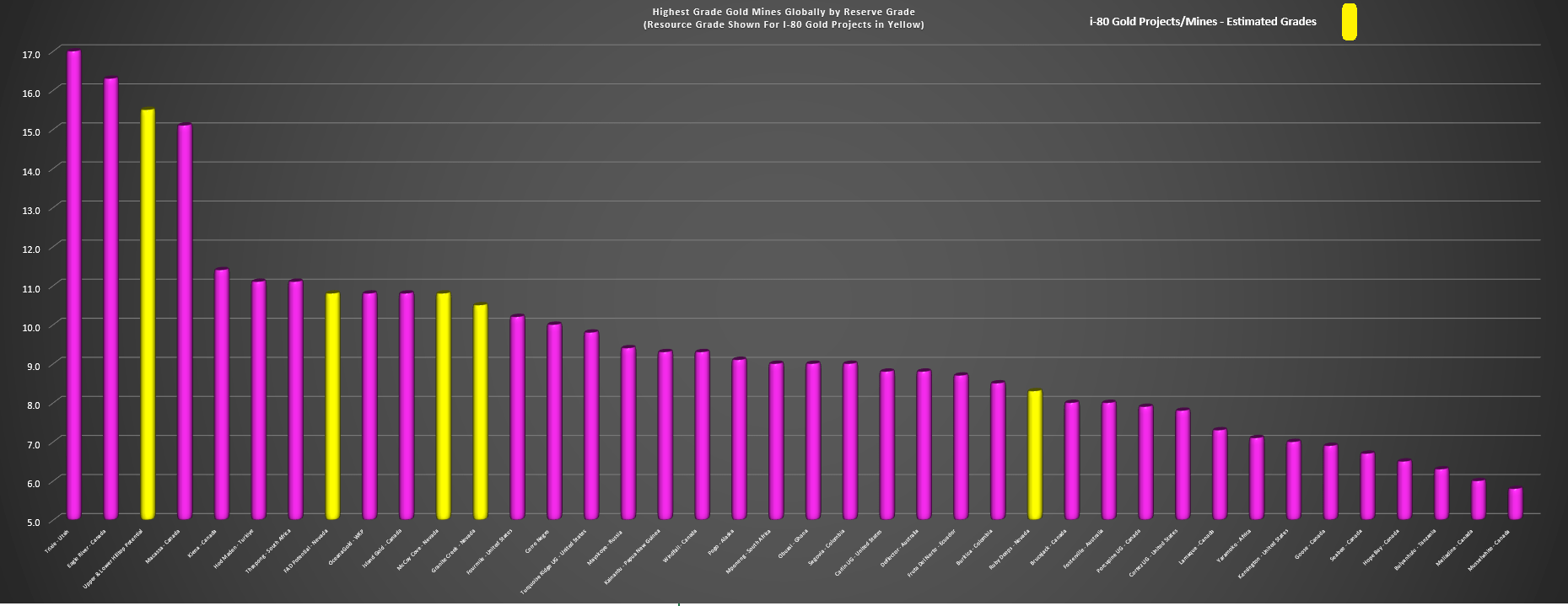

While 2023 was a highly successful year (even if it didn't show up in the share price) with multiple discoveries (Tyche, East Hilltop) on top of a discovery-rich year in 2022 (Upper Hilltop/Lower Hilltop, 428 Zone), investors can expect to see more concrete data from these results in 2024. This is because the company is on track to release economic studies at Granite Creek and Ruby Deeps, as well as maiden resources at Blackjack, FAD, the South Pacific Zone, and the Hilltop zones. These resources should help the company to grow its total resource base to closer to 18 million gold-equivalent ounces company-wide (excluding its silver resources), making it the #2 resource holder in Nevada only behind Nevada Gold Mines, and with a high-grade subset of this resource of 6.0+ million gold-equivalent ounces (Ruby Deeps, FAD, Blackjack, Cove, Granite Creek Underground).

i-80 Gold Resource Size vs. Nevada Peers - Company Website Average Reserve Grades Highest Grade Gold Mines + i-80's Estimated Grades (Projects/Mines) - Company Filings, Author's Chart & Estimates

{kind=link}

{kind=link}

As for additional 2023 achievements, the company has developed 6 levels at its currently operating mine (Granite Creek), secured an oxide ore sale agreement to boost recoveries vs. placing high-grade oxide material on pads, and is in a position to mine first stope ore from South Pacific by summer. Meanwhile, the company's infill drilling has confirmed industry-leading grades at its Cove Mine (planned to be its third spoke), with the average intercept coming in at a grade of 13.0+ grams per ton of gold, above its current resource grade at Cove of ~11.0 grams per ton of gold. In fact, the best intercepts at Cove were among the best drilled sector-wide, with 20.1 meters at 25.4 grams per ton of gold, 36.1 meters at 12.9 grams per ton of gold, and 29.3 meters at 18.9 grams per ton of gold, all ~500 gram-meter intercepts. And like Granite Creek, Cove also has significant upside with the CSD and 2201 zones (not in mine plan), and a massive ~30,000 area land package just north of NGM's Phoenix Mine (gold-copper).

So, what's in store for 2024?

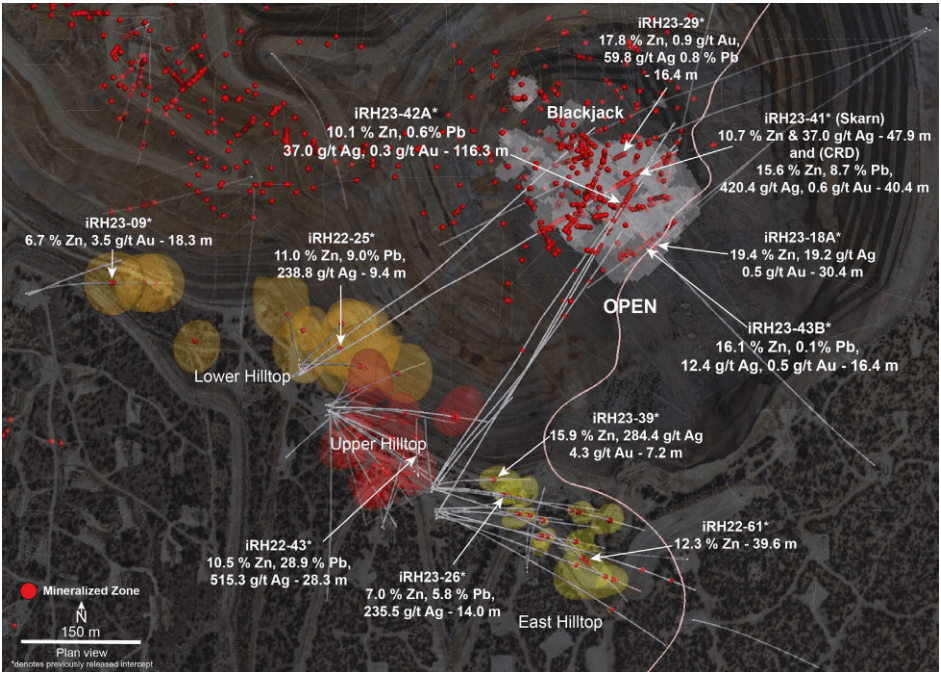

Outside of hoping to make new discoveries in the Hilltop Corridor and potentially adding new high-grade mineralization between Blackjack and East Hilltop, the company expects to make significant progress at its flagship Ruby Hill Property this year with permitting underway for underground development, metallurgical work for the planning of future mining/processing plans, and work that will allow investors to get an idea of the economics here. Notably, early mining of the polymetallic opportunity should include material from the highest-grade Upper Hilltop Zone where gold-equivalent grades were well above 20.0 grams per ton gold-equivalent, meaning that i-80 could be mining one of the highest-grade deposits globally on a gold-equivalent basis by H2 2026. In fact, the best hit at Upper Hilltop was 10.0 meters at 60.2 grams per ton of gold, plus 900 grams per ton of silver, and 16.6% lead/zinc, or a gold-equivalent grade closer to 800 grams per ton.

Hilltop Zones & Blackjack - Company Website

{kind=link}

As for the ultimate opportunity here, i-80's gold second mine (Ruby Hill Polymetallics) could be a 200,000+ ounce per annum producer on a 100% basis at industry-leading costs (assuming 2,500 to 3,000 ton per day throughput rate), and the company should benefit from shared capex here + a cash injection as part of any future joint-venture agreement. This means that i-80 Gold will could be in a far stronger financial position in Q2 of this year, and with its share of Ruby Hill construction fully funded when combined with cash flow from Granite Creek. This is important because the polymetallic opportunity will then provide cash flow to refurbish Lone Tree as part of its Hub & Spoke model, minimizing the need for share dilution. Hence, while the situation may look less favorable today with less than $40 million in cash, I think it makes sense to skate to where the puck will be and how sentiment might shift if a joint-venture agreement is reached vs. focusing on the current cash position relative to future capex.

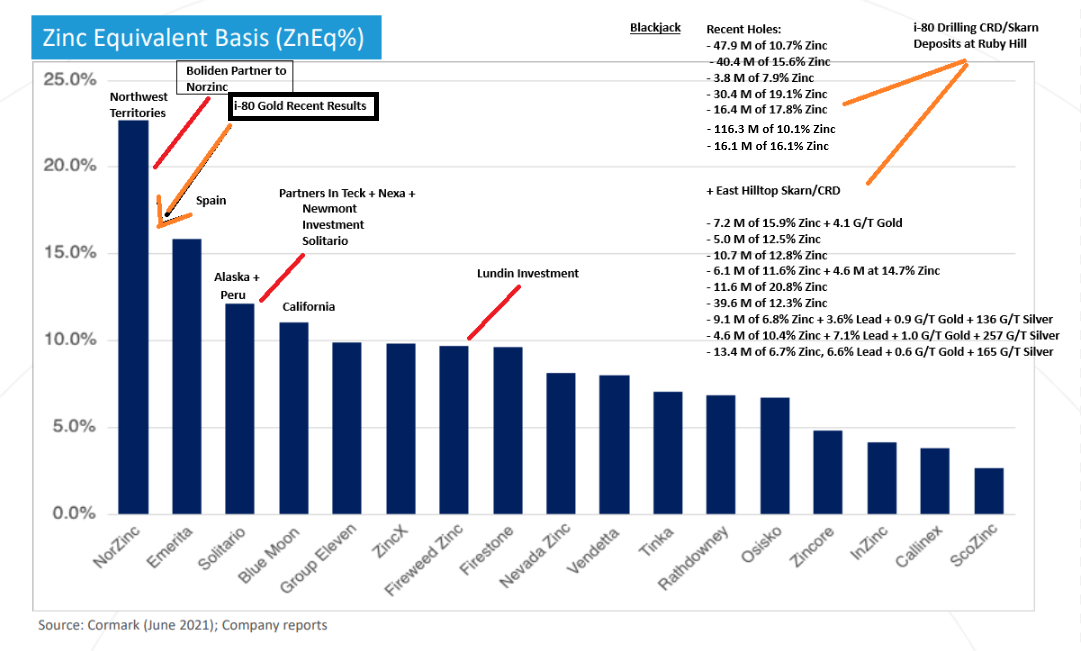

And while on the topic of Ruby Hill, the earlier image shows the company's gold projects and how they have some of the highest grades globally, but Blackjack/Hilltop is also one of the highest-grade assets from a zinc-equivalent standpoint sector-wide as well. In fact, the below chart highlights other assets globally with high zinc values, and I have shown where i-80 Gold could slot in based on its drilling results to date. As we can see, it appears that it would come in at #2 behind Prairie Creek in Northwest Territories from a grade standpoint, and it's in a more favorable jurisdiction than its peers (Nevada vs. Spain, NWT, California, Alaska/Peru), and requires much less upfront capex. So, I don't think there will be any shortage of partners willing to spend a healthy amount to acquire a stake in this asset, as large partners have lined up for similar grade projects in less favorable jurisdictions as shown in the below chart.

Zinc-Equivalent Grade Deposits vs. i-80's East Hilltop CRD/Skarn & Blackjack - Company Filings, NorZinc, Cormark, Author's Notes

{kind=link}

The last point worth noting is that the Granite Creek Project was acquired for ~$60 million in cash shares and contingent value, and the project now looks to have an After-Tax NPV (5%) north of $500 million. Meanwhile, Ruby Hill was acquired for ~$130 million and now looks to have an After-Tax NPV (8%) of up to $1.0 billion. Finally, management did an excellent job selling its last company in a hot market for developers while still retaining significant value with the i-80 assets (Cove, South Arturo 40%). So, given the solid track record of taking care of shareholders in past deals and driving a hard bargain, I am cautiously optimistic on a favorable valuation for Ruby Hill that's significantly above what it paid for this asset. This is important because there have certainly have been some disappointing deals sector-wide over the past 18 months, but I am much less worried about the current deal under negotiation for i-80 at Ruby Hill.

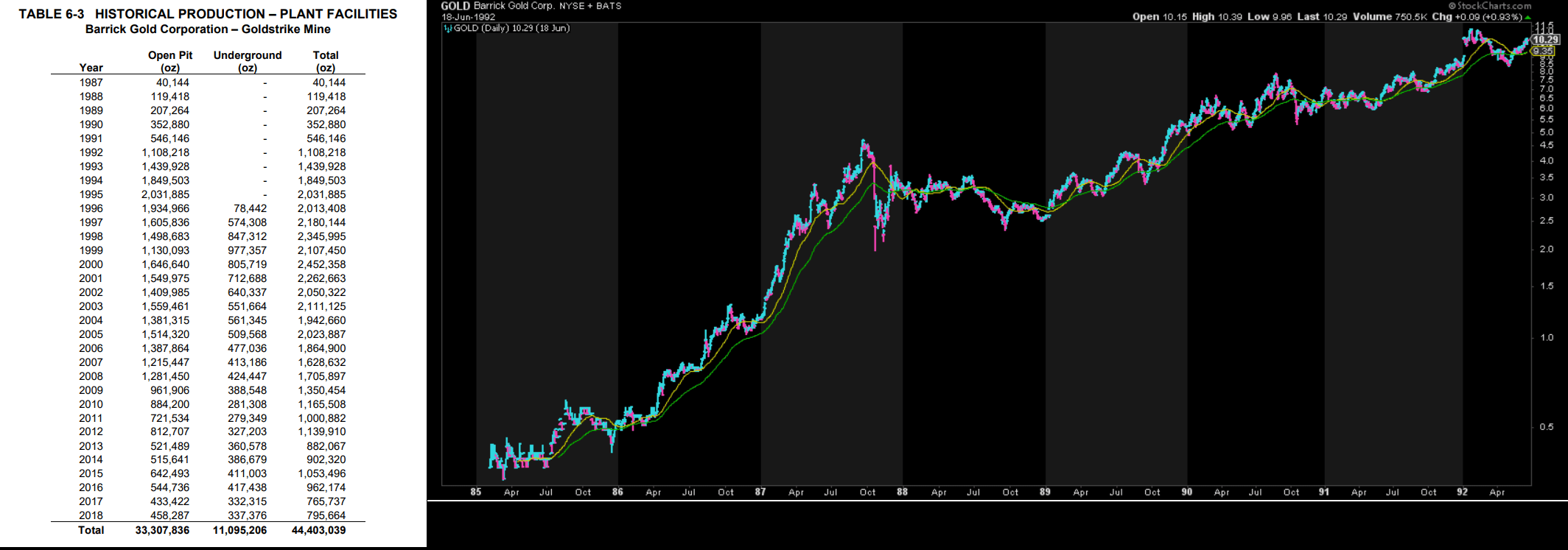

American Barrick Gold Production (Goldstrike) & Share Price Performance (1985-1992) - StockCharts, 2018 Goldstrike TR

{kind=link}

To summarize, there are multiple catalysts on deck for i-80 over the next 18 months, and I would expect the company to grow into an ~85,000 ounce producer in 2025, with a path paved towards becoming a ~380,000 GEO producer in 2028. This is a similar setup to Barrick's rapid growth in the late 1980s following the acquisition of Goldstrike, and Kirkland Lake Gold's industry-leading growth that led both to be significant market outperformers with 2000%+ returns in less than ten years off their cyclical bear market lows. And while there's obviously no guarantee that i-80 Gold can repeat even half of their success, it certainly helps that it has the same unique ingredients (high-grade assets, Tier-1 jurisdictions, considerable exploration success property-wide at all assets), which is why I think the reward/risk is so compelling with the stock sitting well off its all-time highs. In fact, it's a similar setup to when I bought the stock in 2017 at US$6.60 ahead of a multi-year bull market, except i-80 is benefiting from a much more favorable gold market today than where we sat in 2017 below $1,300/oz.

Valuation

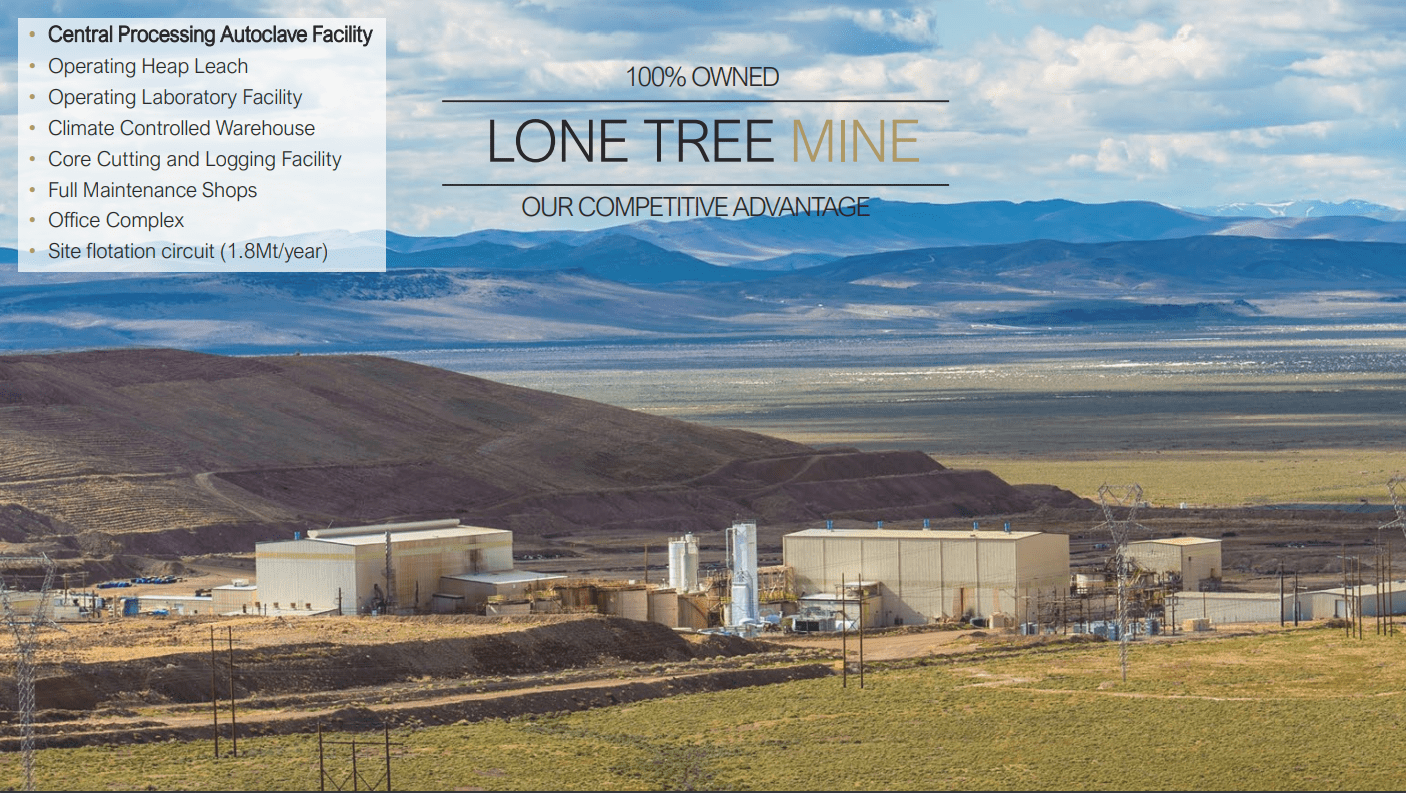

Based on an estimated ~380 million fully diluted shares (year-end 2025) and a share price of US$1.48, i-80 Gold is back to trading at a ~$560 million market cap. This makes it one of the lower capitalization names in the advanced developer space vs. companies like De Grey Mining ( DGMLF ), New Found Gold Corp. ( NFGC ), Snowline ( SNWGF ) and Osisko Mining that trade at fully-diluted market caps between ~$800 million and ~$1.4 billion. Notably, the divergence is despite the fact that i-80 is arguably the most advanced along the Lassonde Curve within the peer group, with mining already underway on one of its assets and is ongoing work to get to Feasibility level on its other three assets, and the fact that it has sunk costs worth more than the entire capitalization of its peers with an autoclave, CIL plants, a flotation circuit, heap leach facilities, and an assay lab/gold refinery as well as a rail siding to provide it access to the Northern Nevada Railway.

Lone Tree Site - Company Website

{kind=link}

This distinction is important not only from a path to cash flow standpoint given that one of i-80's operations will be cash-flow positive this year (vs. nearly every other developer that is not producing any gold and can't use cash flow towards development), but it's also important from a capital expenditures standpoint. The reason is that while the above peer group will need to spend an average of ~$1.0 billion to get into production (drilling, studies, engineering, construction), upfront capex for i-80 is much more modest considering it already has processing infrastructure in place that can be converted/refurbished. In fact, its Granite Creek OP Project has a modest upfront capex bill to become a high-margin ~100,000 ounce per annum operation and its polymetallic opportunity at Ruby Hill also has relatively low capex with underground development and the conversion of its CIL plant to a flotation plant.

Finally, it's worth noting that this capex opportunity looks like it could be shared with another larger operator with the news that i-80 Gold may be able to lock up a minority joint-venture [JV] partner at the asset. If successful, this would reduce i-80 Gold's share of its capex to bring a polymetallic mine into production to less than $150 million (assumes 60/40 JV) while also speeding up development and providing cash flow to fund its autoclave refurbishment post-2026. Hence, i-80 should be in the unique position of having two sources of cash flow by H2-2026 to fund the larger ~$260 million autoclave refurbishment and underground development at Cove. This is a clear advantage (funding operations/construction with mix of cash flow, debt, proceeds from joint-venture agreement) vs. having to rely on solely debt, equity or streams to complete its largest project like nearly all of its development-stage peers.

So, what's a fair value for the stock?

Based on an estimated net asset value of ~$1.48 billion using 8% discount rates (5% for Granite Creek) at an $1,875/oz gold price assumption, I see a fair value for i-80 Gold Corp. stock of US$3.90 to its 2-year target price based on ~380 million fully diluted shares. This assumes a joint-venture partner is secured in a timely manner and the receipt of underground mining permits at Ruby Hill. However, longer term I see the opportunity for i-80 Gold to grow into a $2.0 billion to $2.5 billion market cap company if it can succeed in becoming a ~400,000 GEO per annum producer in Nevada, with closer to a $3.0 billion market cap if it can reach the 500,000 ounce production mark.

The good news is that its vast resource base across its assets means that i-80 Gold already has the projects in place to potentially grow past its initial target of 400,000 GEOs later this decade, with Granite Creek OP being one of the highest-grade open-pit assets in the Great Basin next to Long Canyon (*). And it's worth noting that there looks to be upside the current pit design longer-term at Granite Creek OP with drilling in 2021 yielding high-grade oxide intercepts like 7.5 meters at 3.17 grams per tonne of gold and 51.1 meters at 6.8 grams per tonne of gold below the historic CX Pit. Hence, there looks to be potential mine life upside at Granite Creek Open Pit on top of a potential ~1.0 million ounce reserve base at this less discussed asset.

In summary, with a much lower P/NAV multiple despite a more favorable position on the Lassonde Curve (closer to cash flows), i-80 is a clear standout on valuation among its developer peers.

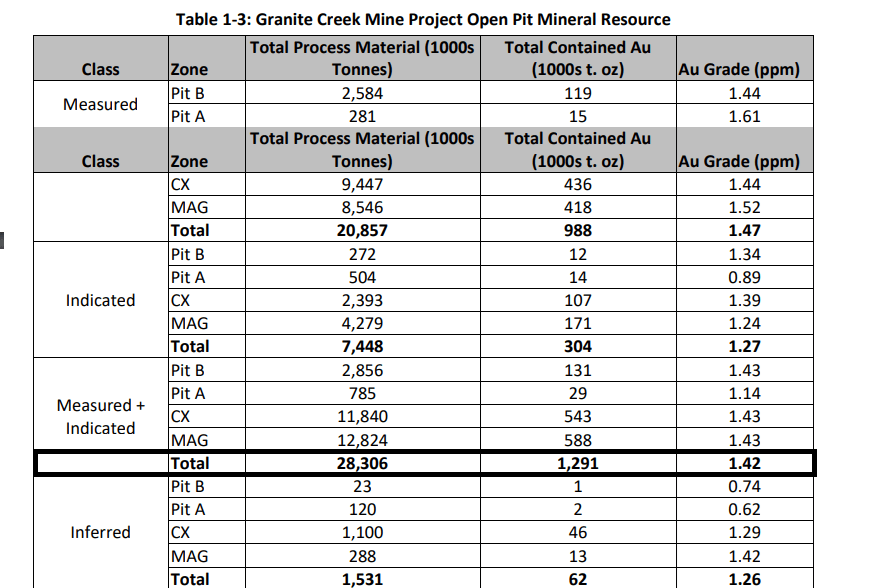

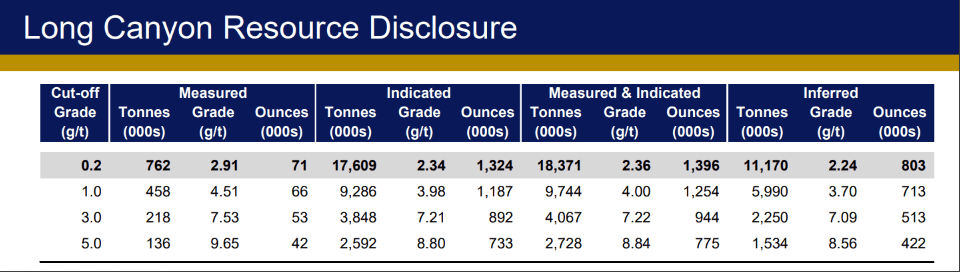

Granite Creek Open Pit Resource - Company Filings Long Canyon High-Grade Open Pit Resource - Fronteer Gold Presentation

{kind=link}

{kind=link}

(*) Long Canyon was acquired through the acquisition of Fronteer Gold by Newmont for over $2.0 billion, suggesting that Granite Creek OP is another underappreciated asset in i-80's portfolio with ~1.3 million M&I ounces at a grade of 1.42 grams per tonne of gold, with high-grade assets amenable to heap-leaching being highly desirable.

Summary

As noted in a previous update, i-80 Gold may have underperformed its peers in 2023 after huge outperformance the previous two years (2021/2022), but this was largely due to digesting a higher share count (Paycore acquisition + equity raise), and worries about the company's ability to fund its ambitious growth plans. However, the company enters 2024 in a much more favorable position with the possibility of securing a JV partner at Ruby Hill. These cash injections from a future deal could allow i-80 to accelerate Ruby Hill development, accelerate portfolio-wide drilling, and ultimately de-risk its path to becoming a mid-tier producer in Nevada. Simultaneously, 2024 will see a significant increase in annual cash flow generation/gold production as i-80 starts mining at the South Pacific Zone (stope ore expected next quarter), and a stronger balance sheet combined with discovery/definition drilling/higher production will ultimately lead to growth in production, resources/reserves, and net asset value per share.

Cove Project Mineralization - i-80 Gold Website

{kind=link}

As for the bigger picture, i-80 has some of the best undeveloped assets in a top-ranked jurisdiction with well above averages, and I would expect a Tier-1 jurisdiction high-grade producer to command a premium multiple given the uncertainty in other jurisdictions and dearth of Tier-1 only producers in the sector. This unique setup lays a path to significant share upside for i-80 Gold as production grows (similar to American Barrick in the 1980s and Kirkland Lake Gold in the 2010s) and I would ultimately not be surprised to see the stock trade above US$5.00 longer-term.

In summary, I continue to see i-80 Gold as one of the best ways to get gold exposure sector-wide and I see this pullback to US$1.47 as a gift, with the stock trading at barely 0.30x P/NAV.

For further details see:

i-80 Gold: A Transformational Year On Deck