IAUX - i-80 Gold: Cove Continues To Deliver

2023-07-28 14:16:59 ET

Summary

- i-80 Gold Corp. has experienced a decline in its stock price due to sector-wide selling pressure and recent dilution from a financing round.

- However, this has not changed the story, and with a catalyst-rich H2 ahead, I would be surprised if the current stock price weakness persisted much longer.

- Given i-80's Gold unrivaled growth story with multiple high-grade assets in the top-ranked mining jurisdiction, I see the stock as a steal below US$2.00 trading at below 0.50x P/NAV.

It's been a rollercoaster ride of a year for investors in gold juniors ( GDXJ ), with the sector briefly up over 15% to start the year before retreating back into negative territory despite minimal erosion in the gold price and the highest three-year average gold price on record ($1,850/oz). This is undoubtedly discouraging for some investors and while i-80 Gold Corp. ( IAUX ) managed bucked the trend in a big way with outperformance in 2021 and 2022, 2023 has seen the stock succumb to the sector-wide selling pressure.

The loss of momentum is partially related to the Paycore Minerals acquisition, which often weighs on the share price of suitors in the short term, in addition to a recent small equity financing. That said, I don't see either of these changing the story in a negative way (in fact, the company paid a very attractive price for Paycore if it can confirm or build on the FAD resource), and the stock is now trading at its most attractive valuation levels since its March 2023 lows before a sharp 35% rally. Let's take a closer look below:

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Cove Drilling

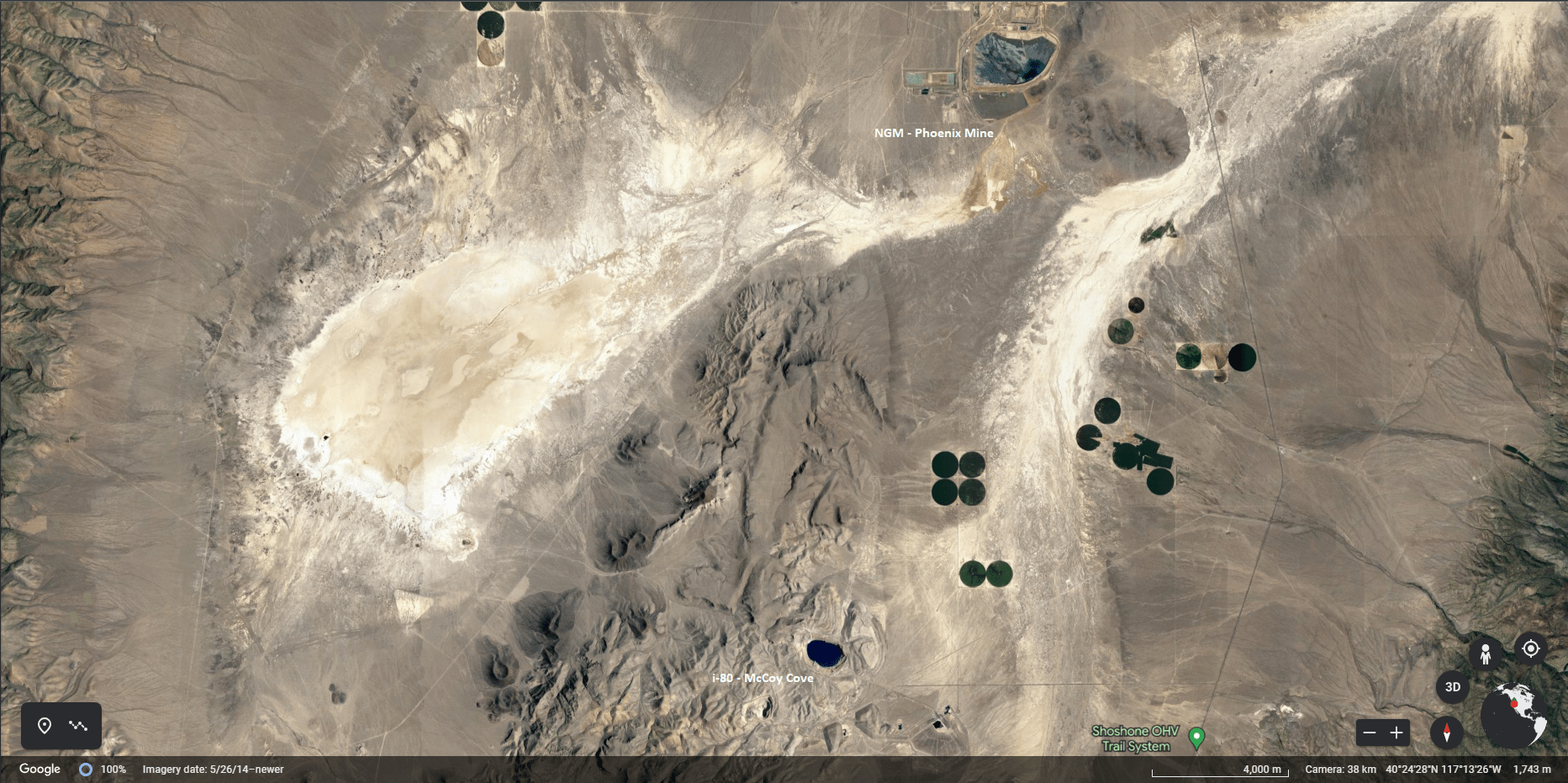

While it's been a quieter start to the year, with i-80 Gold working to integrate its new FAD Property and busy working on test Mining at Granite Creek and a new economic study after a focus on drilling last year, it's been a busy year thus far from the company's Cove Project in Lander County (Battle Mountain-Eureka Trend), Nevada, just south of Nevada Gold Mines' Phoenix Mine. This is a past-producing asset (Echo Bay produced ~3.4 million ounces of gold and over 110 million ounces of silver, with the bulk of this coming from the Cove Mine). However, the property is currently i-80's highest-grade asset and expected to be the third spoke in its Hub & Spoke Gold Model, with a resource base of ~1.6 million ounces of gold at 10.9 grams per tonne of gold. If in production today, this would be one of the top-10 highest-grade gold mines globally, and infill drilling this year has confirmed the robust grades here, with grades exceeding my expectations over impressive widths.

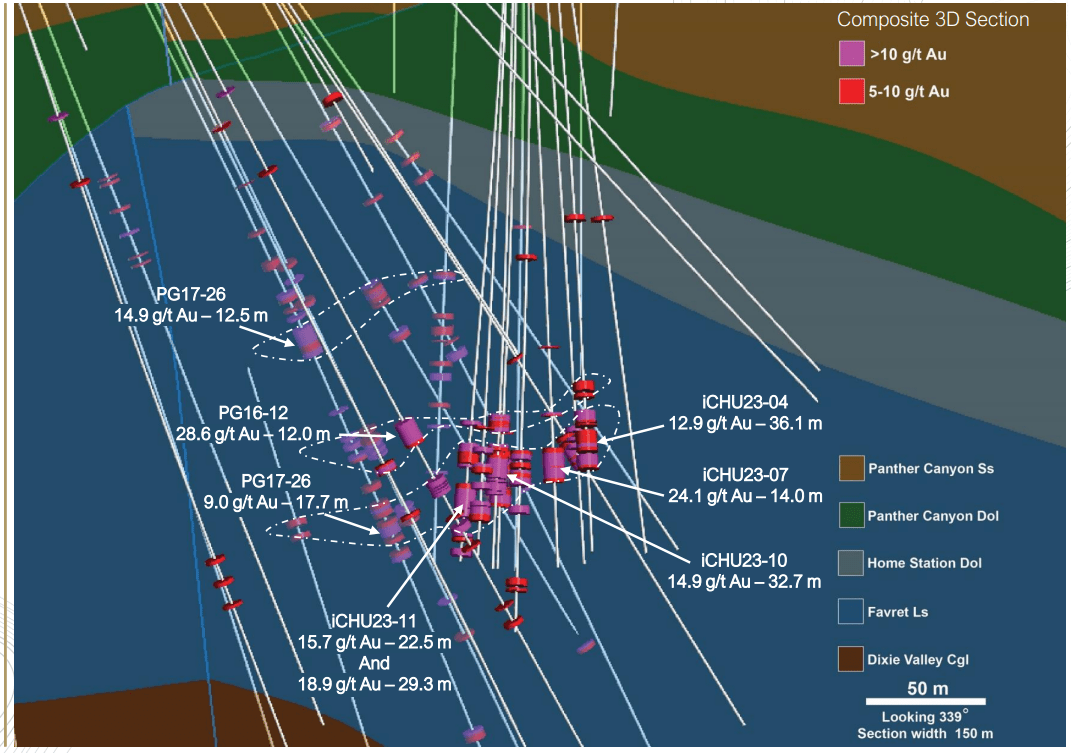

Some highlight intercepts reported to date are as follows:

- 6.0 meters at 13.0 grams per tonne of gold

- 36.1 meters at 12.9 grams per tonne of gold

- 14.0 meters at 24.1 grams per tonne of gold

- 22.8 meters at 9.6 grams per tonne of gold

- 32.7 meters at 14.9 grams per tonne of gold

- 22.5 meters at 15.7 grams per tonne of gold

- 29.3 meters at 18.9 grams per tonne of gold

{kind=link}

Not only are the above intercepts among some of the best intercepts drilled sector-wide at North American gold projects, but some of these holes rival the best intercepts out of the sector's largest joint-venture, Nevada Gold Mines, which has multiple mines and complexes in Nevada. In fact, if we compare these hits to a sample of some of the best intercepts reported by Nevada Gold Mines in the past 18 months, Cove is nearly on par with these other mines/deposits from a grade and width standpoint, but the difference is that this is in a small-scale drill program by a ~$740 million company vs. hits from multiples deposits and mines at a joint venture with a ~$70 billion company in the case of Nevada Gold Mines. For illustration, these are some of the best hits reported by Barrick Gold ( GOLD ), the majority owner at NGM.

- 31.7 meters at 33.6 grams per tonne of gold (Fourmile)

- 18.0 meters at 29.6 grams per tonne of gold (Fourmile)

- 10.0 meters at 28.0 grams per tonne of gold (Turquoise Ridge)

- 34 meters at 12.9 grams per tonne of gold (Turquoise Ridge)

- 27.4 meters at 19.6 grams per tonne of gold (North Leeville)

- 20.1 meters at 9.6 grams per tonne of gold (CHUG)

- 37.8 meters at 16.0 grams per tonne of gold (North Turf)

- 23.9 meters at 15.0 grams per tonne of gold (North Turf)

- 38.3 meters at 18.5 grams per tonne of gold (North Turf)

- 27.7 meters at 11.5 grams per tonne of gold [REN].

To be clear, this is not to suggest that i-80 Gold's market cap should rival that of Nevada Gold Mines, and obviously Nevada Gold Mines and the companies that share this massive asset of gold mines in Nevada have a far greater production profile than i-80 Gold.

That said, the caliber of i-80's drill intercepts across its portfolio at Ruby Deeps, Granite Creek, and Cove comes close to matching what we're seeing out of Nevada Gold Mines, a joint-venture with a far larger land package and exploration budget. And Cove is certainly the one putting up the most consistent and high-grade intercepts, which have mostly beat its resource grade and confirm that this is truly a world-class asset. And the latter point was confirmed by a PEA done in 2021, which highlighted modest upfront capex and a NPV (5%) to Initial Capex Ratio above 3.5 to 1.0 using a conservative $1,700/oz gold price.

{kind=link}

Obviously, we have seen inflation since 2021 and Preliminary Economic Assessments often understate the actual costs of mining and developing an asset. That said, the mine plan excluded ~640,000 ounces at Helen, Gap and Cove South Deep and there's the possibility to build on the resource with drilling between the Gap and Cove South Deep Zone, with the Gap deposit also remaining open down-plunge to the southeast. So, if we assume an ultimate mineable reserve of ~1.20 million ounces (71% conversion rate on total ounces in resource inventory), more conservative mining costs ($129.00/ton), more conservative processing and transportation costs, more conservative recovery rates (82.0% blended recovery rate for autoclave/roaster), and ~$110 million in upfront capex vs. ~$82 million in the 2021 PEA, we arrive at an NPV (5%) of ~$360 million for Cove at an $1,850/oz gold price. This represents $0.96 per share in value to i-80 Gold or half its fully-diluted market cap from this single asset.

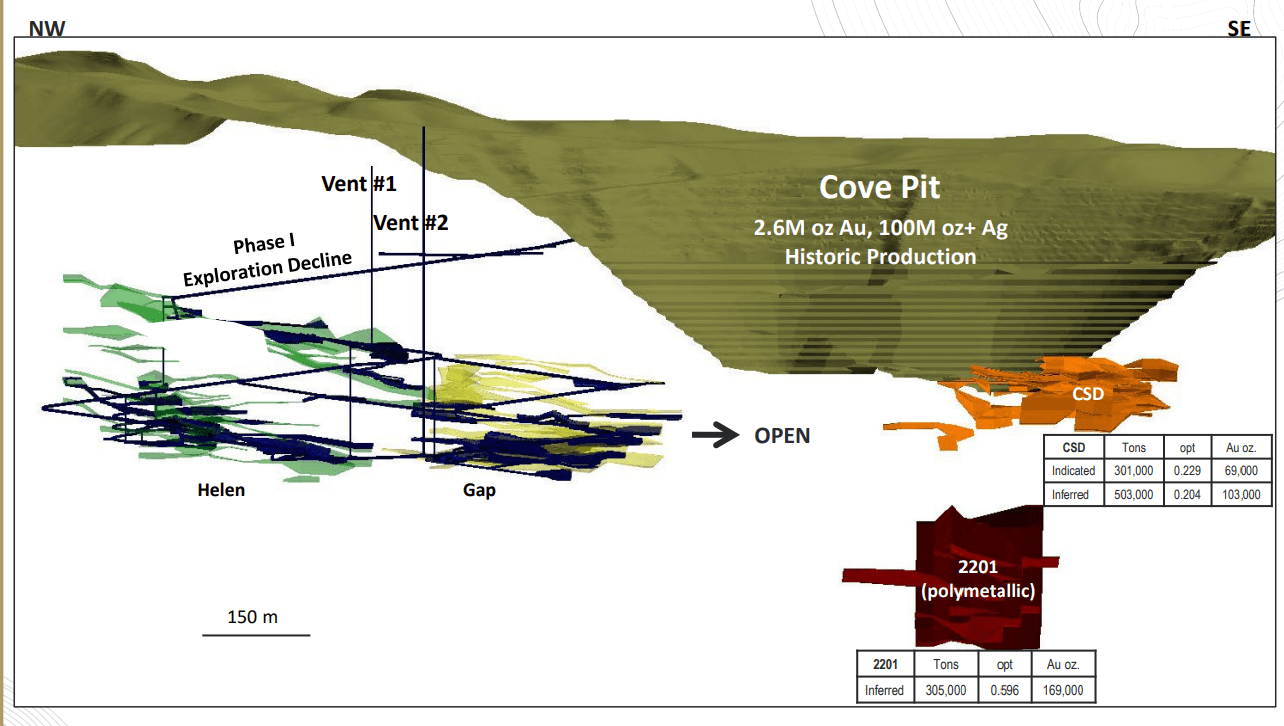

Obviously it's still early days here, and a 40,000-meter drill program is underway to tighten up spacing at Cove while a Phase 1 Underground decline is nearing completion. However, this is an asset in i-80's portfolio that's received little focus that could produce ~100,000+ ounces per annum (1,350 ton per day average mining rate) at all-in sustaining costs below $1,150/oz even after incorporating inflationary pressures. So, this is certainly an asset worth highlighting, and it's extremely encouraging to see the results out of this deposit in confirmatory drilling. Plus, as shown below, there remains meaningful upside at McCoy Cove with multiple styles of mineralization on the property (Carlin-style that's also rich in silver, polymetallic sheet veins, carbonate replacement, skarn), but the focus to date is on Helen and Gap, which has already highlighted a robust mine plan, and potentially the CSD Gap transition zone beneath the pit in future drilling.

Cove Pit & Helen, Gaop, CSD and 2201 Zones (Company Presentation)

{kind=link}

Recent Financing & Liquidity

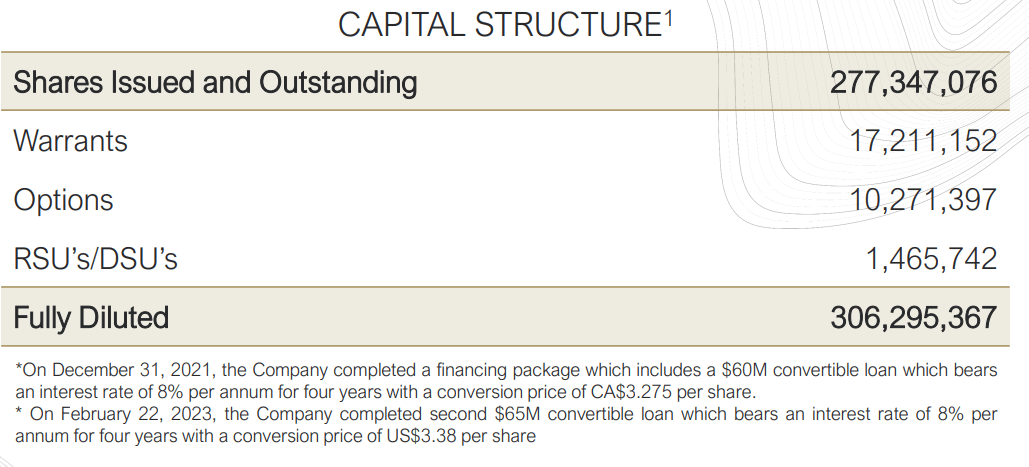

i-80 Gold announced earlier this month that it would be raising ~$24 million through the issuance of ~11.9 million shares at an average price of US$2.05. Understandably, share dilution is rarely welcomed by shareholders and many investors were unhappy with the deal. However, I believe the deal was well structured given the difficult environment to raise capital, especially relative to other developers and producers. In fact, i-80 Gold raised capital with minimal dilution (~3.4% dilution vs. an estimated ~350 million fully diluted shares pre-deal) without any warrants attached and at a price that was over 35% above last year's lows.

i-80 Gold Capital Structure (Pre Recent Financing) (Company Website)

{kind=link}

If we compare this to other advanced developers and producers, Guanajuato Silver ( GSVRF ) recently raised capital with significant dilution with a full warrant attached, a very ugly deal for a producer that translated to over 12% share dilution. Meanwhile, another advanced developer raised ~$75 million earlier this year with a half warrant at barely 30% off last year's lows, a much less attractive deal that resulted in over 10% share dilution.

So, while the recent share dilution by i-80 was unfortunate and it certainly would have been nice to raise into a better environment, I think the deal made sense to ensure that the company was in a better positioned when negotiating any new deals with lenders and to pad its balance sheet ahead of the planned ramp up in production from Granite Creek later this year.

When it comes to funding future operations, i-80 Gold is expected to have ~$43 million in cash post-closing of its recent financing, but it also has an available accordion with Orion Mine Finance for up to $100 million, and it has the potential for ~$45 million in proceeds if warrants are exercised at ~$2.48 and ~$2.76. This translates to nearly $200 million in total liquidity. In addition, while the company may not be generating any meaningful cash flow with small-scale mining at the Ogee Zone (Granite Creek Underground) and residual leaching, the company should see a significant increase in gold production next year to ~60,000 ounces with additional tons to be pulled out of the adjacent South Pacific Zone to push Granite Creek mine production closer to 700 tons per day. Hence, for the first time since going public, i-80 Gold will start generating a decent amount of cash flow next year to help fund company-wide exploration and mine development.

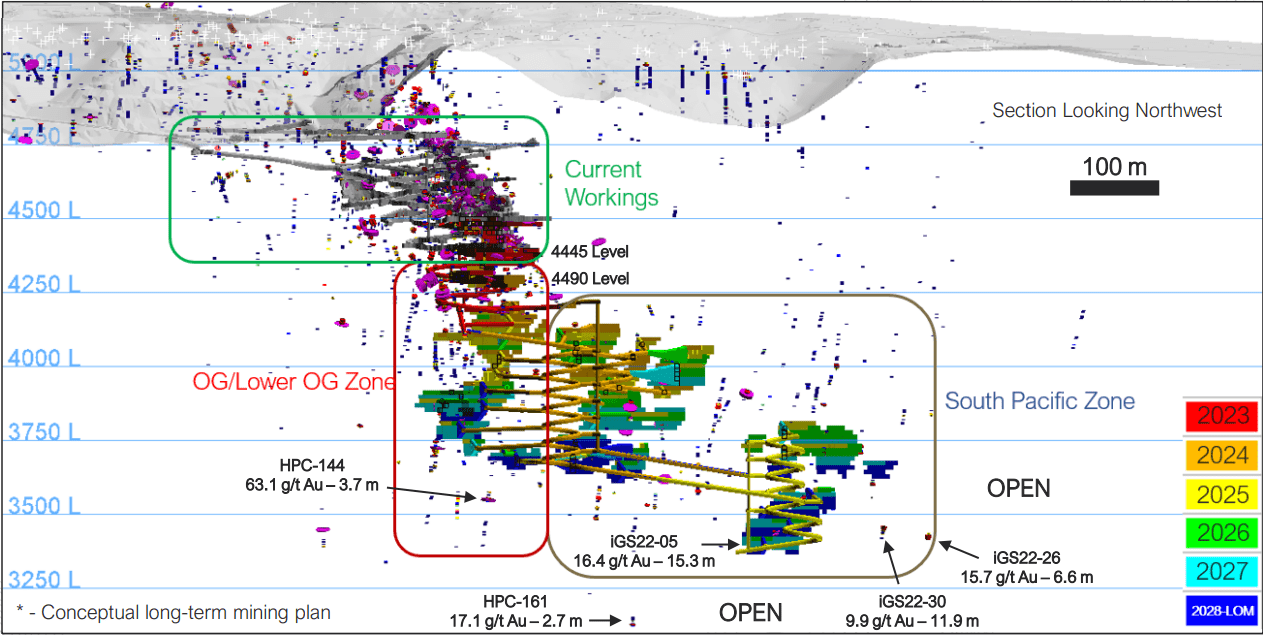

Current Mining Areas & South Pacific Zone (Future Mining Areas) (Company Website)

{kind=link}

To summarize, while the recent dilution was disappointing, it was minimal and without warrants attached, and I have no issue with the recent financing. And with a much higher gold price (~$1,900/oz) increasing company-wide gold production with development work underway into the South Pacific Zone (good rock quality, high-grades, significant resource upside), and the potential to sequence its high-grade polymetallic opportunity with a low capex CIL Mill conversion ahead of the Hub & Spoke Gold model (Cove, Granite Creek, Ruby Deeps), I see i-80 Gold as much better positioned to execute its ambitious growth plans from a financing standpoint than where it was when it went public.

Other Recent Developments

As for recent developments, i-80 Gold noted in its most recent update that production at Granite Creek is going quite well in its early days, with improving mining and development rates at the Ogee Zone and positive grade reconciliation in the first ~10,600 tonnes mined on the 4445 Level, and the first ~10,900 tonnes mined on the 4490 Level. These two fully-mined levels yielded an average grade of ~12.6 grams per tonne of gold, above my expectations, above the resource grade and yielded a total of ~8,700 ounces of gold, a great start to mining at this high-grade asset that lies just southwest of the massive Turquoise Ridge Complex. For those unfamiliar, Granite Creek has a processing agreement to toll-mill ore from Granite Creek at the nearby Sage Autoclave, enabling it to generate cash flow while it works to develop its other mines ahead of an eventual restart of its own autoclave at its Lone Tree Facility.

Granite Creek Mine & Turquoise Ridge Complex/Twin Creeks (Company Presentation)

{kind=link}

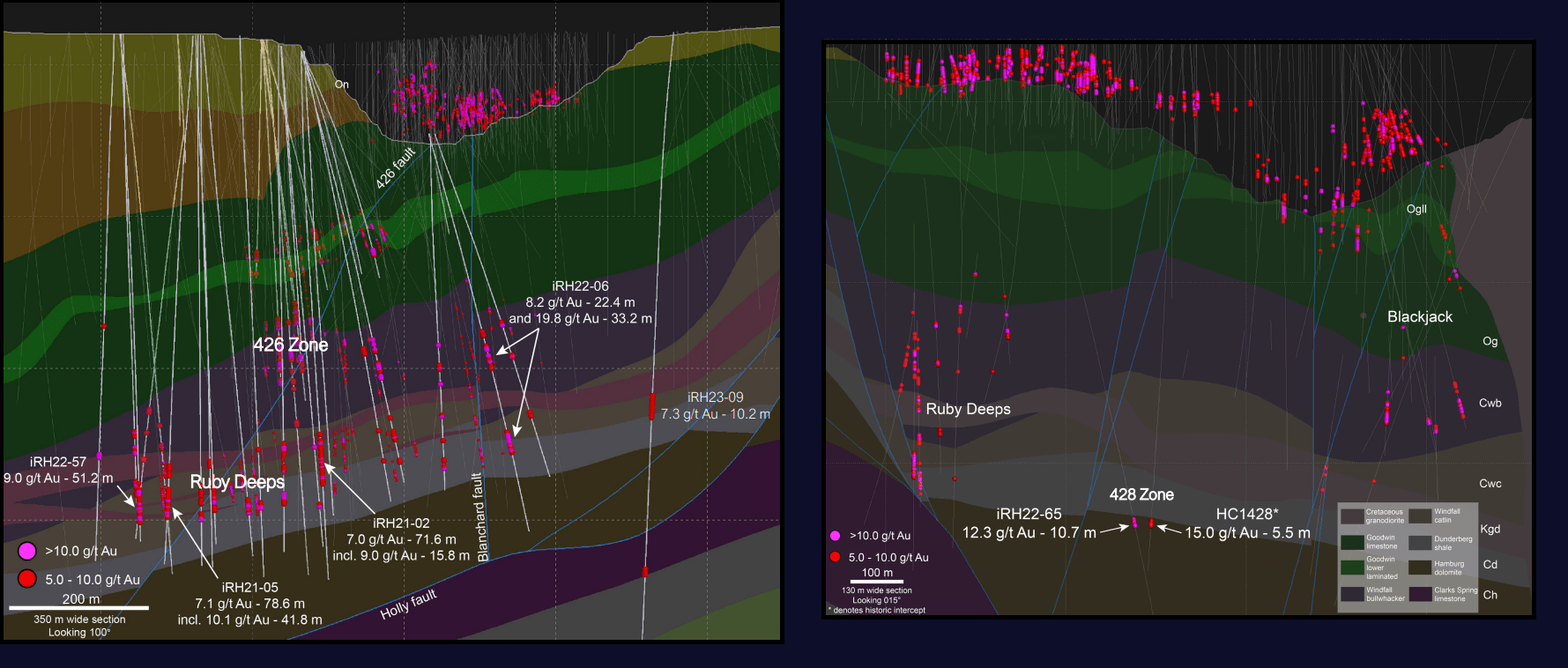

In other developments, Ruby Deeps continues to deliver from a grade standpoint and the resource not only looks set to grow with major step-outs to the south (IRH23-09, which hit 10.2 meters at 7.3 grams per tonne of gold) in close proximity to the Hilltop Fault, in addition to 10.7 meters at 12.3 grams per tonne of gold east of the main Ruby Deeps area near the Blanchard Fault in the newly discovered 428 Zone. In addition, drilling over the past 15 months has continued to intersected wide high-grade intersections that are well above the average grade of ~6.0 grams per tonne of gold at Ruby Deeps (~1.6 million ounce resource base), suggesting that we could see a 20% plus increase in grades that would dramatically improve the average grade of this asset. And with competent rock quality and shared development, this remains an exciting opportunity for i-80 Gold, in addition to its recent polymetallic discoveries and the new high-grade South Pacific Zone discovery made in 2021.

{kind=link}

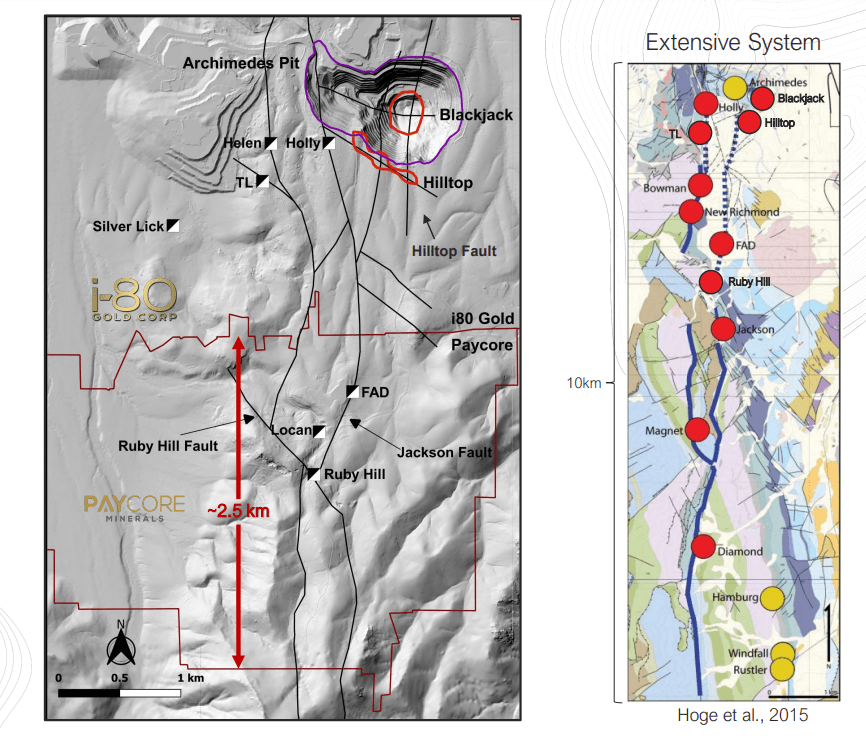

Elsewhere, at Hilltop, the company received approval to drill test the Hilltop Corridor, a mostly untested ~3 kilometer area primarily under alluvial cover that lies south of the Archimedes Pit and its recent discoveries at Upper Hilltop, Lower Hilltop, West Hilltop, and East Hilltop. This is a very exciting development with multiple rigs currently drilling at its flagship Ruby Hill Project and FAD, which is a deposit open for expansion with a historic resource of ~3.6 million tons at ~13.0 grams per ton gold-equivalent, with the potential for i-80 Gold to prove up over 1.5 million GEOs at FAD alone. Notably, there is a major target (4H) in this corridor that remains untested, in addition to high-grade intercepts at depth by previous operators that included an intercept of ~5.8 meters at ~8.0 grams per ton gold-equivalent.

Hilltop, FAD, & Hilltop Corridor + Past Producing Gold & Polymetallic Mines (Company Presentation, Hoge et al. 2015)

{kind=link}

Given the slower first half of the year from a news-flow standpoint due to working to close the Paycore deal and working on additional geophysical surveys to better define targets along the Hilltop Corridor and FAD, it should be a very busy next nine months for the company. And with maiden resources expected at Blackjack, Hilltop, FAD and the South Pacific Zone as well as an updated resource at Ruby Deeps (incorporating higher grades), an economic study at Ruby Deeps, an economic study and reserve declaration at Granite Creek and results from extensive drilling across multiple properties, I would expect it to be a very catalyst rich H2. So, while sentiment is in the gutter, I expect it to swing back positively in short order with several positive developments on the horizon.

Valuation

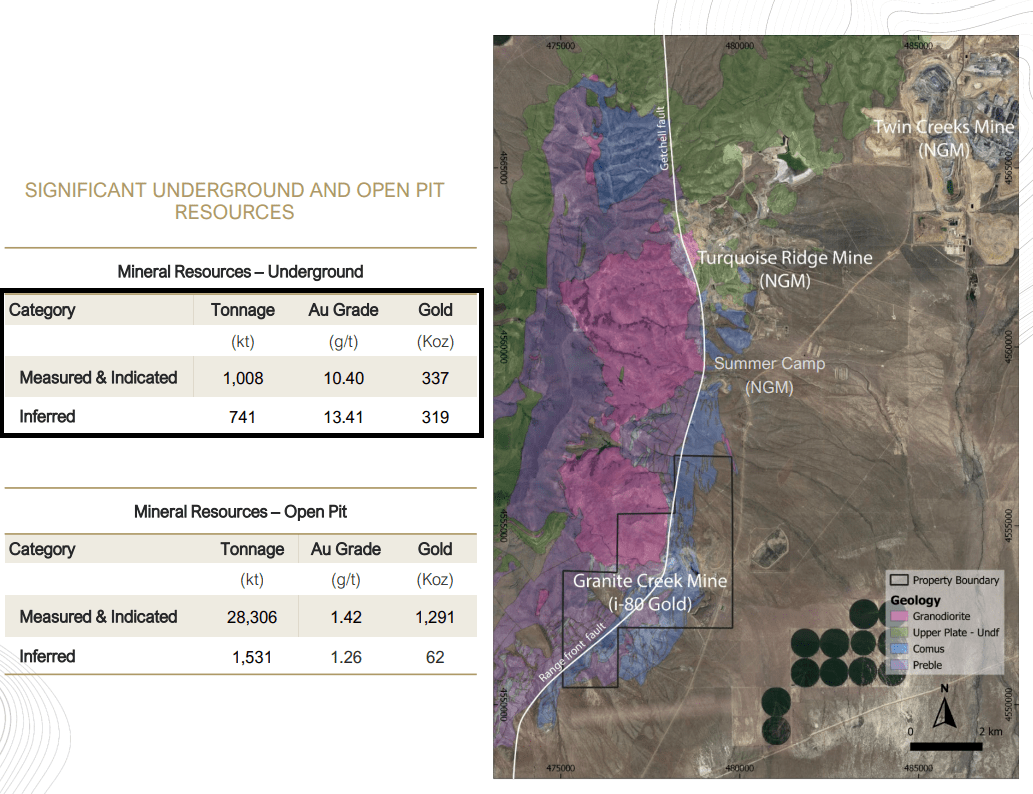

Based on an estimated ~375 million fully diluted shares and a share price of US$1.98, i-80 Gold trades at a market cap of ~$743 million. This valuation continues to leave i-80 Gold as one of the cheapest producers on a per ounce basis in Tier-1 ranked jurisdictions, with i-80 Gold trading at ~$85/ounce on mineral resources based on an ~8.7 million ounce resource (excludes ~5.9 million lower-grade ounces at Mineral Point). However, this per ounce valuation figure does not do the company justice given that it excludes several key new discoveries and deposits that have not made it into mineral resource inventory yet but should be in the nine to eighteen months. These opportunities are:

- FAD (Ruby Hill Project) - CRD mineralization south of previous Ruby Hill Property boundary

- South Pacific Zone (Granite Creek Mine) - high-grade gold mineralization north of underground mine workings

- Hilltop Discovery (Ruby Hill Project) - high-grade CRD mineralization immediately south of the Archimedes Pit

- Blackjack (Ruby Hill Project) - high-grade polymetallic skarn mineralization below the Archimedes Pit.

While it's difficult to estimate how much resource growth i-80 will see in the company's resource update at year-end 2023, as much depends on the timely receipt of assays and adequate drill spacing in some zones, I would not be surprised to see i-80 Gold's mineral resource inventory grow to 18.0 million gold-equivalent ounces [GEOs] by year-end or ~12.0 million ounces excluding lower-grade ounces at Mineral Point with the combined additions from the South Pacific Zone, a portion of Hilltop, Blackjack, FAD, and the potential for a larger and higher grade deposit at Ruby Deeps (potential for grade to improve to 7.5+ grams per ton of gold). And assuming this is the case with resource growth to 12.0 tp 12.5 million GEOs (excluding Mineral Point), i-80's valuation per ounce would decline to $60 - $62/ounce on a fully diluted basis. As the chart below highlights, this is well below where Tier-1 jurisdictions ounces have been valued over the past few years, and Nevada should arguably get a premium for being the #1 ranked mining jurisdiction among these Tier-1 jurisdictions.

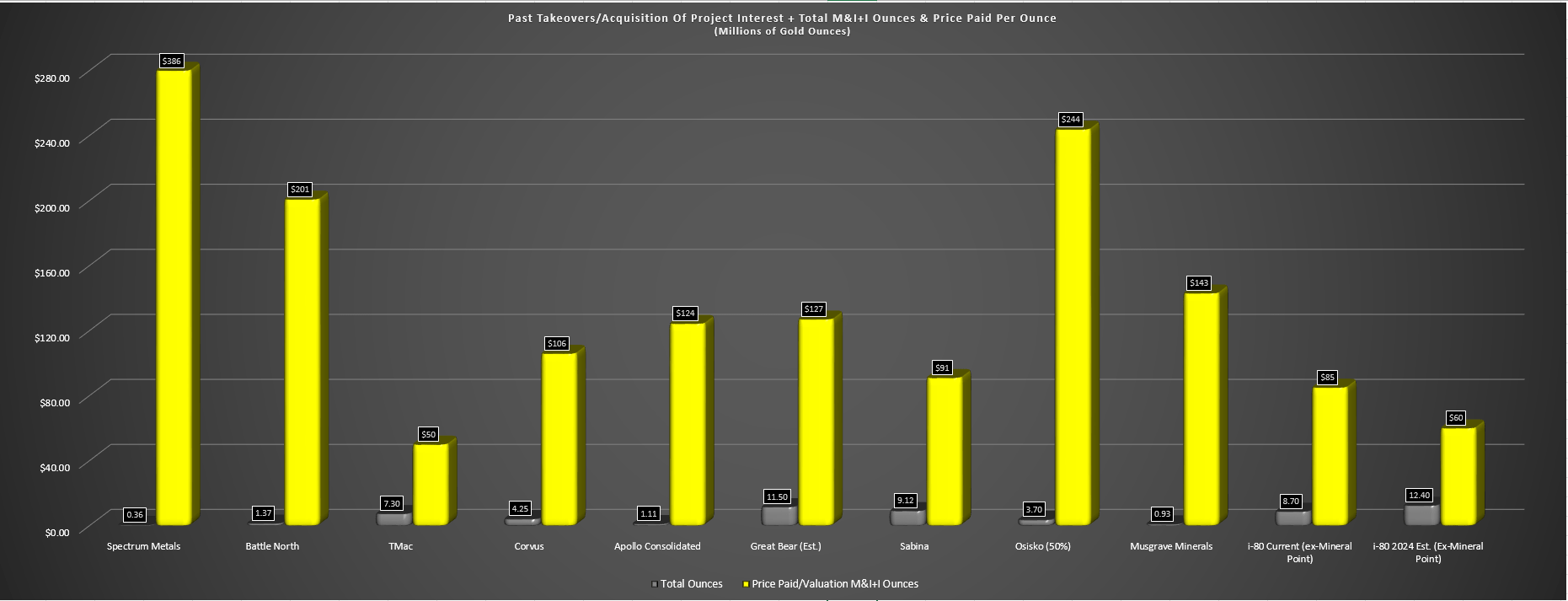

Past Takeovers/Acquisition Of Project Interest & Total Resource Ounces + Price Paid Per Ounce vs. i-80 Gold (Company Filings, Author's Chart & Estimates)

{kind=link}

Digging into the chart above, the most recent acquisition has seen Ramelius Resources ( RMLRF ) bid up for high-grade ounces in the Murchison Province of Western Australia with Musgrave, offering ~$143/oz to acquire the company with a sub 1.0 million ounce resource base. Elsewhere, Gold Fields ( GFI ) paid ~$244/oz to scoop up a 50% interest in the high-grade Windfall Project in James Bay, Quebec, Kinross ( KGC ) paid ~$127/oz to acquire Great Bear in Red Lake Ontario (assuming at least 11.5 million resource ounces are proven up), and in the Beatty District of Nevada, AngloGold ( AU ) paid ~$106/oz for Corvus Gold. The key theme is that high-grade ounces have typically commanded a premium in Tier-1 jurisdictions over the past several years, but even excluding solely high-grade resources, suitors have valued the average resource ounce in Tier-1 jurisdictions (Canada, United States, Australia) at $140/oz.

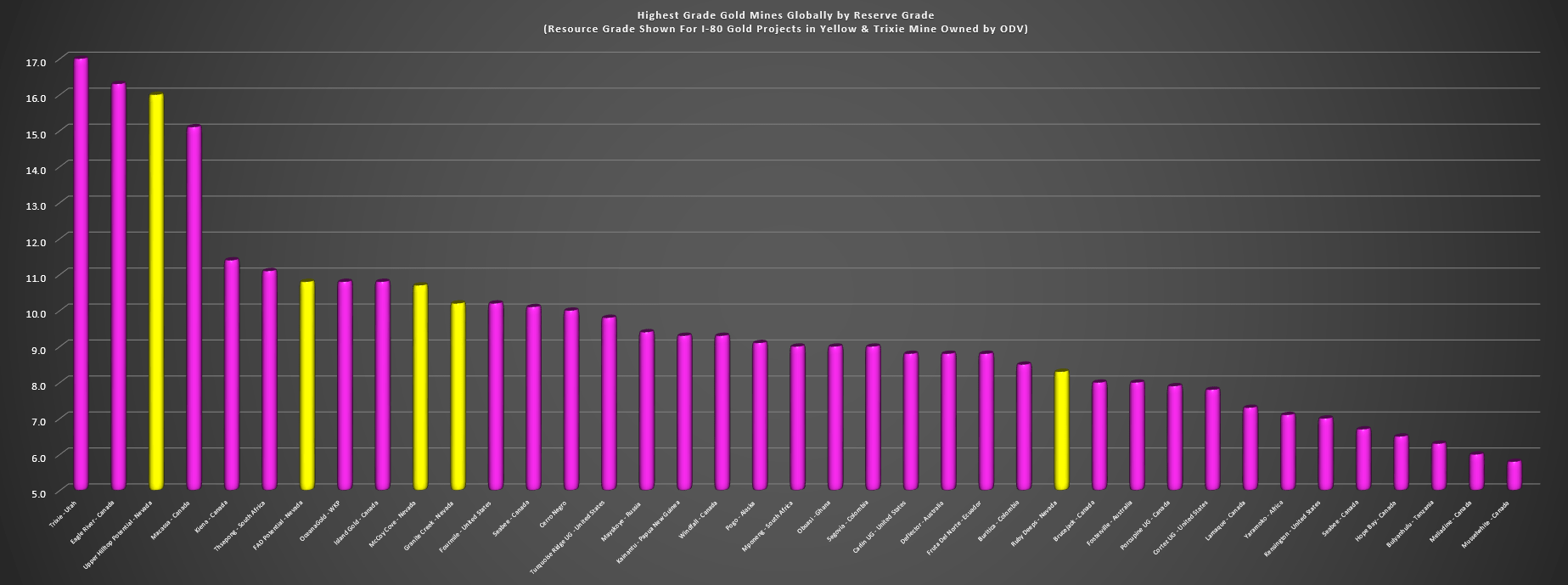

Highest Grade Gold Mines Globally by Reserve Grade vs. i-80 Gold Resource Grade & Estimated Resource Grade at Deposits/Mines (Company Filings, Author's Chart)

{kind=link}

As the chart above shows, i-80 Gold certainly holds project in the upper echelons from a grade standpoint, with the potential for it to have four of the top-20 highest-grade gold mines globally, and five of the top-30 highest-grade mines globally if it can bring all of its core assets into production. The above chart evidences this with i-80 Gold's deposits and mine (Granite Creek Underground) highlighted in yellow, with Upper Hilltop having the potential to be a 15.0+ gram per ton gold-equivalent asset if we continue to see high-grade hits out of this asset, while FAD, Cove, and Granite Creek could rival assets like Fourmile and Windfall from a grade standpoint. Finally, the comparatively lower grade (but still quite high grade) Ruby Deeps could rival assets like Brucejack, Buritica, and Porcupine Underground from a grade standpoint.

{kind=link}

The take-away here is that with i-80 Gold having some of the highest-grade assets globally that are all in the #1 ranked mining jurisdiction globally (Nevada), there's no reason that it should trade at half the average price paid for assets in Tier-1 jurisdictions over the past four years (2020-current). This is especially true given that the three-year average gold price has increased materially over the period from ~$1,600/oz at the mid-point of this period to ~$1,850/oz, suggesting that suitors should arguably be willing to pay a slightly higher price to lock up high-grade assets, and attractive assets like these should trade at a premium, not a discount.

The last point that I'd be remiss not to note is that, unlike most of the developers which have been scooped up over the past several years in Tier-1 jurisdictions, i-80 Gold arguably has the best infrastructure on this list with over $1.0 billion in sunk costs with a strategically located autoclave, CIL Mill, Floatation plant, assay lab and gold refinery at its Lone Tree Facility, heap leach pads at two sites and a CIL plant at Ruby Hill (potential to convert this to a floatation plant to process polymetallic material for modest capex), and a rail siding providing access to the Northern Nevada Railway. This means that from a total acquisition cost standpoint, i-80 is even more undervalued, given that suitors in the past have paid ~$140/oz for Tier-1 jurisdiction ounces and then will have to spend another $400+ million to ~$1.0 billion to operate these assets, with examples including Great Bear which will cost $1.0+ billion, Windfall at $350+ million (50% share), and

Hence, on a crude valuation per ounce basis, i-80 Gold remains heavily undervalued, and this is even if we exclude lower-grade ounces at Mineral Point, which I have not done when calculating the average paid for Tier-1 ounces for other developers.

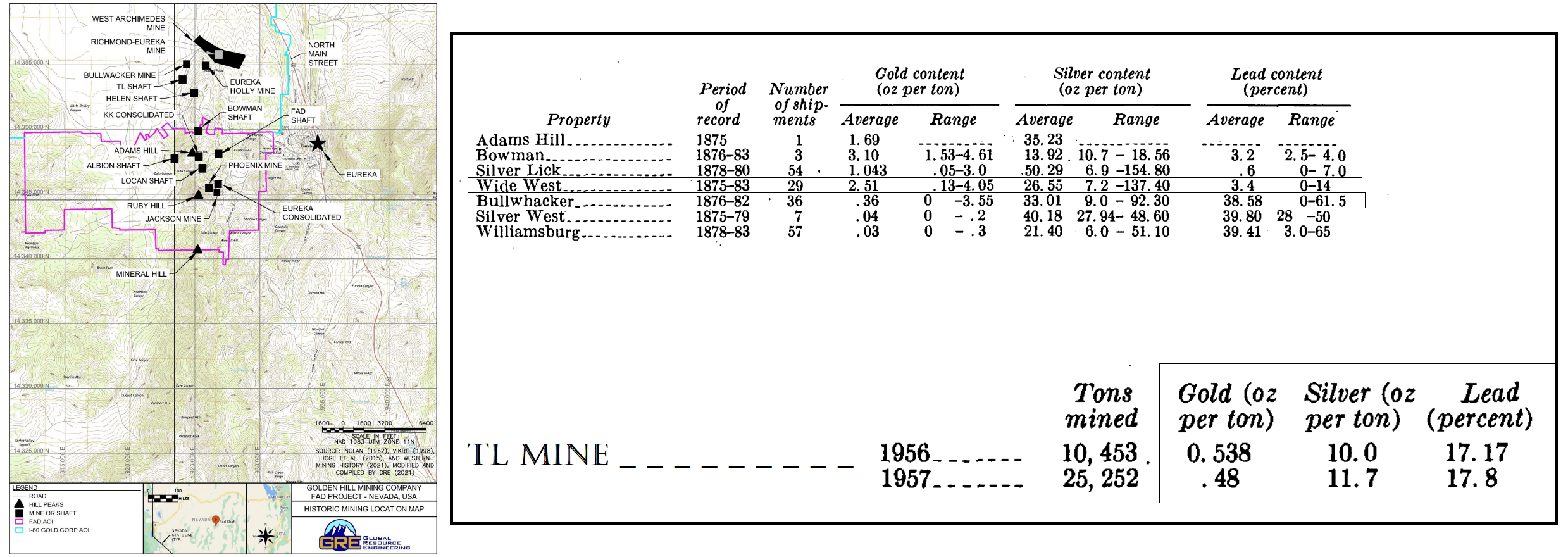

Meanwhile, from a P/NAV standpoint, i-80 Gold is just as attractively valued, trading at less than 0.48x vs. an estimated net asset value of ~$1.57 billion. And this is despite using what I would argue to be conservative gold price assumptions ($1,850/oz), an 8% discount rate for its polymetallic opportunity (Hilltop, FAD, Blackjack) and assigning value to exploration upside, which could be significant, with i-80 hunting for gold just southwest of a mammoth-sized mining complex (Turquoise Ridge) that's home to ~20 million ounces of resources, and hunting for gold and polymetallic mineralization in a district (Eureka) brought to life by miners in the 1800s with average gold grades at historic mines like TL, Bullwhacker, and Silver Lick ranging from ~12 grams per ton to ~35 grams per ton with an additional credit from 340 to 1700 grams per ton silver and 0.60% to 39% lead.

Historic Grades - Mines In Eureka District (Eureka Mining District of Nevada, Western Mining History - Nolan, Vikre, Hoge et Al, GRE))

{kind=link}

In addition, i-80 now owns the land where the ultra high-grade Ruby Hill Mine was located following its acquisition of Paycore, which carried reported grades of ~27 grams per ton of gold, ~660 grams per ton of silver, and 15% lead. This translates to a gold-equivalent grade of 40+ grams per ton, which would make this the richest mine on the planet if it were in production today, and its grades would even dwarf the average grades coming out of the best mine of the past decade, Fosterville, with grades regularly coming in above 25 grams per ton of gold. Obviously, there's no guarantee that i-80 Gold makes a new discovery, but when you're hunting for gold and polymetallic mineralization next to some of the highest-grade mines in a district that wasn't fully exploited, and on strike from elephants (with Granite Creek and Turquoise Ridge to the north), I like the company's odds of making a new discovery, but I have only assigned $100 million in exploration upside across its properties to be conservative.

Summary

i-80 Gold made one of the best discoveries in 2021 sector-wide with the South Pacific Zone and followed this up one of the best discoveries sector-wide at Hilltop, an asset with a highlight intercept of 10.0 meters at ~780 grams per ton gold-equivalent. However, the stock has since slid over 37% from its highs following an acquisition that took the momentum out of the stock and added shares to its registry and a recent follow-on equity raise to pad its balance sheet until it starts generating meaningful cash flow from the South Pacific Zone next year (Granite Creek Underground). This has set up another opportunity to enter the stock at a very attractive valuation, and I continue to see this as one of the best opportunities sector-wide from a reward/risk standpoint given that if the company execute successfully on its plans, there’s no reason it can’t trade at a $2.5+ billion valuation long-term as a 400,000+ ounce producer in Nevada.

Today, the stock sits at barely a ~$620 million market cap (or ~$740 million when factoring in warrants, options, and convertible debt), a valuation that now sits below that of some developers that won't pour their first gold before 2030. In my view, this is a significant valuation disconnect. And with a catalyst rich nine months ahead, I would not be shocked to see a significant recovery in the stock as we see a stream of positive news, including maiden resources, resource upgrades, economic studies, and drill results from multiple properties.

Hence, while the short-term turbulence is frustrating, I plan to continue to build on my position on any pullbacks below US$2.00 per share, and I continue to see i-80 Gold as one of the top-3 most compelling stories sector-wide in the small-cap space.

For further details see:

i-80 Gold: Cove Continues To Deliver