IAUX - i-80 Gold: Drilling Down

2023-10-11 06:06:20 ET

Summary

- i-80 Gold is trying to become a 400,000-ounce, 100% Nevada-focused gold producer.

- The issues with the company.

- IAUX is worth the risk at these levels.

Interstate 80 runs through the Carlin Trend and between the Battle Mountain and Getchell trends in Nevada. i-80 Gold ( IAUX ) is focused exclusively on this highly prospective mining region, hence the name of the company. While Barrick ( GOLD ) and Newmont ( NEM ) dominate in these trends (where the vast majority of the gold in the state is mined), IAUX has accumulated several assets and has the goal of becoming the number 2 player in Nevada. The Granite Creek mine is located just south of the Turquoise Ridge mine owned by the GOLD/NEM Nevada Gold Mines joint venture, while the rest of the company's assets are on the Battle Mountain Trend, including Lone Tree, Buffalo Mountain, Cove, Ruby Hill, and FAD (the latest addition). These aren't early-stage projects; they are either past-producing mines with substantial infrastructure or advanced-stage projects. And all of them have one thing in common: considerable exploration upside.

{kind=link}

i-80's management team, led by CEO Ewan Downie, understands the risks that come with exploration projects and has deployed a strategy that ensures the company is acquiring assets that will still command value even if the project isn't put into production. It's much more capital-intensive to go this route, as IAUX has spent considerable cash/stock - and even traded assets - to accumulate these mines and projects, but it's given the company an impressive portfolio.

A few pictures show these assets and existing infrastructure in more detail. Lone Tree has an autoclave, which is an incredibly valuable asset for gold companies, as this processing treatment releases gold encapsulated in sulfide. There are only three companies in Nevada that have autoclaves/roasters (NGM, i-80, and First Majestic Silver). Lone Tree also has an operating heap leach facility, an on-site lab, a core and logging facility, full maintenance shops, and a flotation circuit.

{kind=link}

Ruby Hill, a past-producing mine as well, has a crushing circuit and processing plant. All of this infrastructure at the mine would cost hundreds of millions of dollars to build today.

{kind=link}

While IAUX is technically a gold producer, it's only doing proof-of-concept mining at Granite Creek, and it amounts to just ~20,000 ounces of gold production per year. The company is very much still in the development phase, with the plan to become a substantial gold producer over the next few years.

The objectives are:

1. Drill at Granite Creek to increase resources, develop the lower levels of the mine (including the OG Zone and South Pacific Zone), and then ramp up production. The good news about Granite Creek is it's fully permitted, and the first stopes in the SPZ are planned for the first quarter of next year. The SPZ is primarily sulfide ore, and it will be sent to the NGM's Turquoise Ridge plant for processing until the Lone Tree autoclave is back online.

{kind=link}

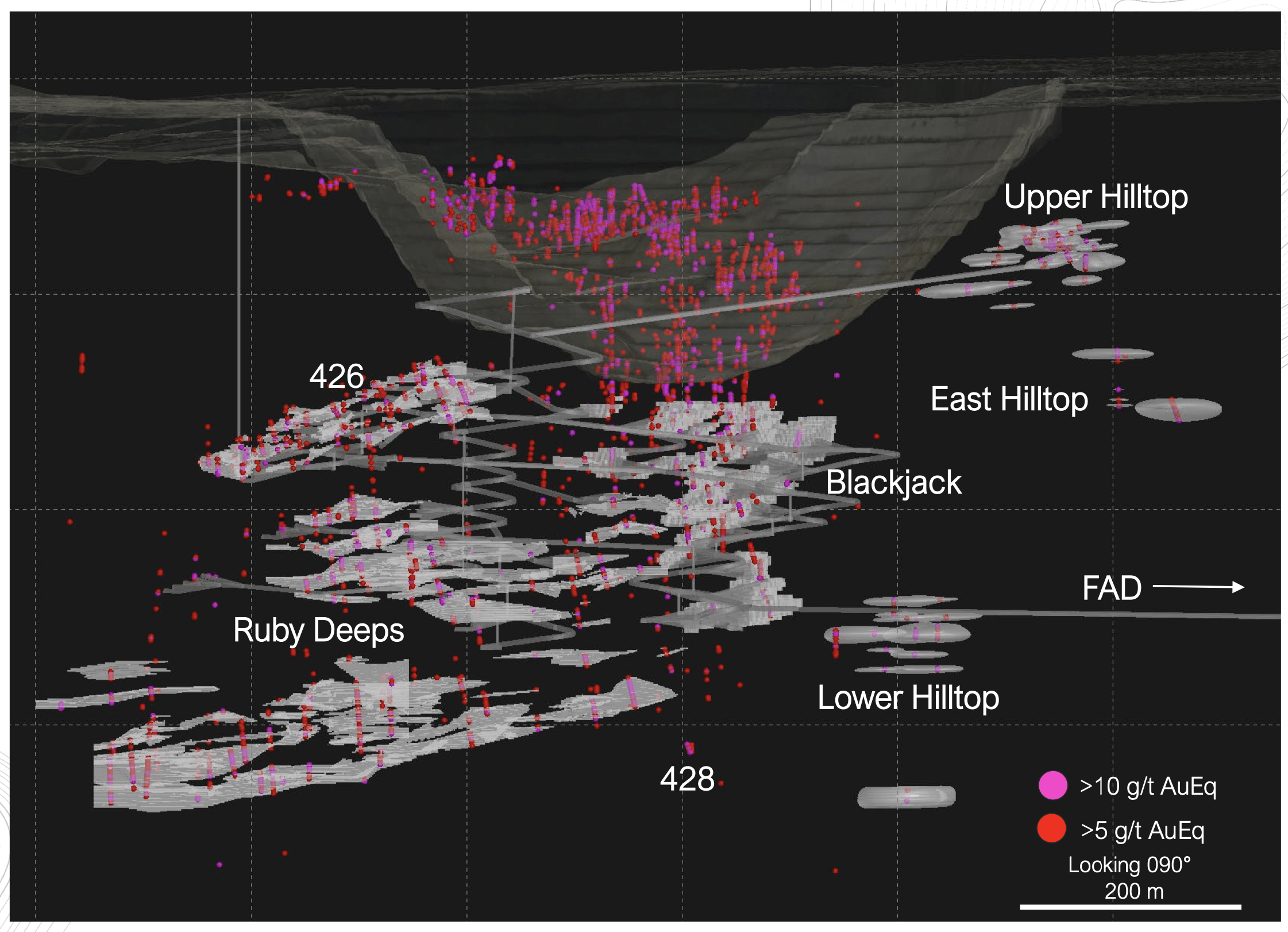

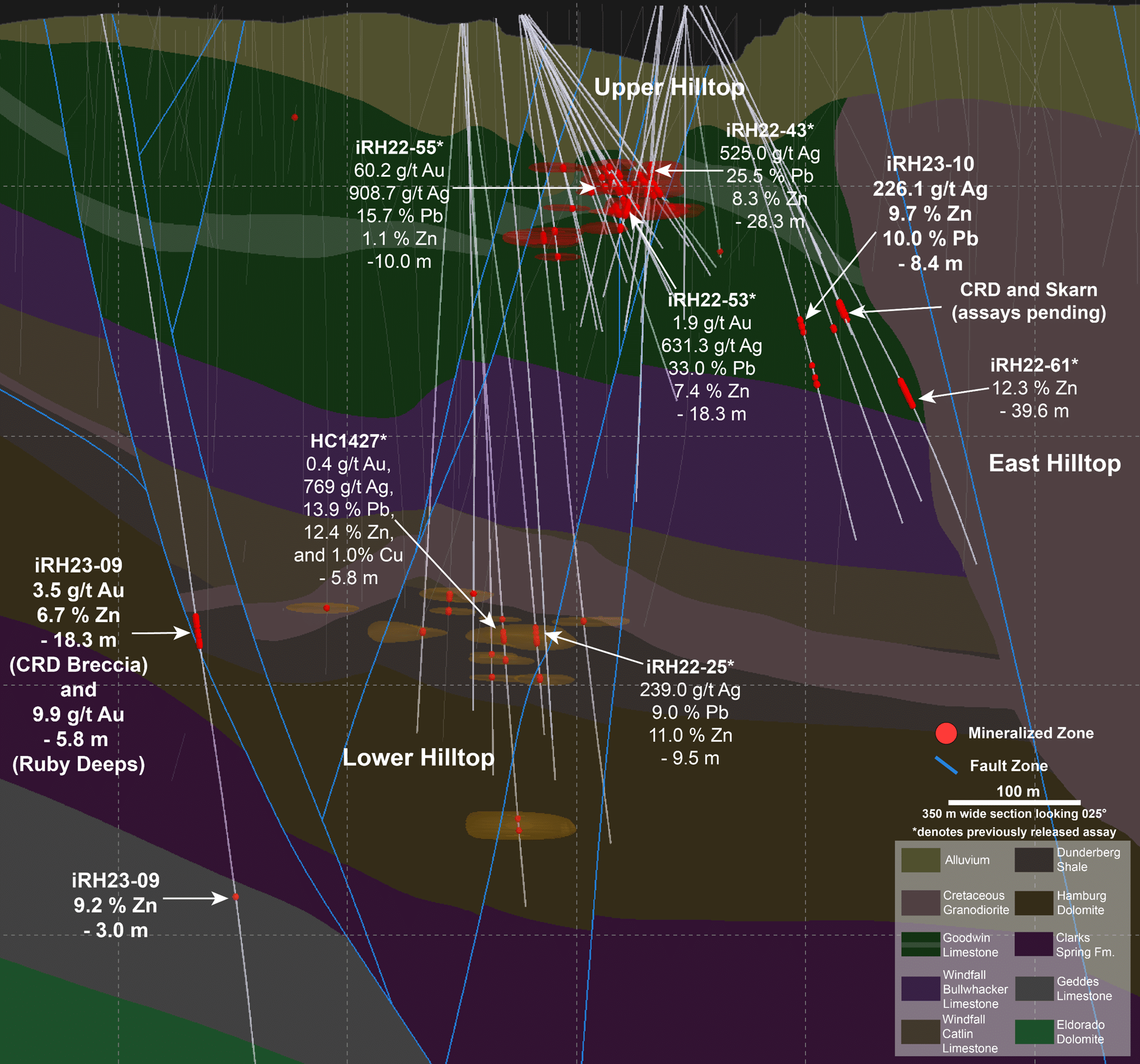

2. Drill at Ruby Hill to add more underground ounces (particularly at Ruby Deeps and Upper and Lower Hilltop) and get that mine back into production. IAUX is also assessing the conversion of the existing processing plant to a floatation plant to recover base and precious metals. While refractory gold from the underground operation will be trucked to the Lone Tree facility, polymetallic mineralization at Ruby Hill could be processed on-site at the existing plant.

{kind=link}

And...

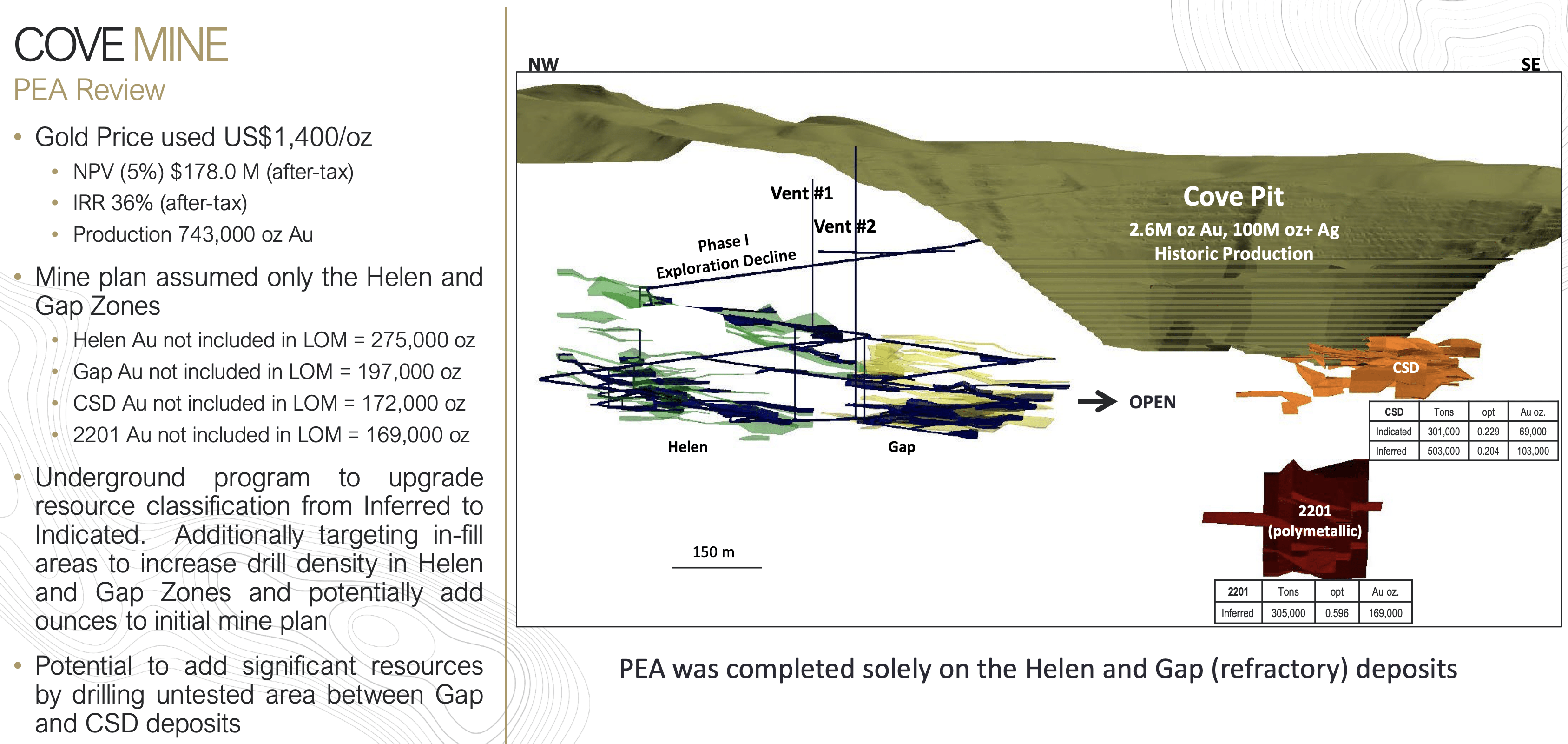

3. Complete infill and expansion drilling at Cove and then bring it online. Cove is a high-grade underground gold project (10+ g/t) with an already strong IRR at much lower gold prices, but only 743,000 ounces were expected to be mined per the PEA, and IAUX needs to add significantly more ounces to make the NPV standout.

{kind=link}

Eventually, there will be three mines in production, with ore processed at Lone Tree and some potentially at Ruby Hill.

It's a portfolio that contains over 14 million ounces of gold resources and could produce 400,000+ ounces of low-cost gold per year. For a company focused 100% on Nevada, investors can understand the potential value of i-80 if it's successful.

The market cap of IAUX is ~US$450 million, and a miner with this level of production, the staggering amount of resources, and low jurisdictional risk would trade at a $2-$4 billion valuation.

On paper, it all sounds good, but up until last year, I was underwhelmed with the story and found it a bit "meh."

I've seen this movie before, as Downie ran Premier Gold, and Cove is a holdover. New assets have been added to the mix, but Premier never turned into a world-class company, and I was skeptical that i-80 would be any different. Premier didn't destroy shareholder value, but it didn't do much either. The concern was that i-80 could be a repeat.

However, in the summer/fall of last year, the company released some stellar drill results from their Granite Creek and Ruby Hill properties. It was a bit too early to call these "game-changing" results, but they most certainly positively impacted the value of i-80, considering the high-grade, wide intercepts at multiple sites.

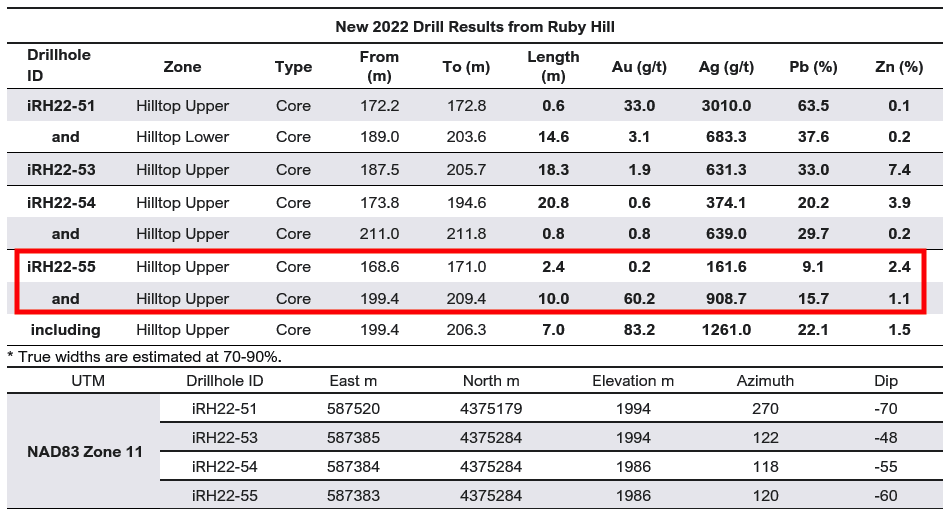

Shortly after, IAUX released some spectacular intercepts from follow-up drilling on the Hilltop Zone at Ruby Hill, which included bonanza-grade gold, along with high-grade silver, lead, and zinc. Hole iRH22-55 was stunning as it intercepted 60.2 g/t gold, 908.7 g/t silver, 15.7% lead, and 1.1% zinc over 10 meters (true width estimated at 70-90%).

{kind=link}

Downie said in the press release : "We believe that the grades of mineralization at Ruby Hill are truly world-class and the Hilltop Zone ranks amongst the highest-grade new discoveries being drilled anywhere on the planet."

While I wasn't in the "world-class" camp yet - as when compared to Filo del Sol, Windfall, Brucejack, Queensway, Kiena Deep, and even Island Gold, the Ruby Hill results didn't quite match up - it was still an extraordinary drill hole and warranted attention to see if a major discovery was unfolding that would dramatically improve the outlook for i-80 Gold.

IAUX surged late last year on the drill results and was far outpacing the rest of the sector, but the share price has since declined sharply. Which brings us to the issues with IAUX and why it's now underperforming so dramatically.

The Issues With i-80 Gold

One of my complaints about Premier Gold was the company was spread too thin, and that's the same trap i-80 is falling into.

Let's recap some of the work being done on the key assets in the portfolio:

- Ruby Hill Property - Major drill program underway, Preliminary Economic Assessment ((PEA)) being completed for the underground gold mineralization, permitting ongoing for underground development, detailed metallurgical work and processing plan under development.

- Granite Creek Property - Underground development progressing, mining rate increasing, economic studies and revised resource estimate being completed.

- Lone Tree Property - Cost estimate for the restart of the autoclave facility completed and work on the Class III Engineering (detailed engineering) study underway, ongoing residual leach program.

- McCoy-Cove Property - Underground development, ~40,000 meter underground drill program, Feasibility Study.

That's four properties that IAUX is trying to develop in tandem, which would be a massive undertaking even by an established mid-tier producer. i-80 is barely producing any gold and has no positive cash flow to help fund all of these projects.

Tens of thousands of meters are being drilled at these projects, and then there are all of the studies in progress, underground development required, permitting costs, etc. Those alone are $100+ million in upfront capital.

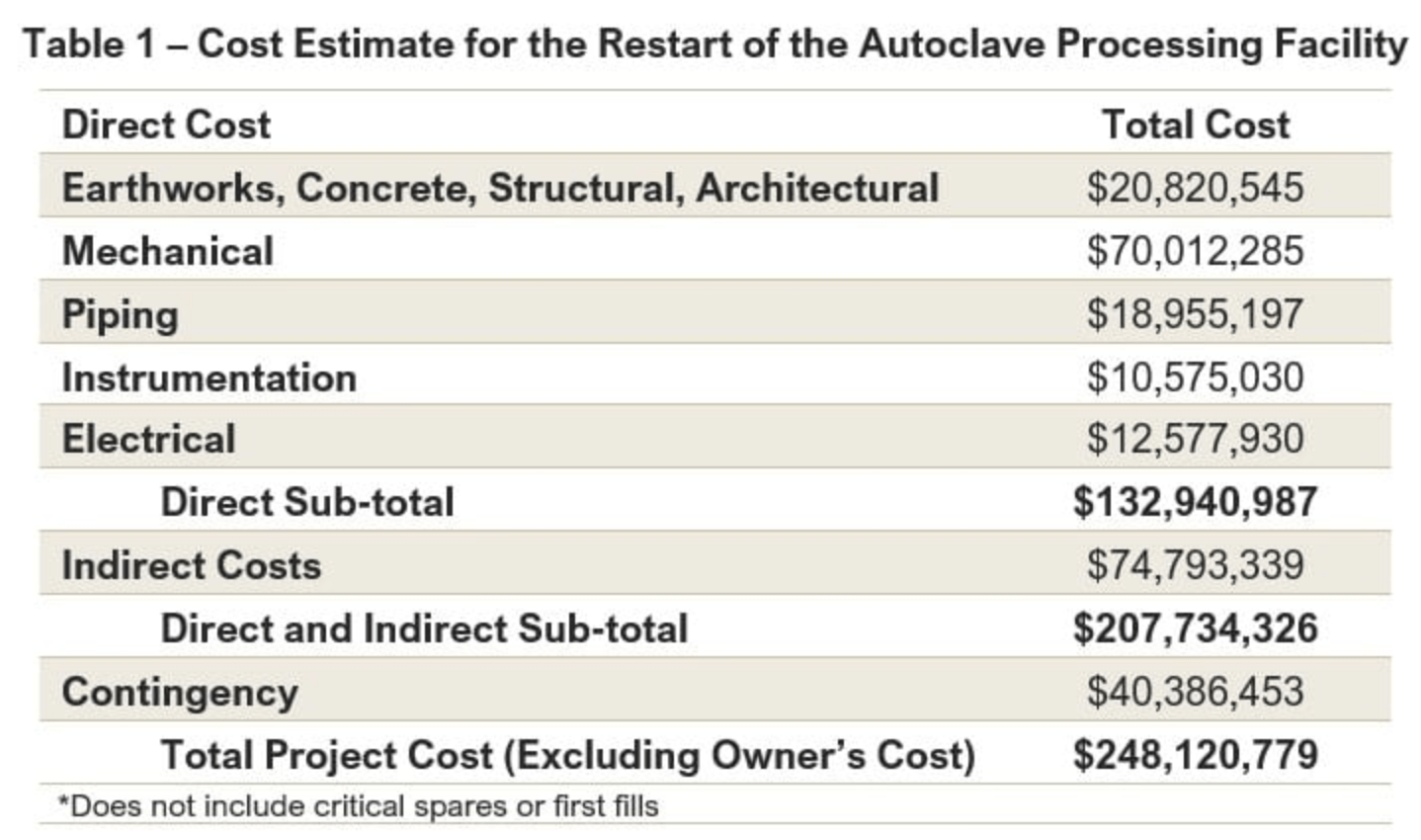

But that's not even the big ticket item, as the estimated cost to restart the autoclave at Lone Tree is US$248 million.

{kind=link}

The preliminary capital estimate for the potential restart of the existing process facilities at Ruby Hill is US$8.9 million, which would allow the company to process oxide material. Part 2 of the study estimated it would cost US$65.7 million to convert the process plant from a mill/leach facility processing oxide gold to a base metal flotation plant producing a lead/silver concentrate and zinc concentrate.

Which brings me to the main issue, which is that IAUX is burning way too much money.

At the end of December 2022, the company had US$48 million in cash. In February of this year, it issued US$65 million of convertible debt, which barely covered the cash spent in the first quarter as negative free cash flow was $33 million, the company spent $11 million on contingent payments for Ruby Hill, and then had almost $10 million of payments for the gold prepay and silver purchase agreements.

{kind=link}

There was simply too much cash burn in Q1 2023.

In the June quarter, the company burned another US$37-$38 million, leaving it with just US$19 million in cash at the end of Q2.

In the Q4 2022 conference call in March of this year, the company stated:

We are prioritizing reserve increases and mine development with minimal dilution in the future to our shareholders. So as we continue to finance our projects, we will look to continue to be creative at how we build our deposits without necessarily coming to the market every year to dilute our shareholders further.

Yet, this past July, the company announced a C$32.0 million private placement (upsized to C$36.8 million) at a 10% discount to the then share price.

Realistically, the company is on pace to spend US$100 million or more over the next four quarters, and that doesn't include any capital to restart the plants at Lone Tree or Ruby Hill.

It raised US$20 million last month via an additional gold prepay agreement with Orion Mine Finance, which is non-dilutive financing. However, there were some warrants (albeit far out-of-the-money) attached to the deal, and it's extending the expiry date of the 5.5 million warrants issued to an affiliate of Orion in connection with the 2021 Gold Prepay Agreement.

Still, with the money raised in Q3, IAUX likely only has enough cash to last through the end of the year, or early next year at the latest.

The company had US$155 million of debt at the end of Q2 2023. It could take on more debt, but I believe dilution will be a continued risk. Management is also more conservative with the balance sheet, and I'm not convinced they are willing to take on the debt required to finance all of this growth.

The risk with this capital-intensive strategy is i-80's market cap increases dramatically in size as it brings production online, but the share price does nothing or underperforms because of dilution. Similar to Osisko Mining ( OBNNF ) and other developers that have relied on heavy dilution over the last few years to fund their projects. In other words, like what's occurred in OBBNF over the years, the market cap of IAUX might double due to the increase in share count, not because of appreciation in the stock price.

That's my main concern with IAUX. It lacks the financial capacity to fund this growth and is spreading itself too thin.

The market has changed over the last 12-24 months. Investors have crushed the stocks of gold explorers, developers, and producers. Trying to raise capital in the current climate - when the value of your currency (i.e., stock price) heads to the depths of despair - is incredibly dilutive for most exploration/development companies at the moment. Some would need to dilute by 50-100% to obtain the funding they require to continue to advance their assets over the next 12-24 months.

This is not the time to spend aggressively. Companies need to pivot on strategy, at least until the market improves.

IAUX isn't in the same position as some of its peers as it has a healthy market cap, but it would still need to dilute by ~20% to raise enough capital for the next year.

The company shouldn't attempt to advance four projects/properties in this market. It needs to shift strategy and rein in some of this spending, at least for the short term.

There will be additional cash flow coming in Q1 2024, as the first stopes from the SPZ at Granite Creek are mined, but it won't be nearly enough to cover all costs.

I would rather IAUX hyper-focus on one or two properties for the foreseeable future. Whichever ones it believes have the most near-term potential.

Let's move to the next issue.

There've been some very strong drill holes recently from Cove, and encouraging holes at depth at Granite Creek. But follow-up drilling in and around Upper Hilltop at Ruby Hill wasn't nearly as breathtaking as hole 22-55 reported last year (which sparked the rally in the stock). For example, 23-10 (also shown in the diagram below) hit solid silver grades (226.1 g/t) and exceptional zinc and lead grades over 8.4 meters, but it contained little gold, and the silver grades were dramatically lower than hole 22-55. However, two months ago, IAUX announced another exceptional intercept in an untested area at Blackjack, which is only a couple hundred meters from Upper Hilltop, as it hit 45.4 g/t Au and 50.2 g/t Ag over 17.5 meters. There is definitely high-grade gold at Ruby Hill, the questions are how continuous is the mineralization and is there a mineable deposit. It's possible that there are only isolated pockets of bonanza-grade ore and it's not an extensive system. Not to be misinterpreted, the recent drill results at Ruby Hill are quite impressive, but there needs to be a lot more work done to identify the system, get a better understanding of its potential, and show a larger structure forming. We don't have enough data. It's like having many puzzle pieces but not knowing what they form yet or where the other pieces are located (and what they even look like). IAUX is trying to assemble this puzzle.

{kind=link}

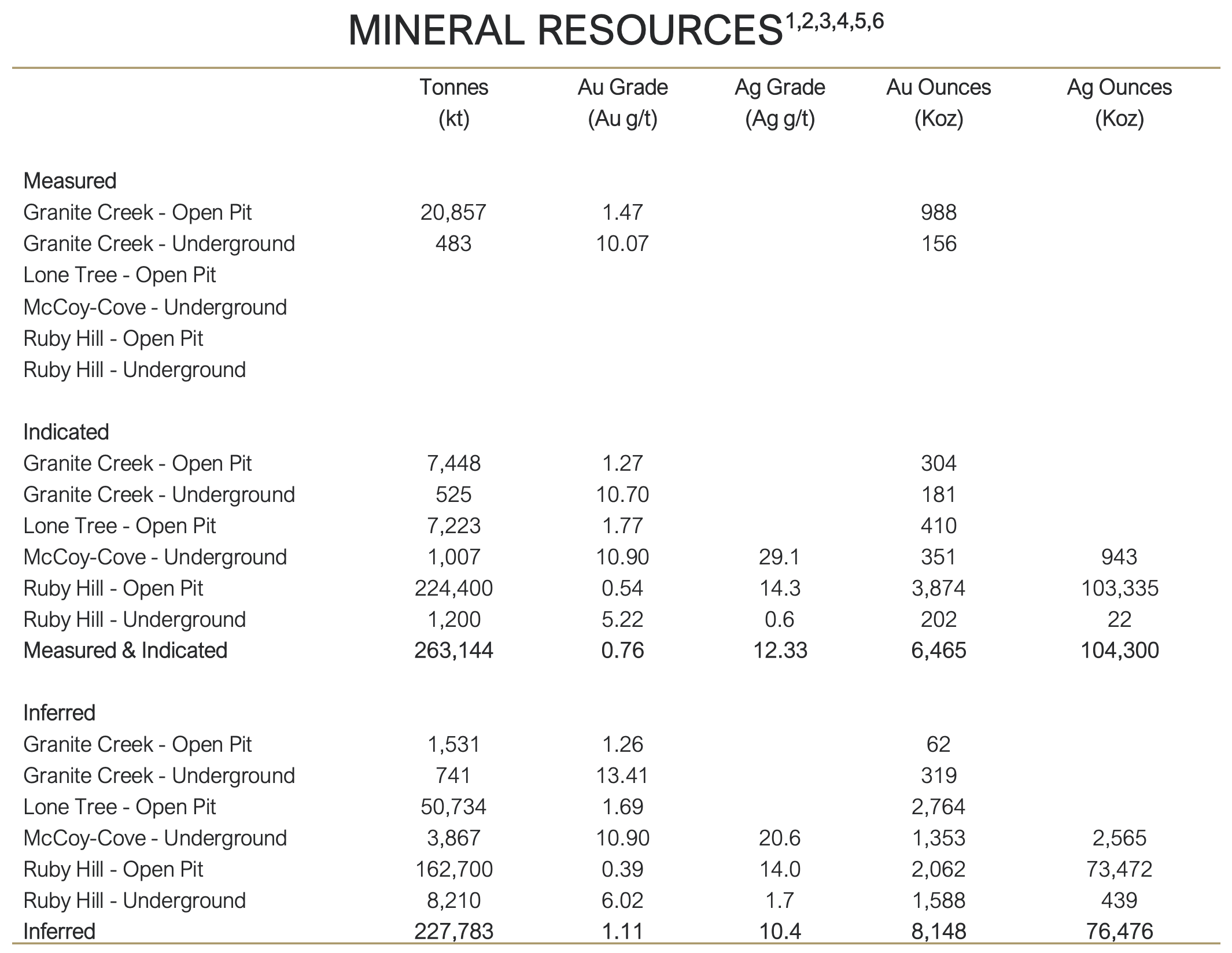

The last issue I want to discuss is the 14.6 million ounces of gold resources and ~180 million ounces of silver resources. For a US$450 million market cap company, this is a colossal amount of ounces. But not all ounces are the same, as what matters is whether they are economical. If you can't extract the gold profitably, it doesn't matter how many ounces you have. Which is the case for the almost 6 million open-pit ounces at Ruby Hill, and almost all of the Ag resources.

First, the grade of the open-pit resources at Ruby Hill is extremely low at just 0.54 g/t for the Indicated ounces and 0.39 g/t for Inferred. These are mostly oxides, so they can be heap leached, but costs will likely still be high. There are significant silver ounces as well, but grade is also low at just 14.3 g/t. Second, the crushed heap leach recovery for gold is about 81%, but only 33% for silver, so only 1/3 of the silver resources could be recovered via heap leach. IAUX would need to build an enormous plant to improve recoveries, but the cost would be US$1+ billion.

{kind=link}

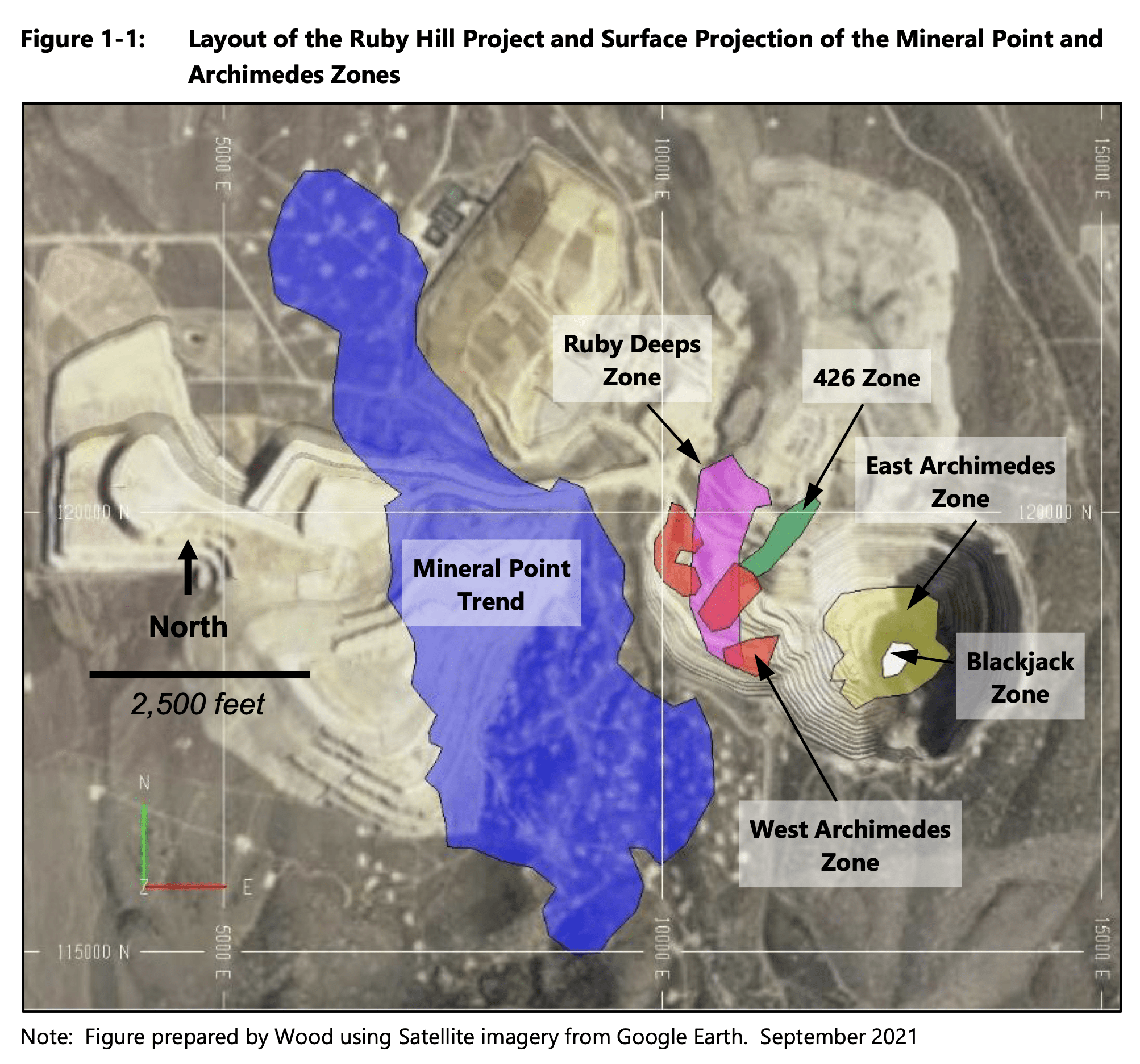

Third, most of these open-pit ounces are at Mineral Point, and there is an old heap leach pad covering the middle of the deposit. There would be a massive amount of waste stripping required to extract these resources, as first you would have to clear the leach pad material, then the waste in the pit.

{kind=link}

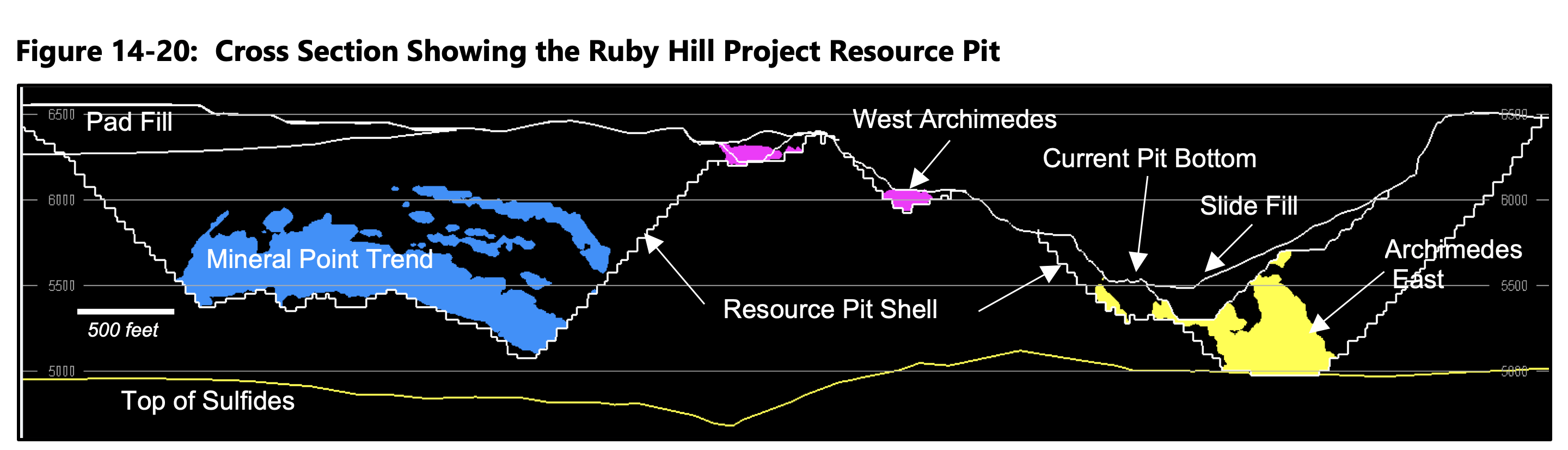

This cross section gives another perspective, as it shows the pad fill that needs to be removed, and then the waste below it, before reaching the mineralization.

{kind=link}

The bottom line is I don't believe any of these open-pit ounces at Mineral Point are ever mined. Technically, they are resources, and it's perfectly fine for IAUX to report them, but they are likely economically worthless. Which is why you can't value IAUX on a per-ounce basis, at least using all of the resources.

I also question the value of the currently defined resource at Ruby Hill underground, as the total ounces are average grade. For these ounces to make sense to mine, there needs to be a substantial amount of high-grade resources added in other areas of the deposit - so you blend the lower grade with the higher grade and come out with a more economical mill feed grade.

In no way am I suggesting that all of i-80's resources have zero value, but I think there is only realistic economic potential for about 3-4 million of those ounces. More depending on Lone Tree open pit. However, that's still a healthy base to start from and exploration success could greatly build on that total. The company could become a 300,000-400,000 ounce gold producer with these resources.

IAUX Is Worth The Risk At These Levels

There is definitely potential with IAUX, and there are many aspects about the story that make it appealing. With the stock down 50% from its highs earlier this year, severely underperforming since July, and extremely oversold in the short term (as I believe we just witnessed capitulation in the stock), IAUX could easily surge 20-30% over the next month or two if the selling in the sector is over.

StockCharts.com

At a market cap of ~$450 million and EV of ~$550 million, the resale value of its assets likely equals its market cap, and possibly the enterprise value, too.

The PP&E on the balance sheet went from US$130 million in 2021 to $630 million today because of all of the properties acquired over the last two years, which supports my assumption.

One can say the value of these assets recorded on the financial statements might be overinflated, but I strongly believe that if you were to liquidate this portfolio, you could walk away with $400-$450 million at current gold prices, and that's conservative.

So, this gets back to Downie's strategy of acquiring assets that will still command, better yet, retain value even if the project isn't put into production. The benefit of spending all of this capital upfront is these assets act as a backstop for the stock price. Unlike other explorers/developers - that only have ounces in the ground and not much infrastructure, and the market is currently paying little for those ounces - i-80 has tangible assets that are liquid. As a result, I believe i-80 is near the floor for its market cap at $1,850 gold.

Notice I said "market cap," not stock price. The main risk is dilution, but with the recent capital raise, I think that pushes out the risk by another ~two months. This stock could move higher quickly over the next two weeks if gold continues to recover. At the very least, I see a compelling short-term tradable opportunity on the long side.

If there are more bonanza-grade intercepts at Upper Hilltop or other deposits, then it makes IAUX even more interesting. There is game-changer potential.

I believe the stock will work well if gold gets above $2,000 and breaks out in the short term, but if gold remains rangebound or declines further, IAUX will need to adjust its plan and reduce spending.

For further details see:

i-80 Gold: Drilling Down