EPRT - I Am Buying These 8% Yielding REITs

Summary

- Dividend yields are high again in the REIT sector.

- Share prices dropped in 2022 even as dividends were hiked.

- We highlight two 8% yielding REITs that we are buying.

In 2022, REITs had their worst year since the great financial crisis as their share prices dropped by 30% on average:

That's just the average performance of a market-cap weighted ETF ( VNQ ) that owns mainly large-cap, investment-grade rated REITs so you can imagine that many of the smaller and lesser-known REITs must have dropped by even more than that.

Quite a few dropped by nearly 50% in a single year ( DEI ; VNO ; NXRT ):

But despite the collapsing share prices, REITs actually grew their cash flows quite significantly in 2022 and most REITs even hiked their dividends . Their cash flows grew rapidly because the high inflation led to rising rents and the rising interest rates didn't have a major impact since REITs have strong balance sheets with low debt and long debt maturities in most cases:

{kind=link}

Rising dividends... coupled with collapsing share prices... has resulted in a lot of high-yielding opportunities in the REIT sector.

Quite a few companies are now offered at up to 8% dividend yields and in today's article, I will highlight two of them that we are buying at High Yield Landlord:

EPR Properties ( EPR )

EPR Properties is a REIT that specializes in experiential properties such as water parks, golf complexes, amusement parks, ski resorts, and movie theaters:

EPR Properties EPR Properties EPR Properties EPR Properties

In 2022, the company hiked its dividend by 10%, but its share price dropped by 23%, and as a result, its yield expanded to 8.1%:

We think that the market is undervaluing EPR because of two key misunderstandings:

- It fears that EPR will suffer in a recession because it owns experiential properties that rely on discretionary spending.

- It also fears that movie theaters are a dying industry and that EPR's properties will suffer great pain in the future.

But here's why these fears are misplaced.

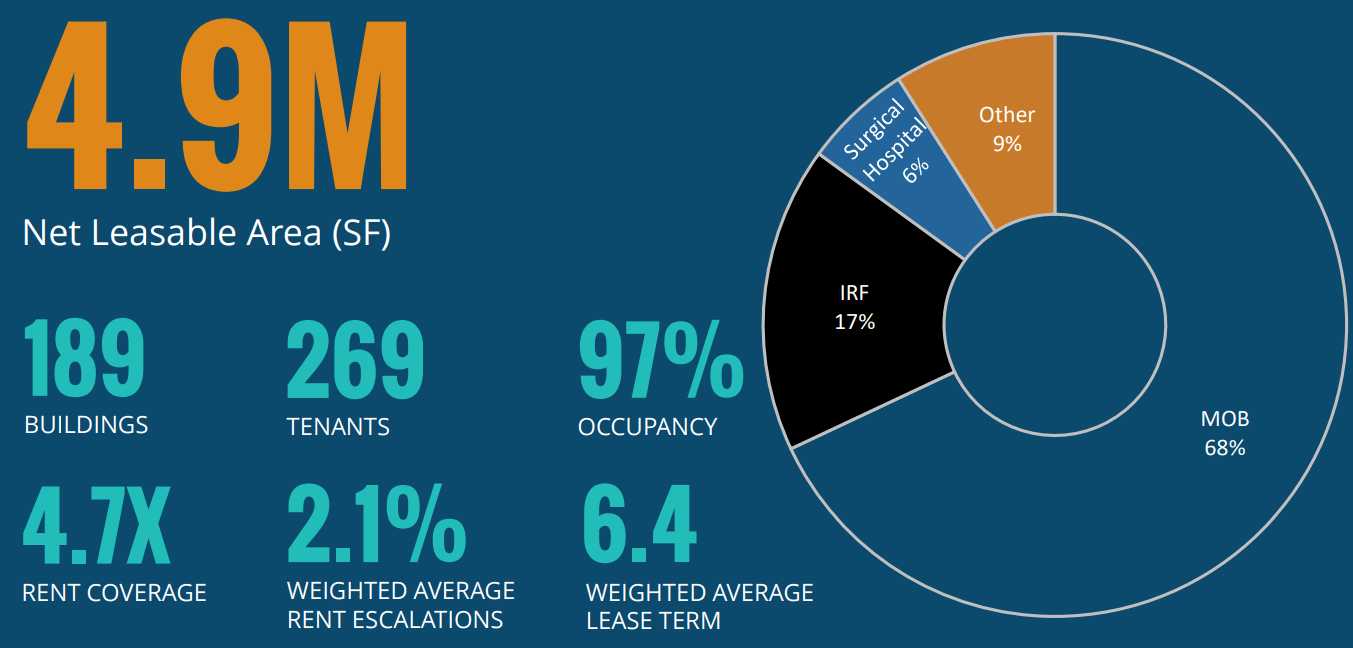

Firstly, EPR is a landlord, not the operator of these properties. It earns steady rental income from triple net leases that have 14-year long terms remaining on average and rents are hiked each year by 2% regardless of a recession. So yes, its tenants may see their profitability go down a bit in a recession, but EPR's rental income won't change as long as its tenants are able to pay their rent. Today, the rent coverage is very strong at 2x so there's a lot of margin of safety even if we hit a recession. Tenants won't stop paying rent and lose their profit centers because of one or two tough years.

EPR Properties

Secondly, EPR's movie theaters aren't just any movie theaters. They are some of the most productive theaters in the nation and those aren't going anywhere. Some of the lower-quality theaters may well close down, but that would actually benefit EPR's theaters because it would consolidate traffic toward the most productive theaters. As such, I expect the weak to get weaker and the strong to get stronger.

EPR today owns 3% of theaters in the US, but they actually generate 8% of the total revenue. These theaters are already profitable today, despite the fact that the box office still hasn't fully recovered from the pandemic. Now, studios are all realizing that theaters remain essential to monetize new blockbusters and the movie slate is recovering. The new Avatar movie has already been one of the highest-grossing movies ever and so clearly, movie theaters aren't dead.

EPR Properties

Clearly, AMC ( AMC ), Cinemark ( CNK ), and Regal ( OTCPK:CNNWQ ) type tenants are somewhat speculative, but again, it is important to remember that EPR owns some of the highest-quality theaters in the nation and these aren't going anywhere.

Besides, even if you disagree with me, these properties represent just around 1/4 of the company's NAV. You can assign them a ~20% discount and the company would still remain undervalued.

EPR has successfully invested in these property sectors for decades and materially outperformed other REITs, despite all the naysayers, and today, the experience economy is booming as we still emerge from the pandemic.

EPR Properties

EPR also has a strong balance sheet with lots of liquidity to keep acquiring new properties and deal with occasional issues at some individual properties.

We expect it to grow its cash flow by around 5% in 2023 as it acquires new assets and its rents are hiked again.

Typically, such REITs are priced at closer to a 4% dividend yield. Good examples are Realty Income ( O ), National Retail Properties ( NNN ), and Essential Properties Realty Trust ( EPRT ).

But today, you can buy EPR at an 8.1% yield due to the market's misunderstanding of the risks.

Is EPR riskier than Realty Income? It sure is. But should it trade at a nearly 2x higher dividend yield? We don't think so. Priced as it is, we think that EPR presents around 50% upside potential as the health of the movie theater industry continues to improve and the market recognizes its mistake.

Global Medical REIT ( GMRE )

Global Medical REIT is a REIT that specializes in medical office buildings in secondary markets:

Global Medical REIT Global Medical REIT

In 2022, the company hiked its dividend by 2%, but its share price dropped by 47%, and as a result, its yield expanded to 8.3%:

The market is worried because the entire healthcare sector suffered great pain from the pandemic and the high inflation in labor costs. Many operators of senior housing and skilled nursing facilities are still losing money and fighting to stay alive. It caused the entire healthcare property sector to underperform.

But what the market appears to have overlooked is that medical office buildings are far safer than other healthcare facilities.

Their rent coverage is around 5x, whereas the typical rent coverage of skilled nursing facilities is closer to 1-1.5x in many cases.

As such, medical office buildings have stronger tenants that are much less likely to default on their leases.

{kind=link}

The market also appears to have overreacted to the surge in interest rates. Yes, about 20% of its debt has a variable rate and so its interest expense will rise, but this is not a catastrophe. Its leases also include 2.1% annual rent hikes that compensate for it.

Its growth won't be significant in the near term but priced at an 8.3% dividend yield, we don't need much of it to reach double-digit annual total returns.

And eventually, as the market sentiment of the healthcare sector improves, we expect GMRE to reprice at closer to a 5% dividend yield, unlocking ~50% upside to shareholders.

Bottom Line

Right now, the REIT market is a goldmine for high-yield-seeking investors who know where to look.

The sector offers up to 8% dividend yields that are not only sustainable but even growing. Obviously, you need to be selective and there are risks as well, but overall, the risk-to-reward is very compelling and this is why most of my capital is going into these opportunities at the moment.

For further details see:

I Am Buying These 8% Yielding REITs