E - I Am Long Eni: Dividend Raise And Key Role For Europe

Summary

- Eni is an oil major that is set to play a strategic role for Europe in trying to diversify its gas supply chain.

- Eni is set to achieve strong results even in case of a more normalized scenario.

- A strong CFFO generation is able to support yet another dividend increase and a buyback plan of up to 4.5% of the current market cap.

Introduction

Energy and utilities stocks can usually be found as part of my portfolio. However, especially energy stocks are among the ones I trade it and out of depending on how I see the economic cycle.

Last year, I started exiting all of my energy stock positions, locking in some gains as many of them reached ATHs. However, I felt there was a stock that still need to express its value. I am speaking of the Italian oil-major Eni ( E ).

This is why I wrote this article " I Locked In Some Profits From My Oil Stocks, But I Kept Eni ".

I thought Eni was being way too discounted compared to its main peers (even Seeking Alpha recently listed it among the top 10 large-cap stocks with the lowest P/E), with the marker underestimating the key strategic role the company has to play for Europe's energy future. In fact, its network in Africa and the Middle-East is crucial to secure new gas supplies from countries outside of Russia.

In addition, the company was clearly set to generate billions of free cash flow that could also be used to strengthen its (already solid) balance sheet while leaving wide room for dividends and buybacks.

Since then, E stock has returned a nice 24.4% including dividends versus [[SPY]] that has basically been flat (-1.35%). Eni has also outperformed the industry in the past six months, second only to [[BP]].

Now, it is time to look at Eni once again to see if it is worth holding on to it or if it time to rotate out of it.

A look at Eni

That 2022 was going to be a great year for oil-companies - and Eni, in particular - was out of doubt. Many shareholders have also benefited from the high dividend (as I explained in the past, Eni had a variable dividend policy linked to a floor dividend that can be increased based on the average Brent price; buybacks were linked to this too).

In 2022, Eni's sales from operations topped €132 billion, an impressive +73% YoY. But we all know this was mainly due to sky-high oil prices linked to the conflict in Ukraine.

Operationally, the company reached a profit of €20.4 billion that turned into a net profit of € 13.8 billion, which is a +137% YoY. This shows something that is true for many oil companies, as oil prices go up, driving revenues upwards, the companies benefit from better scale and efficiency and make each dollar of extra revenue more valuable.

However, while the full year results were impressive, some investors were concerned about Q4 results. Here, although sales increased by 17% YoY, the operating profit decreased by 6% to €3.6 billion. Net profit was even worse as it moved down from €3.5 billion last year to just €550 million in this past quarter.

What happened? This time Eni had many so-called special items impacting the quarterly net profit, which, if adjusted would have been 47% more than the net profit of the same quarter in 2021.

These items included the one-off solidarity contribution it had to pay in Italy and Germany (€1.7 billion). Eni had also to record net charges of €645 million related to projects write-offs and asset impairment charges, among others. While these accounting facts should not be ignored when looking at the full picture, from a point of view wanting to assess how a company is operating we can look more straightforwardly at the adjusted results.

Moving on to cash flow from operations, Eni generated over €20 billion. Its use was something I particularly liked. As we can see, it wasn't used only for shareholder distributions, but also to cover organic capex (which increased because of FX) and to achieve a €2 billion net debt reduction.

ENI 2023 Capital Markets Presentation

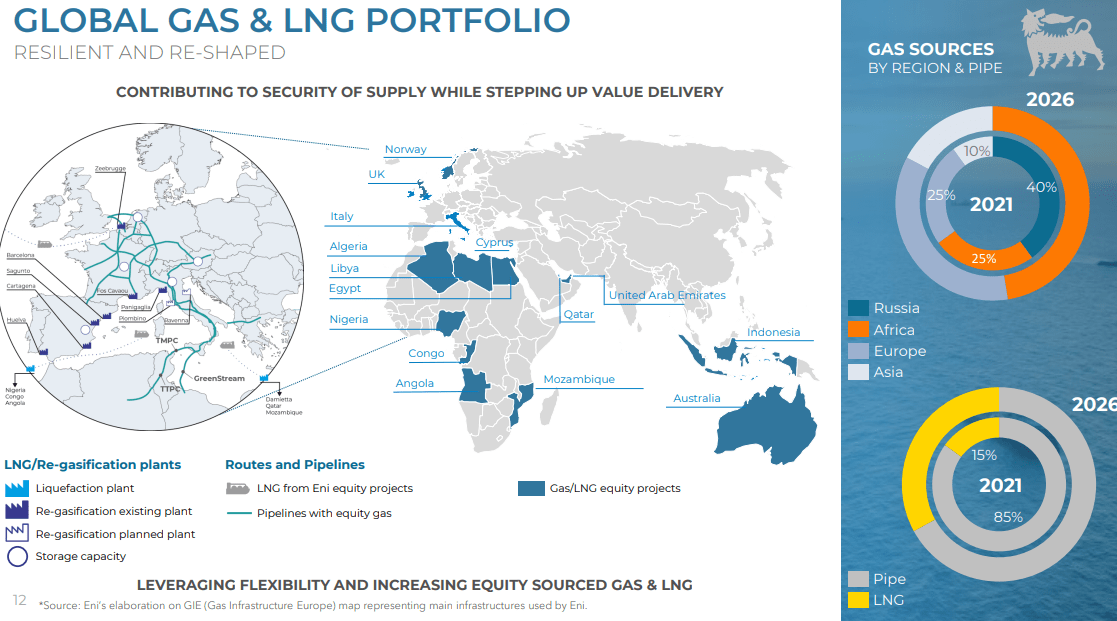

More importantly, I am following how Eni is operating to pursue the goal of fully replacing Russian gas volumes by 2025. By leveraging its relationships with producing countries such as Algeria, Egypt, Mozambique, Congo LNG, and Qatar, Eni has been able to replace more than 50% of its Russian gas. Thanks to its new strategy contractual LNG volumes are expected to exceed 18 MTPA by 2026 (9 MTPA in 2022). This sets the company to become a major European player in the new gas supply chain Europe needs. As it is shown in the map below, Italy, thanks to its geographical position and its infrastructures, could actually become the European southern hub of the whole gas supply chain. In this case Eni would really assume a key role for the whole continent that needs yet to be understood by investors.

{kind=link}

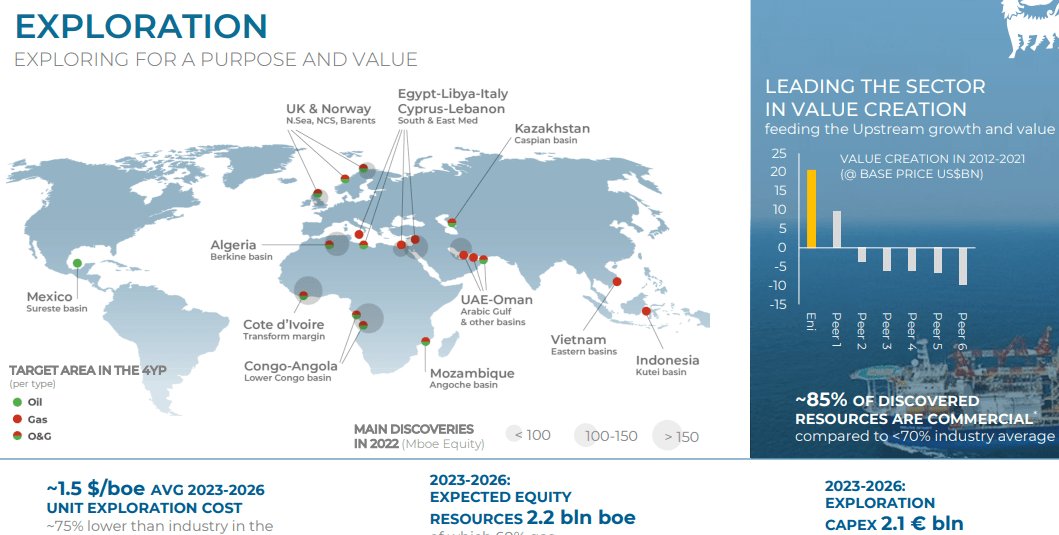

Eni is a leader in value creation through its exploration activities, with a track-record that shows how 85% of Eni's discovered resources are commercial, versus the industry average that is below 70%.

{kind=link}

Outlook

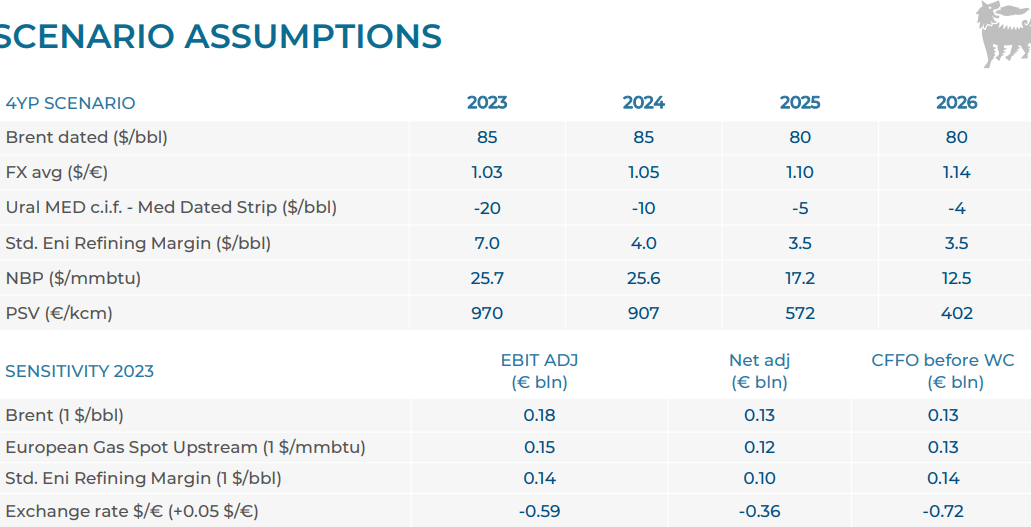

The company shared the following assumptions for the next four years. We have seen how we live in a world where things can rapidly change. However, I think these assumptions are realistic, especially when they consider Brent price to stay around $80-85/bbl all the way through 2026. Considering geopolitical tensions and growing demand from China that should more than offset any mild recession in the West, I don't see oil prices go down a lot from where they are now. Actually, I think there is a higher chance to see them peaking from time to time above $100. This is a tailwind for Eni, as any extra dollar per barrel adds about €200 million of adj. EBIT.

{kind=link}

In 2023, Eni expects to reach an EBIT of €13 billion, with CFFO before working capital at replacement cost forecasted to come in over €17 billion, and over €69 billion along the plan period. This is particularly important because part of my investment thesis on energy companies is linked to their generous distributions which need to be supported by real cash flow and not by debt.

From 2023 to 2026 Eni expects capex to be around €37 billion, a 15% increase compared to last year's guidance which reflects both inflation and the need to accelerate and increase in scale of existing projects in the Upstream (Europe needs new gas sources quick!). However, even with this increase, Eni should have abundant cash to fund dividends, buybacks while keeping on deleveraging. Right now, Eni's capital structure sees less than €20 billion of long-term debt at 2.2% average cost thanks to the fact that 86% of the whole LT debt is at fixed interest. From its 2020 leverage of 31%, Eni is already down at 13% and it plans on staying in the range of 10-20% over the whole plan.

Distribution

A major news was Eni's new enhanced and simplified distribution policy. Last year the company had already instated a quarterly dividend instead of its semi-annual one. However, the distribution policy was somewhat complicated.

Now the criteria are much easier. Eni will distribute between 25%-30% of annual CFFO by way of a combination of dividend and share buyback. In case of particularly strong scenarios, investors can expect Eni to apply 35% of incremental CFFO to distribution. In a downside scenario, Eni will still have balance sheet and capex flexibility to protect its distribution.

To start at the right pace, Eni announced a 2023 dividend raise to €0.94 per share, a 7% increase on 2022, which will be paid in four equal quarterly installments, in September 2023, November 2023, March 2024 and May 2024.

In addition, investors will also see a new €2.2 billion share buyback in 2023, equivalent to around 4.5% of the current market cap. In total, we have a total return of around 11.5% for 2023.

Valuation

Although I think it is fair to discount Eni more than some other peers, due to its country risk, I still stick to the valuation I have already shared. A P/E of 3.6 is unjustified before its European peers that currently trade above a 6 and its North-American peers trading around a 10. Its EV/EBITDA multiple is a 2.1 which is quite low if we consider how strategic Eni will be in the future and how much gas it will handle while carrying it from Africa to Europe. In addition, last year Eni's revenue was the one that grew the most among the industry.

More importantly, Eni is able to achieve a higher return on total capital compared to most of its peers. In fact, it achieves a 19% versus 13.8% of Chevron (CVX) and Shell (SHEL). For sure, Eni can still improve on efficiency, scale and marginality. But, as we have seen, the company is well managed, not much levered and pursues strategic investments in key areas. Not much is going against it at the moment nor in the foreseeable future.

The stock is currently on a small dip and this could open up a buying opportunity.

For further details see:

I Am Long Eni: Dividend Raise And Key Role For Europe