WMT - I Blame Warren Buffett: 5 Dividend Aristocrats I Wouldn't Touch With A 10-Foot Pole

2023-10-18 11:54:12 ET

Summary

- Dividend investing is often oversimplified, leading to potential risks for investors.

- Warren Buffett's approach to buying quality assets at fair prices is misunderstood and misapplied.

- Here are five stocks which are not good dividend investments due to low yields and limited growth potential.

- I throw in a stock I think is a good buy (no extra charge).

Written by Sam Kovacs.

Introduction

I blame Warren Buffett for the misconceptions which plague investors throughout the dividend investing community.

How so? Just read on, it will become apparent.

Dividend investing is a great strategy... when done right.

A lot of the content found on the Internet about the strategy is extremely watered down and simplified in the approach, which puts the retirement prospects of dividend investors at risk, by encouraging them to not only buy stocks which are potentially overvalued, but by encouraging them to never sell.

The dividend investing approach championed online follows a few basic tenets, which can all be derived from sentences which Warren Buffett may have said at some point, tainted with some efficient market theory.

Let's take a closer look at some of his sayings.

A truly great business must have an enduring 'moat' that protects excellent returns on invested capital. -WB.

This, I have no issues with. Investing is not lottery picking. I wouldn't want to own a poor quality small business, why would I want to own shares of a bad quality public company?

Buying quality assets is a given for long term stock market investors, which dividend investors are.

Forget what you know about buying fair businesses at wonderful prices; instead, buy wonderful businesses at fair prices -WB.

This is where it gets more complicated. To further express how important it was to buy companies which had enduring competitive advantages, Buffett and Munger suggest it is better to buy wonderful businesses at fair prices, than fair businesses at wonderful prices.

This is part smart wordplay, and part to drive home the idea that wonderful businesses will create so much value over time that the creation of value will outpace the rerating of an undervalued business.

This is true, but it brings up a question which is often left unanswered: What is a fair price?

This is a question that many chose not to tackle. The thinking goes something like this:

These are wonderful businesses. They will generate tons of value. They have moats. 10 years from now, the price will be higher than today.

Therefore, whatever price the market offers is a fair price.

From here, the idea of DRIPping came. Let's just reinvest the dividends in the same companies regardless of the price.

All you really need to do is buy a diversified basket of dividend aristocrats, champions, or whatever cheesy label is being given these days, and you're set...or so the thinking goes.

This does contradict somewhat Buffett's other quote that says:

Whether we're talking about stocks or socks, I like buying quality merchandise when it is marked down. -WB.

And getting a discount is something which we believe is non-negotiable for success, more on that later.

Dividend investors can build a portfolio of 30-40 stocks overnight, as price is no concern, and they're set.

A pesky question does soon come into play... When should we sell?

Thankfully Warren Buffett, the investing god, has an answer to that as well:

Our favorite holding period is forever - WB.

Done, sorted, we'll never sell. That's his favorite holding period. So it's our favorite holding period.

Not so fast... consider that Warren Buffett also gave two scenarios in which he should sell.

1. We would sell if we needed money for something else -- I would reluctantly sell something terribly cheap to buy something even cheaper

2. We sell really when we think we're reevaluating the economic characteristics of the business. We probably had one view of the long-term competitive advantage of the company at the time we've bought it, and we may have modified that.

He would reluctantly sell something terribly cheap to buy something even cheaper. What about selling something overvalued to buy something cheap? It follows that this is sound logic which Buffett is all for.

But these scenarios are often ignored by investors who want simplicity over anything.

Simplicity is great, unless it comes at the cost of returns.

It doesn't take too many poor decisions to put your retirement nest egg in jeopardy.

We propose that dividend investing is done successfully if you:

- Buy low.

- Get paid a sufficient amount to wait.

- Sell high.

Let's now walk through a first example of how an investor following the simple buy and hold at whatever price approach would be tricked into making a good decision.

Walmart: so safe it hurts (your returns)

Walmart Inc. (WMT) is a stock which draws in some very vocal long-term fans.

I never really got why people become fans of digital ownership rights of companies. They serve us a purpose, which is to generate wealth. Stocks are not sport teams, and you shouldn't get emotional.

Walmart is often seen as the quintessential 20th century American Business. Grown from the ground up into this juggernaut which owns 25% of the American groceries business in dollar share.

The dominance and scale means that the company could beat its peers on pricing amid sky high inflation.

Reuters

The scale gives it a moat, and investors love this. It's a consumer staples company which is easily understood to the lay investor, which also helps a lot in its popularity.

The problem is, it barely qualifies as a dividend stock.

Dividend stocks must be sized up both on their dividend yield and their dividend growth potential.

What does this mean? A stock that pays a low dividend yield is acceptable provided that it grows the dividend at a high rate.

A low dividend growth stock is acceptable, provided that it pays a higher dividend yield.

There's a trade-off between dividend yield and dividend growth.

Walmart is one of those worst case scenarios where you get virtually no dividend yield, and no dividend growth.

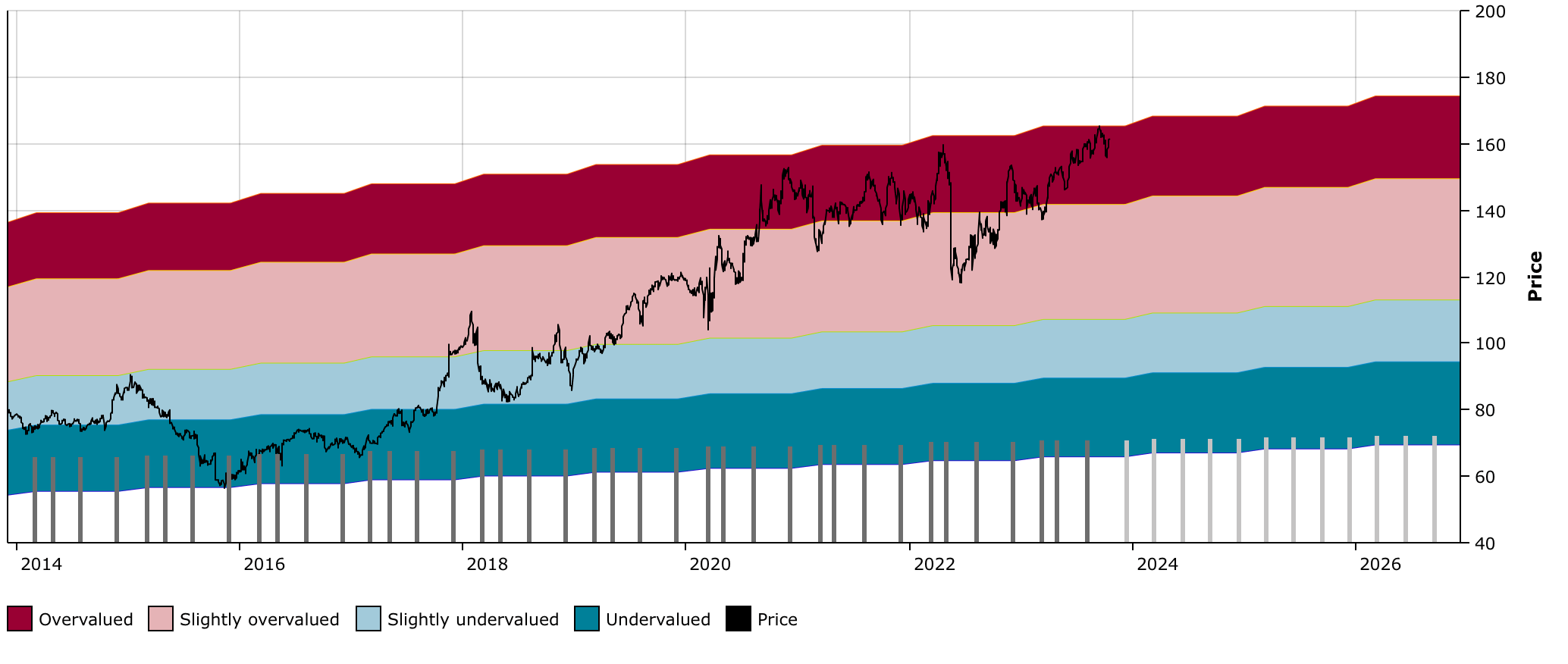

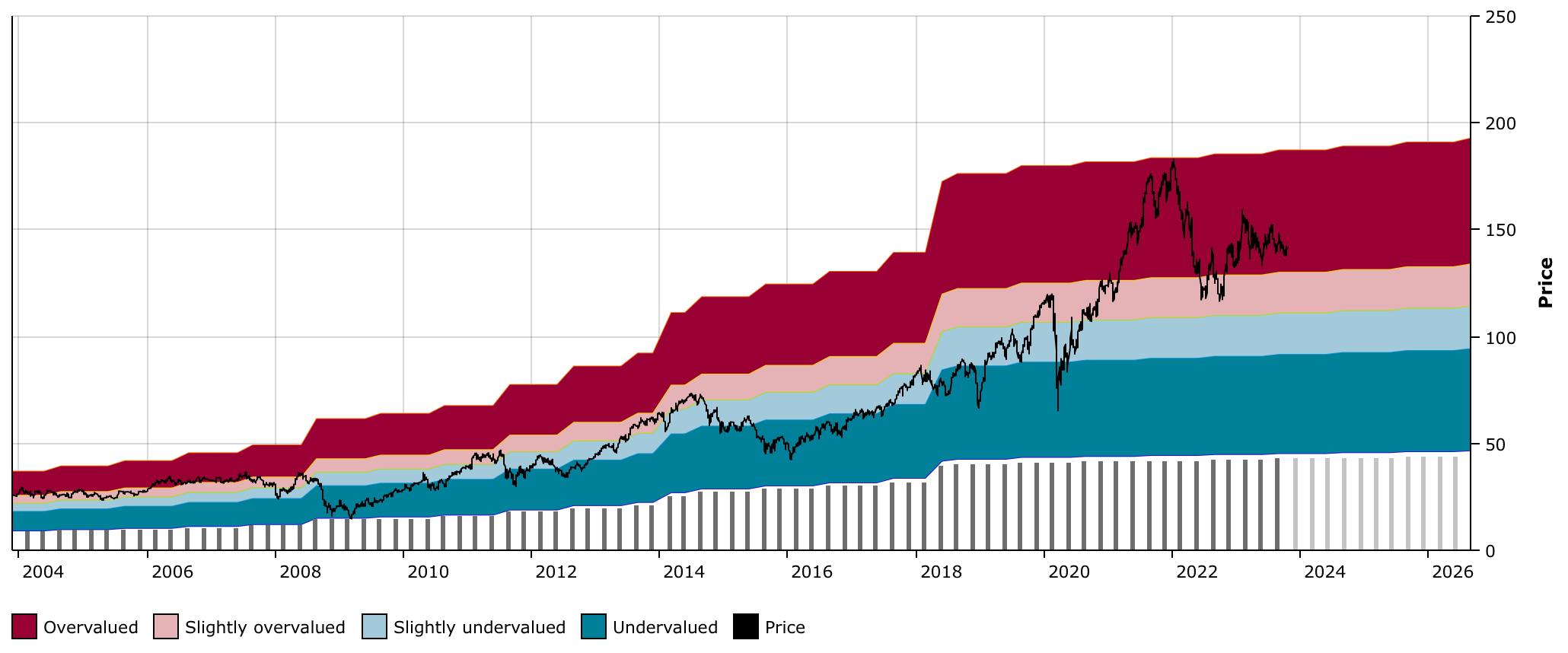

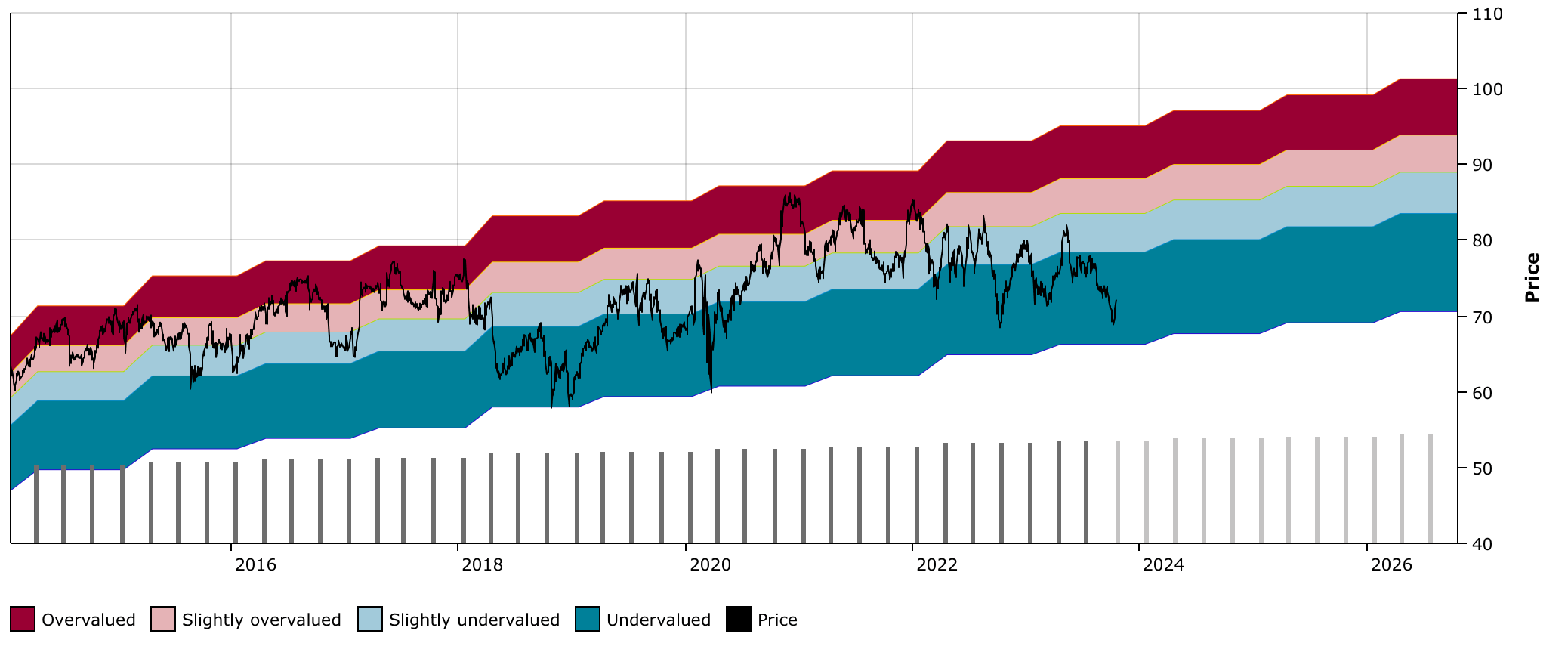

The stock currently trades at $161 and yields 1.4%. while the dividend has grown at a 1.8%-1.9% CAGR for the past decade.

{kind=link}

This is a yield well below the 10 year median 2.14% yield, which suggests that historically, it's not a fair price. Although, even if it were yielding 2.14%, given the utter lack of growth, it still wouldn't be a fair price relative to the income you're going to get.

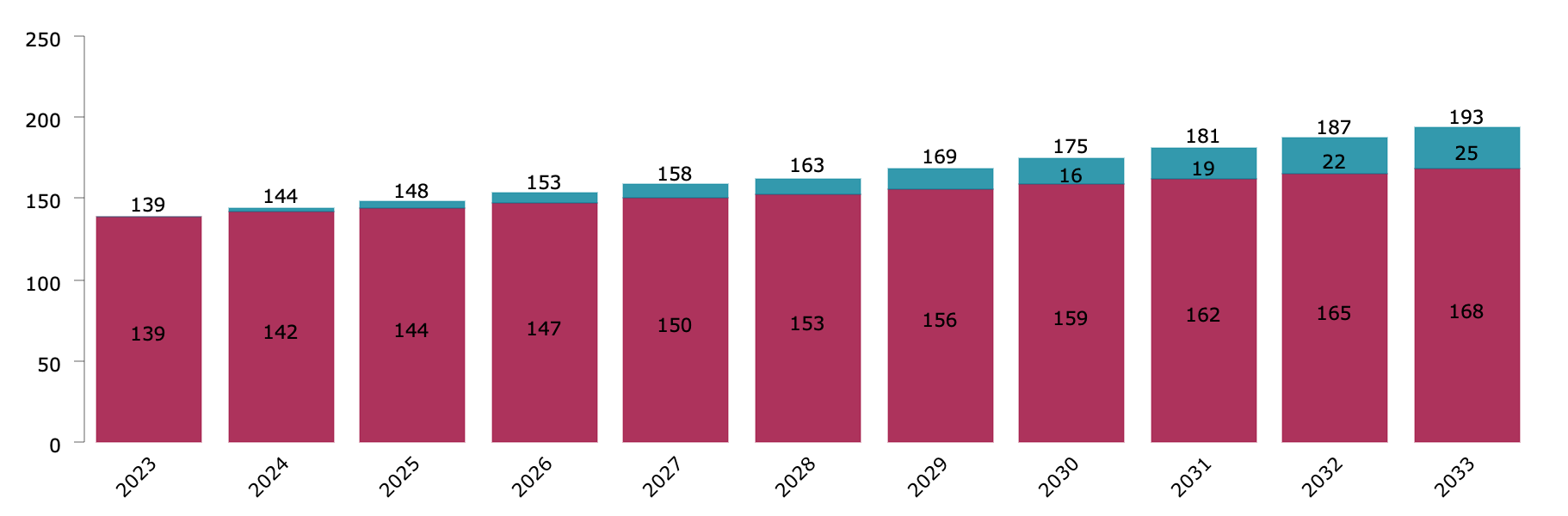

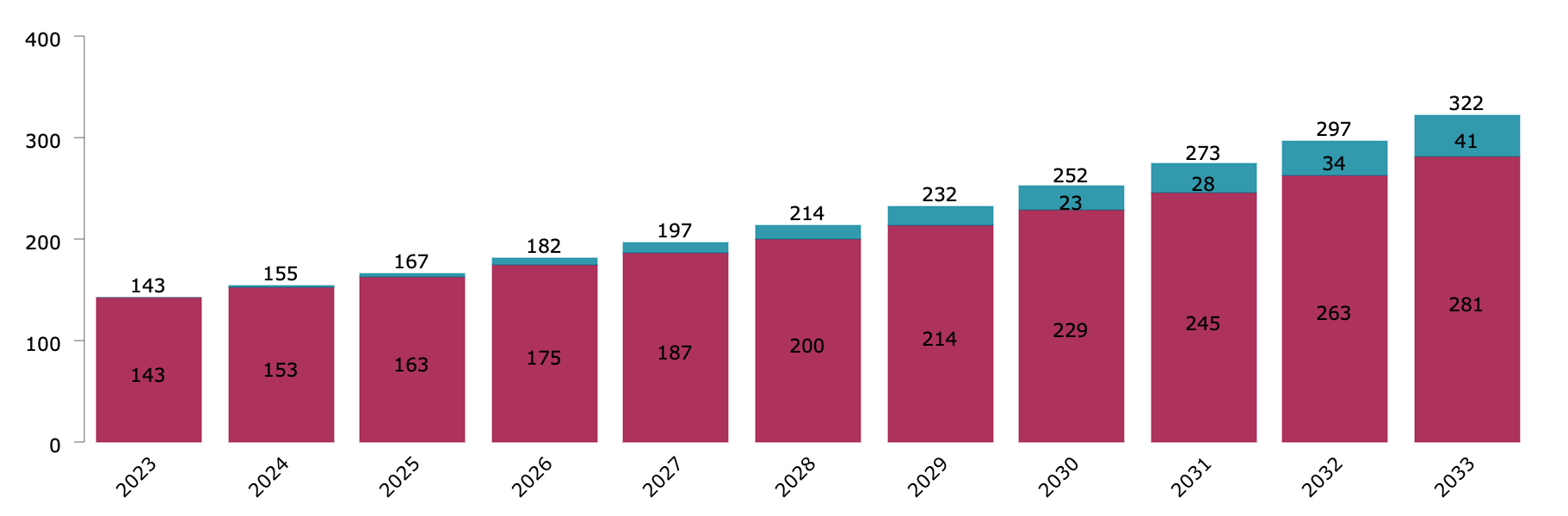

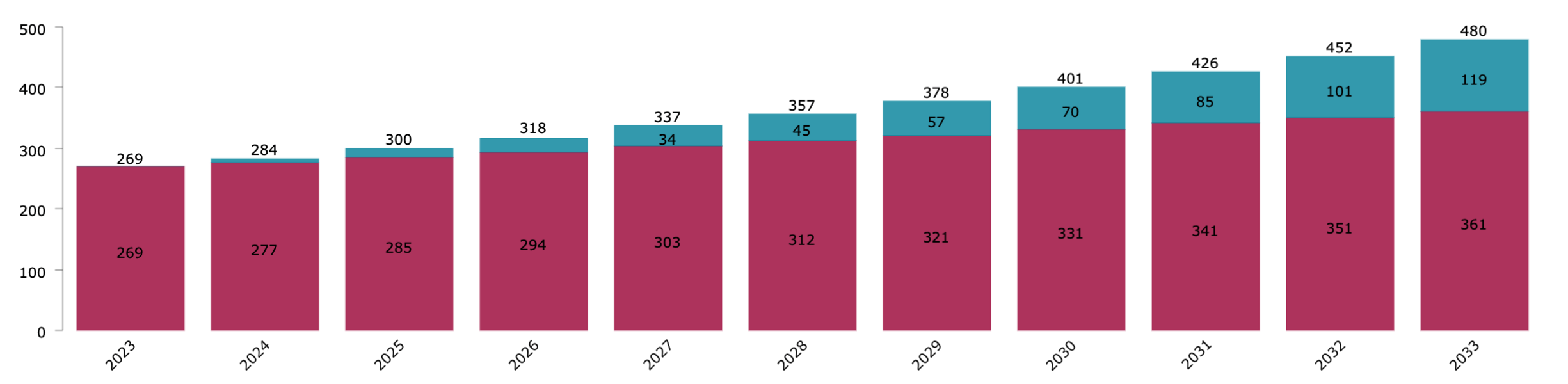

Let's look at it this way: if you invest $10K in WMT today, and reinvest dividends while it continues to grow the dividend at 1.9%, then 10 years from now you'll expect to receive $193 in annual income, or about 1.93% of your original investment.

{kind=link}

Now I don't think you need me to tell you this is awfully low.

If you had $2,000,000 worth of such stocks in 10 years, you'd only be getting $38,000 in income from it.

The prospects of WMT increasing its dividend at more than 2% per year in the future seem pretty low.

But here investors will say: But my WMT stock is up!

Now yes, that might be true.

But if you never sell: what difference does it make?

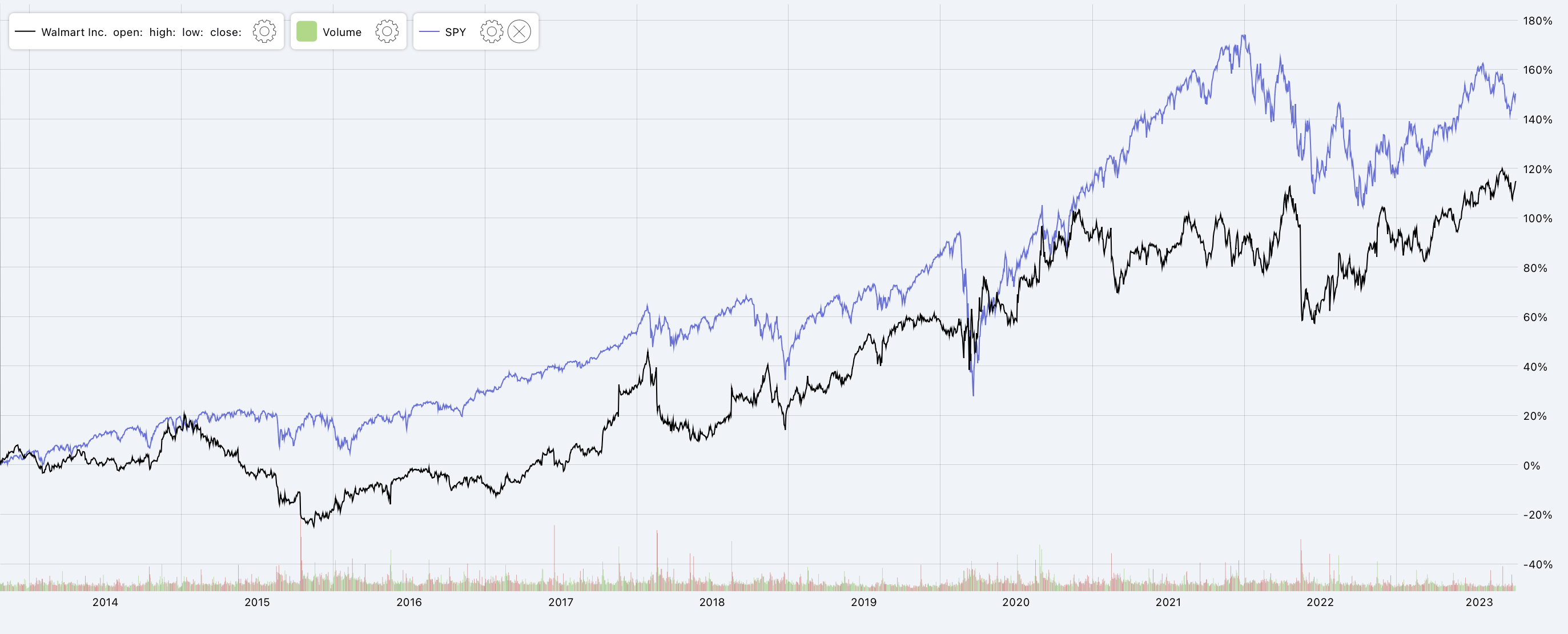

And even if you considered selling your stock to realize the gain, it doesn't take a genius to figure out that during the past 10 years, WMT has underperformed the S&P 500 (SP500).

{kind=link}

People will say that it goes down less in tumultuous times, but that is only because it doesn't fall from very high to start with.

In the current environment the whole "but it's a store of value" rationale doesn't make sense. You can get 4.7% on 5-year treasuries (US5Y), which is more than triple the income from WMT.

Consumer staples have had a bad year, with the sector down 9%. WMT, on the other hand, is up 12%.

Its valuation is at odds with the market, at odds with its dividend, at odds with its peers, you're not likely to get massive growth from the stock.

One must ask... unless you're a fanboy, why own the stock?

Can you really expect management to change their mind and start growing the dividend at double digit rates? I doubt it. Even if they did, could they maintain growth which outpaces the business growth for a long time? Of course the answer is no.

What is a good dividend return?

This should bring an important question up:

What is a good level of income 10 years down the line? And why 10 years down the line?

Well for one, most of us should expect to still be alive 10 years from now (my crude estimates suggest 88-90% of the current population will still be alive 10 years from now), so it is not so far in the future that it is irrelevant.

It is also far enough that we can clearly visualize the compounding effect of dividend growth over time, which should inform our decisions if we are long term oriented investors. Small differences over 3 years can amount to huge differences over 10 years.

And we set what we believe to be good income opportunities based on experience, a lot of simulation running of different peoples income and savings profiles, coupled with projected retirement spending.

What we've found is that 8% income on your original investment 10 years from now, is the base acceptable level of income.

Anything above 10%, is great.

That means if you invest $10K today, if you can get $800 from that investment per year in 10 years, you're doing good. If you can get $1,000 you're doing great. If you get more than $1,000, you're paying for our drinks.

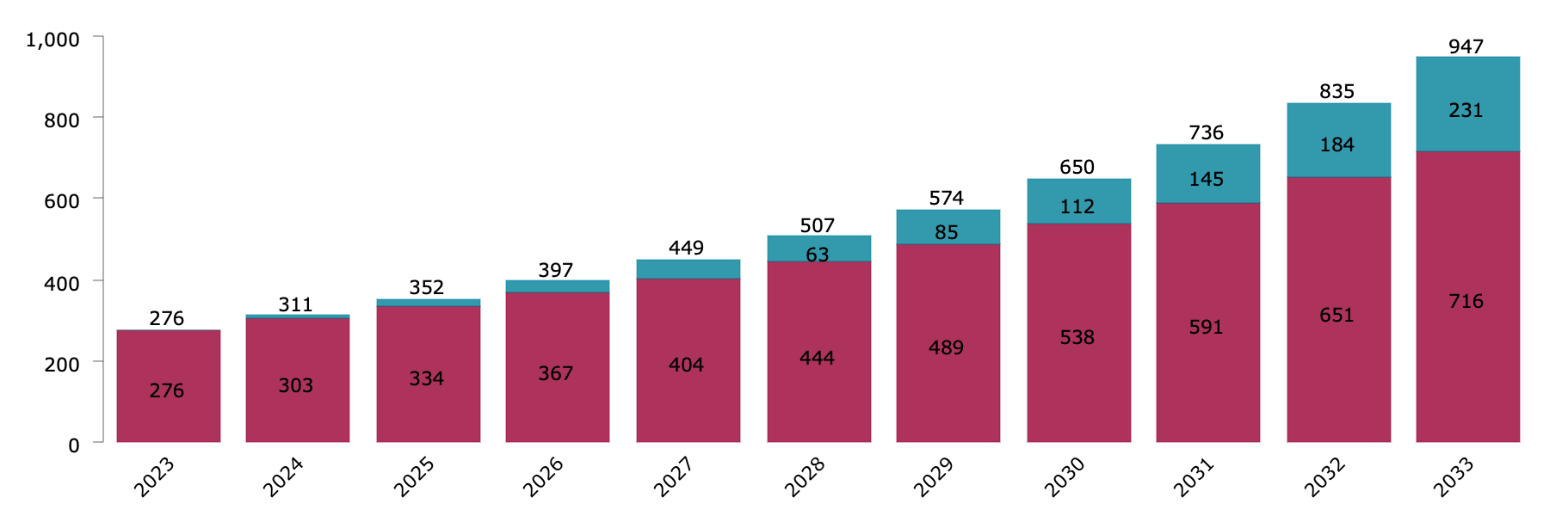

So, if you take a stock like The Home Depot (HD), for instance, and you do the same $10K simulation investing at a 2.8% yield and assuming 10% dividend growth per year, then you'd expect $947 in income per year in year 10, which is quite attractive.

{kind=link}

Now not too many people are arguing that HD is a worse business than WMT; in fact, many might suggest just the opposite. Yet your income profile would be much better.

HD is still on our buy list.

But that's enough about stocks which are good buys, we're here to talk about stocks to buy only if you HATE money.

More dividend stocks to buy if you hate money

There are loads of these stocks that pass for dividend stocks, when in fact they neither have the yield nor the growth to remotely be on our radars.

Dover Corporation (DOV) is one such stock.

Dover makes and sells a wide range of specialized products and components for various industries. These products range from things like fuel pumps at gas stations, equipment to print designs on shirts, refrigeration systems for supermarkets, and many other unique tools and machinery for different industries.

The business model is somewhat more difficult to understand than WMT's, as you usually don't yourself shop for a fuel pump or other random pieces of machinery.

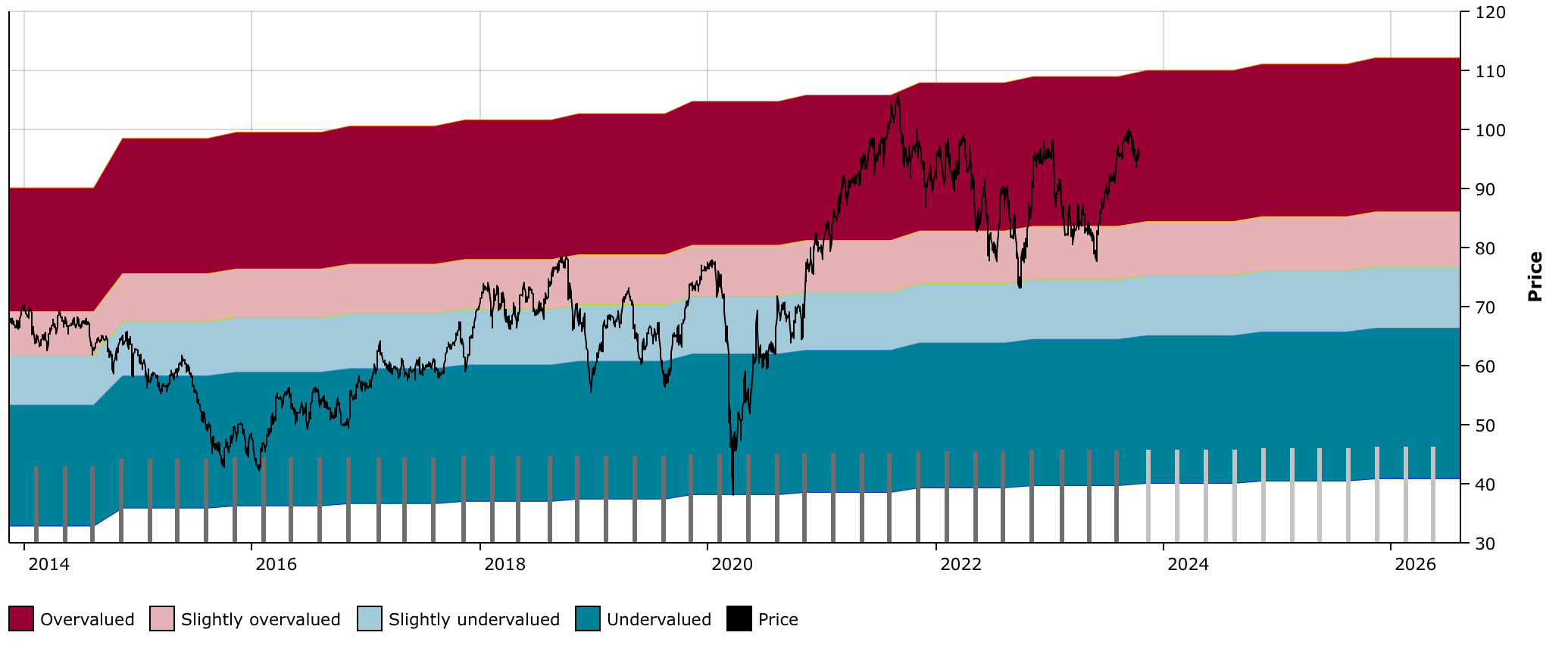

The stock now trades at $141, and yields 1.4%.

During the past 2 decades, it has yielded a median 1.8%, a number which again isn't justified given the rate of dividend growth.

{kind=link}

During the past 5 years, the dividend has grown at just a 1.2% CAGR, which guarantees poor dividend outcomes just as we saw with Walmart above.

But investors don't quite get how high the growth rates need to be for stocks with such low yields.

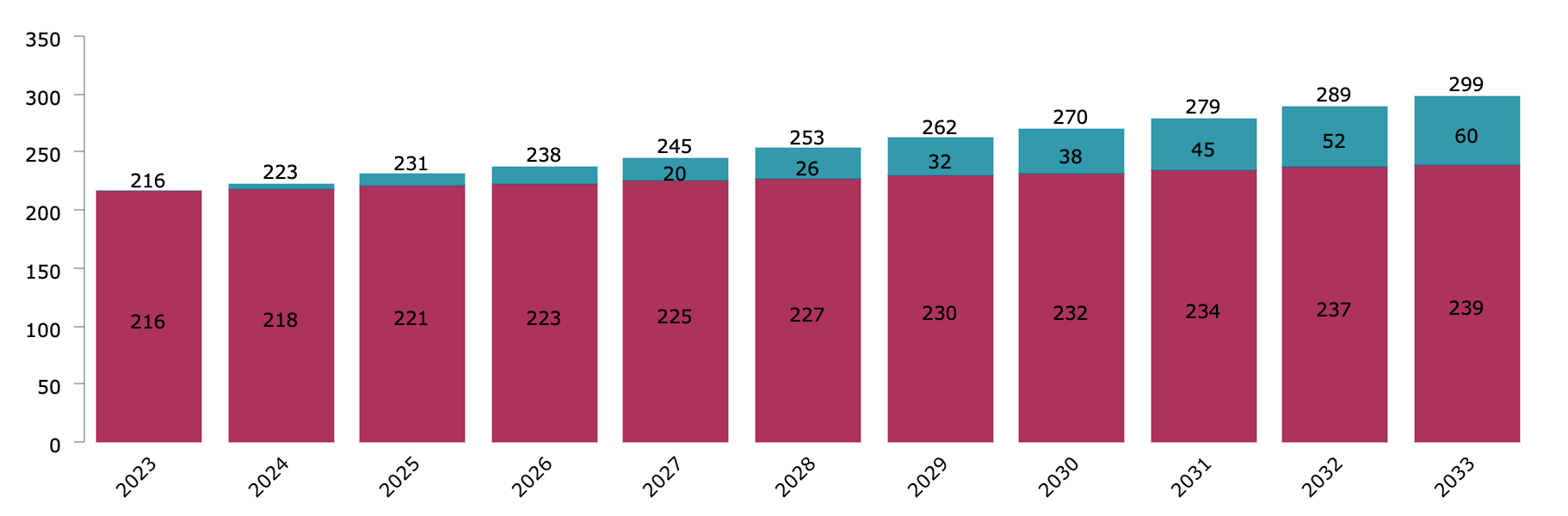

Even if DOV could achieve 7% dividend growth over the next decade (matching its 10 year CAGR, which was front loaded in the first part of the past decade), then investing $10K today and reinvesting the dividends would result in an annual income of $322 ten years from now.

{kind=link}

This is still a very poor 3.2% of your original investment.

For stocks which yield as little as 1.4%, you'd need 17% growth per year to get to the target $800 in 10 years on a $10K investment, or 20% to get to that $1,000 in 10 years.

Emerson Electric Co. (EMR) is another you should avoid like the plague. At the current price of $96 it yields 2.16%, and its dividend growth rates have been declining as time goes by.

{kind=link}

During the past 5 years, the dividend growth rate averaged 1.4%. This year it was 1%. Where will EMR find the will or the way to increase its dividend by more than it does, when the market doesn't seem to care?

No point in showing the income chart, you know it will look bad, but for the sake of it: $10K in EMR today with 1% dividend growth, income in 10 years will be $299 per year, or 3% of your original investment.

{kind=link}

Colgate-Palmolive (CL) is another such stock.

It currently trades at $72 and yields 2.6%. Unlike the three stocks mentioned above, it trades at a price which gives it a higher yield than its 10 year median yield (2.3%).

{kind=link}

But this is why it's an interesting example. It might look "cheap" relative to its historical dividend yield, and even its historical P/E, but it is not cheap relative to the income that you can expect from the stock.

I recently wrote a "free" article about why CL was a bad dividend investment.

(To understand what free means and how it differs from the rest of our content, check this article out ).

Below is a snippet from that article:

The problem is that Colgate is both a low yield stock, and a low growth stock.

During the past 10 years, its dividend has grown at a CAGR of 3.5%. During the past 5 years, that number dropped to 2.7% and just 2.1% last year.

For the sake of the example, let's say they manage to get the future dividend growth back to 3% for the next decade.

Let's simulate the dividend income you could expect from a CL investment over the next 10 years.

If you invest $10,000 in Colgate today, and reinvest the dividends you receive while the dividend grows at 3% per year, then 10 years from now...

...you'll expect to receive $480 in annual income.

That's 4.8% of the original investment...10 years from now, which is considered extremely mediocre.

{kind=link}

The last stock I'll bring up is one that isn't quite as bad as the others, and that I'd actually buy if it returned to its poorest valuations in the past decade (a time when I did in fact buy the stock).

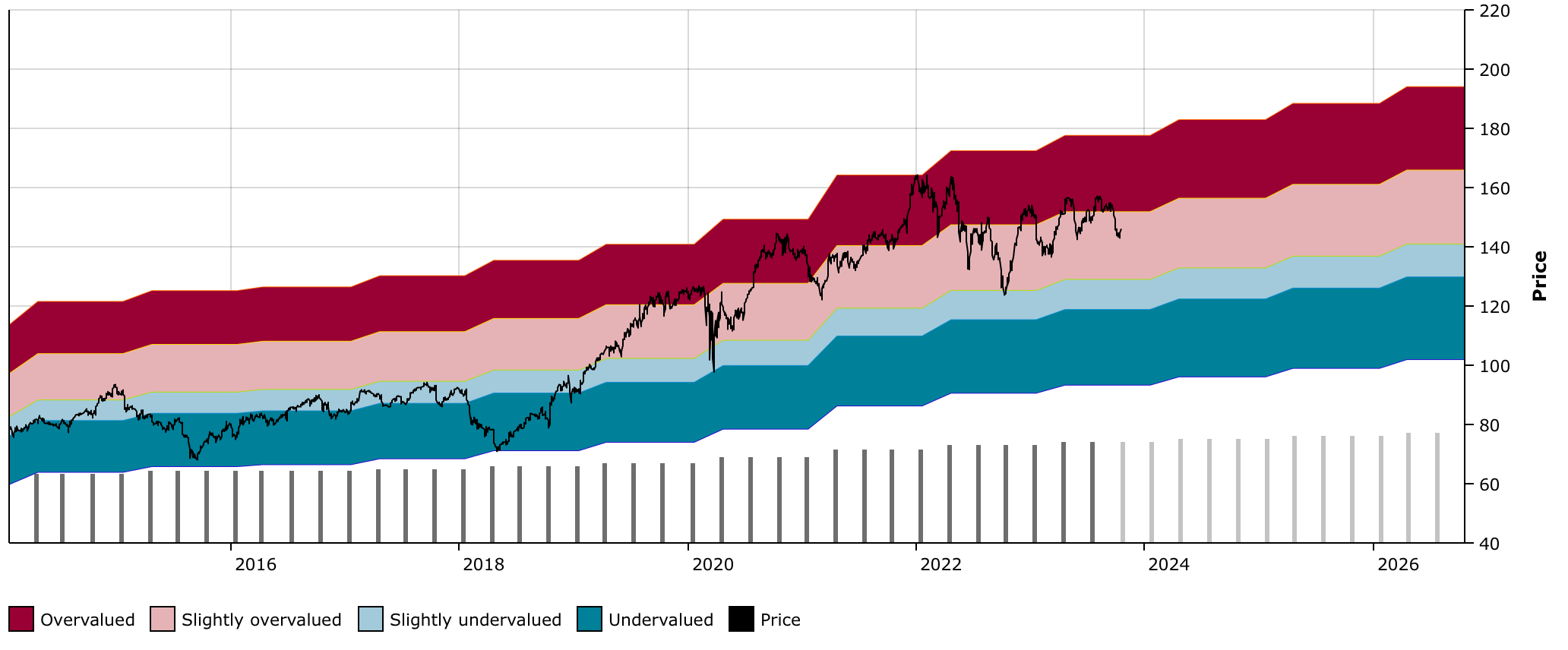

It's The Procter & Gamble Company (PG).

PG currently trades at $146 and yields 2.57%. This is somewhat less than its 10 year median yield of 2.9%.

{kind=link}

During the past decade, dividend growth has averaged 4.6%. During the past 5 years it has averaged 5.6%, boosted by the higher increases during pandemic years. This year it increased just 3%.

I believe PG can likely continue to increase the dividend between 4 and 6%. Let's call it 5%.

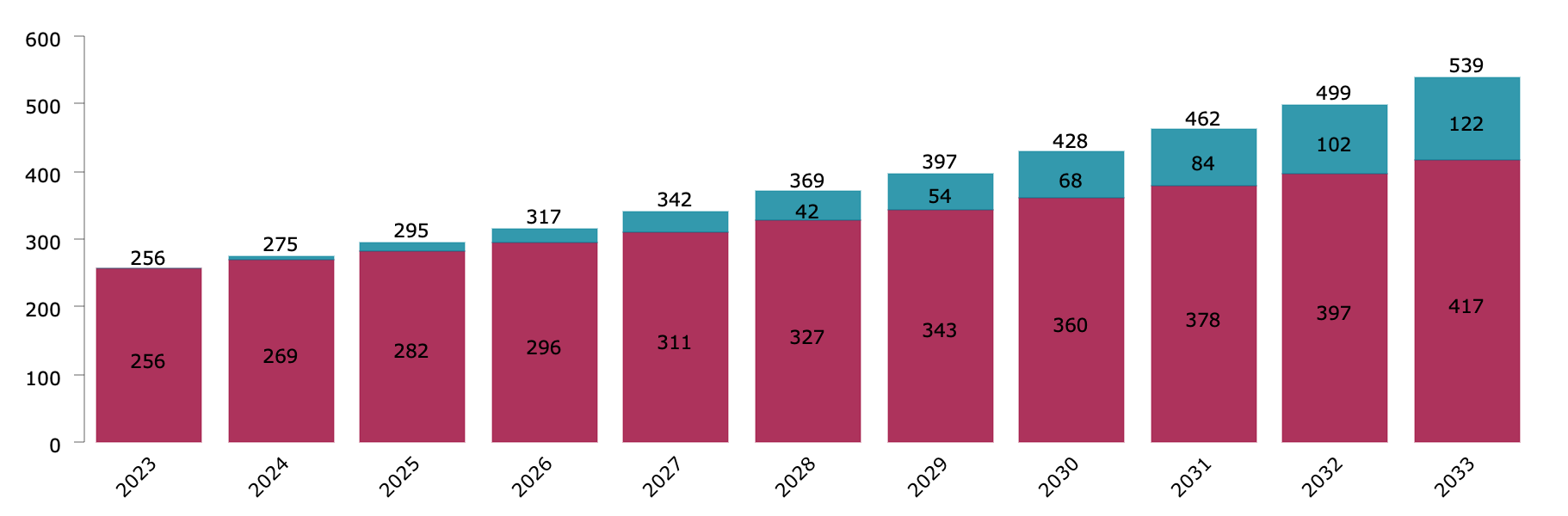

If you bought $10K now and reinvested your dividends, assuming 5% growth, then 10 years from now you'd expect $539 in income per year.

{kind=link}

That's 5.4% of your original investment, which is edging closer to our minimum accepted goal of 8%, but still, it's no good.

It's like you're a 4 foot 1 point guard who wants to join the NBA. You're still a 50% growth sprout short of even remotely having a shot.

But in the past, PG has yielded as much as 4% or very close to that level.

If it were to return to that level, then it is likely that I'd change my mind, but in the meantime, no puedo .

Conclusion: Bracing myself

Anytime I tell dividend investors to stay away from stocks which don't provide attractive combinations of both income and growth potential, I get the Internet version of a mauling.

I fully expect the same this time. For some reason, saying "Sell WMT" has the same ring for some investors as if I told a New Yorker that the Knicks are terrible. (Well, they are terrible, but that's another discussion).

We advocate against getting attached to your stocks. They serve a purpose. They're wealth-creation vehicles. If they cease to effectively be that, switch out the stock for something better.

Whatever you do, don't base your investment philosophy off a few quotes you heard out of context.

For further details see:

I Blame Warren Buffett: 5 Dividend Aristocrats I Wouldn't Touch With A 10-Foot Pole