NVR - I Disagree With Buffett Buying Lennar And D.R. Horton

2023-08-16 09:23:16 ET

Summary

- Berkshire Hathaway's 13F filing reveals that Warren Buffett has added homebuilders to his portfolio.

- Despite high mortgage rates, homebuilders have been performing well and outperforming the S&P 500.

- I dislike the current risk/reward, as margins are under pressure, building permits are contracting, and economic risks are elevated.

Introduction

It's 13F time again!

The Securities and Exchange Commission's ("SEC") Form 13F is a quarterly report that institutional investment managers with at least $100 million in assets under management are required to file.

While we're dealing with lagging info (funds may have sold it already), it allows the masses to take a look behind the curtain of major funds.

This includes Berkshire Hathaway ( BRK.A ).

The Oracle of Omaha made some interesting moves that caught some attention - as they usually do.

{kind=link}

Google News

As we can see in the overview below, the only investments he added were homebuilders!

- He bought 6 million shares of D.R. Horton ( DHI ),

- 11 thousand shares of NVR ( NVR ), and

- 150 thousand shares of Lennar ( LEN )

However, it's not a massive bet. D.R. Horton, the biggest addition to his portfolio, accounts for just 0.2% of his portfolio.

Additionally, Bloomberg makes the case that the world's richest investor is becoming a more active investor.

Recent disclosures from Berkshire related to its stock portfolio revealed a departure from its long-held strategy of buying shares and holding them for the long term. Berkshire revealed a stake in Taiwan Semiconductor Manufacturing Co. last year, only to largely rotate out of that position in subsequent months.

Having said all of this, let's dive into the homebuilders, as there's a lot to unpack. For starters, homebuilders are doing extremely well, despite high rates.

Additionally, Buffett isn't a bottom buyer in this situation, as he's buying after a significant surge.

Homebuilders - The Place To Be?

In the past few quarters, we've spent a lot of time discussing homebuilders, as we might be dealing with the most fascinating homebuilding trend in decades.

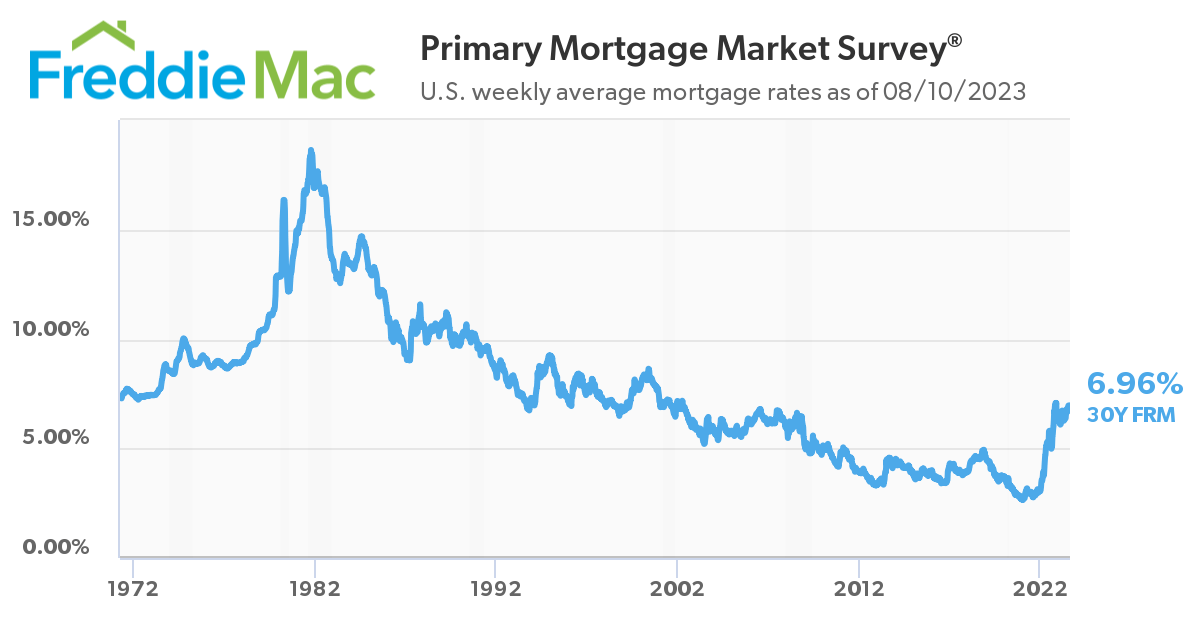

Using Freddie Mac data, we see that mortgage rates are at 7% (30Y fixed). This is the highest level since the early 2000s.

{kind=link}

Freddie Mac

This is a response to the Fed's consistent hiking cycle to control elevated inflation since 2022.

What's so fascinating is that homebuilders are doing just fine.

Looking at the chart below, we see that homebuilders have outperformed the S&P 500 by a huge margin since 2018.

Bloomberg

Furthermore, looking at the chart below, we see that homebuilders ( ITB ) had a tough time when rates started to accelerate in early 2022. However, they started to gain significant upside momentum when rates rose from 3% to 4%.

In this case, I'm using 10Y government bond yields as a proxy.

Historically speaking, homebuilders tend to do well when rates are declining. That's what triggered a massive rally in 2019 (and after the Great Financial Crisis).

That thesis is easy: lower rates make it more attractive to purchase homes, which increases demand and results in more orders for homebuilders.

Right now, the thesis is different. Rates are so high that existing homeowners aren't willing to sell their homes. They know that if they want to buy other properties, they may have to take on a very expensive mortgage.

As of August 6, the number of new listings is down 16% year-on-year.

Redfin

Another chart that perfectly shows the current trend is the share of new single-family home sales of total sales. At the start of the second quarter, that number was close to 35%. The longer-term median is close to 15%.

Wall Street Journal

Unfortunately, cracks are starting to appear.

Homebuilders Are On Increasingly Thin Ice

While I wouldn't make the case that homebuilders are in danger, they are increasingly in a tricky spot.

For example, homebuilding stocks could suffer the moment housing supply increases.

Higher supply could be triggered by a decline in interest rates.

- For example, if the economy weakens so much that the Fed is forced to cut rates, it could trigger a situation where homeowners start selling their homes.

- Related, if economic growth is weak, potentially higher unemployment may force some people to sell, which could trigger a domino effect of rising supply.

Eventually, the central bank will start to cut rates. While the timeline of that easing remains unclear, a decline in borrowing costs could reinvigorate existing homeowners to place their homes back on the market, introducing more inventory.

“Ironically, if rates went significantly lower from here, it could juice demand a little bit, but you also might have a lot of competition coming in from the resale side of things,” Oppenheimer & Co. analyst Tyler Batory said. - Bloomberg

I have heard a number of comments from major funds that are waiting for unemployment to rise before jumping back into the housing market. I believe their strategy may turn out to be correct.

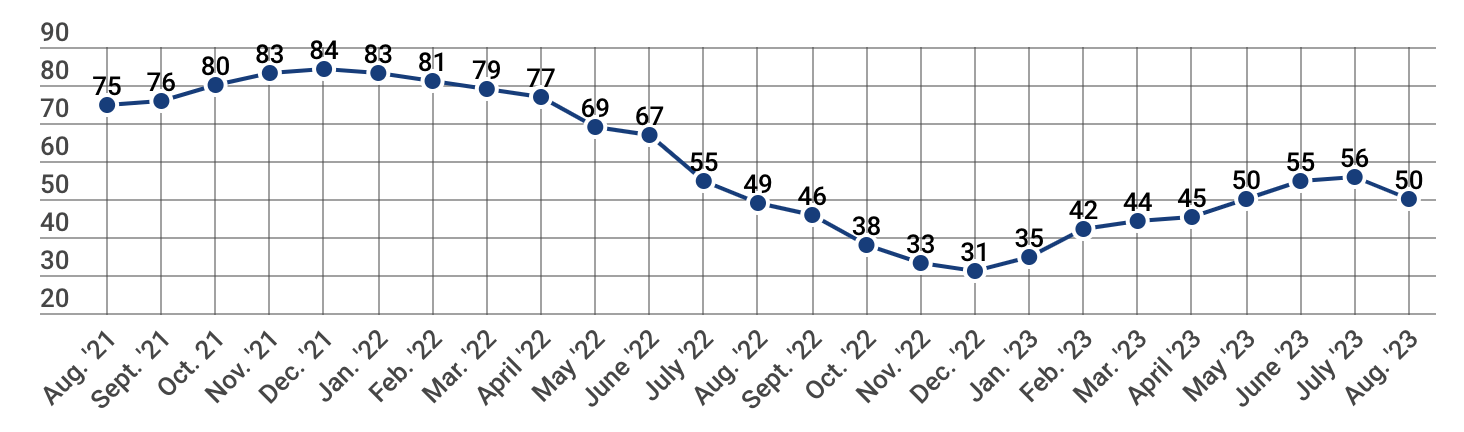

On top of that, we're now seeing a decline in builder confidence due to rising mortgage rates.

In August, the National Association of Home Builders/Wells Fargo Housing Market Index fell to 50. That's the first decline since December 2022.

{kind=link}

NAHB/Wells Fargo

Essentially, the decline is the result of high construction costs and a lack of skilled labor. Low housing affordability is still a bullish driver of demand.

“ Rising mortgage rates and high construction costs stemming from a dearth of construction workers, a lack of buildable lots and ongoing shortages of distribution transformers put a chill on builder sentiment in August,” said NAHB Chairman Alicia Huey, a custom home builder and developer from Birmingham, Ala. “But while this latest confidence reading is a reminder that housing affordability is an ongoing challenge, demand for new construction continues to be supported by a lack of resale inventory , as many home owners elect to stay put because they are locked in at a low mortgage rate.” - NAHB

However, we also see that due to high rates, homebuilders are forced to use incentives to attract potential buyers.

The August HMI survey also revealed that rising mortgage rates are causing more builders to use sales incentives to attract home buyers . After dropping steadily for four months (from 31% in March to 22% in July), the share of builders cutting prices to bolster sales rose again to 25% in August. The average decline for builders reducing prices remained at 6%. - NAHB

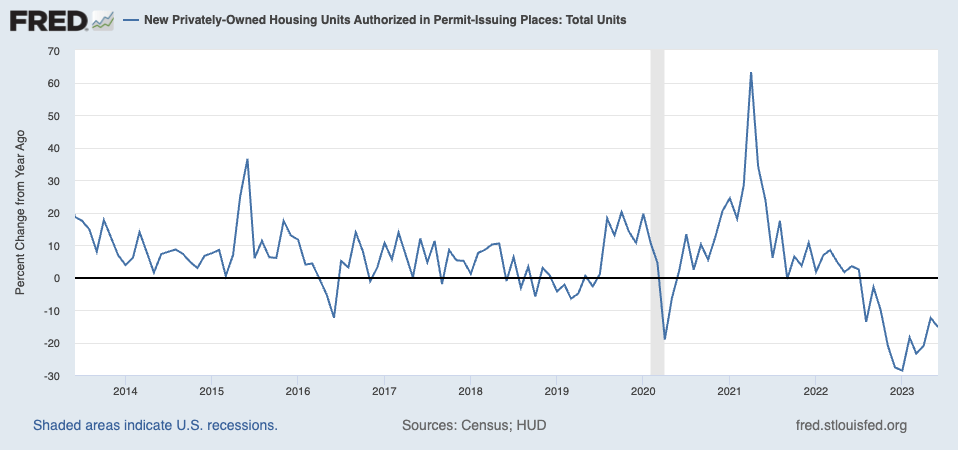

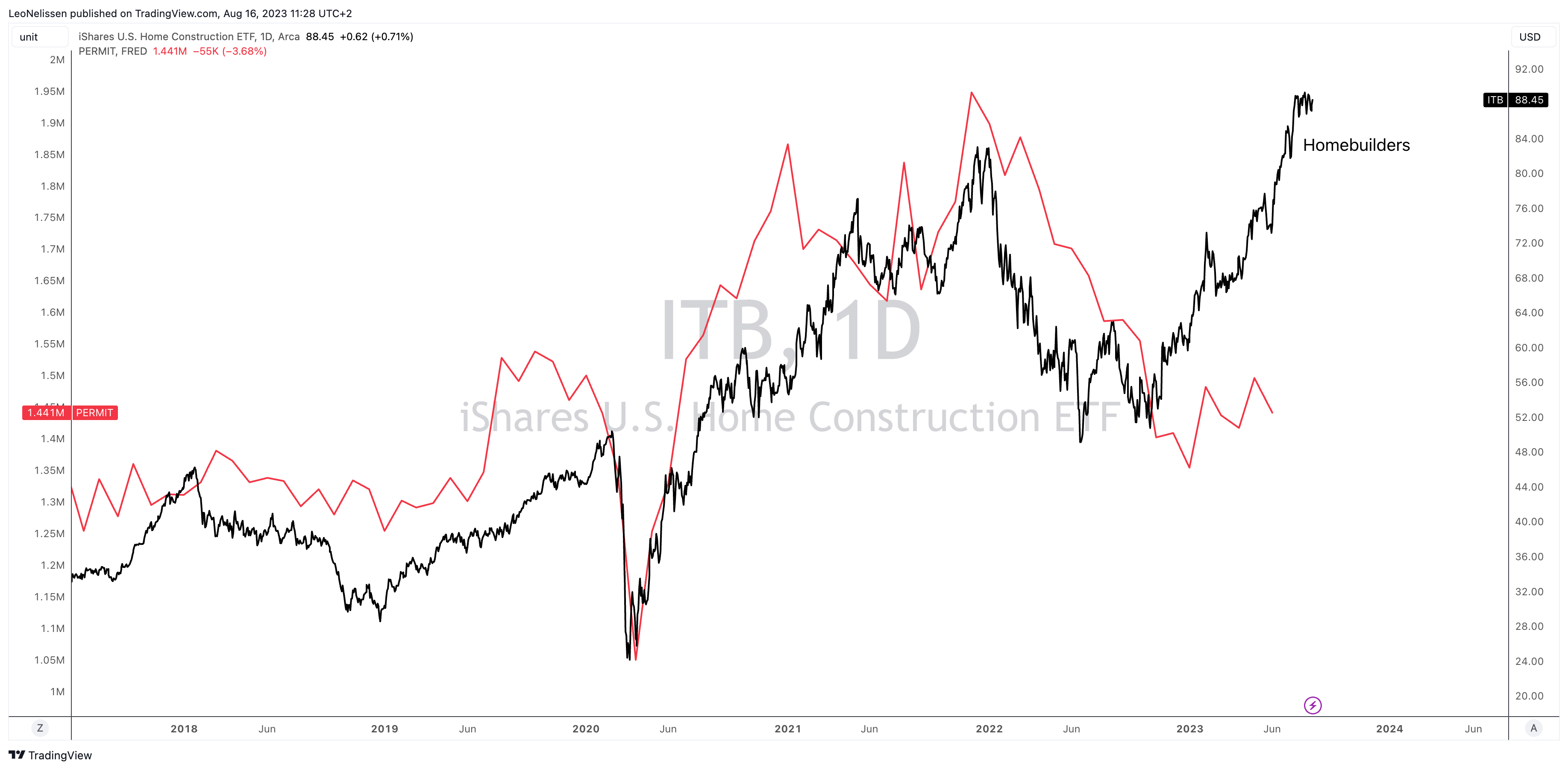

On top of that, it needs to be said that building permits continue to decline, an indicator that homebuilders are not accelerating production.

{kind=link}

Federal Reserve Bank of St. Louis

When comparing homebuilding stocks to building permits, we see a wide divergence. It seems that the only reason why homebuilders are still doing so well is the hope that elevated rates will eventually cause demand to increase.

{kind=link}

TradingView (ITB, Building Permits)

Additionally, pricing is a big factor.

The median sales price is now higher than in 2022, which indicates that home builders are able to benefit from strong pricing power.

If that erodes, we could see more weakness.

Redfin

Using the data so far, I cannot make the case that Buffett is betting on the wrong horse. However, it's also not an investment with a great risk/reward ratio.

If rates remain elevated, we could see severe economic weakness, which could trigger home sales (higher supply) if unemployment rises.

In other words, an event where forced selling could occur is what worries me the most - not just in homebuilding but as an economic risk in general.

Also, if rates fall without a recession, supply increases as well. It won't likely crush homebuilding stocks, but it will stress the risk/reward.

Having said all of this, let's look at some of the stocks Buffett bought. After all, he bought some giants that tell us a lot about the homebuilding industry.

D.R. Horton - The Affordability King

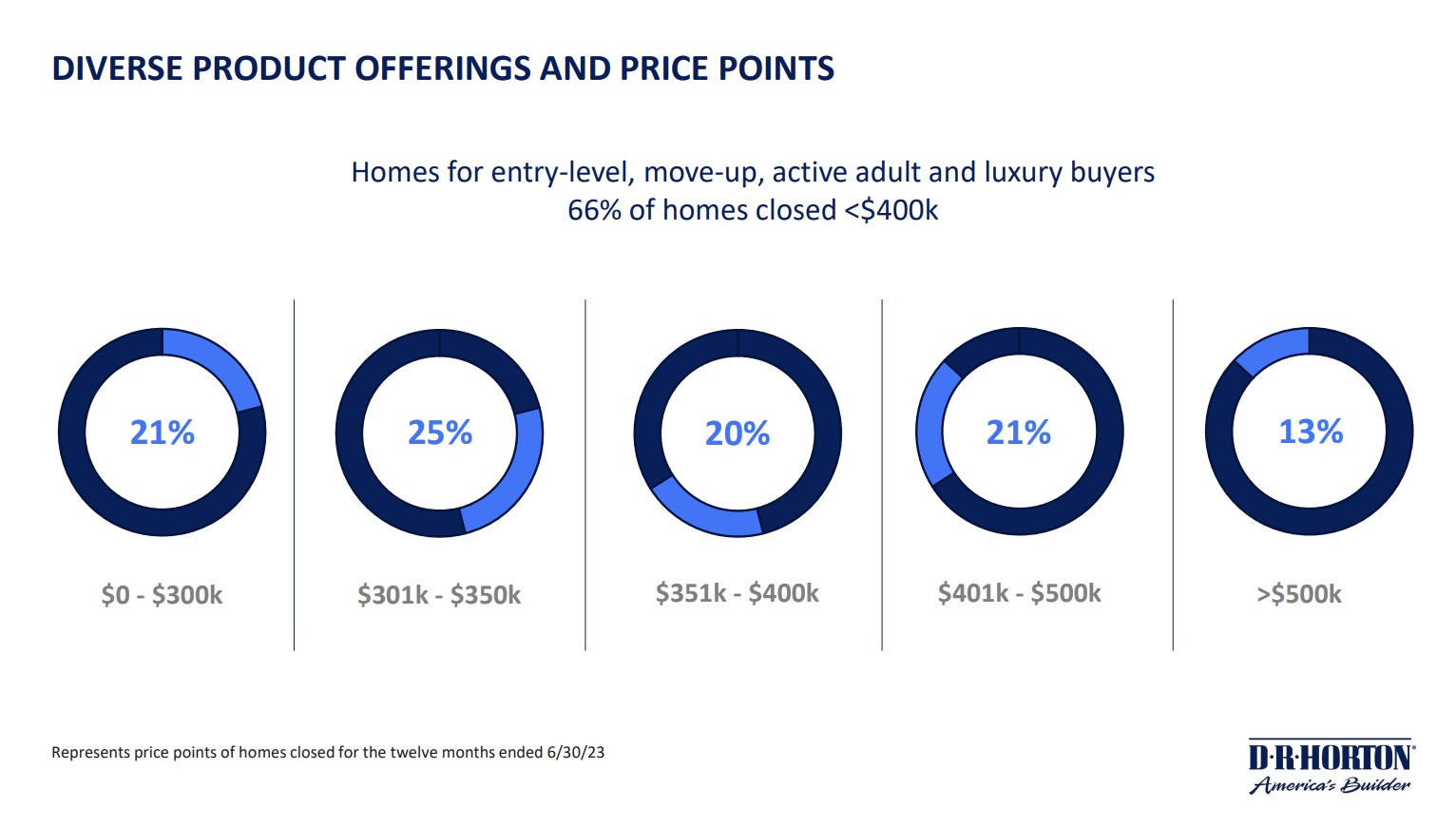

With a market cap of $43 billion, D.R. Horton isn't just America's largest homebuilder but also a homebuilder with a focus on affordable homes.

Close to 70% of its homes were sold with a price tag of less than $400 thousand. A fifth of its homes sold for less than $300 thousand.

{kind=link}

D.R. Horton

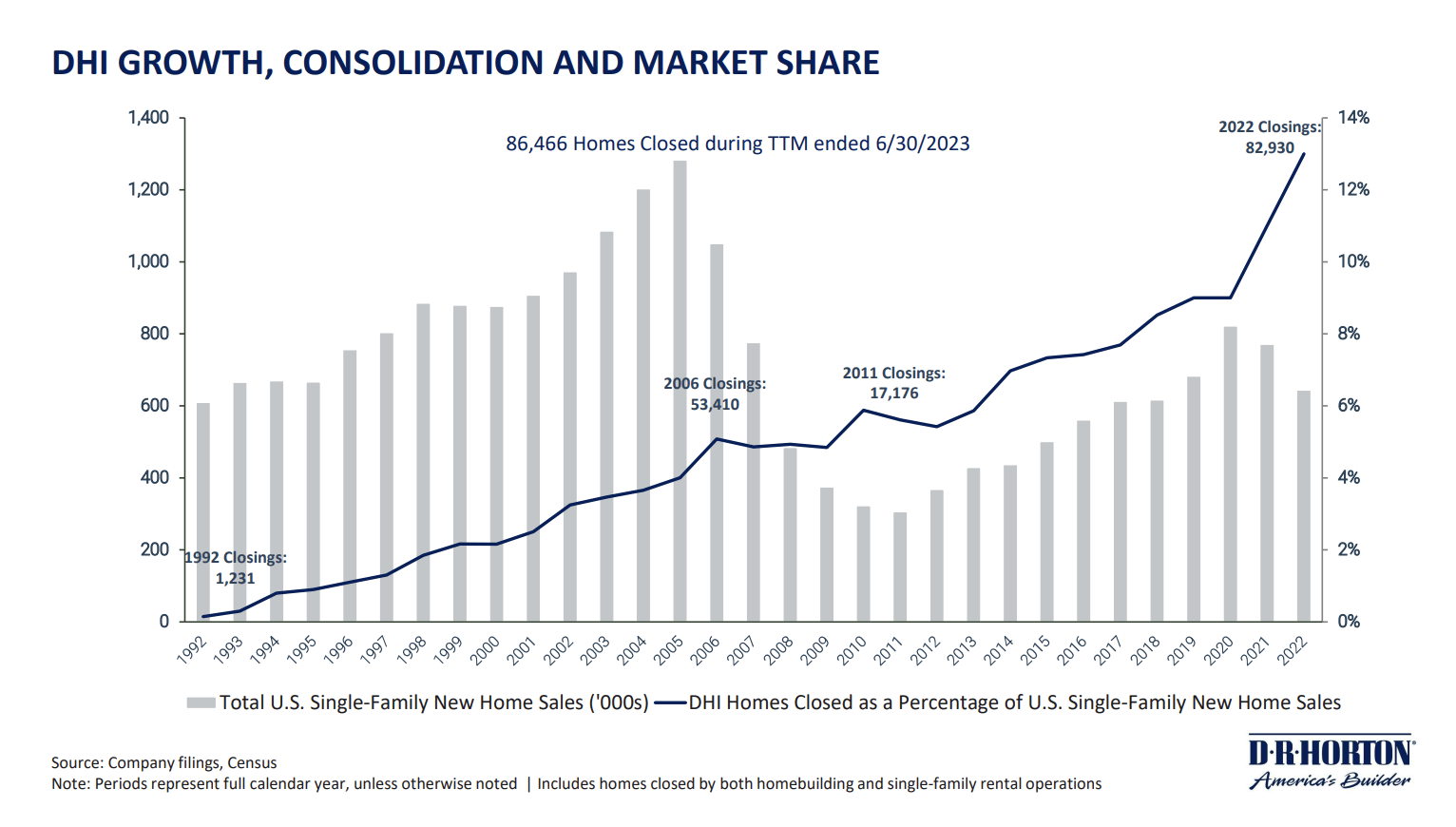

Thanks to an emphasis on the biggest issue since the Great Financial Crisis (affordability), the company was able to boost its market share to almost 14% - that's up from 6% in 2011.

{kind=link}

D.R. Horton

As a result, DHI shares have returned 639% over the past ten years, beating the market and homebuilders by a wide margin.

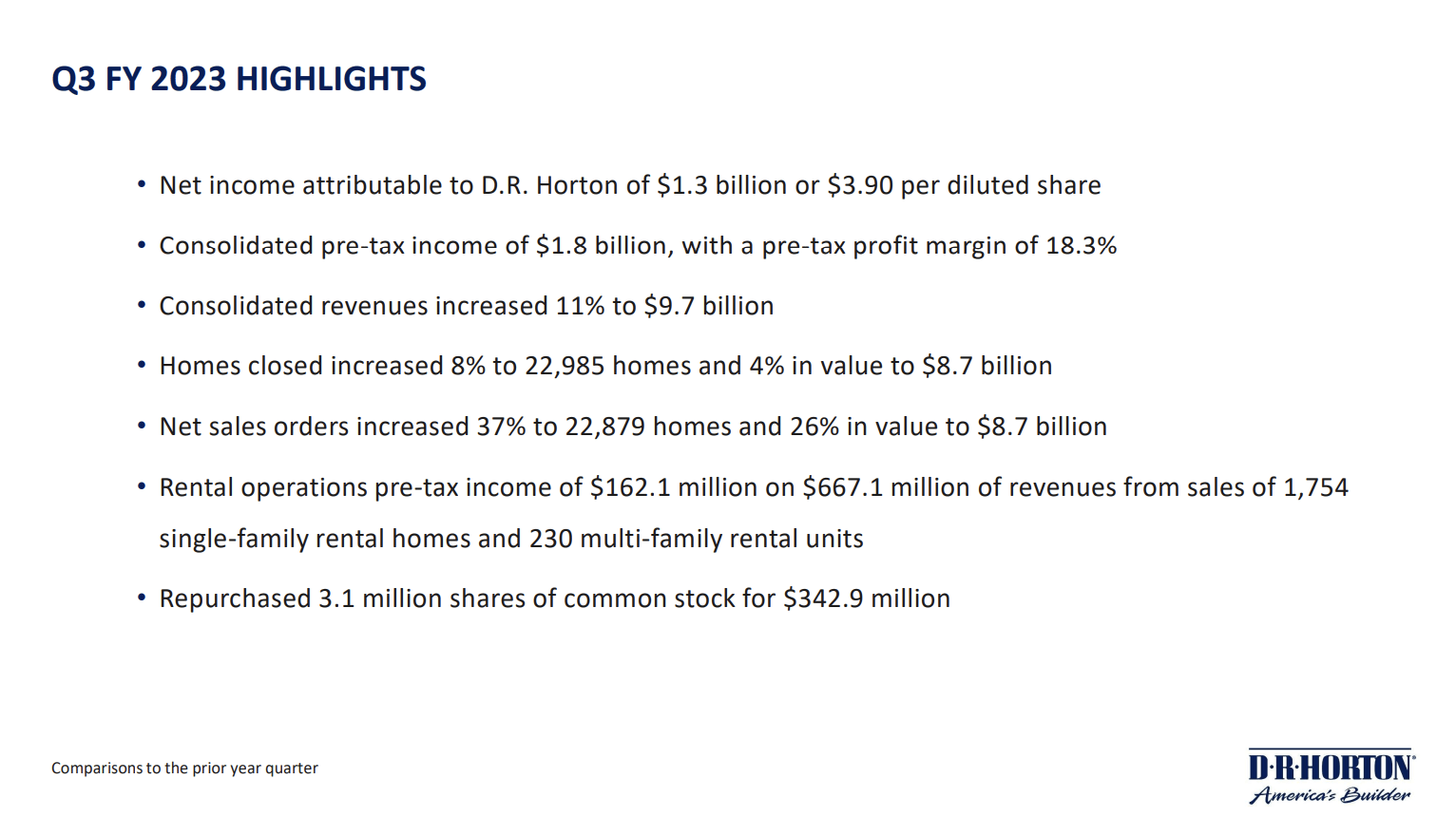

In the third quarter of the fiscal year 2023, the company reported strong numbers.

Despite challenges like high mortgage rates and inflation, net sales orders grew by 37% compared to the prior-year quarter, driven by limited affordable housing supply and favorable demographics.

{kind=link}

D.R. Horton

The company's strategic focus includes increasing market share and capital efficiency, with improvements in labor capacity and construction cycle times.

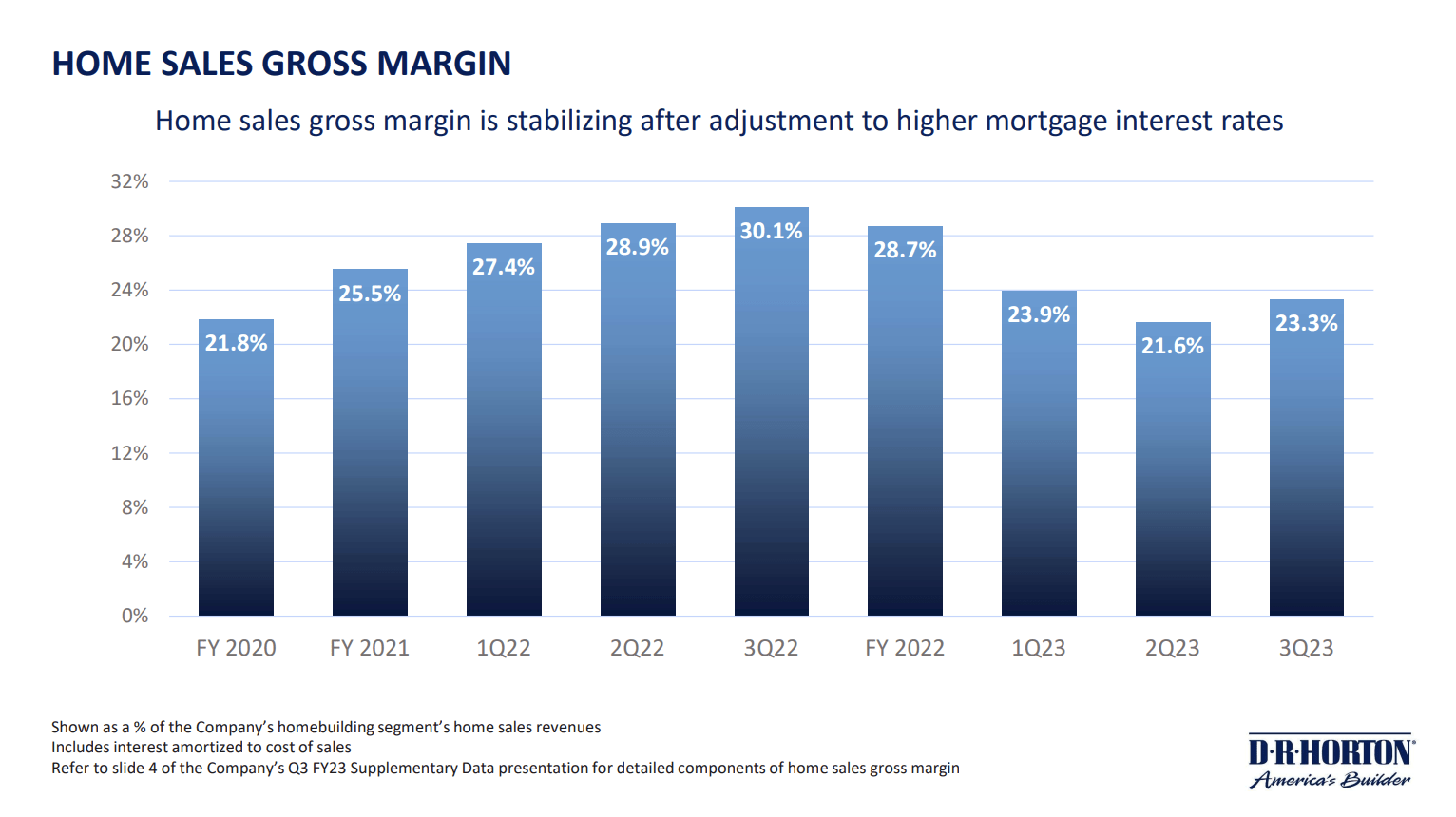

However, homebuilding operating margins faced pressure due to cost inflation and pricing adjustments to address homebuyer affordability challenges resulting from higher mortgage rates. These developments make sense with regard to the incentives we discussed in the first part of this article.

{kind=link}

D.R. Horton

The good news is that sequentially, margins improved from the March to June quarter as home prices and incentives stabilized, coupled with some reduction in construction costs.

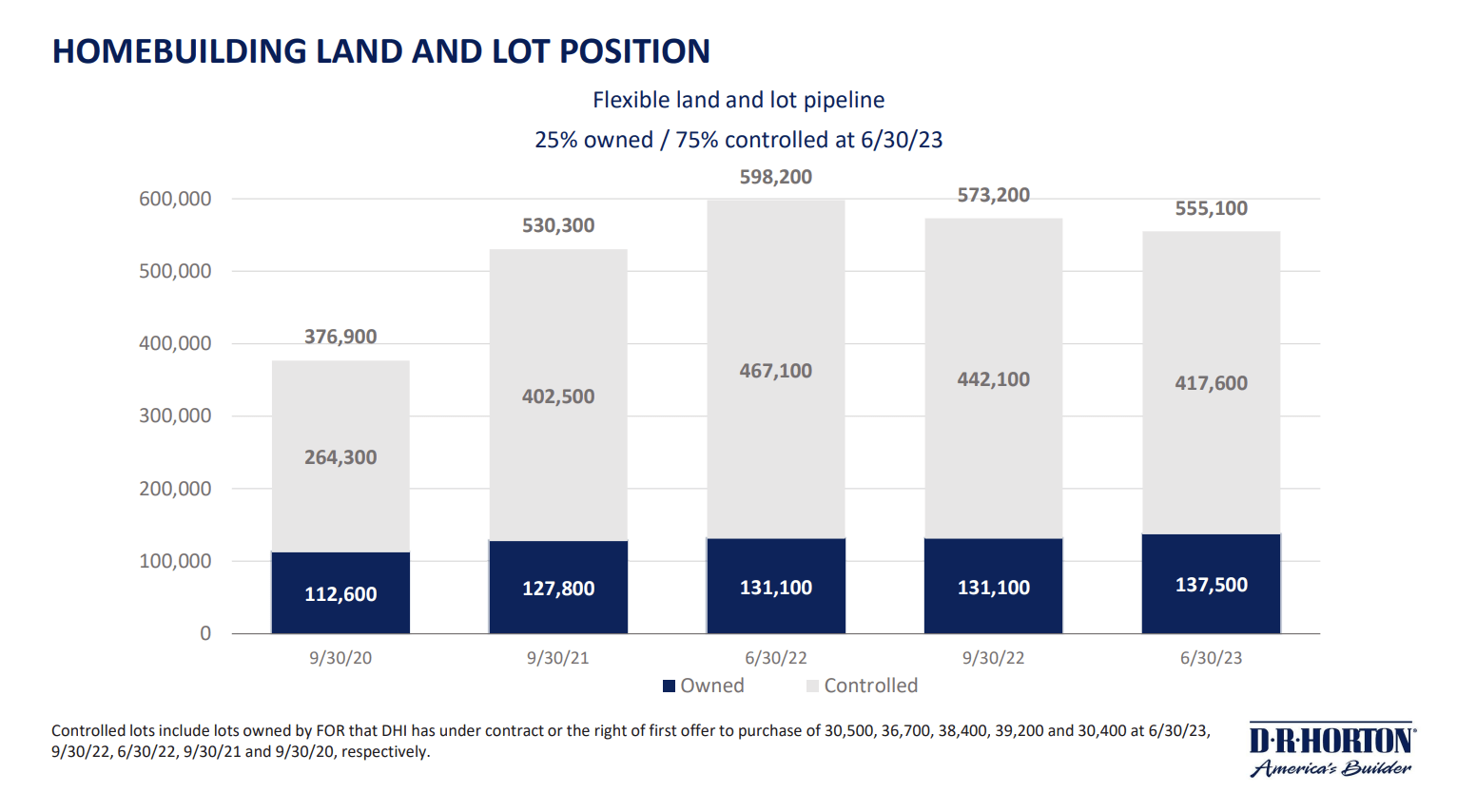

Furthermore, the company is increasingly flexible. At the end of the third quarter, the company owned roughly 555,000 lots. Only a quarter of these lots were owned. The remaining lots were controlled through options.

{kind=link}

D.R. Horton

Looking forward, D.R. Horton anticipates continued uncertainty in the market, influenced by factors such as mortgage rates and economic conditions.

Adding to that, for the full fiscal year, the company expects:

- To close between 82,800 and 83,300 homes, generating consolidated revenues in the range of $34.7 to $35.1 billion, and

- Cash flow from operations is projected to exceed $3 billion, with

- Share repurchases approximating $1.1 billion.

Valuation-wise, we're dealing with a 7.4x forward EBITDA multiple, which isn't overvalued, but also far from undervalued.

The current consensus price target is $143, which is 13% above the current price.

At these levels, I rate DHI shares a Hold . That's mainly based on my view on economic risks and the fact that DHI shares are up 42% year-to-date.

FINVIZ

This brings me to stock number two.

Lennar Corp. - An All-around Homebuilder

With a market cap of $36 billion, Lennar isn't far behind D.R. Horton.

What's interesting about Lennar is that prior to the accelerating migration from states like California, New York, and Illinois to the Sunbelt, it already had a strong focus on states like Florida and Texas. In 2019, these two states accounted for almost half of its sales.

{kind=link}

Lennar Corp.

Furthermore, the company has had a focus on entry-level buyers for many years, which is one of the segments that lack supply.

With that in mind, the company's 2Q23 earnings were reported on June 13.

In its earnings call, the company highlighted that the current economic environment had stabilized, with customers adjusting to higher interest rates and supply chain disruptions normalizing.

Notably, Lennar also mentioned that housing inventory remained limited across the country, which it attributed to a chronic housing supply shortage.

This shortage led customers to stretch their finances for housing, supported by incentives and price reductions. Again, D.R. Horton reported the same.

Hence, despite persistent inflation, the company believes that the market has adapted to more measured rate movements.

In this environment, the company's strategy includes attractive pricing and compelling mortgage rate programs to capture this demand (discounts).

During its earnings call, the company emphasized the use of a dynamic pricing model and the Lennar machine to determine market-clearing prices and maintain a balance between starts and sales.

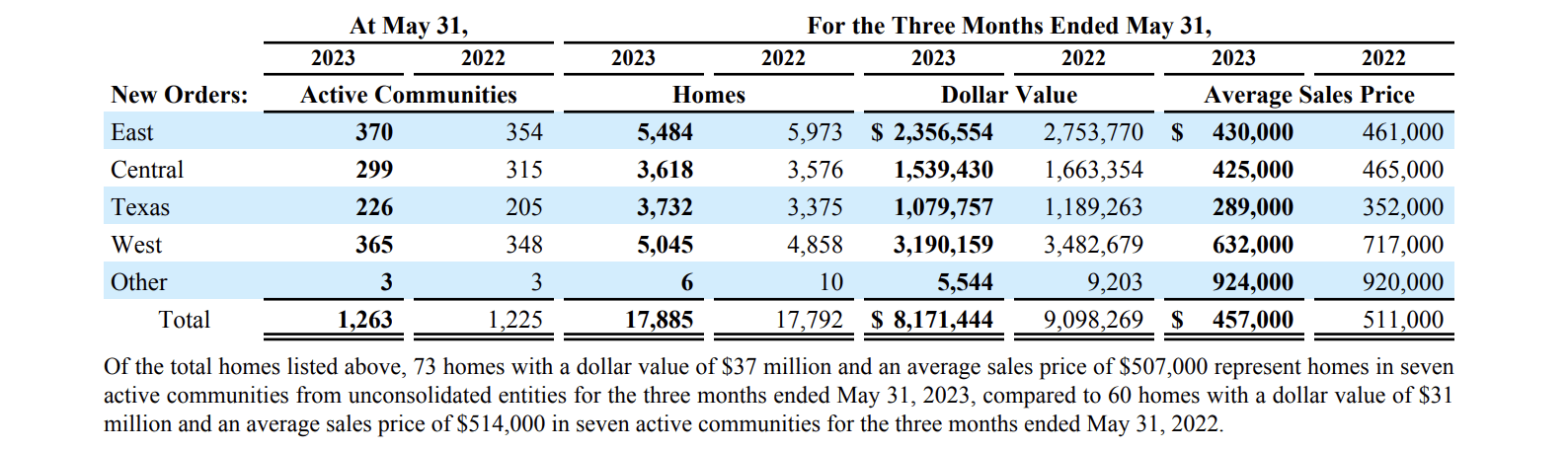

The second quarter results highlighted the success of the price-to-market strategy.

- New sales orders increased by 1% from the prior year and 26% from the first quarter, with sequential growth each month during the quarter.

- The community sales pace averaged 4.8% in the second quarter, reflecting stabilization and normalization across markets.

{kind=link}

Lennar Corp.

Lennar's focus on using price and incentives to achieve sales targets led to favorable results, increasing market share.

Additionally, the company's markets are categorized into three types: performing well, performing but requiring adjustments, and markets requiring aggressive adjustments. There were no markets in the third category during the second quarter.

The community count increased by 3% from the prior year, and further growth is expected by the end of fiscal 2023. Community count growth is particularly anticipated in the fourth quarter.

Moreover, just like D.R. Horton, Lennar saw s steep decline in gross margins as a result of its aggressive strategy to attract buyers in this environment.

Gross margins on home sales were $3.0 billion, or 21.9%, in the six months ended May 31, 2023, compared to $3.9 billion, or 28.4%, in the six months ended May 31, 2022. During the six months ended May 31, 2023, gross margin decreased because revenues per square foot decreased year over year as the Company priced homes to market and costs per square foot increased primarily due to higher materials and labor costs. In addition, land costs increased year over year. - Lennar 2Q23 Earnings

Next month, the company will report its third-quarter earnings. In that quarter, the company expects to deliver between 17,750 to 18,250 homes.

The projected gross margin for this period is expected to be between 23.5% and 24.0%.

On a full-year basis, the company has revised its delivery expectations upwards. It is now targeting between 68,000 to 70,000 homes, compared to the prior guidance of 62,000 to 66,000 homes.

This adjustment reflects the company's confidence in its operational capabilities and market positioning.

With regard to its valuation, LEN isn't overvalued. The stock is trading at 7.1x NTM EBITDA.

The current consensus price target is $138, which is 10% above the current price. I agree with that.

However, given my view on the economy, I rate LEN shares a Hold .

Takeaway

As much as I like both LEN and DHR, the companies are in a tricky spot. They can only continue the current growth streak if the housing supply remains low.

I also expect that margins will remain under pressure as interest rates have not yet come down.

As most homebuilders have almost doubled from their 52-week lows, I believe the risks of forced selling caused by potential economic stress make new investments at these levels unattractive.

Hence, I assume Buffett bought builders at lower prices in the past quarter. I also do not expect him to hold these investments for the long term.

Needless to say, this isn't an article to scare anyone out of homebuilding stocks.

I'm just sharing my view on the bigger picture here. The risks outlined in this article also explain why I'm building a bigger war chest to buy attractive housing-related plays on weakness.

For further details see:

I Disagree With Buffett Buying Lennar And D.R. Horton