OXLC - I'm Betting On America With 18% Yields: OXLC

2024-01-14 11:30:00 ET

Summary

- Election years historically provide strong returns in the market.

- Default rates remain below 2% and likely won't exceed 3% in 2024.

- I am long on the U.S. economy and getting a massive 18% yield.

Co-authored by Treading Softly.

2024 is set to be an important year for many different reasons. One, we'll see whether or not the long-awaited and expected recession will arrive or the Federal Reserve will successfully pull off a soft landing. Secondly, we're all focused on November with the increase in election news and election advertising throughout the year – the U.S. election process is a lengthy one and a big one. It also typically has impacts on not only the economy but also on the stock market itself. Historically, election years are good market years, with the majority of the time being that the market receives positive returns regardless of who is elected. Source .

ftportfolios website

Well, different economic events may have bigger impacts on a portfolio. Interest rates are a huge factor for those invested in startup growth companies that need a lot of capital upfront and burn through a lot of cash. Lower interest rates, if they were to fall, would be a huge benefit to them. For fixed-income investors, default risks and interest rates have a bigger impact overall than election years. But overwhelmingly, during an election year, all eyes get glued on an election.

When it comes to the market, I'd like to have a strong level of exposure, simply because I learned that through innovation, dogged determination, and the patriotism of the average citizen, the U.S. economy is a place that I want to have continual, strong exposure to. One way I do this is by investing in the debt that maintains the entire economy through all of the various private and public companies in existence.

Today, I want to look at one fund that allows you to have exposure to a vast array of debt that comes from across the entire U.S. economy.

Let's dive in!

When Being Last Means The Biggest Payout

Oxford Lane Capital Corporation ( OXLC ), yielding 18.7%, is a closed-end fund, or CEF, that invests in CLO (Collateralized Loan Obligation) equity positions. CLOs are investment vehicles that buy up leveraged loans and then "securitize" them. Investors who are willing to pay large premiums get the benefit of being first in line to get paid. The "equity" tranche is the last one to get paid. It absorbs the risk of borrowers defaulting while getting the potential to have the greatest reward.

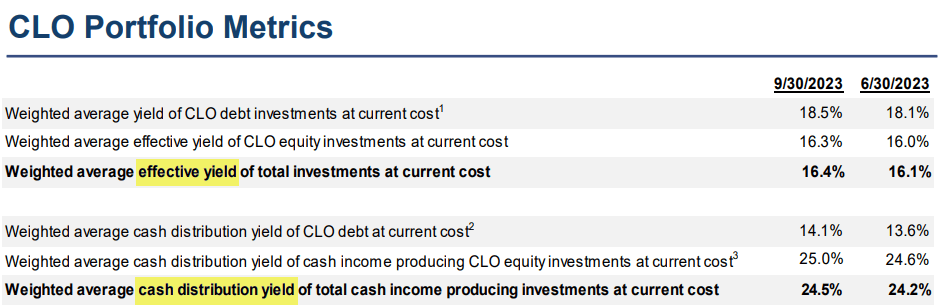

OXLC is getting an incredible yield on its investments. Source .

OXLC September 2023 Presentation

{kind=link}

The "effective" yield of 16.4% is a yield that projects future defaults. The "cash distribution" yield is annualized from the actual amount of cash that OXLC received from its investments last quarter. Note that both yields are based on OXLC's current cost , not the market value.

It is worth noting that OXLC regularly receives payments that are considered a return of capital. In recent articles, I have received comments from some readers noting that some of OXLC's investments have a fair value that has declined to near zero. They often conclude that OXLC has much larger losses than are being indicated by earnings.

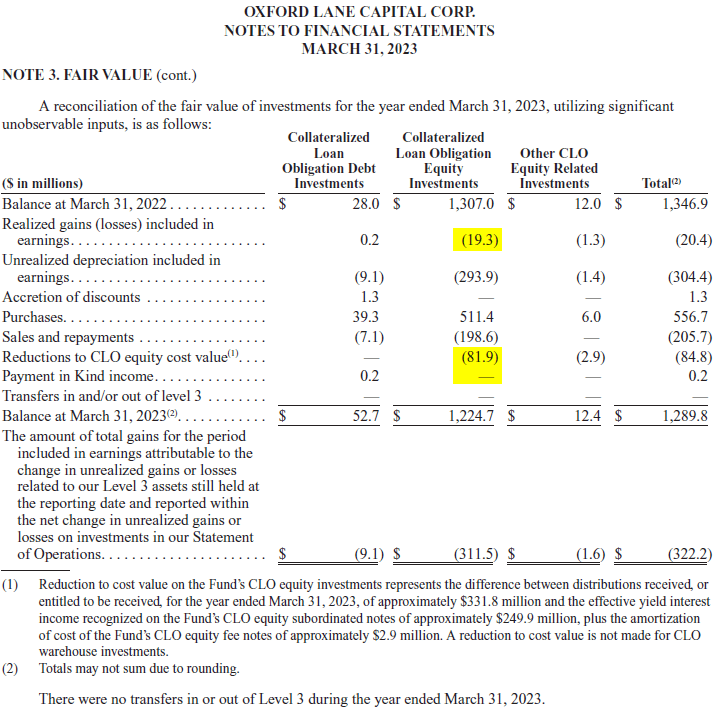

The accounting for a CLO equity position can be complicated, and it is primarily driven by nobody knowing how much it will ultimately pay. Fortunately, in its annual report (fiscal year ended March 31st), OXLC provides the details we need to see how their positions are performing. OXLC tells us how large realized gains/losses are: Source .

{kind=link}

We can see how OXLC's asset value in CLO equity declined from $1.3 billion in March 2022 to $1.2 billion in March 2023 despite investing/reinvesting $511 million in capital.

$19.3 million was realized losses. These are positions that OXLC either sold at a loss or could include realized credit-related losses. Next to $1.3 billion in assets, not a bad year!

"Unrealized depreciation in earnings" is the change in market value that is reflected in earnings. Changes in market value indicate the trading price of CLO equity positions. While it is possible that the market "knows" something and these unrealized losses could result in future realized losses, they can often be reversed. These unrealized losses accounted for a $293.9 million decline in asset value for OXLC last year – the most substantial impact.

Then we have "sales and repayments"; these are repayments of principal or the sale of a CLO for cash. OXLC sold $198.6 million in 2023.

Finally, we have "Reductions to CLO equity cost value." What is this? Remember the "effective yield" discussed above that reflects an estimate of future defaults for GAAP (Generally Accepted Accounting Principles)? Well, for accounting purposes, GAAP earnings need to reflect an assumption of default rates. But default rates have been very low. GAAP earnings need a way to account for the cash in excess of the effective yield that is received. That is done by treating the excess cash as "return of capital" and reducing the cost basis of the investment. Note that these payments are not "repayments of principal" – the borrowers are still paying interest, but those interest payments received are higher than the model predicts. If you read footnote #1, you can see that OXLC received $331.8 million in payments from its equity positions, but only $249.9 million is reflected in GAAP earnings. As a result, $81.9 million was recorded as a reduction in cost basis.

Offsetting these declines, OXLC invested/reinvested $511.4 million in new purchases – well exceeding the repayments, sales, and the excess cash flow recorded as a reduction in cost basis.

Clearly, the largest detriment to OXLC's NAV is unrealized depreciation. The realized losses were minimal. That was last year; how is OXLC doing this year?

Quarter-to-quarter, we can track this in OXLC's quarterly presentation (for the first half of their 2024 fiscal year): Source .

OXLC September 2023 Presentation

{kind=link}

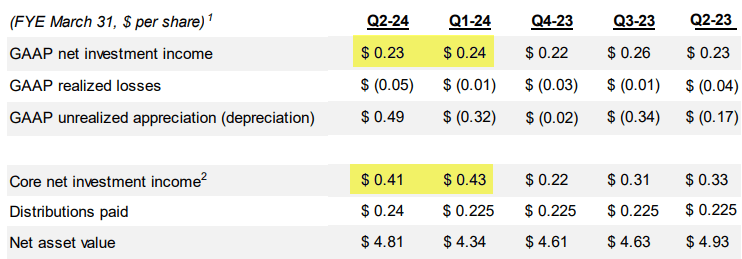

We can see that "GAAP Net Investment Income," which is calculated from the effective yield, totals $0.47 the past two quarters – continuing to cover OXLC's distribution. Core net investment income, which includes an adjustment for the actual cash received, totaled $0.84/share for the two quarters. This excess will be accounted for as a reduction in cost.

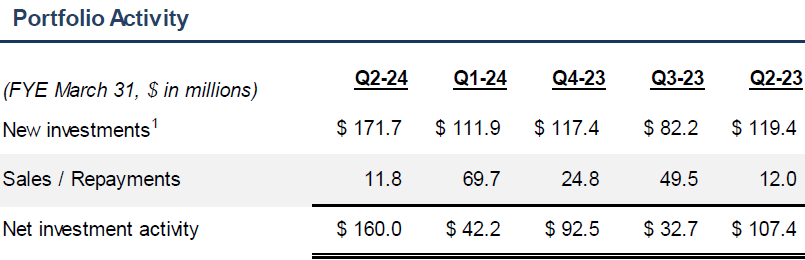

What does this tell us? OXLC's actual cash flow continues to dramatically exceed GAAP projections. Yet OXLC has opted not to distribute that excess cash. What are they doing with that cash? OXLC is continuing to reinvest it:

OXLC September 2023 Presentation

{kind=link}

Realized losses are roughly on the same pace they were last year, at $0.06/share.

One major difference? In the past two quarters, OXLC saw unrealized appreciation in Q2, offsetting all the unrealized depreciation in Q1 and offsetting a portion of the unrealized depreciation from last year. Loan prices have improved, and with the Fed softening and considering a pivot, loan prices have been quite strong this quarter as well.

When investors see a high yield, it is natural for them to wonder if the yield is "covered" by cash flow. They worry that their principal will be "eroded" as the company is overpaying the distribution. It is a legitimate concern, and some investments do that. It isn't necessarily a "bad" thing, but it is something you want to be aware of as an investor.

However, we need to recognize that asset prices change, and those changing prices are not always indicative of what will be real losses. Determining where cash flow supporting a dividend is coming from often requires a bit of legwork. When we look at OXLC's financials, we can see that last year, OXLC produced much more in cash flow than it needed to cover its dividend. The decline in OXLC's NAV last year was primarily driven by unrealized losses, which are caused by the mark-to-market change in the value of its portfolio. OXLC had plenty of cash flow and opted to reinvest a large portion of it. This is a pattern it has continued to follow so far this year.

OXLC is paying out an extremely high yield, while still retaining very substantial capital for reinvestment. That adds up to a very interesting opportunity for investors who are willing to stomach the price volatility that is inherent in CLOs.

Conclusion

The overarching question with any sort of debt investment or credit product is going to be the default rate. A CLO structure is designed to withstand a certain level of defaults while maintaining a positive return. Being that OXLC invested in the lowest level of a CLO, that means that its exposure to default rate is higher.

Before you start googling what the 2024 expected default rates are, both SP Global and Fitch have projected default rates for 2024. You must understand that both of those firms vastly overestimated the overall default rate for 2023. For example, Fitch expected that the default rate would be in the 3-3.5% percent range in December 2023 , after predicting upwards of 4.5% in May 2023. Yet the reality was that it barely even broke 2% over the last 12 months. Source .

{kind=link}

You need to have income to survive and shouldn't rely on doomsday predictions. Time and time again, they cannot accurately predict what the default rates will be going forward for the very markets that they're supposed to oversee. This reminds me that the U.S. economy often performs outside and beyond what others could expect it to. Many times, people have doubted the ability of the United States to continue to produce strong returns economically, or to weather storms that come, and the nation continues to prove its doubters wrong. I have learned it is beneficial to bet on the U.S. rather than against it. With my retirement portfolio, I want a strong income from the market, and one of the strongest places to get that is from the U.S. economy. This is one way to find the American Dream and embrace it.

That's the beauty of my Income Method. That's the beauty of income investing.

For further details see:

I'm Betting On America With 18% Yields: OXLC