BAK - I'm Buying More Braskem: You Should Consider Doing The Same

2023-03-09 16:25:27 ET

Summary

- I've written about Braskem a few times, and I also have a small position in the company. Braskem is a Brazilian-based petrochemical giant.

- While the company has been underperforming for some time, I believe the value that you're getting from investing here is quite compelling.

- Here is my 2023 thesis update for Braskem - and why I'm still at a "Buy" here.

Dear readers/followers,

Braskem ( BAK ) isn't an easy company to invest in. There's a lot of volatility inherent in the stock, and how uncertain the company can deem to be can be easily seen in the difference between how the company is rated by the analysts following it, and systems like Quant investing/rating, the latter tends to view the company unfavorably, and the former more favorably.

Me, I believe that the company will eventually be judged on fundamentals and good earnings, and its low valuation will reverse, but the timing of this reversal is uncertain.

Since my last article, Braskem stock has underperformed the broader market and relevant indexes. This doesn't faze me, though it's of course always a negative when a holding underperforms. I have added some shares, though my position in Braskem is still somewhat minor.

Let's look at my overall updated thesis for the company here.

Braskem for 2023 - Why the company is attractive

Braskem is more attractive now than it was the last time I wrote about it. Because the company is down around 10% since then, and it is the #1 thermoplastic resin producer in all of the Americas, this puts the company in a very attractive overall position in South America, North America, and Latin America. With 15M tons of resin production per year, as well as compounds, advanced materials, and other things like biopolymers, Braskem is probably one of the more relevant indicators and players in the industry.

The company is, on a high level, highly correlated to the prices of Crude, Gas, LNG, Ethane, Naptha, and other things, there are movements in the share price that have very little to do with individual company performance - only that the performance is highly correlated at this time.

So, simply put - the company is more or less a play on feedstock pricing and trends. And because these areas are currently (and often) highly volatile, and currently fraught by macro uncertainties and geopolitical issues, it's no surprise to me that the company is still being pressured.

To be clear, 4Q22 and full-year results are released in about 2 weeks from this article. At that point, I'll be updating the piece where necessary, but expectations for the company's earnings for both the year, and for future periods, look something like this.

{kind=link}

This is an interesting trend and forecast for Braskem. You can really see here how things go extremely up, then extremely negative for some time. During these cycles, the company will go down significantly. That is also the time, if you're interested in investing in Braskem, to buy the company and to hold it to the upcycle. The difference that I see here in this cycle, is that it is possible that the earnings during the downcycle are not forecasted or might not actually go fully negative.

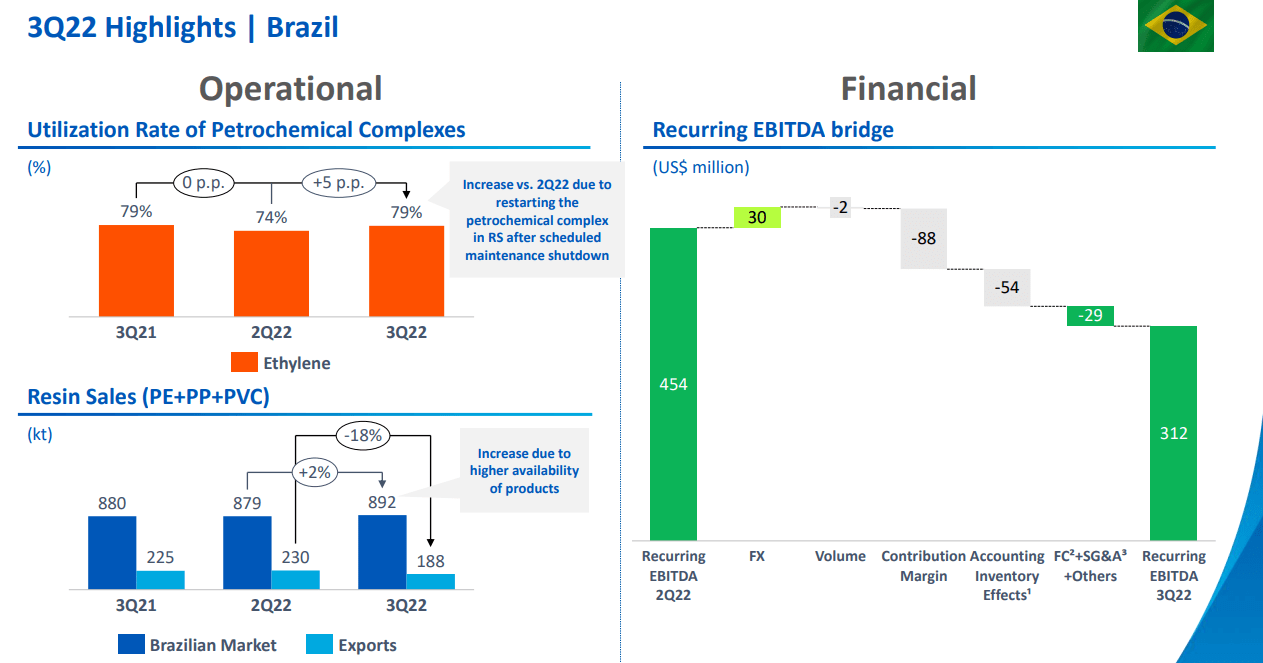

The company's current trends are fully in line with the current EPS expectations. EBITDA is down sequentially and YoY both, with significant drops of over 50% due to lower spreads for resin, PP in USA/EU, and PE in Mexico. This affects all chemical companies in the segment, not just Braskem. Export volumes are declining as well, and the company had negative accounting effects related to inventories during the last quarter. Still, the highlights were solid, especially solid.

{kind=link}

The company's trends and results are still overshadowed by some of the geological and company-specific issues, including the Alagoas event, which has caused provisions of over R$13B to begin with, though some of that has already been disbursed, leaving a provisional impact of around R$7.2B - based on relocation and compensation for affected, closing and monitoring of wells, sociourban measures, and additional measures. It leaves the company with nearly R$5B in current liabilities.

{kind=link}

The company's results and expectations for EU/US are far more impacted, with a massive EBITDA decline despite essentially unchanged utilization rates of company assets as well as only marginally changed sales in Europe PP, and a 19% decline in US PP, reflecting some of these trends we've been seeing over the past 2 years or so.

It's accurate to say that overall, the utilization rates and sales are overall fairly solid, or not massively negative for the quarter or for the full year of 2022. The company's expansion projects include things like the Ethane import terminal in Mexico which is slated to be completed in the next few years. This asset is expected to be able to start supplying about 80,000 ethane barrels per day, which covers Braskem's feedstock needs at a rate of 120%. The facility is slated to start up in 2024.

The company's fundamental debt and maturity profile are generally attractive. 4% of the company's debt matures in 2023, with another 6% in 2024. Beyond that, most are in 2027 and beyond, with 29% after 2032. So the company should be viewed in the very long term. Adjusted net debt/recurring EBITDA is around 1.55x - the company uses recurring/normalized numbers due to the massive volatility in its annual numbers. Gross debt is more or less on the same level, add or subtract about $100M.

The main case for Braskem is looking at the sensitivity tables related to the various petrochemical scenarios that could occur. A weaker global demand for resins and higher overall global inflation and inventories are continuing to impact things here and based on the latest forecasts seen from the company's guidance, there's a weaker demand to be expected both in resins and other segments. With new PP/PE capacities coming online globally, this is likely to put further strain on pricing, which will affect the company's bottom line and short-term spreads.

The outlook, therefore, is mixed, and how Braskem intends to utilize its assets differs on the basis of its operating geographies. In Brazil, Braskem will be winding down most of its Ethylene assets somewhat, with expected sales pressure along the resin segment, and worsening spreads in all resins (PP, PE, PVC) as well as chemicals.

Europe, on the other hand, is expected to be stable throughout 4Q22, as well as going into 2023, with NA and Mexico only slightly worse, with somewhat worse spreads and slight headwinds.

What should we be looking at then?

Spreads are one of the major issues here, and it's expected to get worse. The latest company communication is that demand is expected to look somewhat different in 2023. There is new capacity coming online, but the global demand is also expected to increase somewhat - not as high as peaks, but higher than in 2022. However, this is expected to reverse more in 2024, because speaking from a global chemical perspective, investments that should be made into the sector for 2025 are not being made at this time, so the company is expecting this to improve during that year.

Spreads are inherently part of the cyclical nature of this industry. There is nothing you can do about the ups and downs of them - and drops in companies like Braskem or other related businesses are when realizations by far are worse than the expectations. It's kind of like other commodities. If you expect the coffee bean harvest, based on relevant meteorological trends and commodity-specific flows, to go one direction, but something happens and it instead goes the other way - this influences futures and other pricing.

Investing in Braskem means "riding" these trends somewhat, much like riding on, and being if not comfortable, at least tolerant of the wild swings and motions of the markets, while knowing that the company is "safe" enough fundamentally so that you're really not in any danger.

Braskem isn't the best long-term performer. Long-term investors have made 20-year returns of 6.2%, which is below par. However, if you take advantage of the cycles, you're walking away with market-beating returns.

So far, we've not seen a bottom - but we're well below the level where I started buying Braskem.

Let's look at the company's current valuation.

Braskem's Valuation is attractive here, but volatility is high

Braskem's business remains somewhat troubled, as I've said before. Yes, every company does have a price where it becomes attractive - theoretically - but Braskem is one of those businesses that we need to be careful about, because there are so many better potential options out there, even in the case of "cheap" valuation, which we have for Braskem here.

I invest in several chemical businesses - fairly heavily as well, with over 10% of my total portfolio value being exposed to basic materials and chemicals. A common denominator for these businesses is that they are and tend to be more volatile than other businesses. Real Estate can be as volatile, but as always there are internal, sector-specific differences in volatility. Braskem is simply a very volatile example of a chemical business, making its petrochemical peers look stable by comparison, despite this being a volatile segment. The combination of Brazilian exposure, FX, and the overall volatility of this market makes for a very interesting investment. You can go years with zero dividends or EPS, as well as declines - just look at 2019-2020 or the like.

After years, you then get sudden surges of huge payouts that make up, or more than makeup for the downer years.

From any conservative multiple, this company is still undervalued. The 10-year average P/S is around 0.4x. It's now at 0.16x Same thing with revenue - typically above 0.8x, currently at below 0.6x. These fairly simple multiples imply to us a massive undervaluation that in part makes sense due to the expected spread development as well as the next few years of sales trends.

Realize though, that the implied or targeted share price here based on targets is very different from the share price the company currently trades at. Baskem is currently at $8/share for the NYSE ticker. The average PT from 7 analysts is $16.5/share, with 4 out of 7 at a " Buy ". So analysts seem willing to take the risk here and give the company a 105% average upside.

When I last reviewed the company, I applied a 10-20% discount to the company's NAV and forecasts based on spread trends, the company's somewhat worse fundamentals, and what peers we do have, reaching a PT of around $12/share. We're now in a position where this is an attractive "BUY". We can still conclude based on peer multiples, forecasts, and the company's NAV/fundamental multiples, that Braskem is undervalued.

The company's valuation is far more attractive than any of its peers in terms of straight multiples - but there are risk explanations for this, and I've tried being clear about these explanations here.

We do have an upside - though seeing such an upside based on forecasts is difficult because analysts cannot really, with any accuracy, forecast this company - they either miss negatively or positively 100% of the time with a 10% margin of error when it comes to Braskem.

So, if you're in for a wild ride and can tolerate this in exchange for near-double-digit upcycle yields and potential returns in the quadruple digits over time if bought cheaply, this one is a play for you.

For me, this is a "speculative BUY" with a PT of $12/share - I'm not impairing this further, though I might change it after the 4Q22.

For now, this is my thesis.

Thesis

- Braskem is an attractive company from a fundamental viewpoint, and it does have the potential of granting you some massive returns if bought at trough and held to an upcycle. The recent 2021 is an excellent example.

- Based on this, it's a speculative "BUY" when it's cheap. While it can go lower from $10-12/share, I would say that at less than 0.6x revenues and lower-priced than almost every peer, I see it as a " Buy ".

- The company is undervalued here - though I want to really emphasize the speculative nature of the investment, and my initial position will likely be low to reflect this.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italic).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

While the company does fulfill all of my valuation-related criteria, it does not fulfill the dividend and conservatively-run criteria, and therefore is a bit of a wildcard.

This one is for the most risk-tolerant investors. I have only a small position in the business.

For further details see:

I'm Buying More Braskem: You Should Consider Doing The Same