PSA - I'm Hoarding Self Storage REITs How About You?

2023-07-23 07:00:00 ET

Summary

- I’ve seen studies showing that real estate is the most common source of value creation for millionaires.

- Many investors aren’t comfortable with a debt-fueled real estate empire plan or the hassles of being a landlord, and that's where the simplicity of self-storage REITs comes in.

- Blue-chip self-storage companies have proven their ability to generate strong cash flows throughout a wide variety of economic environments, making properties in this industry attractive, relatively defensive assets.

Hoarding disorder : An ongoing difficulty throwing away or parting with possessions because you believe that you need to save them.

Real estate is one of the very best ways to build wealth over the long term.

I’ve seen studies showing that real estate is the most common source of value creation for millionaires.

At the very least, this is likely due to the capital appreciation of the average Joe’s primary residence (assuming that they’re a homeowner).

But many people take this a step further, using investment properties to build wealth and accelerate their journey toward financial freedom.

Using debt to accumulate cash flow properties, allowing other people to pay down that debt (tenants) and build your equity, and generate positive cash flows allows real estate investors to build vast fortunes with relatively little cash down.

Using debt to build a real estate portfolio is one of the lowest risk ways to use leverage to your advantage.

But, debt is still debt… no matter how reliable a property’s cash flow is thought to be.

With this in mind, I know many investors who aren’t comfortable with debt-fueled real estate empire plans.

What’s more, cash flow coming from real estate is not truly “passive” income.

Believe me, it takes a lot of work to be a landlord.

You have to deal with tenants, property maintenance, and pay taxes on your assets.

The reason why so many people are REIT investors, rather than physical landlords, is because they’d rather avoid the "three Ts" - toilets, trash, and taxes.

Using leverage to build wealth can be attractive to more risk-tolerant investors. However, simplicity is key to sleeping well at night .

Dividends paid by REITs are truly passive income; the only things required to generate these reliable payments are the patience and discipline required to make investments and hold them over the long term.

By owning REITs, you allow professional investment teams and property managers to take on that work (and the headaches that come from the three T’s) for you.

The individuals who make up these teams have decades upon decades of combined experience when it comes to screening investment properties, finding reliable tenants, generating cash flows, and maximizing shareholder value.

Another problem with investing in physical real estate is that even if you’re someone who is willing to leverage debt to acquire a cash flowing property, there’s a chance that you can’t (or shouldn’t) receive a loan large enough to buy income property(ies).

Remember, staying diversified across your investment portfolio is very important… as is staying liquid (it can take weeks, months, or even years to sell large-scale real estate investments).

Now, if it makes sense for you to invest in physical real estate, when it comes to the commercial property space, one of my absolute favorite industries to invest in and own are self storage facilities .

You see, investors who own properties in this industry don’t have to deal with the 3 T’, at least, in the traditional sense.

Yes, they still have to pay taxes (that’s unavoidable).

But, tenant issues and overhead are minimized in this space with the use of auctions and automation.

In general, eviction in the self storage industry is a quick and easy process (especially compared to residential properties).

If a tenant stops paying rent, landlords in this industry can recoup some of these costs by selling the assets stored in their facilities.

And due to the barebones layouts of these facilities, the risk of property damage inside of each unit is extremely low.

Furthermore, self storage facilities have reduced overhead over the years by relying on SEO and digital assistant-like infrastructure to find and book tenants.

They use automated keypads to provide tenants with entry into their spaces, reducing the need for on-site management.

And generally speaking, there isn’t a lot of plumbing or cosmetic maintenance that these properties have to worry about (a good commercial roof and HVAC system for higher premium climate controlled spaces are the main things that a landlord needs).

In short, the self storage industry is one of the lowest overhead real estate investments that anyone can make, and therefore, it’s one of the highest margin situations that a landlord can find themselves in.

Regardless of what industry you’re in, margins are everything.

This is why I’ve been so bullish on triple net lease REITs over the years - they do their best to pass along all of the major costs associated with owning real estate onto their tenants.

But, I’m also really bullish on the self storage industry as well because of technological advancement that has allowed owners of these properties to cut costs by avoiding certain issues all together.

And last, but certainly not least, I should mention that blue-chip self storage companies have proven their ability to generate strong cash flows throughout a wide variety of economic environments , making properties in this industry attractive, relatively defensive assets to own, even during recessionary times.

And thankfully, even if you’re someone who isn’t interested in taking out a loan on a seven-figure industrial property, there are ways to gain exposure to this fabulous industry in the stock market.

There are a handful of REITs that operate in the self storage space, but I believe that two in particular have separated themselves from the pack in terms of quality metrics and these are the stocks that I want to focus on today.

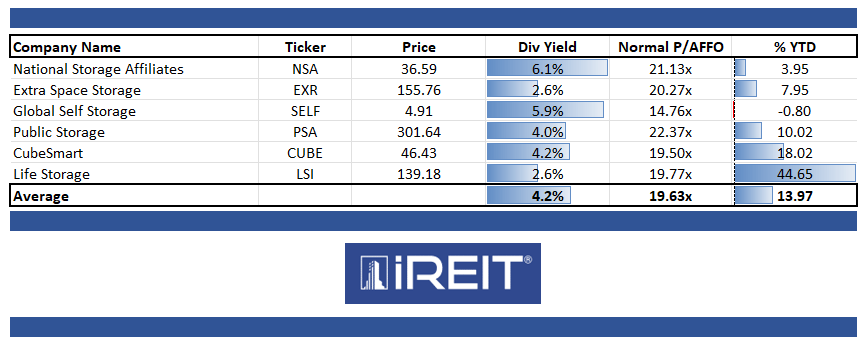

Extra Space Storage ( EXR )

EXR is my top pick in the industry.

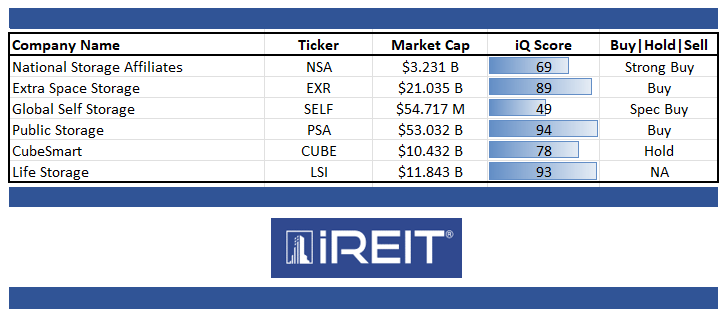

Our IQ quality ranking is 93/100, making it one of the highest rated REITs in the entire sector.

I recently highlighted my bullish stance on this company in an article, writing:

“Simply put, owning real estate with pricing power can benefit landlords during periods of high inflation.

One of my favorite pricing power picks is Extra Space ( EXR ), a leading self-storage landlord that has an impressive portfolio of 2,388 properties (owned and managed) in 41 states.

While most don’t consider EXR to be a technology play, I consider the company to be a tech-savvy player due to their customer acquisition and data analytics capabilities.

EXR has doubled in size since I began coverage (in 2013) from just over 1,000 facilities to over 2,300, and should merge with Life Storage ((LSI)) in the second half of 2023 to become the largest self-storage landlord in the world – with over 3,500 properties and close to 13% market share in the U.S. (PSA has 10.1% market share).”

I love the size/scale advantage that EXR is expected to have once the Life Sciences deal closes… but even without these assets under its umbrella, EXR has proven itself to be a wonderful operator over the years.

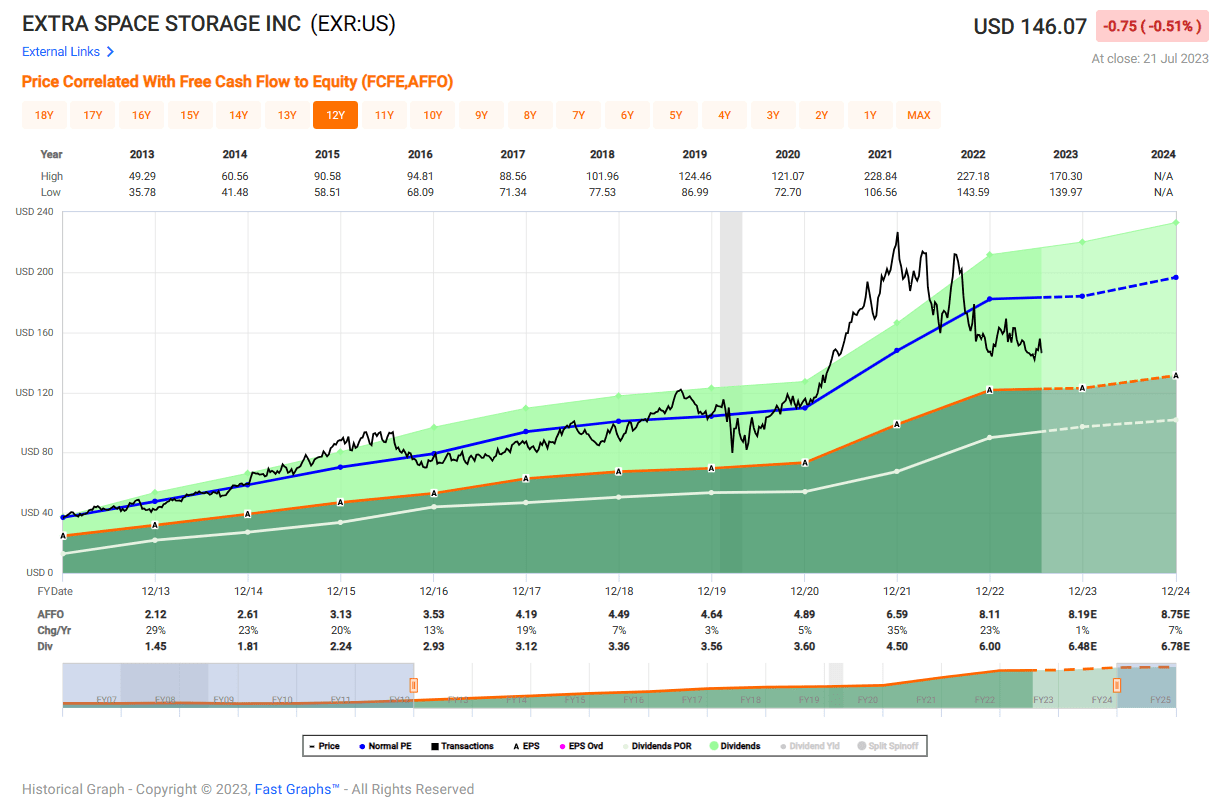

Looking back to the Great Recession, we see that EXR shares have posted negative annual AFFO growth just once (in 2009).

{kind=link}

The company managed to grow its bottom line during 2008 and during 2020 when the broader market crashed.

And while 2023 is expected to be a relatively tough year by analysts (currently, the consensus estimate for EXR’s AFFO growth in 2023 is flat) the future outlook for this company remains positive with mid-single-digit growth expectations in both 2024 and 2025.

What’s more, I expect to see the company outperform those future estimates - especially if the Life Storage deal closes and Extra Space is able to increase its size and scale drastically in the near term.

Looking at the chart above you’ll notice that EXR’s valuation got ahead of itself during 2021/2022 when we saw an “everything rally” play out.

Since then EXR shares have given back quite a bit of those gains... shares are down by more than 30% since their all-time highs in the $225 area back around the start of 2022.

But I wasn ’t banging the table for EXR back then.

It was obvious that the stock was caught up in an irrationally bullish momentum wave and I was happy to wait for shares to cool off before buying into this story heavily.

After EXR’s -30% declines, shares are quite attractive .

Currently, this stock trades with a blended P/AFFO multiple of 19.2x.

That’s higher than many of its brethren from the REIT sector; however, it’s well below EXR’s 5 and 10-year average P/AFFO multiples of 21.9x and 22.5x, respectively.

Given the rise in interest rates, I think the recent sell-off makes sense.

But I think the bearish pendulum has swung too far (just as the bullish one swung too high during the stock’s 2021/2022 rally).

The sentiment-driven market nearly always overdoes its moves. Traders aren’t making decisions based upon fundamentals here, they’re allowing emotions to drive their decision-making. And, this has created an opportunity.

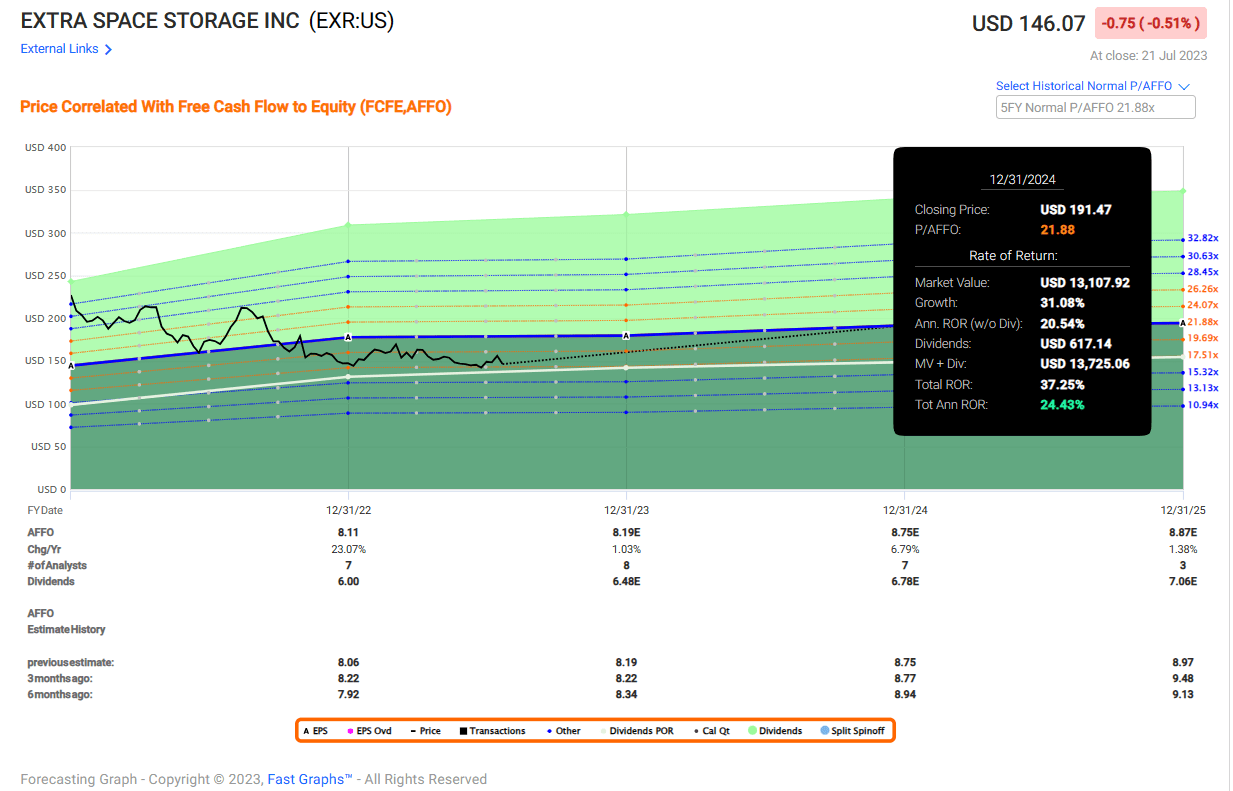

I believe that EXR shares are worth approximately $170.00 and therefore, at today’s $155/share levels, we’re looking at an ~8% margin of safety.

That’s not an extraordinarily wide discount. However, I’ve been pleased to take advantage of it because anytime a blue chip name like EXR goes on sale, buying shares and holding them over the long-term tends to work out well for the patient investor.

And, in the meantime, while I wait for this stock’s multiple to rise back up towards that 20x-21x level, I get to sit back and collect Extra Space’s extra safe 4.15% dividend.

Since its IPO, EXR’s average P/AFFO multiple is in the 20.3x area.

Assuming we see mean reversion back up to those levels… looking at the stock’s forward consensus fundamental and dividend growth prospects, investors buying shares today would see annualized total returns in the 10% ballpark looking out over the next two and a half years.

That’s not bad for a high yielding stock like this one.

And therefore, no one should be surprised that we have a “Buy” rating.

{kind=link}

I should note that there are investing sites that show EXR’s yield as ~2.5%. However, it’s important to note that this is due to them annualizing the stock’s recent $1.01/share special dividend.

That dividend was great to receive, but investors should not be confused, as of right now, EXR’s annual dividend is $6.48, or $1.62/share quarterly, and that $1.01 was a special payment related to the LSI deal.

With that $1.62/share quarterly dividend in mind, we’re looking at a forward AFFO payout ratio of 79.8%.

That’s more than safe for a REIT that generates this sort of reliable cash flow.

Moving forward, I expect for EXR’s dividend to grow in-line with its AFFO growth, meaning that once the LSI deal closes and the company begins to normalize its payment schedule, I believe that investors can expect to see a ~4-7% annual dividend increase moving forward for the foreseeable future.

This stock is on a 12-year dividend growth streak, and therefore, I believe that EXR remains on track to slowly, but surely, work its way up toward dividend aristocracy (which would be achieved when the stock’s annual dividend increase streak hits 25 years).

Public Storage ( PSA )

Speaking of rising dividends, PSA, a company with a quality score which is actually slightly above EXR’s, coming in at 94/100, recently provided its shareholders with a massive raise.

In February of 2023 PSA raised its dividend by 50% to $3.00/share.

Today, PSA shares yield 3.98%.

That increase was great news… especially since PSA hadn’t increased its dividend since 2017 (something that was disappointing to many investors, myself included).

Despite this company's previously frozen dividend, PSA’s quality metrics were very high, in part because of its strong balance sheet.

Public Storage sports an S&P credit rating of A, which is higher than Extra Space’s BBB rating.

Like EXR, PSA has posted incredible bottom-line growth over the years.

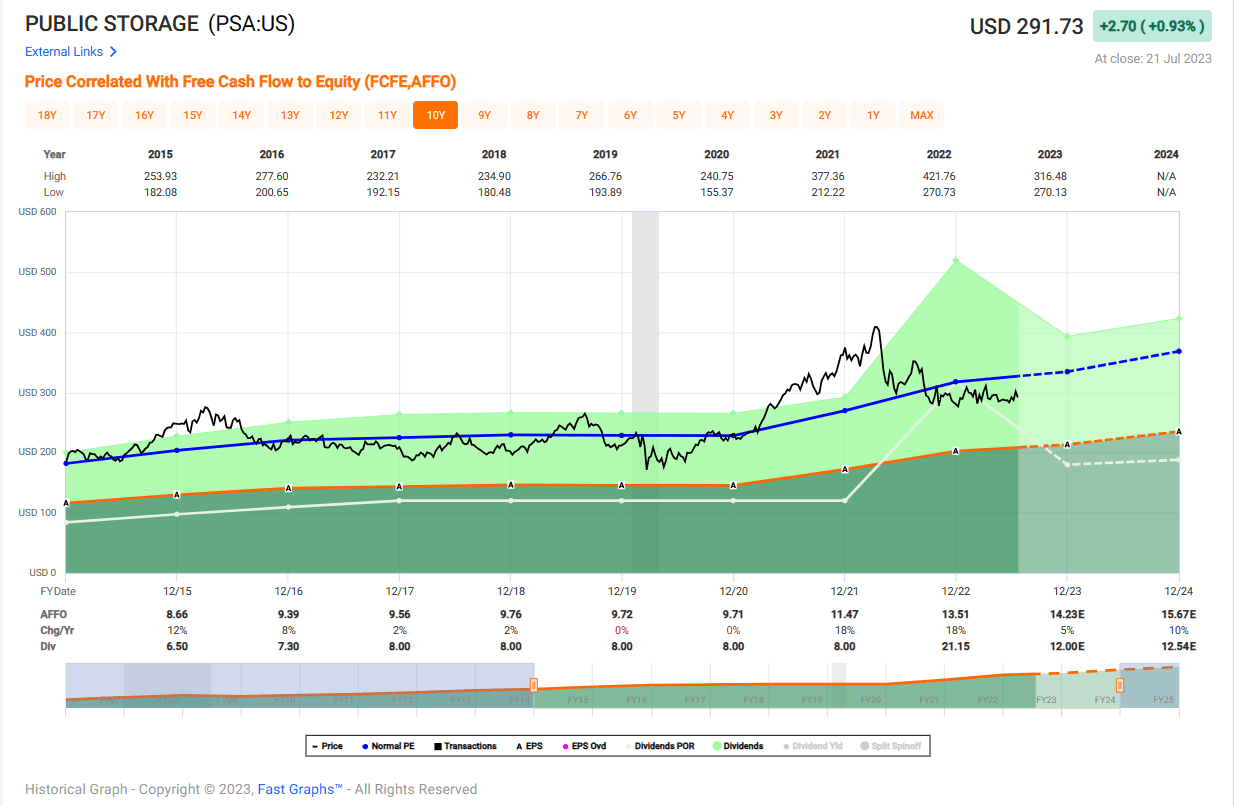

Also, like EXR, PSA shares are down big from their prior highs.

PSA shares hit all-time highs in the $410 area in early 2022 and since then they’re down by more than 26%.

Yet, this stock’s rising AFFO and its falling share price has resulted in an attractive opportunity for investors.

Once again, looking back to the Great Recession period, you’ll notice that PSA’s AFFO has risen by leaps and bounds since 2007.

{kind=link}

Yes, from 2016-2020 PSA struggled to grow its bottom line.

This was a tough five-year period for this company.

However, since the COVID-19 pandemic hit, PSA’s growth is back online, with 18% growth during 2021 and 2022.

Furthermore, looking ahead, you’ll notice that Wall Street is more bullish on PSA’s growth prospects than it is on EXR’s.

This company is expected to compound its bottom line at a high single digit clip over the next 2.5 years, whereas EXR’s growth expectations are in the mid-single digit area.

The market has responded to these higher growth prospects with a higher premium.

PSA’s blended P/AFFO multiple is currently 21.7x.

That’s well above EXR’s 19.2x figure… and plays a large role in why I am more bullish on EXR shares at the moment.

But it’s important to note that even though PSA shares trade at a premium to its soon-to-be larger peer, this 21.7x present day multiple still represents a discount to its 5 and 10-year average P/AFFO multiples of 22.1x and 23.1x, respectively.

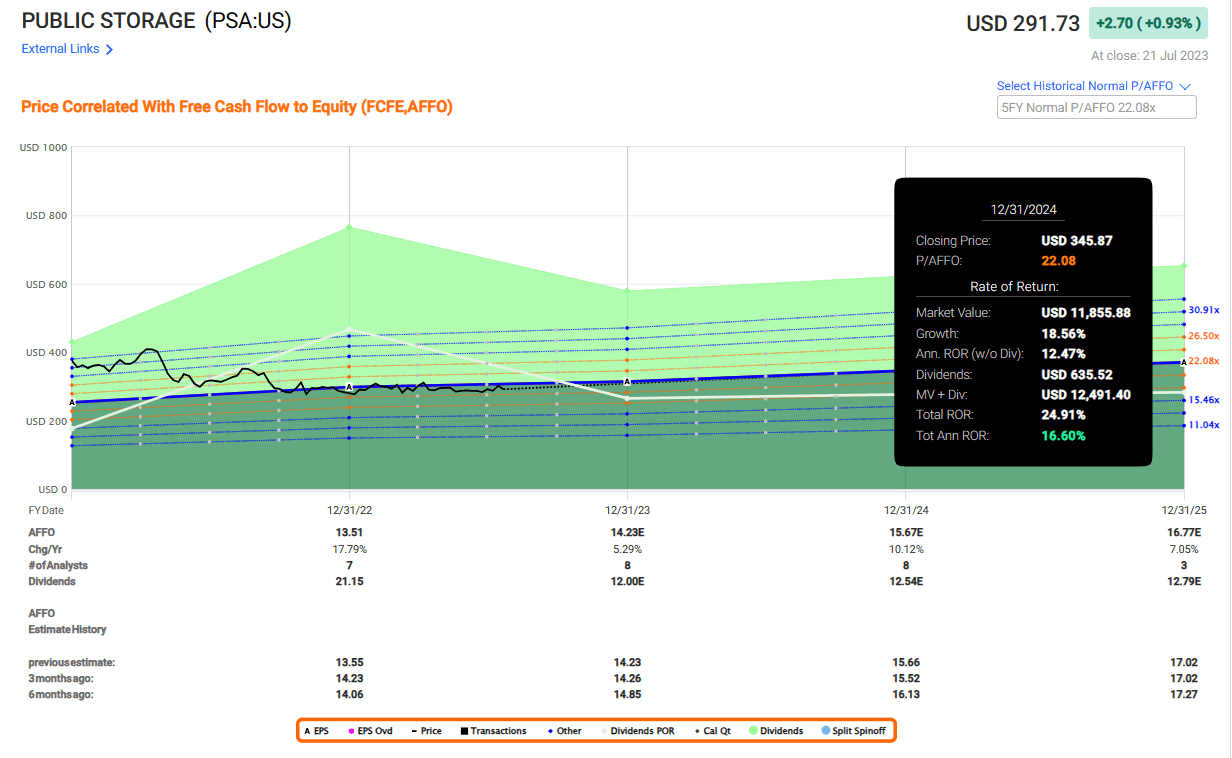

Over the last 15 years, PSA’s average P/AFFO multiple was 22.4x. If the stock were to see mean reversion back up to that level, the combination of its recently increased dividend and strong fundamental growth prospects would result in an annualized total CAGR of 12.9% between now and 2025.

{kind=link}

Granted, this calculator involves a higher target multiple than the scenario we ran for EXR.

If PSA were to trade with the same 20.3x multiple that I used to estimate EXR’s forward return prospects then we’d be looking at lower results here… PSA would compound at an 8.8% clip.

Now, even if we were to see PSA’s valuation settle in at the low-end of its historic range, there’s nothing wrong with compounding your wealth at an 8-12% rate.

This is why we currently have a “Buy” rating on PSA shares as well.

I believe that PSA’s fair value is $315.00/share, meaning that its current share price in the $302 area equates to a margin of safety of roughly 4%.

So, the discount here isn’t as deep as EXR’s, but this blue chip is still trading with a discount attached.

Conclusion

Overall, both of these stocks offer investors a chance to own a piece of extremely high-quality companies.

After their recent sell-offs, both stocks have fallen into “Buy” territory.

{kind=link}

Both stocks pay a solid ~4% dividend that I expect to see grow over time.

Both EXR and PSA are leaders in the very attractive self storage industry, and while EXR is my favorite of the two, I don’t think that long-term investors can go wrong when buying shares of either of these companies whenever they trade at a discount to fair value.

Both EXR and PSA have proven themselves more than capable of compounding their fundamentals, dividends, and their investors’ wealth throughout bull and bear market periods - that’s why I’m becoming increasingly interested in adding to these types of positions in today’s volatile market environment.

{kind=link}

For further details see:

I'm Hoarding Self Storage REITs, How About You?