PSA - I'm Still Betting On The Tortoise: REIT Quality Wins The Race

2023-09-12 07:00:00 ET

Summary

- Loneliness has negative effects on physical and emotional health outcomes and overall wellbeing.

- Our desire for companionship is natural and built into our biology.

- Seeking validation through brand names and peer approval can lead to short-term satisfaction but may not be sustainable in the long run.

It's easy to get dazzled by the opinions of others.

We're built to be social creatures. Yes, even those of us with an XY chromosome.

It doesn't matter how introverted we may be or how much others may annoy us. In the end, some part of us doesn't want to be alone.

Exploring this, NBC News wrote this back in January 2018:

"'Human beings are an ultra-social species - and our nervous systems expect to have others around us,' Emiliana Simon-Thomas, PhD, Science Director of the Greater Good Science Center at The University of California, Berkeley, tells NBC News Better. In short, according to biology, neuroscience, psychology, and more, our bodies tend to work better when we're around not alone.

" Being lonely has been linked to worse physical and emotional health outcomes and poorer wellbeing . Plus, a lack of social support can directly (affect) our potential for experiencing happiness," explains Simon-Thomas, who studies the biology of our emotions and thinking. ' We're built to really seek social companionship and understanding .'"

In other words, our desire for companionship is a good thing.

We need others to actually want to be around us.

Which means offering them something they deem worthwhile.

Admittedly, that concept can be taken way too far too quickly.

It's All in the Name

Social media immediately comes to mind when thinking about peer approval gone wrong.

Facebook.

Twitter (now X).

Instagram.

Even LinkedIn.

You don't have to look long to see examples of foolishness on display - all for the purpose of generating clicks, likes, praises, and other reactions.

"I'm here!"

These posts seem to say.

"Notice me! Please! Please? Pleeeeease???"

Sometimes we'll even take negative attention just as long as it means we're not being ignored.

The same thing could be said with people who are obsessed with name brands.

Nothing against well-known companies, mind you.

I'm a man who owns a Porsche, or two, after all.

But there's a point where it gets a little… dare I say "unnecessary?"

Let me use a set of luggage as an example, starting with the "Wheeled Carry-On in Signature Canvas" you can get from Coach.com. This 13.5 x 18.25 x 9-inch option is made from refined calf leather and features:

- Inside shoe mesh pockets

- Inside compression strap

- Two-way zip closure

- Top and side handles

- A telescoping handle

- Outside zip pockets

- An outside ID holder

- A laundry bag

This item costs $695. For a carry-on.

Now search for luggage on Macy's website, where you can find a perfectly respectable five-piece set for $240.

And in case you're wondering, yes, it features two-way zip closures and multiple handles. You might have to pay extra for a laundry bag, but I think the pros might outweigh that con.

Even so, I'm absolutely sure people will buy the former.

The very successful and market-savvy Coach wouldn't price it the way it is otherwise.

It knows people will pay for that brand-name validation…

Even if it means they're trading short-term hits for long-term sustainability, security, and even sustenance.

You Want Something More Dependable Than a Flash

I don't mean to pick on Coach alone - or even Coach at all.

Or people who like Coach.

(Full Disclosure: My wife absolutely loves Coach…ouch?!)

The psychology behind it and its customers governs so many other companies as well, all of which create a lot of jobs.

Tiffany's diamonds.

Modelo beer.

Apple (AAPL) computers.

Now, you can argue all you want that Apple, for one, makes better products.

And you might very well be right.

I own an iPhone myself - an intentional choice over its competitors.

However…

Do you remember that ad campaign Apple ran back in the 2000s starring Justin Long? To quote Wikipedia (an acceptable decision this time, I think), it personified the PC as being "formal and somewhat polite, though uninteresting and overly concerned with work."

That stodgy, out-of-date, rather pathetic persona compared to Long's casual yet impressive capabilities gave Apple countless sales - not just at the time but for the next decade plus.

Now, again, I own an iPhone.

Moreover, I overall like owning an iPhone.

And there are my Porsches too.

So I'm the first person to say that, sometimes, brand names are worth it.

Ever tried the generic version of Cheerios?

It's not the same thing.

The same principle applies to investing.

You never want to sacrifice quality in your search for stocks.

It's OK to own household names like Apple, Amazon ( AMZN ) and Coca-Cola ( KO ).

It's just that shouldn't be the only reason you buy it. You need the data to back up the reputation.

I can just imagine the hare in the Tortoise and the Hare story all decked out in designer running pants with the most pointlessly expensive sneakers… only to lose out in the end.

It's quality that wins, not immediate approval from our peers on whether we're on-trend or not. Take it from the tortoise, who got all the attention in the end after all.

Federal Realty ( FRT )

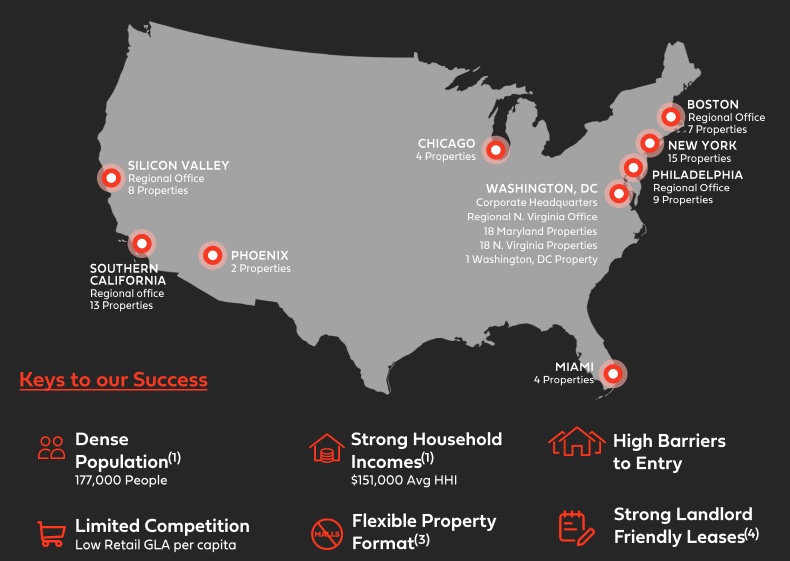

Federal Realty is a shopping center REIT that owns 102 open-air properties located in first ring suburbs of nine major high-barrier to entry markets. The portfolio consists of 3,300 tenants and 3,100 residential units - all located on 2,000-plus acres.

{kind=link}

Federal Realty is a quality REIT defined by the strength of the balance sheet and the strength of the earnings stream.

The balance sheet is rated BBB+ (S&P) and Baa1 (Moody's) with over $1.3 billion of liquidity ($1.2 billion revolver plus $100 million in cash). In Q2-23 the company accessed the unsecured market with a $350 million green bond (5.38%) and it plans to return to mid-5 debt-to-EBITDA (around 6x in Q2).

The company always has maintained a disciplined capital structure and I credit the CEO, Don Wood, who has been running the company since 2003.

He joined the company in 1998 and before that he worked at Caesars World, Arthur Andersen, and worked for Donald Trump as the VP of finance for the then newly acquired Trump Taj Mahal casino in Atlantic City. (I was once a shareholder in the company.)

{kind=link}

Federal Realty is a dividend king, and the only dividend king in the REIT sector.

In case you didn't know, a dividend king is a company that has paid and increased dividends for over 50 years in a row.

That's what I call consistency.

OK, I'm sure you're asking, "what have you done for me lately?"

In Q2-23 FRT generated FFO per share of $1.67 and beat the company's previous record of FFO in Q2-22 by 5%. The company exceeded expectations based on the following drivers: (1) higher property-level POI than, (2) continued strength in rents, parking, specialty leasing and percentage rent (3) lower operating expenses.

As a result, the company increased its forecast for FFO per share by $0.04 per share at the midpoint to $6.52 from a range of $6.38 to $6.58 per share to a new range of $6.46 to $6.58 per share. Guidance now reflects 2023 FFO growth over 2022 of about 2% to 4% or 3.2% at the midpoint.

{kind=link}

Federal's dividend is safe, based upon a payout ratio of just 67% (AFFO payout ratio is 86%).

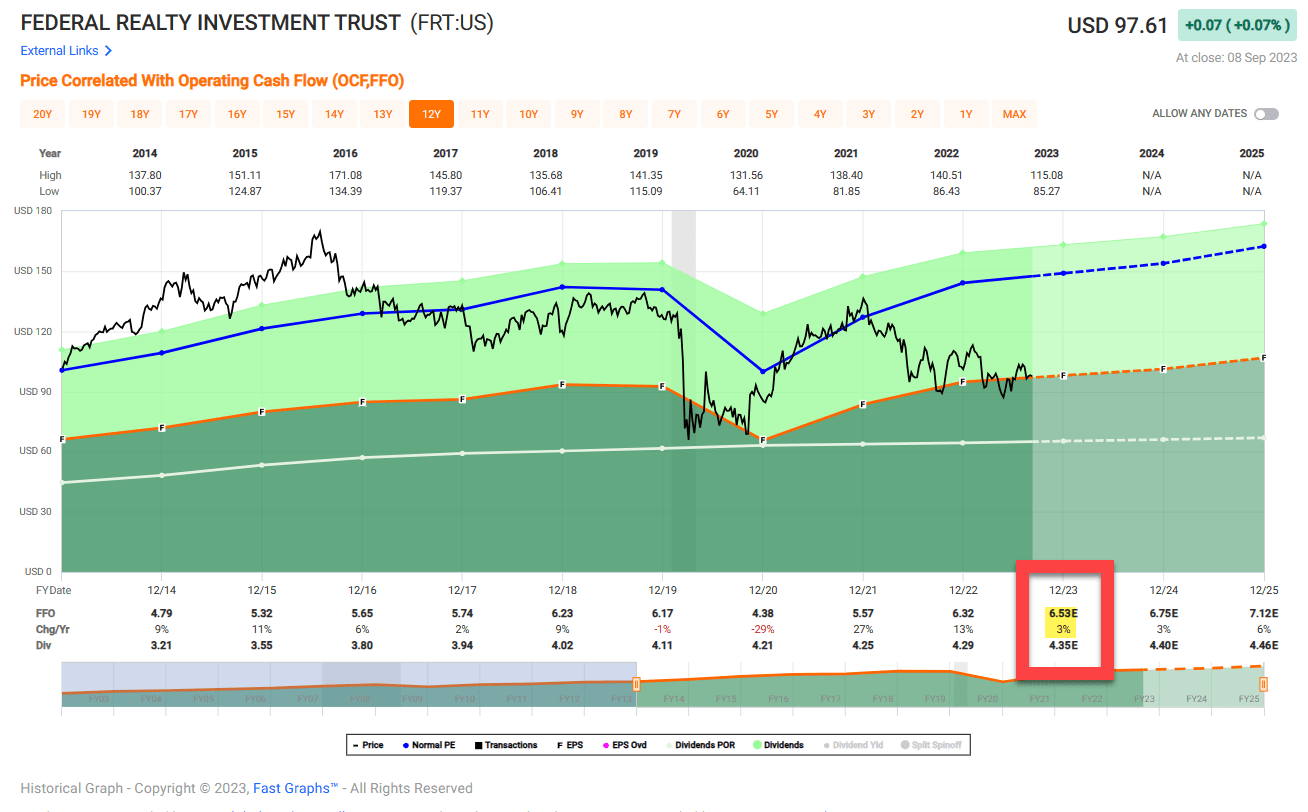

In terms of valuation, Federal is now trading at $97.61 per share with a P/FFO multiple of 15.x (normal is 22.8x). The dividend yield is 4.5%.

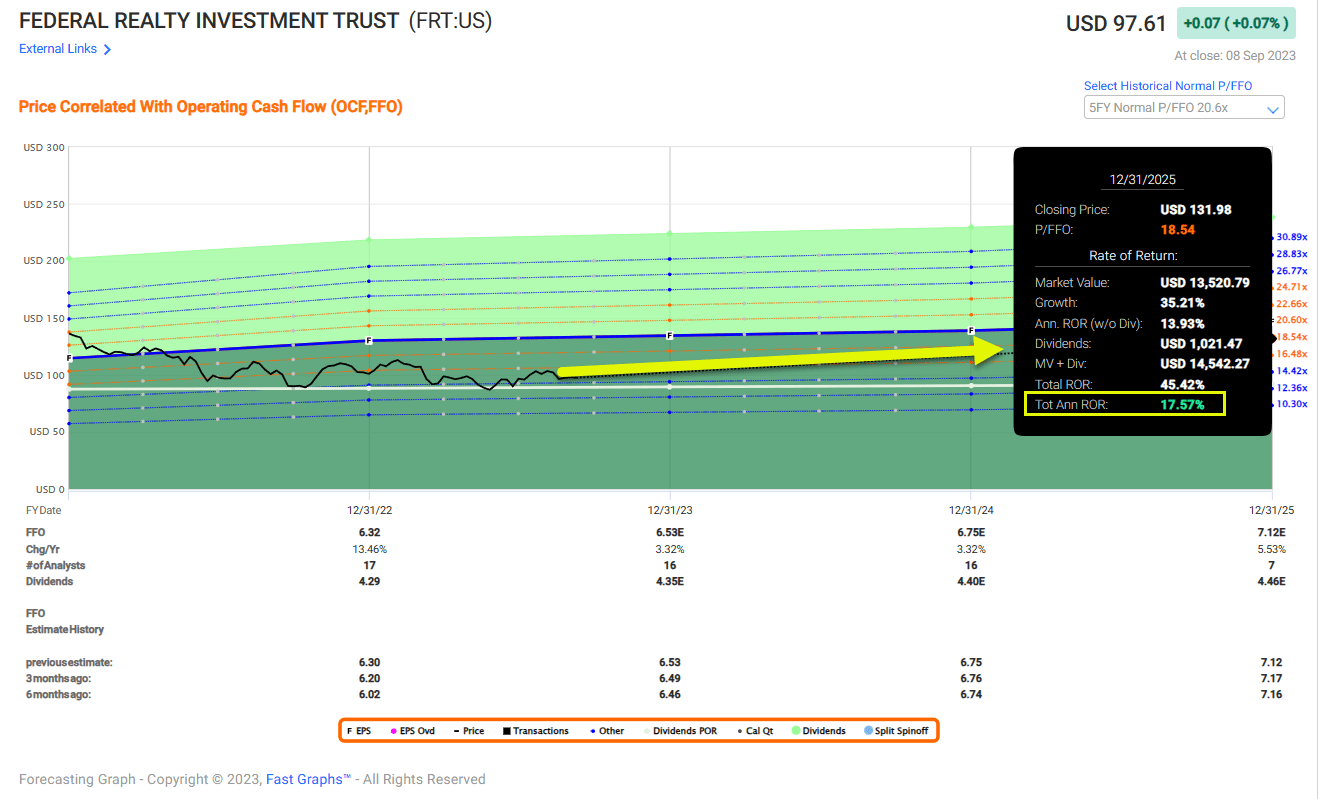

As shown below, we model FRT to return between 15% to 20% annually over the next two years. Analysts estimate growth of 3% in 2024 and 6% in 2025.

{kind=link}

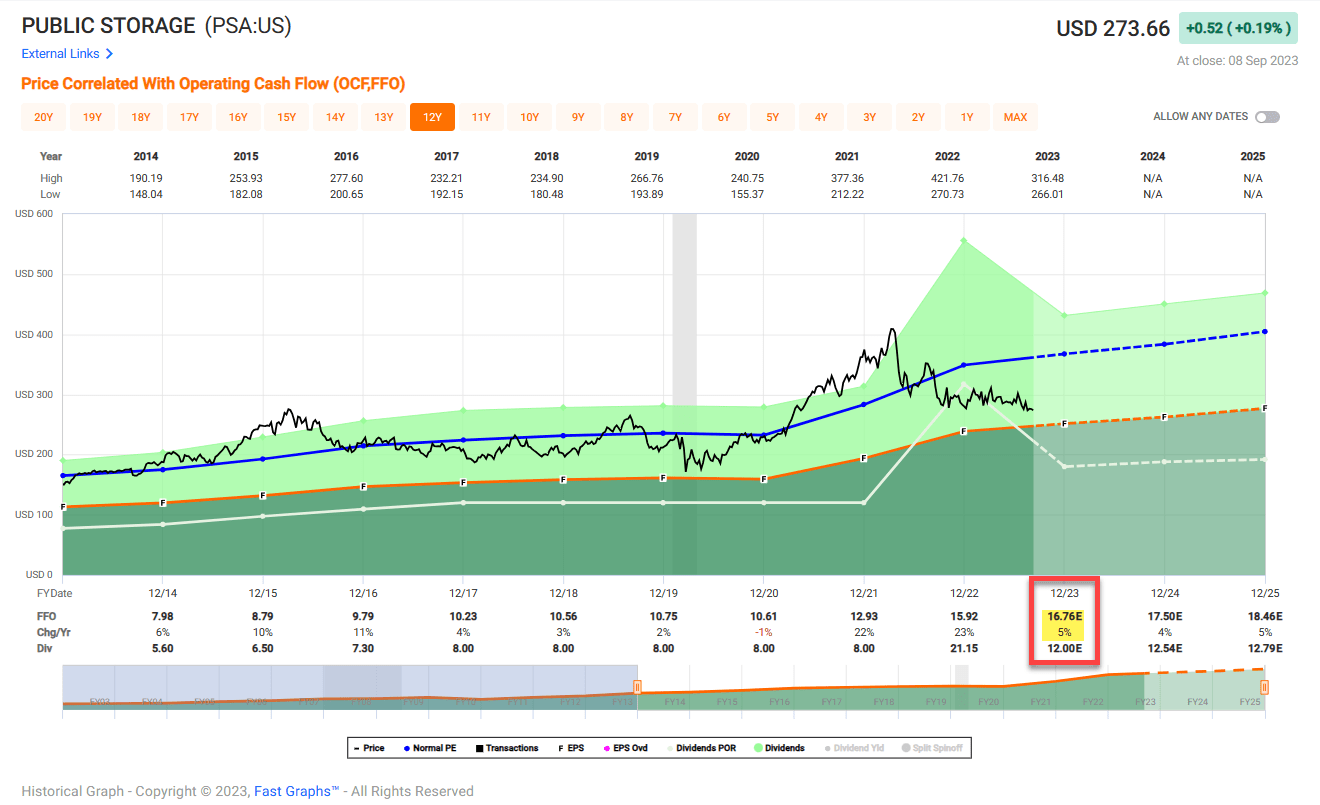

Public Storage ( PSA )

Public Storage is another blue-chip REIT.

As one of the largest self-storage landlords in the world the REIT owns 2,900 properties serving nearly 2 million customers (which I'm one). Public Storage has seen 27% portfolio expansion through $8.4 billion of investment since the beginning of 2019.

PSA Investor Presentation

In Q2-23 PSA acquired 11 properties for $144M (~$160/SF) and post Q2-23, acquired/under contract for $118.2M ($147.8/SF), in addition to the announced $2.2 Billion acquisition of "Simply" (owned by Blackstone's non-traded REIT BREIT).

PSA's (re)development pipeline was stable at $1.027B with a basis of $214/SF.

Public Storage maintains a "fortress balance" sheet rated A- by S&P with significant preferred exposure that has been refinanced at lower rates.

The company has issued ~$6 billion of preferred equity refinanced since 2015 at a blended rate reduced by more than 130 bps to 4.5%. At the end of Q2-23 leverage was flat q/q (-40bps y/y) at 3.3x (Net Debt & Preferred/EBITDA).

What's again, let's highlight the disciplined capital allocators.

Joseph D. Russell, Jr., CEO since Jan. 1, 2019, and President since July 2016. Prior to joining Public Storage, he was president and CEO of PS Business Parks, Inc. from August 2002 to July 2016.

PSA Website

In Q2-23 PSA bumped core FFO guidance +>$12.5 cents to $16.60/share (midpoint) and SSRev +25bps to +4.13%. The company also increased its acquisition guidance (post Simply) +$1.85 billion to $2.6 billion. PSA's FFO guidance also was raised.

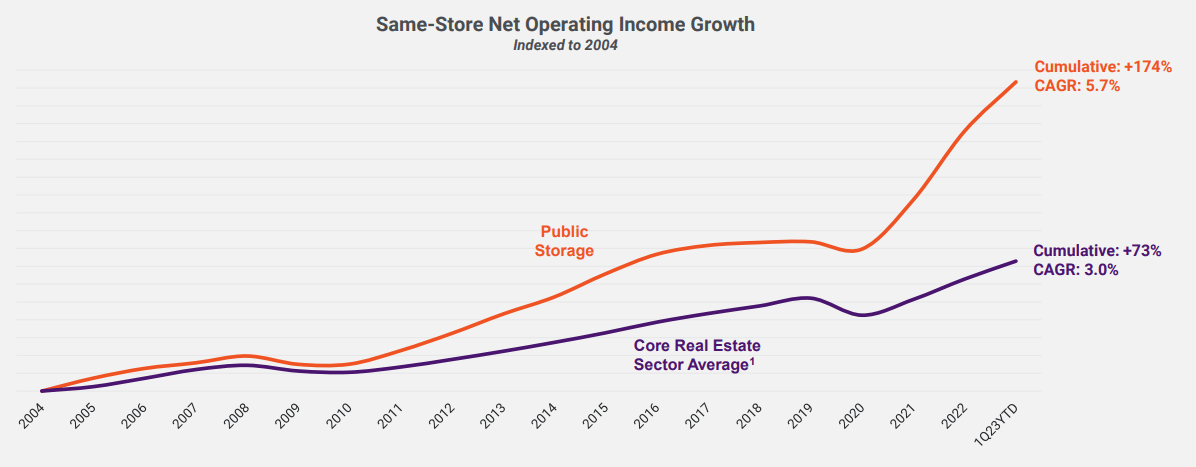

Public Storage's income generation outpaces and is more resilient than the broader real estate spaces, as shown below:

{kind=link}

As seen below, analysts estimate PSA could grow by 5% in 2023, 4% in 2024, and 5% in 205.

{kind=link}

Meanwhile, the dividend is well covered with a payout ratio of just 72% (AFFO payout ratio is 84%).

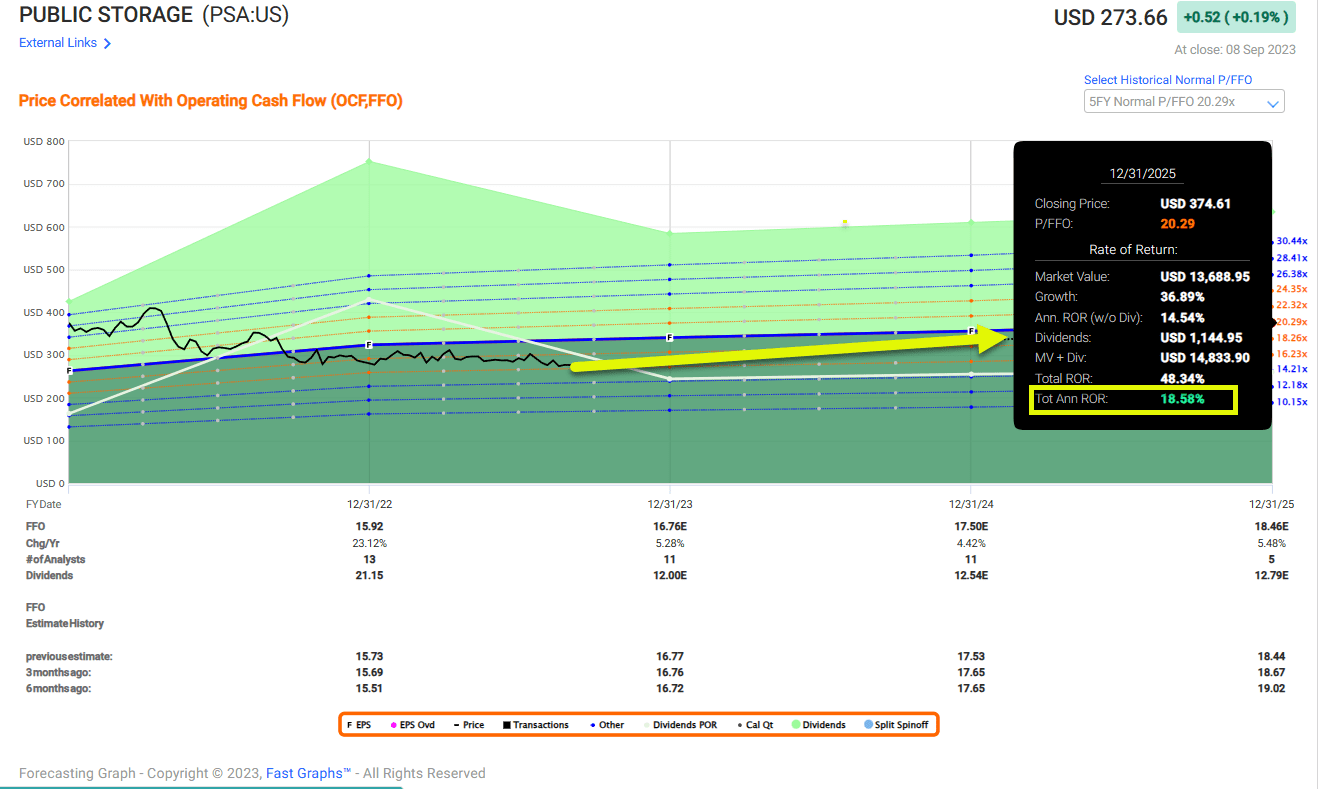

Shares are trading at $273.66 with a P/FFO of 16.6x (normal is 21.9x). The dividend yield is 4.4%.

As shown below, we model PSA to return between 15% to 20% annually over the next two years.

{kind=link}

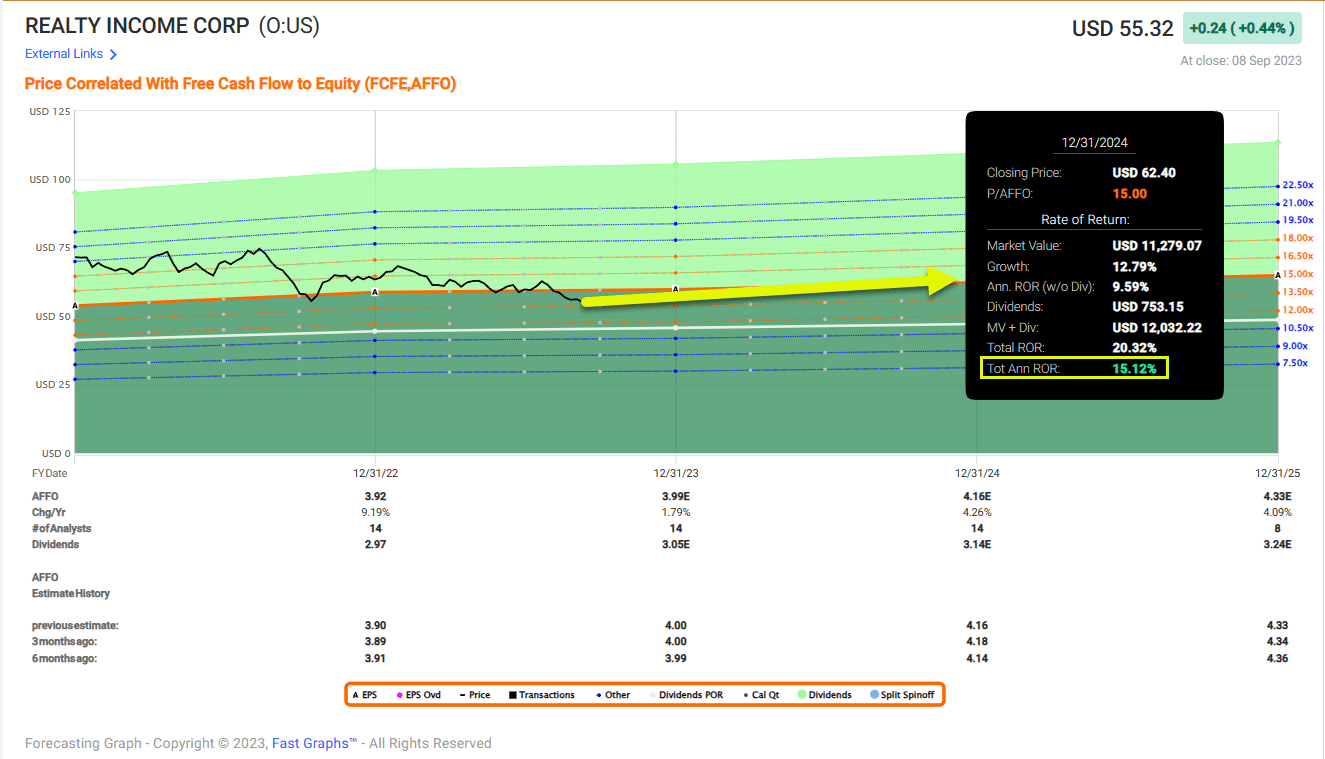

Realty Income ( O )

The Monthly Dividend Company...

Yes, you guessed it…

Realty Income is a pick in our "Tortoise and the Hare" article.

There's no need to spend much time on this since I covered it in detail (a deep dive ) just a few days ago.

Shares in O are now trading at $55.32 with a P/FFO of 13.5x (normal is 20.4x) and the dividend yield is 5.5%.

As seen below, we forecast O to return ~15% annually:

{kind=link}

A Few Other Tortoises to Consider…

In addition to these three REITs (FRT, PSA, and O) we also like these:

- Agree Realty ( ADC )

- Mid-America Communities ( MAA )

- Camden Property ( CPT )

- Alexandria Real Estate ( ARE )

- Rexford ( REXR )

- Regency Centers ( REG )

- American Tower ( AMT )

That's 10 picks!

Be careful when it comes to yield chasing.

In a few days I will be writing a " REIT Gold Digger " article which will detail names that I'm avoiding.

Remember…

Always insist on quality…

…and value.

That my friends is the key to sleeping well at night!

Happy SWAN investing.

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

I'm Still Betting On The Tortoise: REIT Quality Wins The Race