XOP - I Might Double My Pioneer Natural Resources Investment - Again

2023-08-29 15:05:50 ET

Summary

- I've been bullish on oil due to tight supply growth, consistent demand, the end of the U.S. shale revolution, and geopolitical risks.

- Pioneer Natural Resources stands out with efficient Permian operations, aiming to distribute 75% of FCF to shareholders through dividends and buybacks.

- PXD's outperformance versus peers and potential for strong free cash flow underpins my belief in its undervaluation; I am considering increasing my PXD exposure.

Introduction

I doubt it's a surprise to any of my regular readers when I say that I've been bullish on oil for a while. In this case, I turned bullish on oil in 2020, as I expected a significant shift in supply and demand dynamics.

Essentially, my thesis has been tightening supply growth and consistent long-term demand growth. The end of the U.S. shale revolution, OPEC cutting output to protect $80 Brent, and geopolitical risks are putting a floor under oil prices.

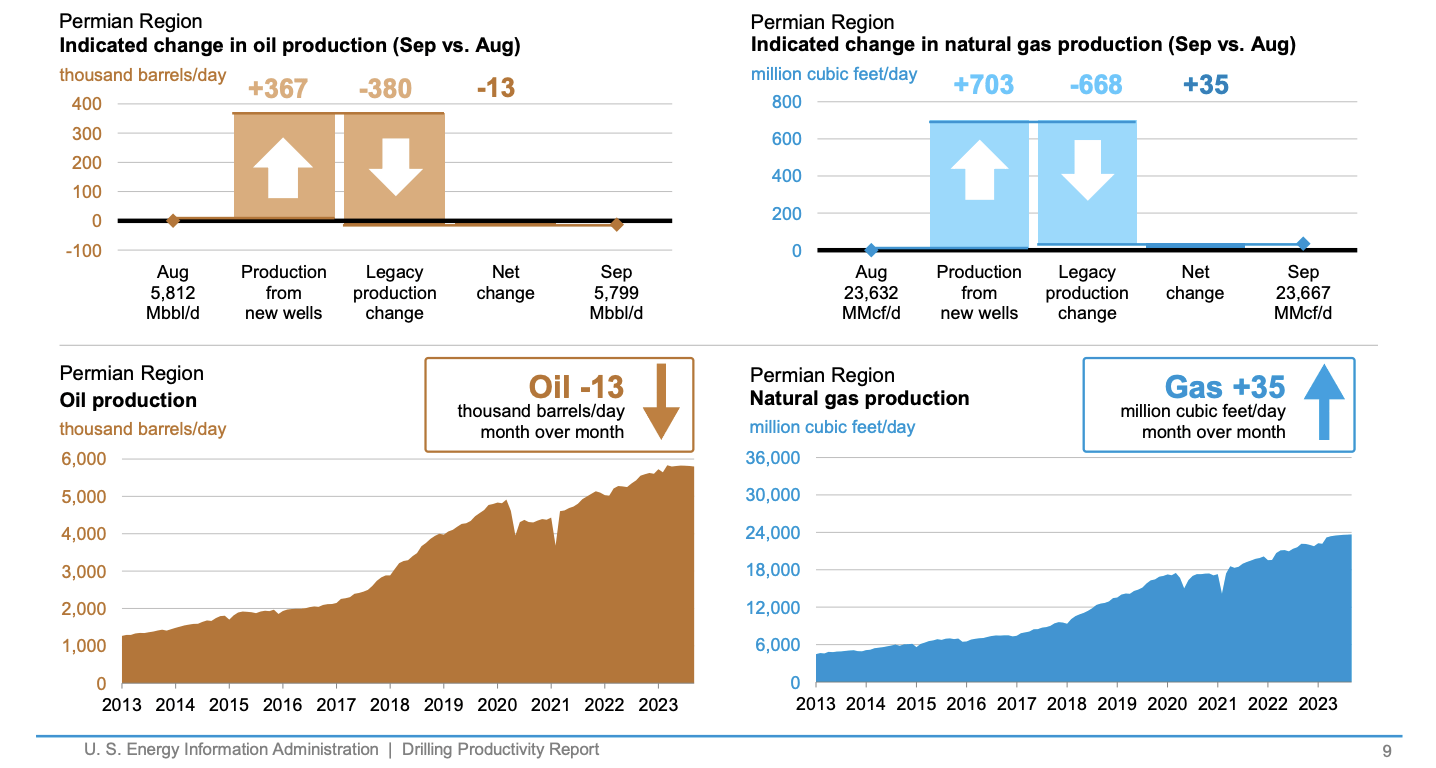

Even the mighty Permian basin in the United States, which is the only driver of unconventional oil supply growth, is now losing steam.

The most recent report showed that declines in legacy production are now more than offsetting production gains from new wells - natural gas remains in an uptrend.

{kind=link}

Energy Information Administration

If we get peak production in the Permian in 4Q24 (as discussed in this article ) and long-term oil demand growth, I expect oil prices to remain elevated and work their way into triple-digit territory.

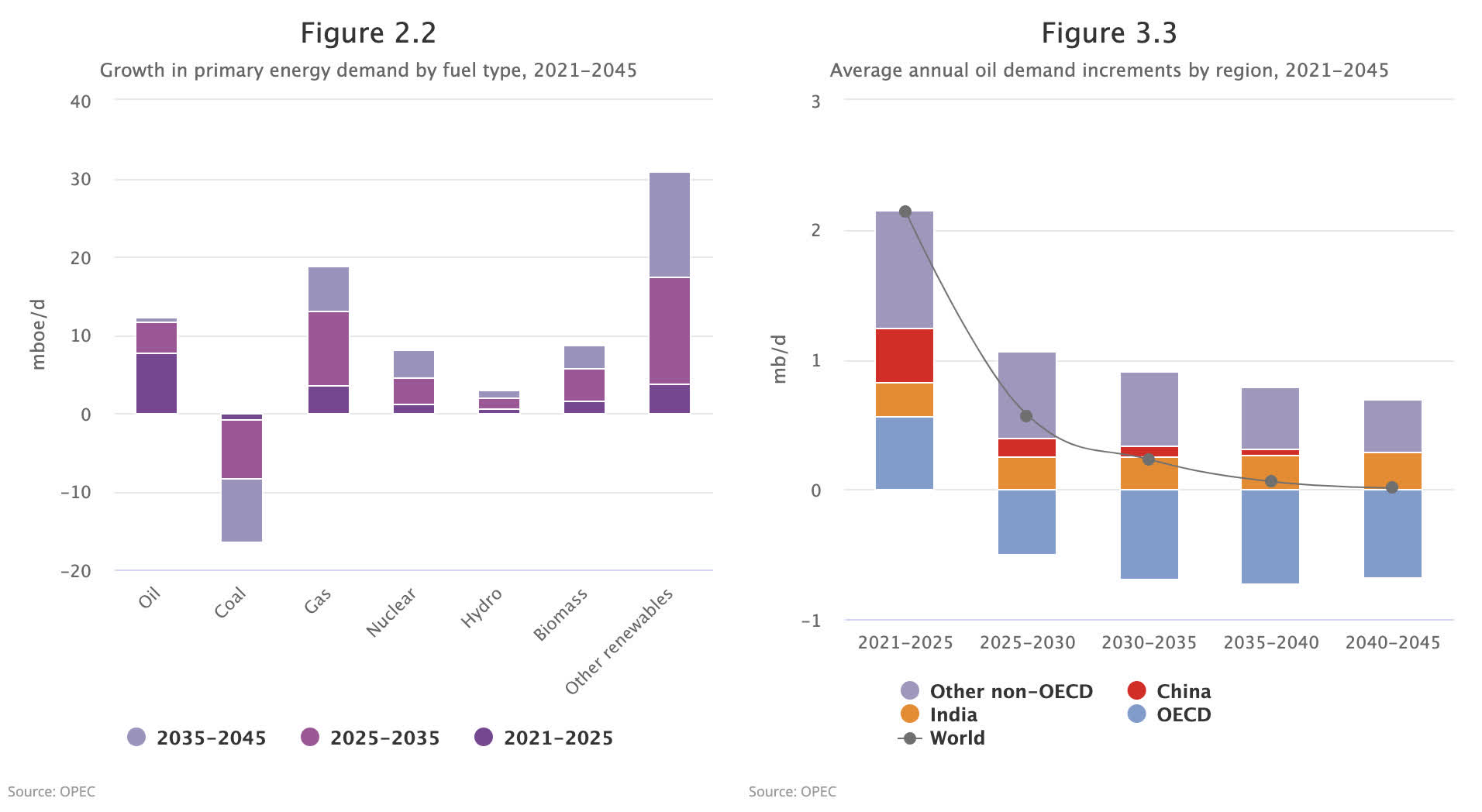

This is what long-term oil demand might look like:

{kind=link}

OPEC (Long-Term Demand Estimates)

To prepare for such a scenario, I have bought 19% energy exposure, which I expect to increase even further.

I'm not rooting for elevated inflation. I just want to be prepared. After all, if I'm right, we could see a development that is negative for the market, in general. This would also apply to a lot of my other holdings.

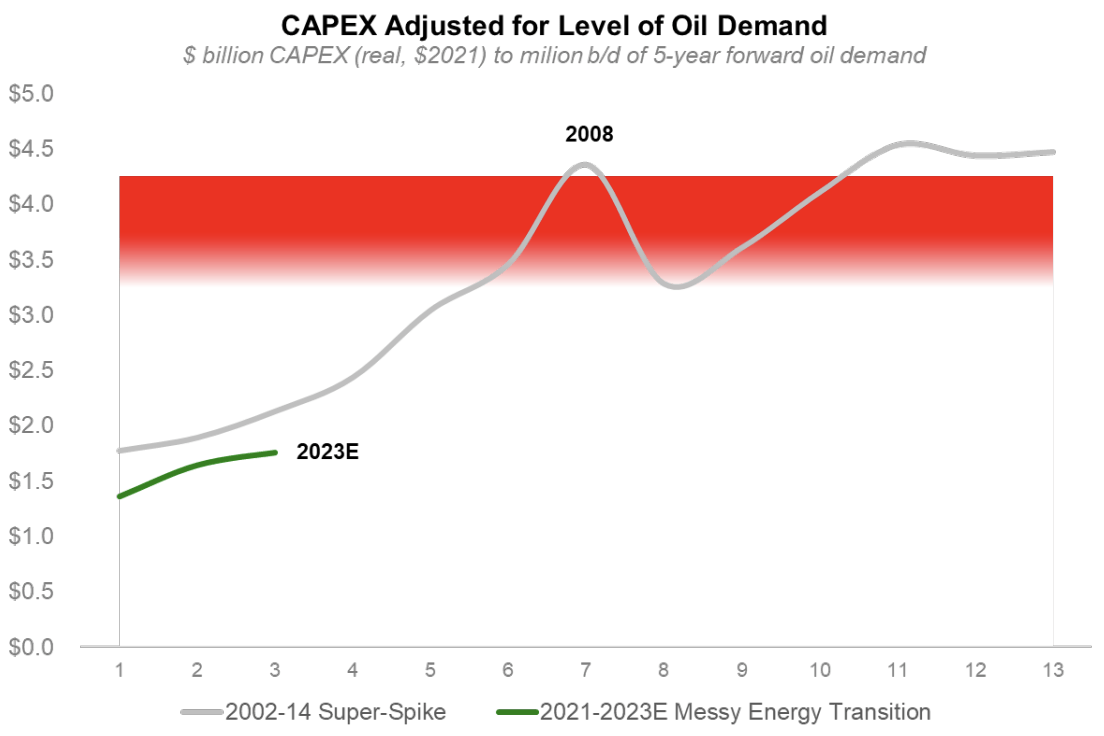

The chart below reinforces my view, as investments in oil supply remain well below levels that would support rising demand growth. This is inflationary, especially if demand comes roaring back.

{kind=link}

IEA, S&P Capital IQ (Via Super Spiked)

Given the shift in supply dynamics, I believe that upstream oil companies (the ones that drill for oil) are the best way to get the job done.

In this case, I focus on:

- Companies with deep reserves. Because drillers are running out of Tier 1 reserves, some will be forced into (risky) M&A deals.

- Companies with very efficient production. These companies have low breakevens, allowing them to generate high free cash flow - even at subdued oil prices.

- Companies with healthy balance sheets. I don't have the patience anymore to buy companies with high debt loads. I need healthy balance sheets that lower financial risks. Also, healthy balance sheets allow companies to distribute their free cash flow to shareholders.

- Companies that are willing to distribute most of their free cash flow to shareholders through (special) dividends and buybacks. I prefer (special) dividends.

One company that checks all boxes is Pioneer Natural Resources ( PXD ) .

On May 14, I wrote an article titled I Made Pioneer My Largest Energy Investment .

That's exactly what I did, as the company now accounts for more than 5.3% of my portfolio.

In this article, I went with a bullish title again, as I want to consolidate my energy holdings. I'm looking to shift some money from Chevron ( CVX ) into PXD purely because I prefer its aggressive shareholder distribution plans.

While I haven't made a final decision on the CVX to PXD shift, I'll also deploy new capital, as I believe I need to own more oil.

And what better way to buy oil than via PXD?

So, let's dive into the details!

PXD Continues To Shine

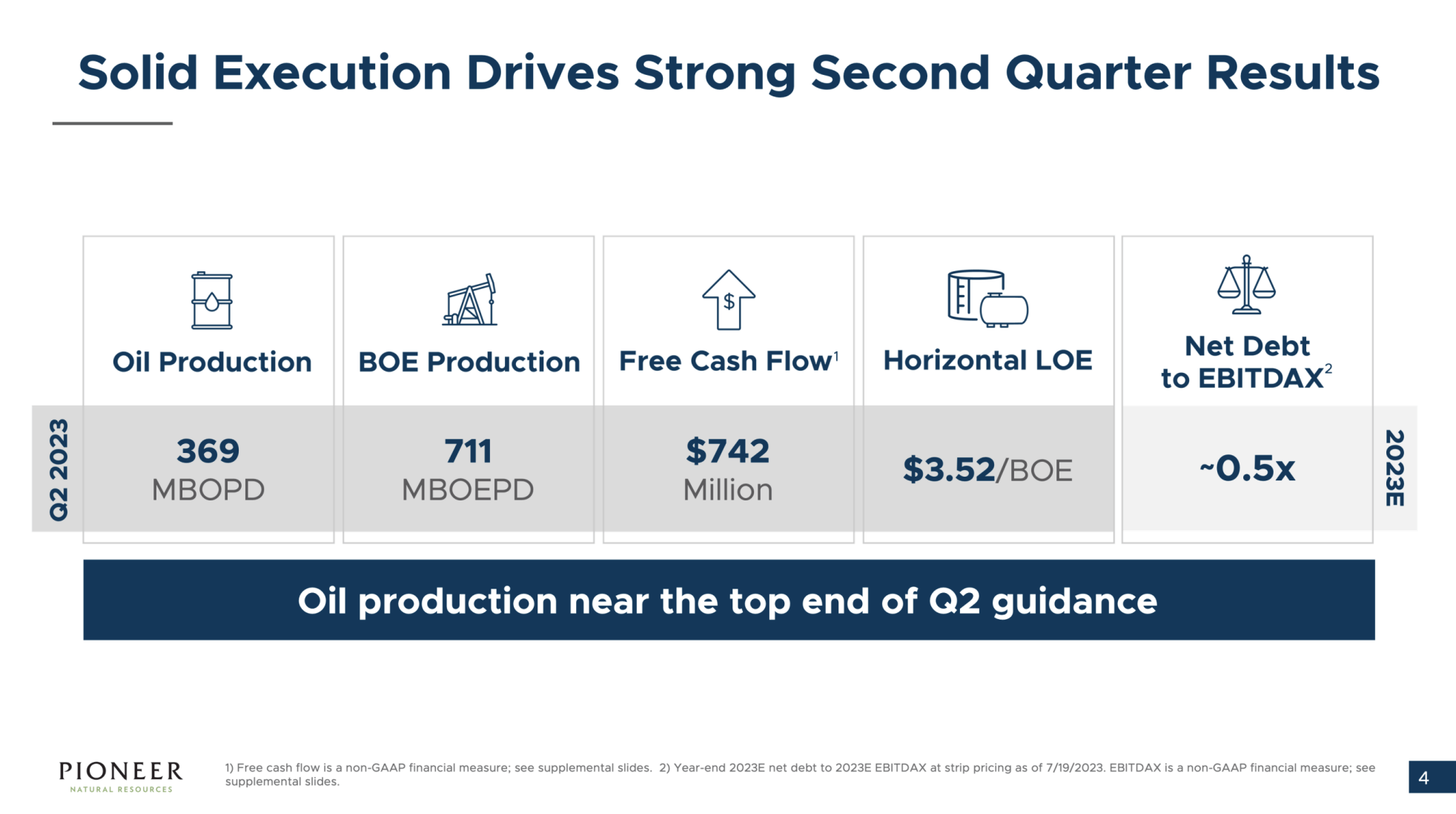

With a $55 billion market cap, PXD is one of America's largest onshore oil producers. In the second quarter, the company produced roughly 370 thousand barrels of oil per day. It also produced 341 thousand barrels (48%) of equivalent.

It has a 0.5x net leverage ratio with a BBB+ credit rating.

{kind=link}

Pioneer Natural Resources

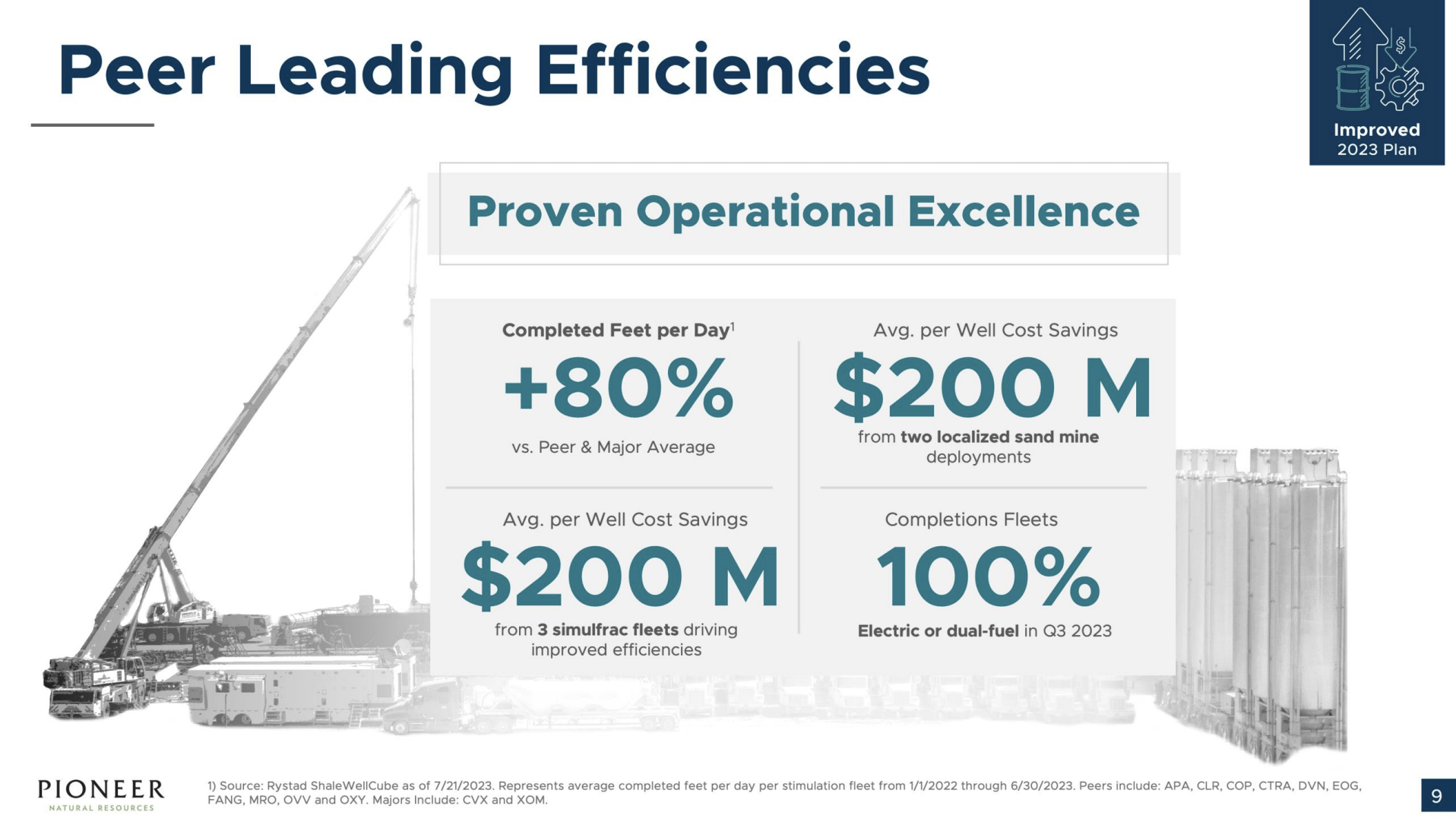

The company exclusively produces its oil in the Permian basin, where it achieved industry-leading efficiency.

For example, the company not only achieved higher-than-expected production in the second quarter, but it is also capable of boosting output with subdued CapEx.

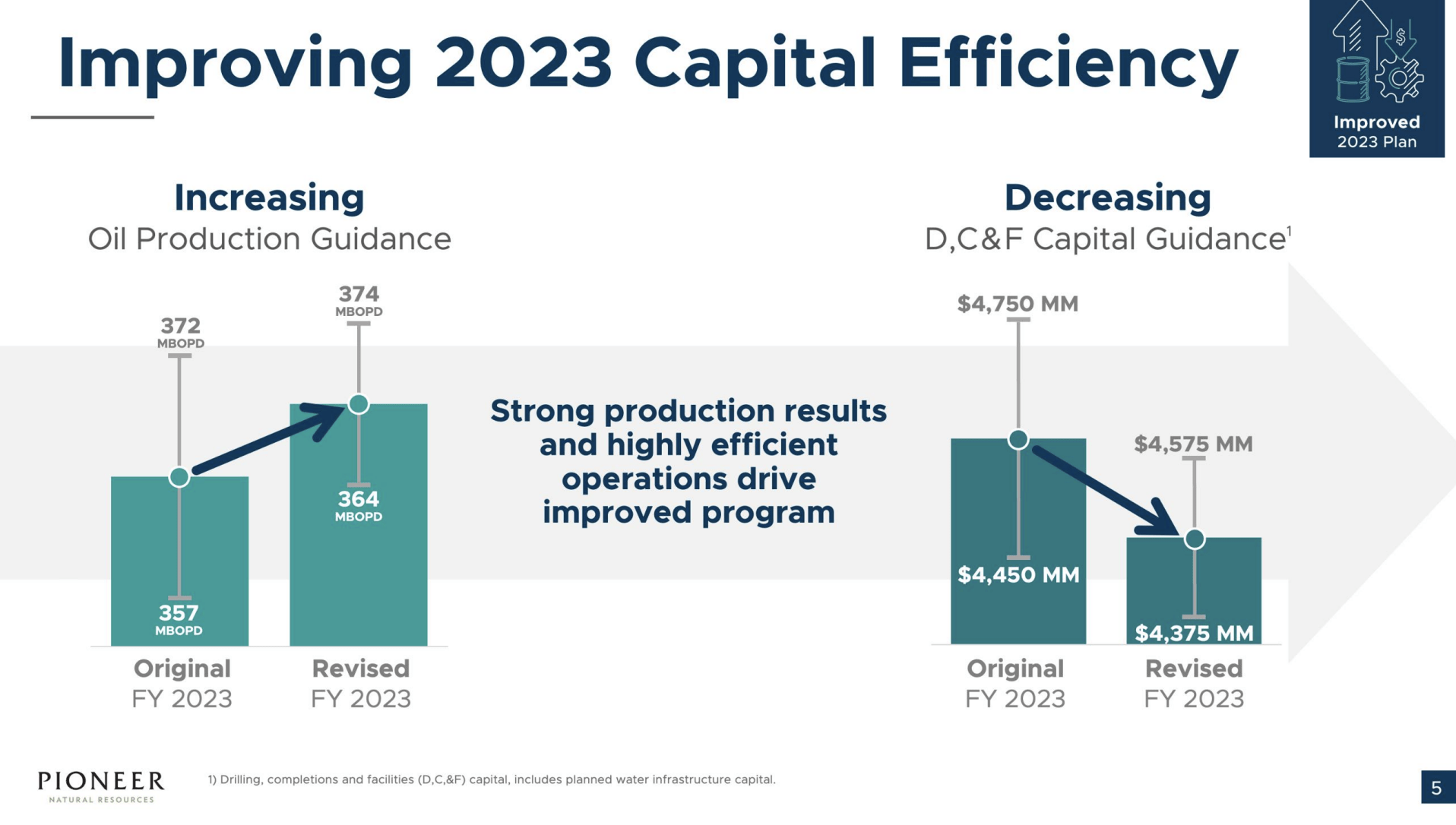

In the second quarter, the company raised its production guidance for the year while reducing the capital budget allocated to drilling, completions, and facilities.

{kind=link}

Pioneer Natural Resources

The oil production guidance midpoint is now 369 thousand barrels of oil per day, and the revised drilling, completions, and facilities capital budget is $125 million lower than the initial 2023 outlook.

This adjustment was attributed to the efficient execution of well-productivity and operational activities by its teams, leading to a more capital-efficient program.

The company's investment framework remains aligned with moderate annual production growth of up to 5%.

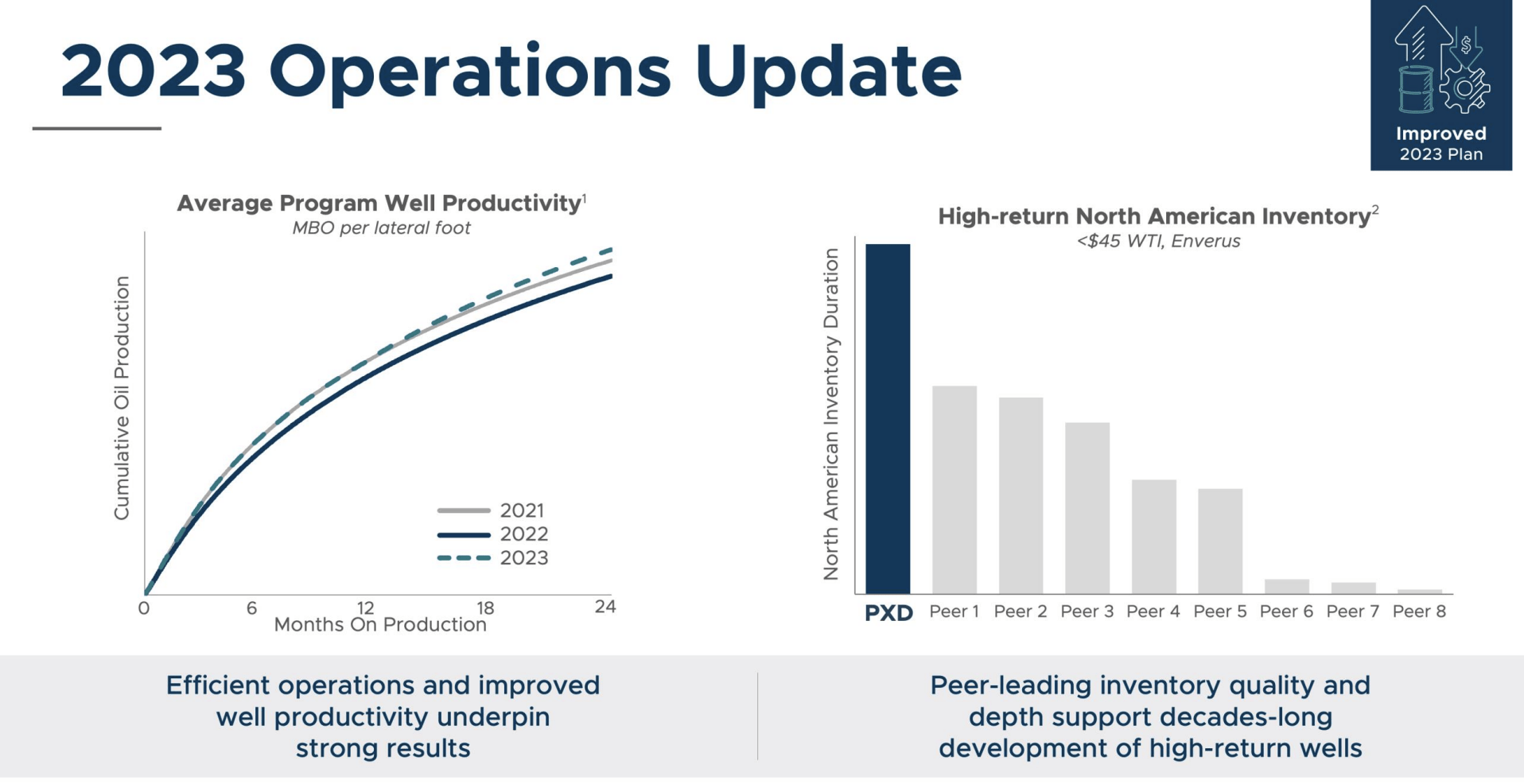

Furthermore, the company's 2023 average well productivity significantly surpassed both 2022 and 2021 levels over the first 24 months of production.

According to the company, its focus on full-stack development enhances long-term recovery and optimizes returns.

Essentially, the company's substantial inventory of low-breakeven, high-margin locations positions it favorably compared to peers. With roughly 15,000 top-tier locations, Pioneer believes it is set for best-in-class development in the years to come.

{kind=link}

Pioneer Natural Resources

While it isn't visible in the chart below, the company has more than 20 years' worth of top-tier drilling, which surpasses any of its major peers.

{kind=link}

Pioneer Natural Resources

But wait, the good news continues!

The company is also getting better access to export markets for its natural gas. In the second half of this year, the company expects to sell 70% of its gas out of the basin. Next year, that number is expected to be 80%, thanks to new pipelines leading to the Houston Ship Channel.

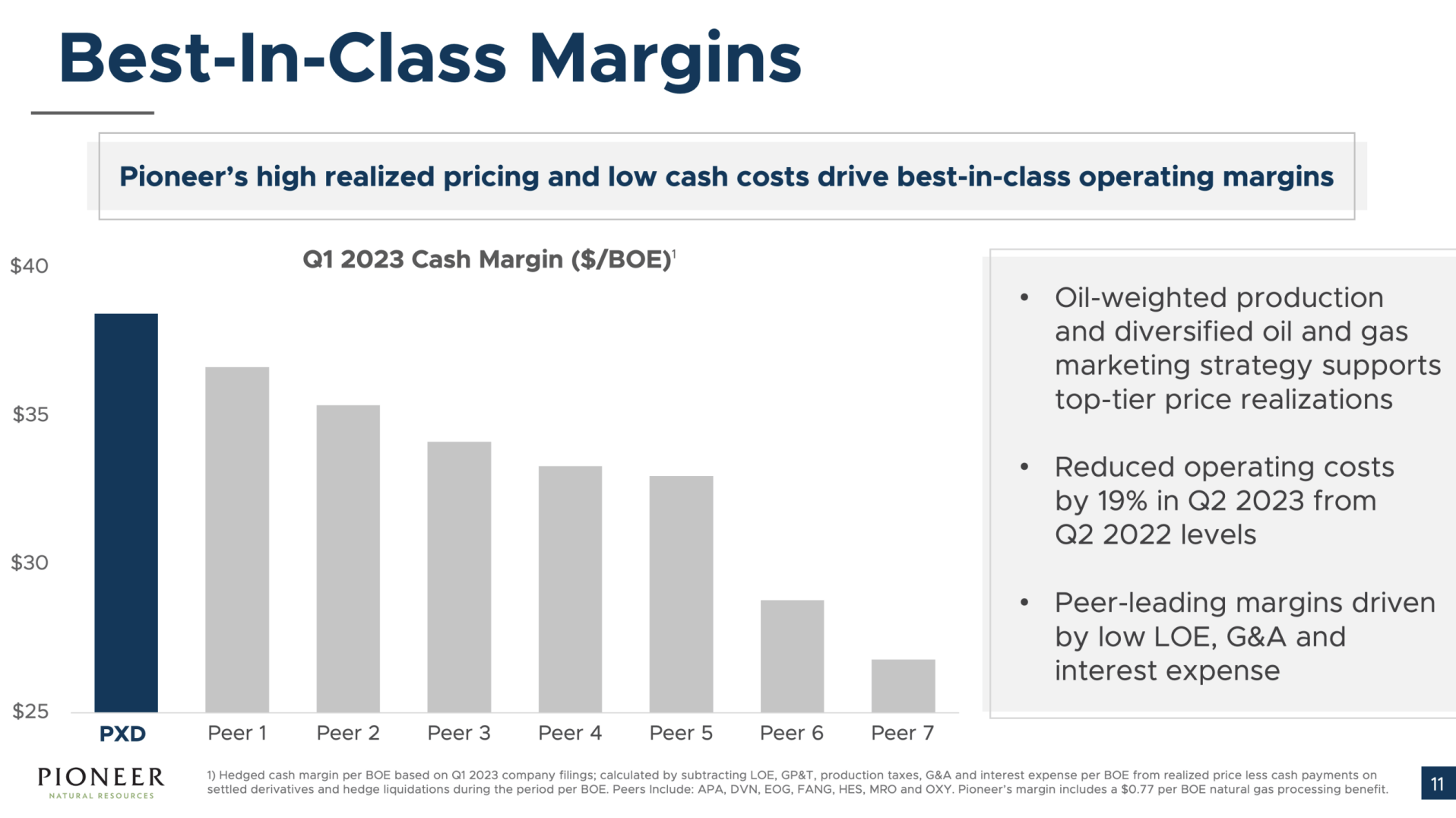

In 1Q23, the company received 19% higher prices for its gas than its peers.

In general, it has much higher cash margins. In 1Q23, the company had cash margins close to $37 per barrel, exceeding any of its major peers.

{kind=link}

Pioneer Natural Resources

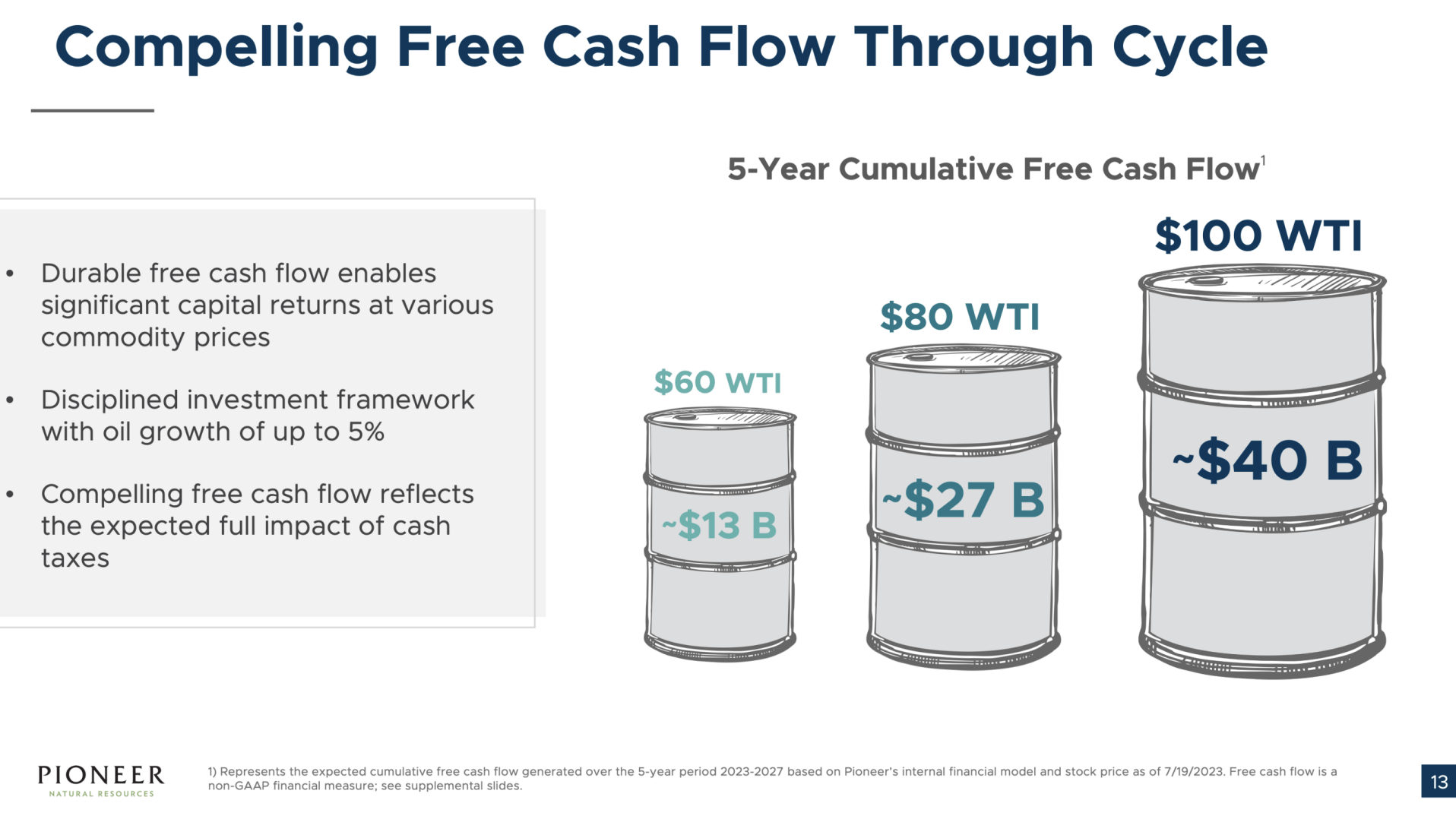

Thanks to these efficiencies, the company believes it can generate $27 billion in cumulative free cash flow over the next five years at $80 WTI - that's the current oil price.

{kind=link}

Pioneer Natural Resources

$27 billion is 49% of its current market cap. At $100 WTI, that number rises to $40 billion (73%).

I'm adding the implied free cash flow yield because the company has a very ambitious capital return plan.

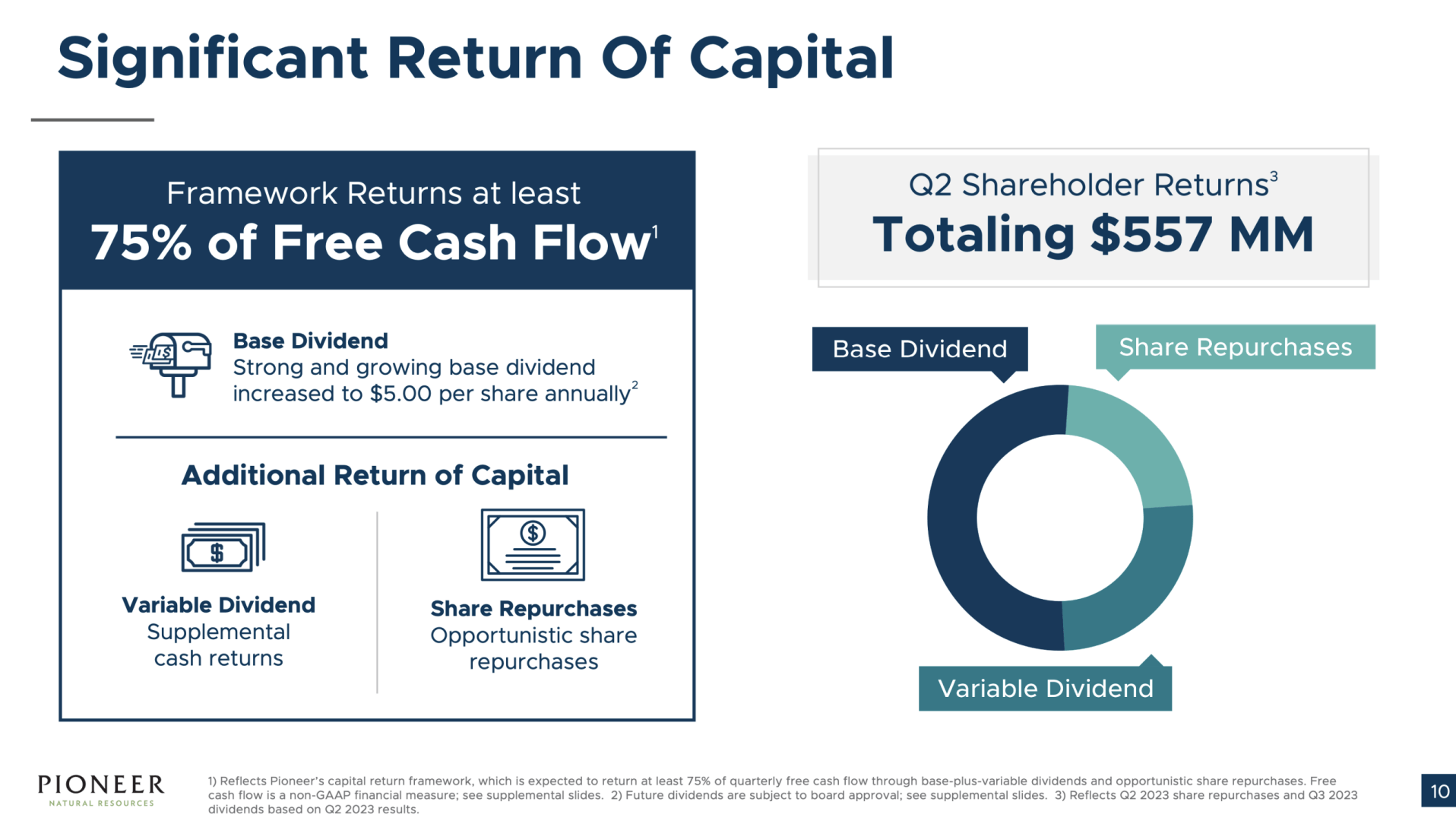

The company aims to distribute at least 75% of its free cash flow to shareholders through its base dividend, the variable dividend, and buybacks.

{kind=link}

Pioneer Natural Resources

At $90 WTI, the company has the potential to achieve a double-digit return yield, which would be great for income-focused investors.

On a long-term basis, I expect investors to benefit from total annual dividends exceeding 10%.

For the third quarter (payable on September 21 for shareholders of record on September 6), the company is paying $1.84 per share. This consisted of a $1.25 base dividend and a variable component of $0.59.

The annualized yield is 3.1%.

Please note that the steep drop in its special dividend is likely temporary.

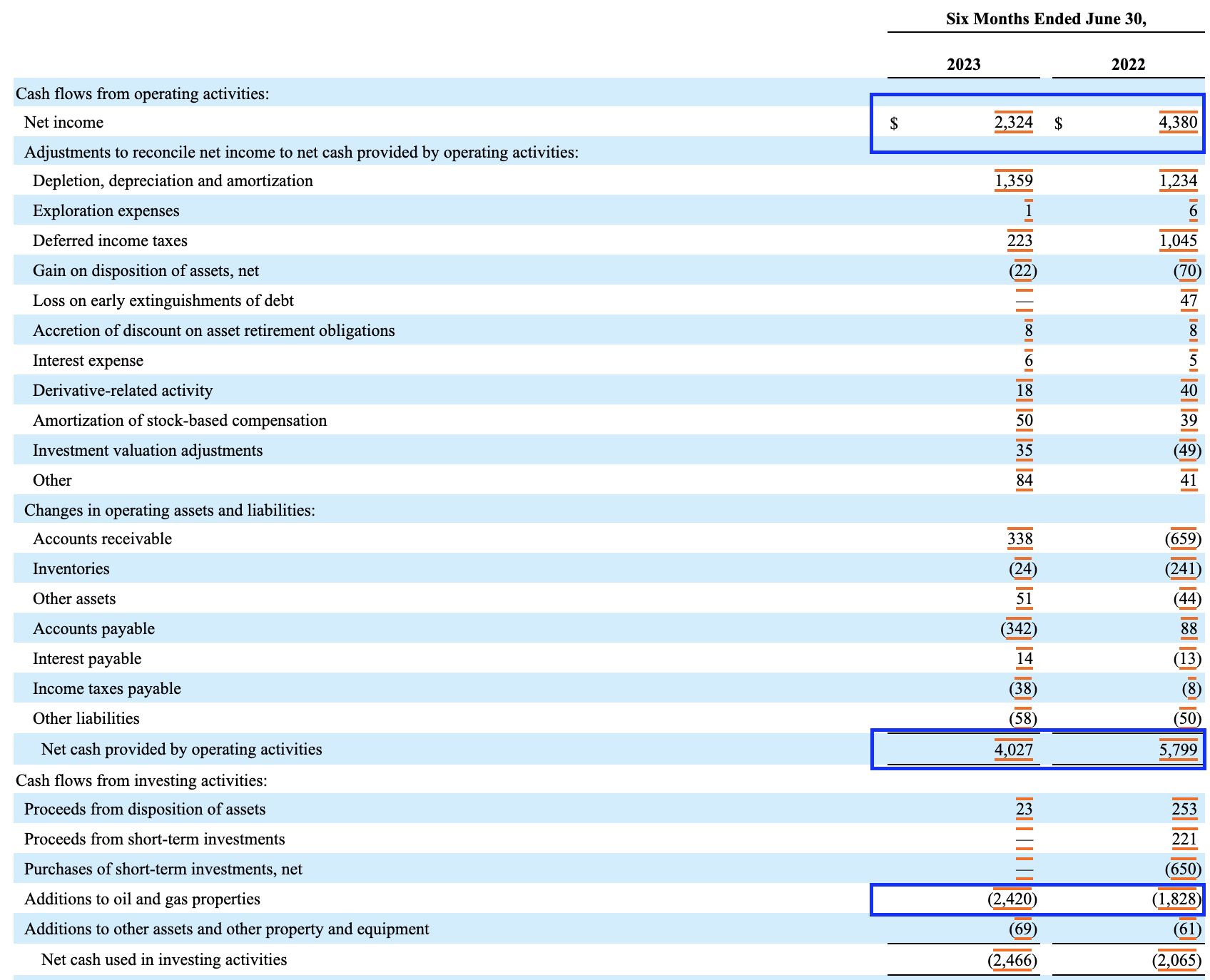

- The company saw an operating cash flow decline from $5.8 billion in 2Q22 to $4.0 billion in 2Q23.

- Investments in oil and gas assets rose from $1.8 billion to $2.4 billion.

{kind=link}

Pioneer Natural Resources (Author annotations)

Now, oil prices are much higher, and investment volumes will likely subdue.

I expect the next dividend announcement to come with a much juicier special dividend.

Outperformance & Valuation

I've spent the past few years praising PXD. Hence, I'm happy that PXD is outperforming its peers.

Compared to pre-pandemic levels, PXD shares have returned 67% compared to five years ago. The Energy ETF ( XLE ) and Oil & Gas Exploration & Production ETF ( XOP ) have returned 52% and -2%, respectively.

Going back ten years, the performance is somewhat equal at 67%, caused by the poor price levels of oil and gas after the 2014 peak.

Going forward, I expect PXD to continue outperforming its peers and the S&P 500, as I believe in prolonged sticky inflation and the tailwinds that come with a new era for oil supply growth.

Hence, I'm considering buying much more PXD, including the proceeds of my successful Chevron investments. While I believe that Chevron is one of the best-diversified energy investments, I prefer PXD because of its focus on drilling and high shareholder returns.

Please note that I haven't made a final decision. I may keep CVX and boost PXD purely using new cash.

Valuation-wide, I believe that PXD is undervalued. This is mainly based on my oil outlook and its potential to generate strong, double-digit free cash flow at elevated oil prices.

Investors will likely recognize that and keep moving funds into the company and its peers.

The current consensus price target is $257, which is 9% above the current price.

On a longer-term basis, I expect PXD to move well beyond $350 if oil prices go into triple-digit territory.

Takeaway

My bullish outlook on oil has been reaffirmed as supply dynamics shift and demand remains strong.

The decline in legacy production and the end of the U.S. shale revolution are bolstering oil prices, with the Permian basin losing momentum.

To capitalize on this trend, I've increased my energy exposure, favoring upstream companies with deep reserves, efficient production, and healthy balance sheets.

Pioneer Natural Resources stands out as a prime candidate, boasting industry-leading efficiency and substantial low-breakeven locations.

With its strategic focus on shareholder distribution and potential for substantial free cash flow, PXD aligns perfectly with my long-term vision.

While I may still decide on the Chevron to PXD shift, PXD's reserves, the potential for outperformance, and special dividends make it a compelling choice in the evolving energy landscape.

Reasons To Be Bullish

- Efficiency Leader: PXD excels in onshore oil production, displaying efficiency in the Permian basin. It consistently surpasses output expectations while keeping spending in check.

- Robust Cash Margins: With cash margins around $37 per barrel, PXD's profitability outshines its peers, offering strong free cash flow potential even at subdued oil prices.

- Strategic Gas Markets: PXD's approach to gas sales, both now and in the pipeline, bolsters revenue prospects and adds to its strong cash flow potential.

- Investor-Focused: PXD's commitment to shareholder value shines through aggressive dividends and buybacks, potentially leading to double-digit returns at $90 WTI (and beyond).

For further details see:

I Might Double My Pioneer Natural Resources Investment - Again