SPG - I Pity The Fool That Doesn't Own These A-Rated REITs

Summary

- Did you know that some of my followers call me Mr. T?

- That shouldn’t be a surprise since my last name is Thomas, right?

- I pity the fool that doesn’t own these A-rated REITs.

Here's a question for my "old" millennials and the generations before. Those younger than, say, 35, might not have a clue what I'm about to talk about.

There are plenty of TV shows that have debuted since January 1983, after all. And who has time to go back and watch the series your parents did?

Even if they're classics like The A-Team .

The A-Team revolved around a special forces unit that served in Vietnam. After robbing the Bank of Hanoi as ordered, they were then framed for the heist and sent to military jail. But they escaped - determined to clear their names - and helped others along the way as essentially hero vigilantes.

The main characters on this memorable team were:

- Colonel John "Hannibal" Smith, a smart, savvy tactician and a master of disguise who loved to smoke cigars

- First Lieutenant Arthur Templeton "Faceman" Peck, the ladies' man who could con and scrounge with the best of them

- Captain H.M. "Howling Mad" Murdock, a flying pro despite being classified as clinically insane

- Sergeant First Class Bosco Albert "B.A." Baracus, the larger-than-life master at arms played by Mr. T. who could fix almost anything and growl the fear into any fool.

That was the A-Team. And, man, could they get things done.

Forget the Casting Calls; There's Only the Original to Consider

The A-Team was a fictional story, of course. But it left quite the impression on its viewers. Wikipedia - which I always have to clarify I only quote when it comes to pop-culture types of topics - says that:

"In a Yahoo! survey of 1,000 television viewers published in October 2003, The A-Team was voted the 'oldie' television show viewers would most like to see revived, beating such popular television series from the 1980s as The Dukes of Hazzard and Knight Rider."

There was clearly a nostalgia factor at work, and I don't think the last 20 years has changed that.

Yet I don't think a rerun would live up to any of our expectations. Who could possibly play B.A. the way Mr. T. did? Name me one actor who could suffice.

For proof of this, note the audience ratings for the original TV show versus the 2010 movie someone thought it was a good idea to make.

The former has 7.5 out of 10 stars; the latter just 6.7. And I have to wonder how many of those even somewhat satisfied viewers knew the shoes those other actors were trying to fill.

To quote "SnoopyStyle," who awarded the movie a mere four stars:

"Liam Neeson [who plays Hannibal] is too grumpy. Bradley Cooper is good having fun with Face. Sharito Copley is a bad Murdock. The problem is that these characters are so iconic in TV history. Other than Cooper, nobody really hit it on the head.

"This is just an excuse to put in ridiculous action. It's all very disappointing. It's missing the heart of the TV show. It's missing the humor and the chemistry of the group."

If I had watched it, which I didn't, I'd probably have felt the same.

A REIT A-Team I'm Proud to Present

Okay. Enough reminiscing.

Those of us who knew and loved the show can probably all agree it's a tough act to follow. And I'm sure it's never coming back regardless.

Fortunately, there are other A-rated teams out there to help us when the chips are down. Even better, some of them are real.

The portfolio of real estate investment trusts (REITs) I write about below certainly are. And not just in the sense that they're actual companies that operate in the actual world.

They're also the real deal when it comes to their balance sheets.

It's not easy to achieve an A-rated operation, where growth is weighed so well against debt. There are a lot of columns that have to tally up appropriately, which means a lot of factors handled extremely well.

And to not only achieve that status but maintain it quarter after quarter and year after year? I challenge even the fictional A-Team to manage that.

After all, as I recall (with Wikipedia's prompting), the TV show with all of its fiction-based allowances started going downhill after the third season:

"During the show's first three seasons, The A-Team managed to pull in an average of 20% to 24% of all American television households… During the second season, the ratings continued to soar, reaching fourth place in the twenty-highest rated programs behind Dallas and Simon & Simon, in January (mid-season), while during the third season, it was beaten out only by two other NBC shows, including The Cosby Show."

Season 4 wasn't so kind. And Season 5 was received poorly enough that the show got cancelled.

The REITs below, on the other hand, are very much positioned to keep their ratings for quite a while to come…

Prologis, Inc. (PLD): S&P Credit Rating: A

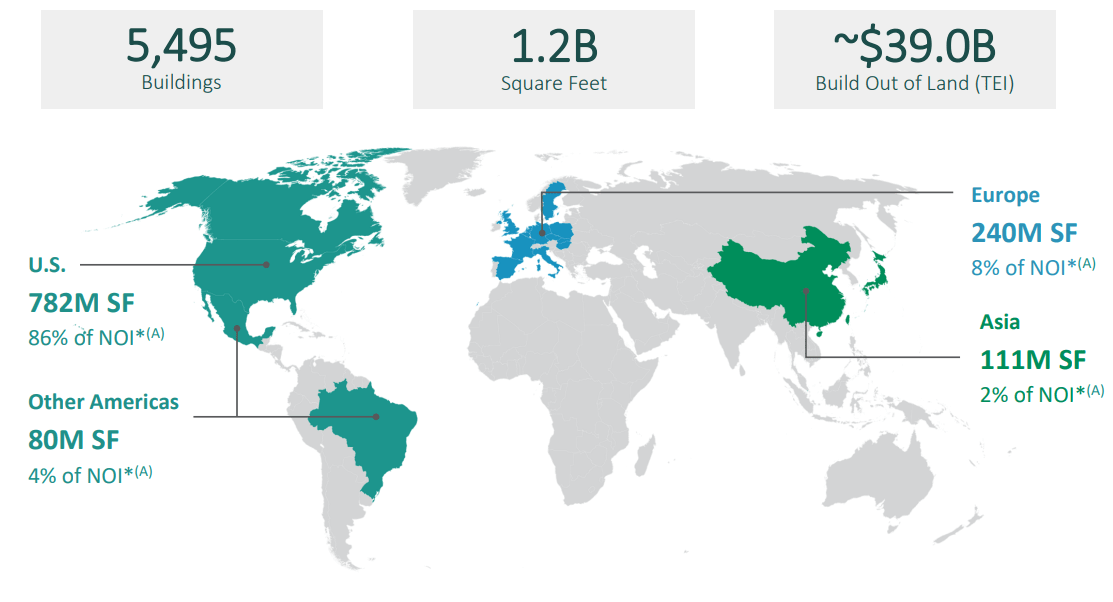

Prologis is a real estate investment trust in the industrial sector. They are the global leader in logistics properties with 5,495 buildings covering 1.2 billion square feet in 19 countries. They serve approximately 6,600 customers in two main categories: business to business and online fulfillment.

Prologis - 4Q 2022 Supplemental

{kind=link}

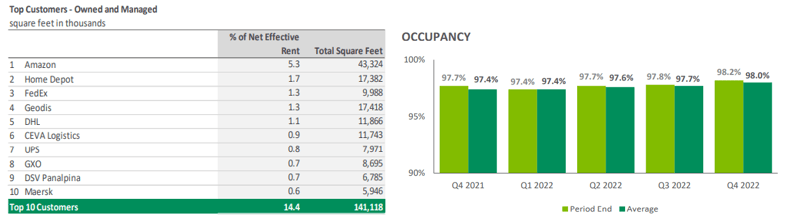

Prologis is diversified in its geographic locations as well as its tenant base. In addition to having 6,600 customers, their top 10 customers only make up 14.4% of their rent while their top 25 customers only contribute 20.5%. At the end of 2022, PLD's occupancy rate stood at 98.0%.

PLD has some very well-known names among its top ten customers such as Amazon, Home Depot, FedEx, and UPS. This diversified and high quality tenant base should provide PLD with earnings stability for years to come.

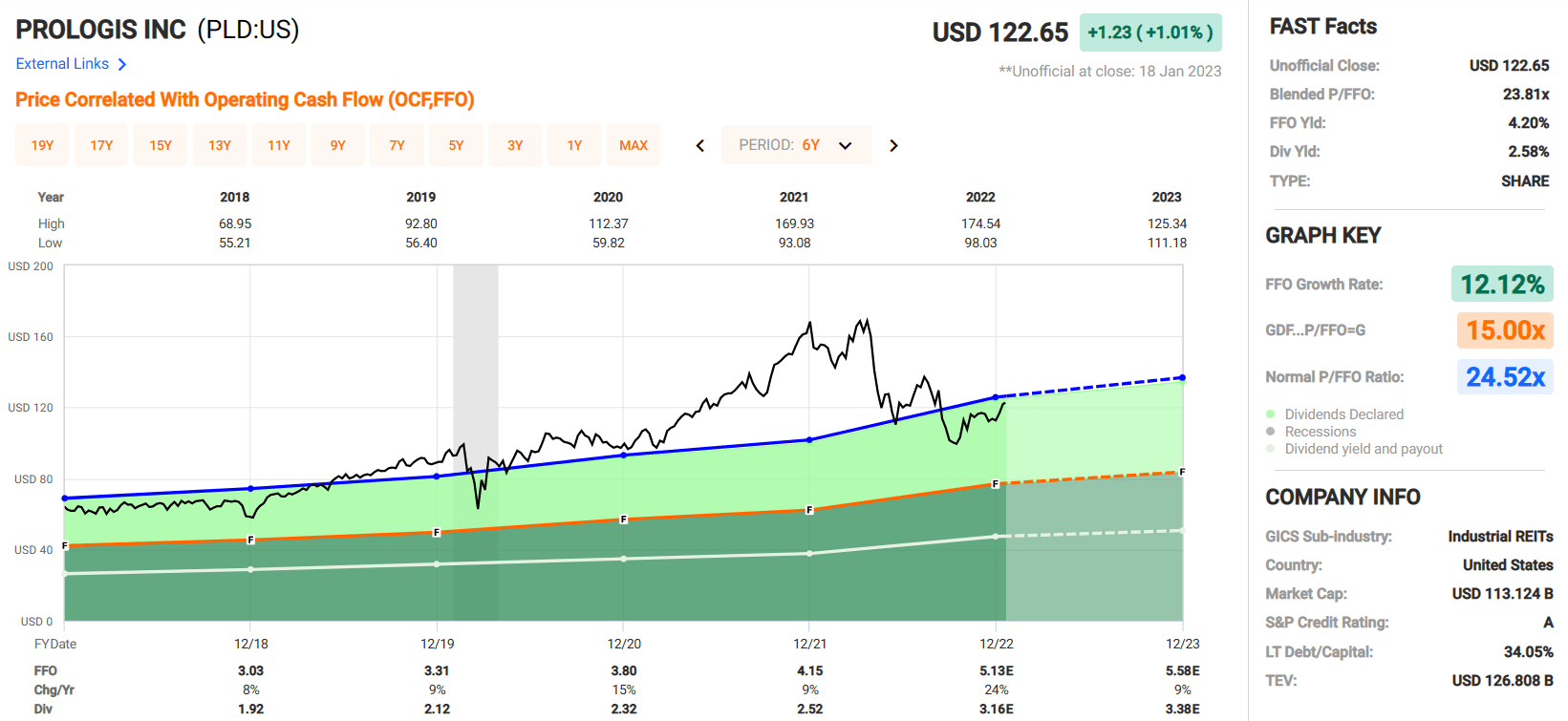

Regarding earnings, Prologis released its full-year earnings for 2022 on January 18, 2023. Core FFO (funds from operations) came in at $5.16 per diluted share for the full year 2022, up from $4.15 in 2021.

Prologis - 4Q 2022 Supplemental

{kind=link}

Prologis has excellent debt metrics with a debt to gross real estate assets of 28.2%, a fixed charge coverage ratio of 11.2x, and a debt to adjusted EBITDA of 4.0x.

Their debt has a weighted average interest rate of 2.5% and their weighted average term to maturity is 9.1 years. At the end of 2022 Prologis had $3.8 billion available to them under their credit facilities and $278 million in cash and cash equivalents for a total liquidity of $4.1 billion.

Prologis - 4Q 2022 Supplemental

Prologis currently has a dividend yield of 2.58% that is very secure, with an AFFO (adjusted FFO) payout ratio of 72.56% and a 10-year average dividend growth rate of 11.13%

The projected FFO growth in 2023 is expected to come in at 9% and its blended 6 year average FFO growth stands at 12.12%.

Currently, PLD is trading at a blended FFO multiple of 23.81 which is a discount to its historic FFO multiple of 24.52x. At iREIT, we rate Prologis a STRONG BUY.

{kind=link}

Realty Income Corporation (O): S&P Credit Rating: A-

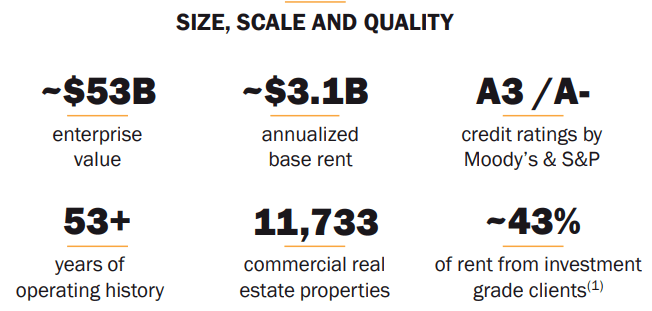

Realty Income is a triple-net real estate investment trust that owns and leases single tenant free-standing properties. As of 9/30/22, they owned approximately 11,733 properties located in all 50 states with international properties in the UK and Spain.

They have declared 631 consecutive monthly dividends and increased the dividend 118 times since their public listing in 1994. Realty Income has a 27 year streak of dividend increases, making them one of the elite members of the S&P 500 Dividend Aristocrat index.

Realty Income - Investor Presentation

{kind=link}

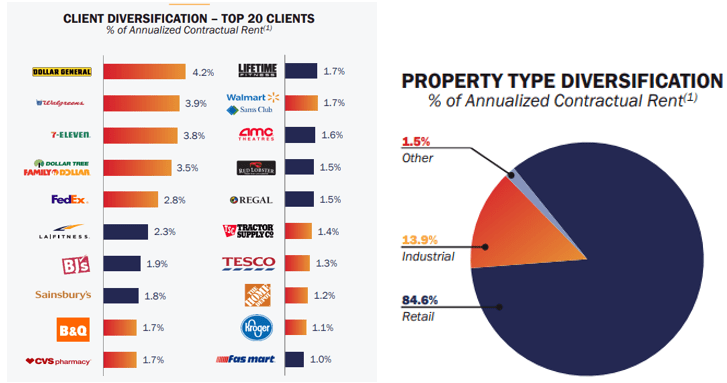

Realty Income has a high-quality tenant base with names like Dollar General, Walgreens, 7-Eleven, Walmart, Home Depot, and FedEx listed among their top 20 clients.

In all, their top 20 clients make up 41.60% of their annual rent. Although they are primarily concentrated in retail properties, 13% of their annual contractual rent comes from industrial properties.

Realty Income - Investor Presentation

{kind=link}

Realty Income has great credit metrics, with a Net Debt to Annualized Pro Forma adjusted EBITDA of 5.2x and a 5.5x Fixed Charge Coverage Ratio. 95% of their debt is unsecured and 88% is fixed rate.

Their weighted average term to maturity is 6.3 years and their total debt is 31% of their total market capitalization.

As of 3Q22 Realty Income, had $2.3 billion available to them under their revolving credit facility and $188 million in cash & equivalents for total liquidity of $2.5 billion.

Realty Income - Investor Presentation

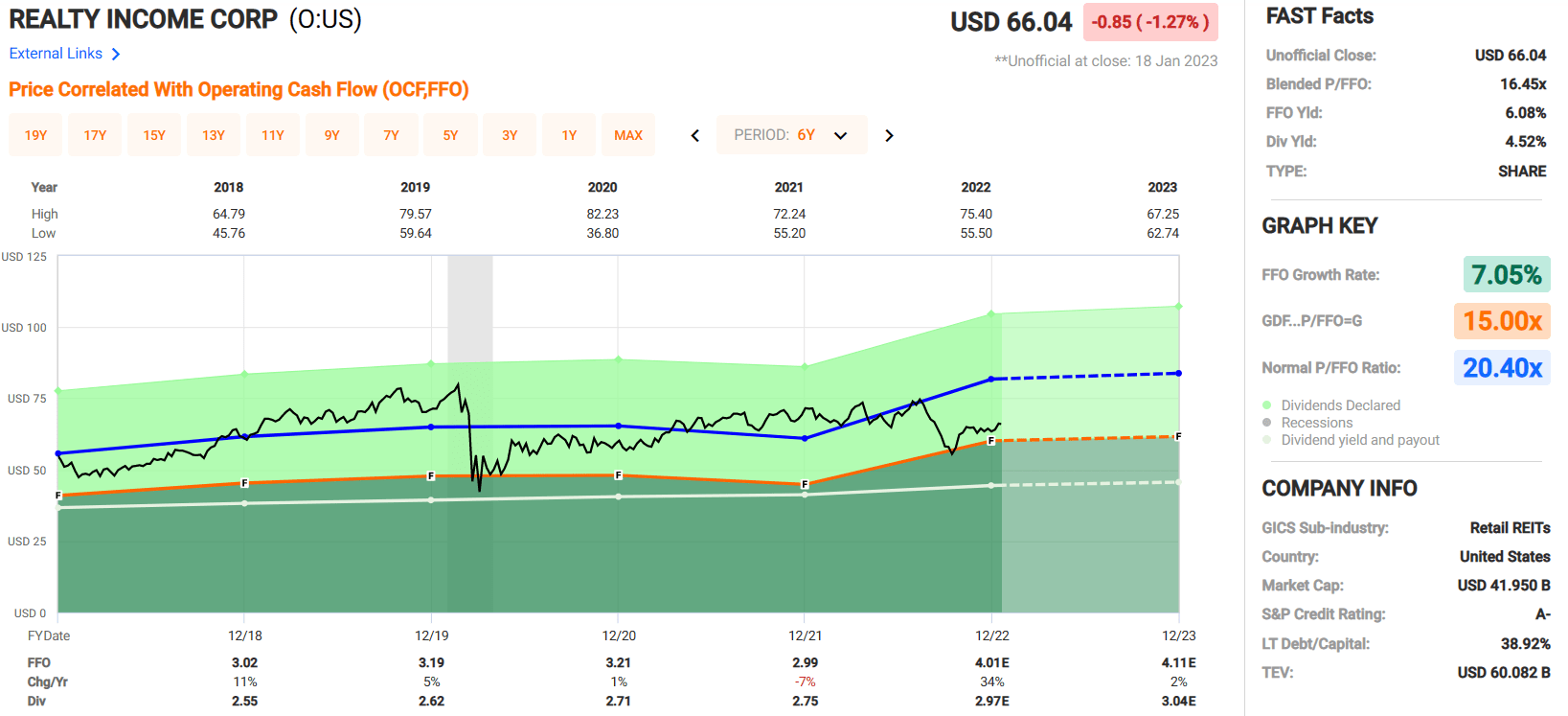

Realty Income currently has a dividend yield of 4.52% that is very secure, with an AFFO payout ratio of 76.17%. They have a blended average FFO growth rate of 7.05% rate over a 6-year period and currently trade at a blended P/FFO of 16.45x, which is a discount from their normal P/FFO of 20.40x. At iREIT, we rate Realty Income a BUY.

{kind=link}

Simon Property Group, Inc. ( SPG ): S&P Credit Rating: A-

Simon Property Group is a real estate investment trust that owns, develops, and manages Class-A Malls, Premium Outlets, The Mills, and International Properties. As of 3Q22 they owned or had an ownership interest in 230 properties covering 184 million square feet in North America, Europe, and Asia.

SPG also has an 80% ownership interest in The Taubman Realty Group ("TRG"), which owns super-regional and outlet malls and a 22.4% interest in Klépierre that owns shopping centers in 14 European countries.

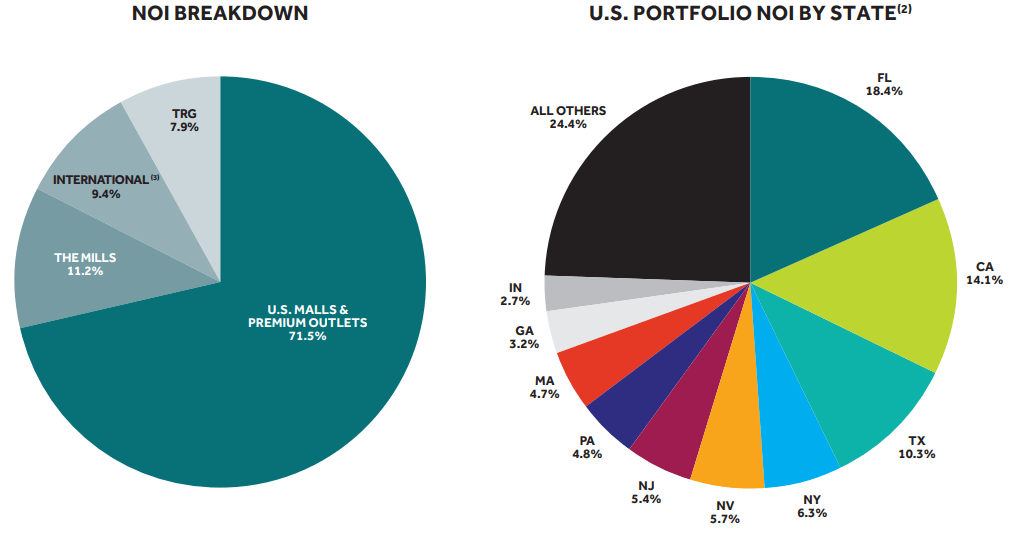

The primary source of their Net Operating Income ((NOI)) came from U.S. Malls and Premium Outlets with NOI of 71.5%. Followed by 11.2% NOI from The Mills, 9.4% NOI from international properties, and 7.9% NOI came from their interest in Taubman Realty.

SPG has a relatively large concentration of properties in Florida, California, and Texas, but overall, they are geographically diversified with properties across the U.S. as well as their international interests in Klépierre and Taubman Realty.

SPG 3Q 2022 Supplemental Information

{kind=link}

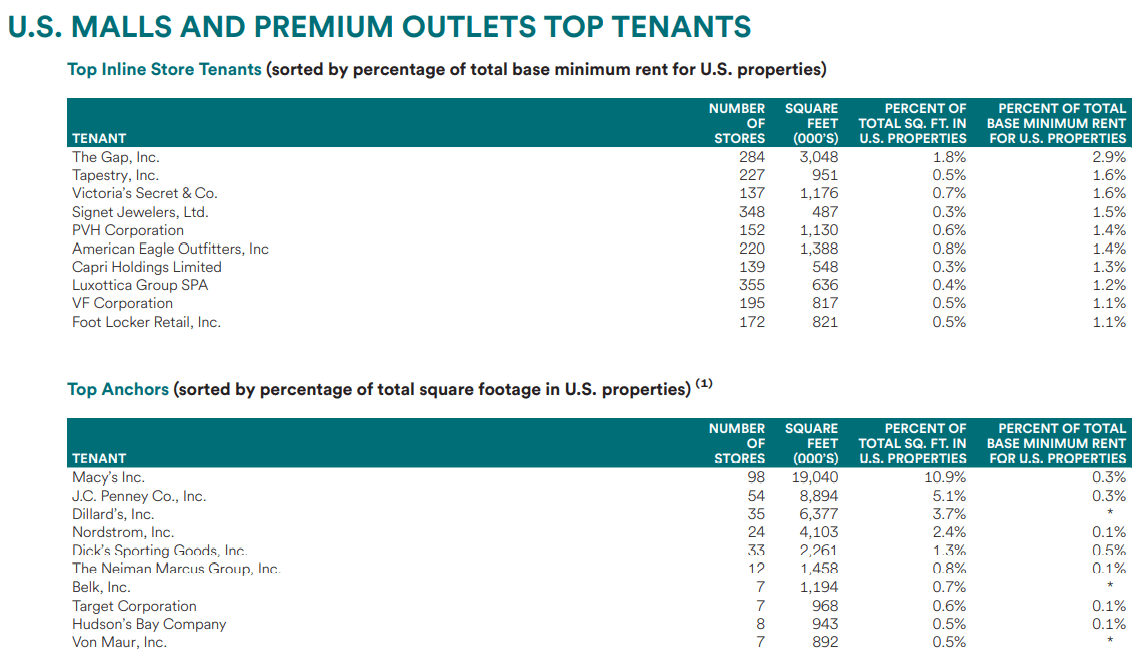

Simon is well-diversified by tenant, with their largest tenant, The Gap, Inc., only making up 2.9% of their base rent while their top 10 Inline Store tenants combined only make up a total of 15.10% of their base rent.

Simon has some notable names listed among their top tenants, including The Gap, Victoria's Secret, American Eagle Outfitters, Macy's, and Dick's Sporting Goods.

SPG 3Q 2022 Supplemental Information

{kind=link}

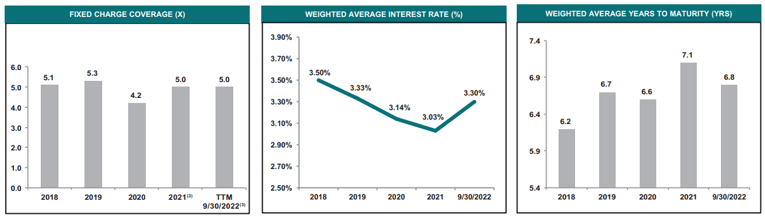

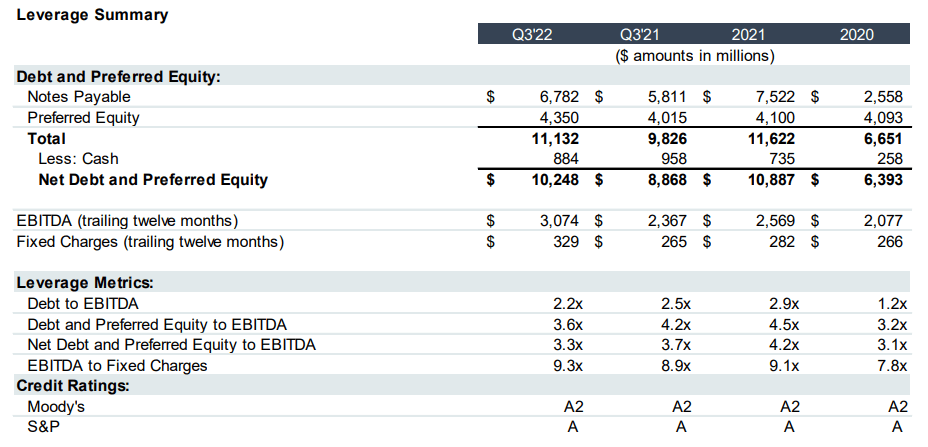

Simon has a strong credit profile with a Total Debt to Total Assets ratio of 42%, a Net Debt to EBITDA of 6.6x (as of 2Q22) and a Fixed Charge Coverage of 5.0x as of 9/30/22.

Their weighted average interest rate is 3.30% and their weighted average term to maturity is 6.8 years. Additionally, as of September 30, 2022, SPG had $7.4 billion available to them under their revolving credit facilities and $1.2 billion in cash for a total of $8.6 billion in liquidity.

{kind=link}

SPG 3Q 2022 Supplemental Information

{kind=link}

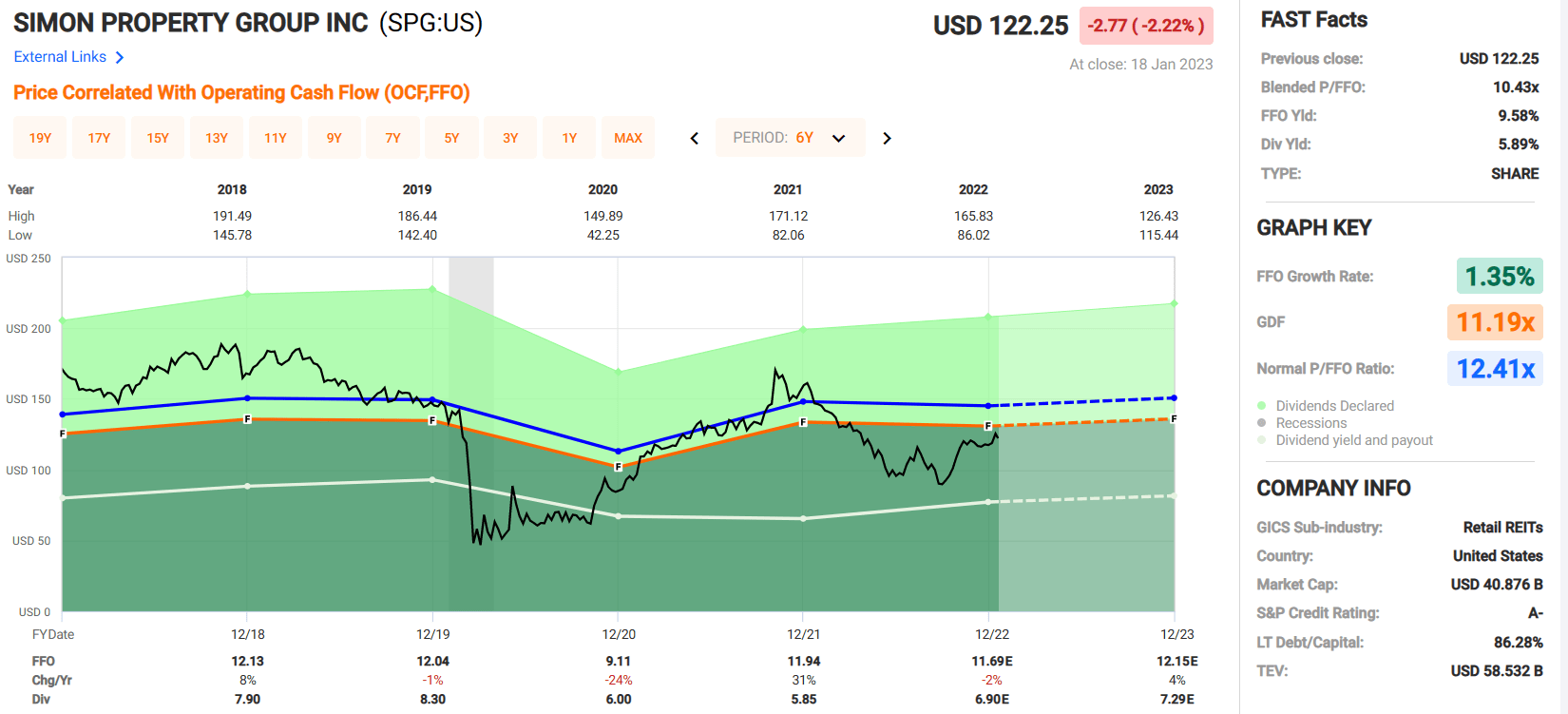

Currently, SPG pays a 5.89% dividend yield that is well covered with an AFFO payout ratio of only 63.01%. The low payout ratio secures the dividend and allows Simon to retain a large portion of earnings for reinvestment.

Simon currently trades at a blended P/FFO of 10.43x, which is under their normal P/FFO of 12.41x. At iREIT we rate Simon Property Group a BUY.

{kind=link}

Mid-America Apartment Communities, Inc. ( MAA ): S&P Credit Rating: A-

Mid-America Apartment is a real estate investment trust that builds, acquires, manages, and leases multifamily residential properties.

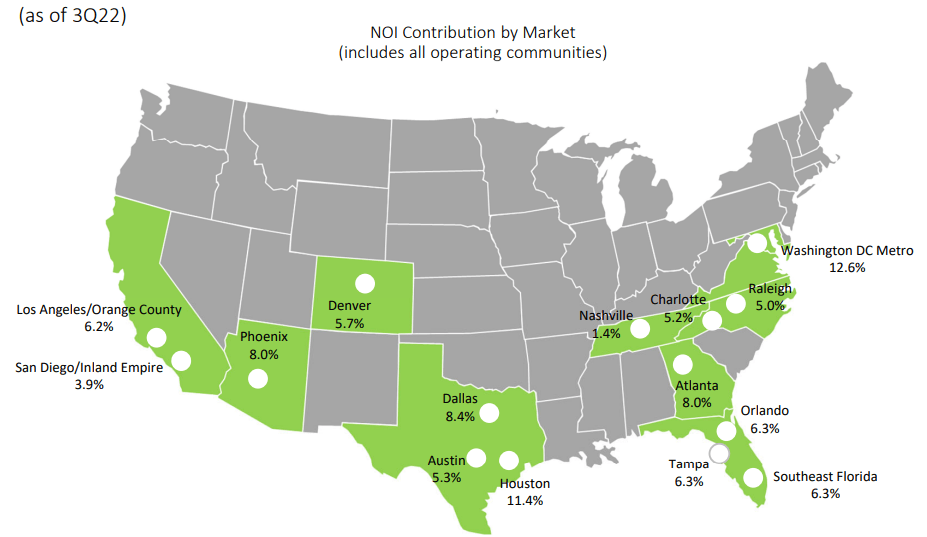

MAA was founded in 1977, went public in 1994, and currently has approximately 102,000 apartment units primarily located in the southeast, the southwest, and the mid-Atlantic. MAA has particularly strong focus on the sunbelt, with their top 10 markets all located in the sunbelt region.

MAA Investor Presentation

Mid-America Apartment had a good year in 2022 with forecasted effective rent growth of 14.5% and an average occupancy rate of 95.8%. Analysts estimate Funds from Operations to come in at $8.41 per share in 2022, up approximately 17% from the prior year.

MAA Investor Presentation

MAA has excellent debt metrics with a Total Debt to Adj Total Assets of 29.1%, a Net Debt to Adj EBITDAre of 3.97x, and a Fixed Charge Coverage of 6.1x. Their weighted average interest rate is 3.4% and their weighted average term to maturity is 8 years.

Additionally, 97.2% of their debt is held at a fixed rate and they have near full capacity available on their $1.25 billion credit facility and $625 million available on their commercial paper program.

MAA Investor Presentation MAA Investor Presentation

{kind=link}

{kind=link}

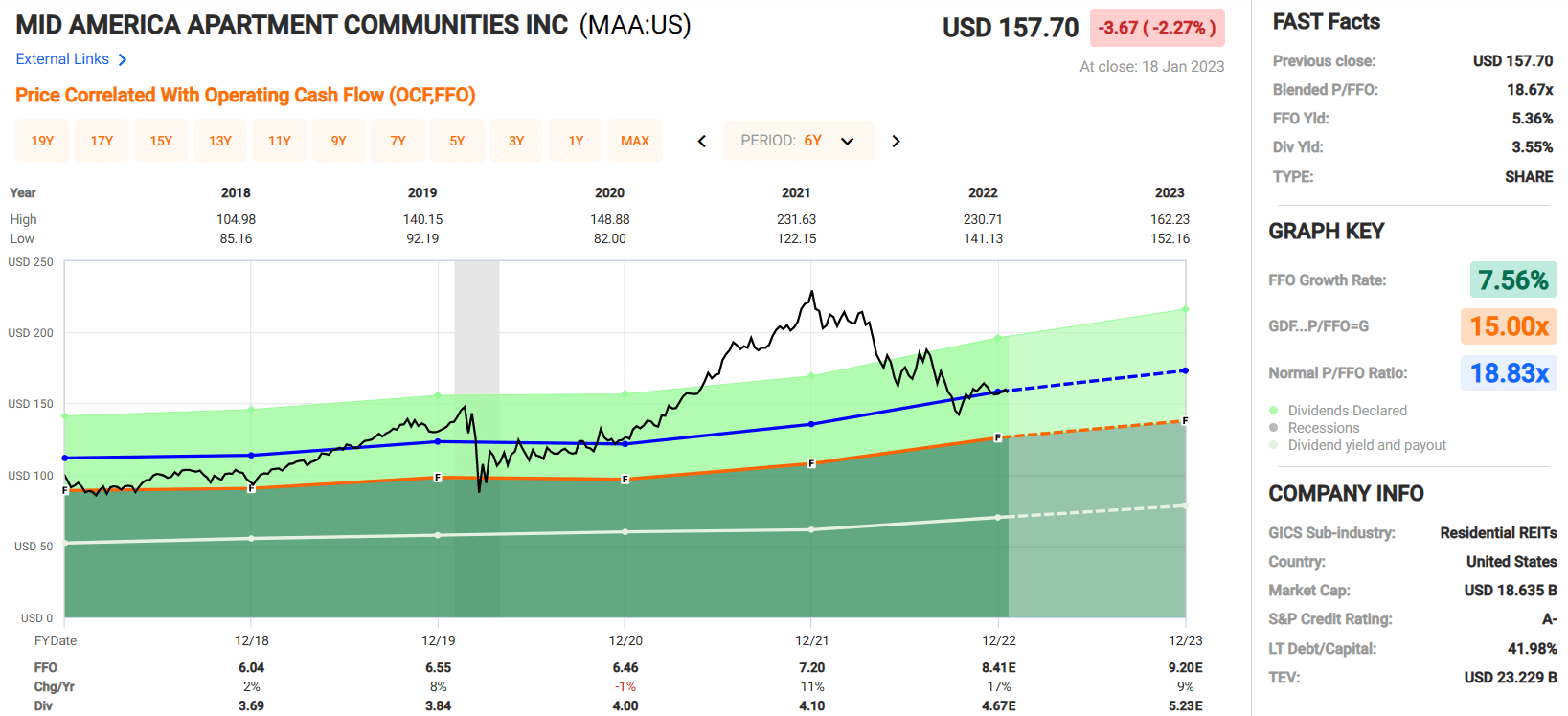

MAA has averaged an FFO growth rate of 7.56% over the last several years and are projected to grow FFO at a rate of 9% in 2023.

They currently pay a dividend yield of 3.55%, which is secure with an AFFO payout ratio of only 61.51%. MAA trades at a blended P/FFO of 18.67x, which is in line with their normal FFO multiple. At iREIT, we rate Mid-America Apartment a BUY.

{kind=link}

Camden Property Trust ( CPT ): S&P Credit Rating: A-

Camden Property is a real estate investment trust that is primarily engaged in the ownership, management, and development of multifamily apartment communities.

As of December 31, 2022, Camden Property owned and operated 171 properties consisting of 58,433 apartment homes across the U.S. Camden is geographically diversified with a particular focus on the sunbelt region with a large portion of their Net Operating Income ((NOI)) coming from Texas and Florida.

{kind=link}

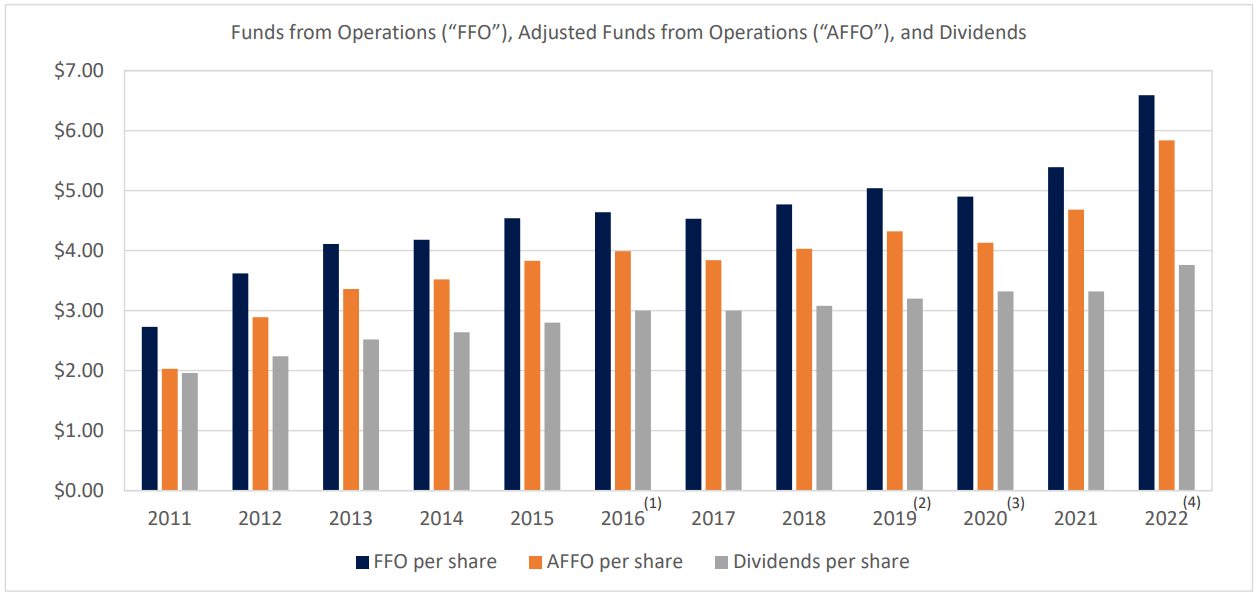

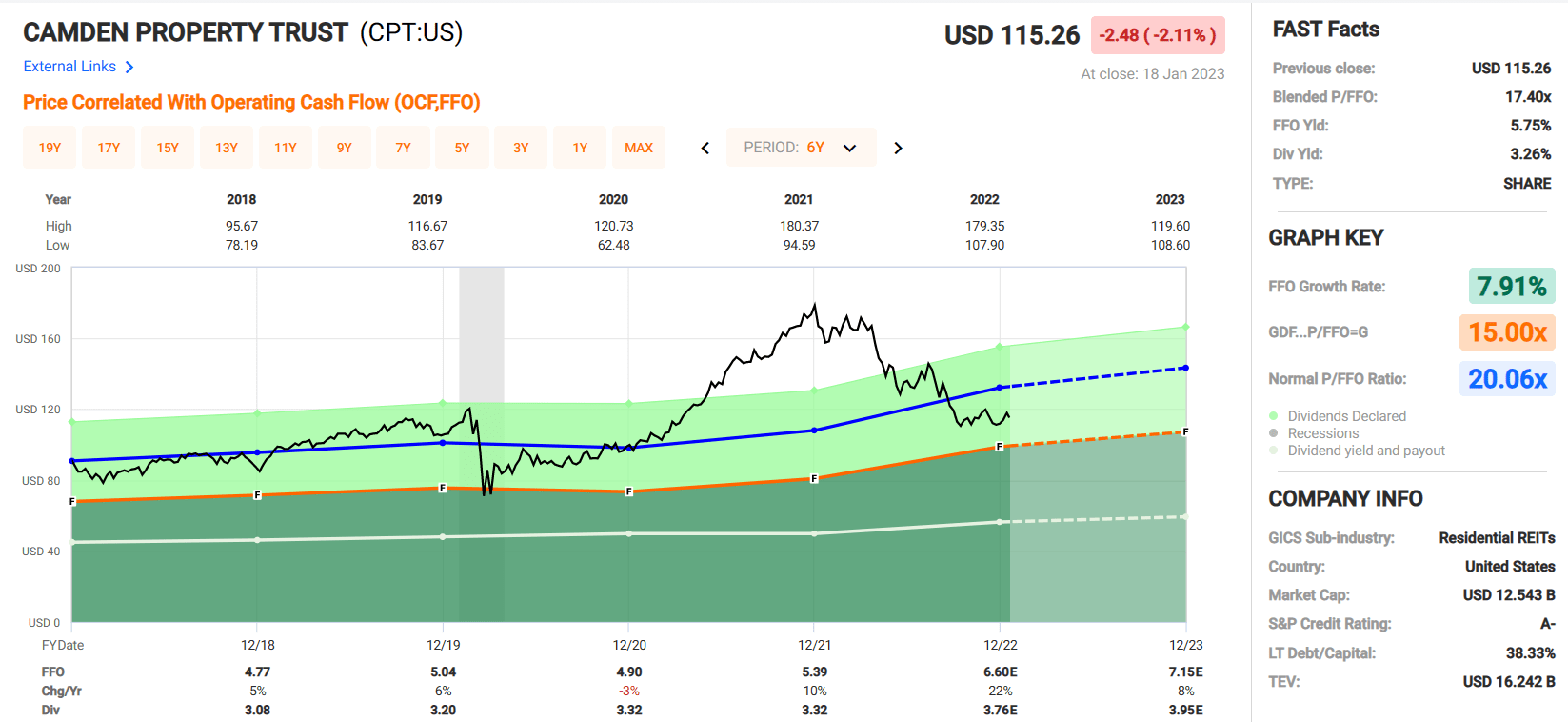

Camden has mostly shown consistent growth in Funds from Operations over the last decade, with FFO growth accelerating over the last several years. Analysts project FFO to come in at $6.60 per share in 2022, up from $5.39 in 2021 for a 22% year-over-year increase. Since 2018, Camden has averaged an FFO growth rate of 7.91%.

{kind=link}

Camden has a very strong balance sheet with $1.5 billion available under their credit facility, a Net Debt to Annualized Adj EBITDA of 4.2x, and a Fixed Charge Coverage ratio of 5.7x.

Additionally, 93.9% of their debt is fixed rate and 86% is unsecured. They have a weighted average interest rate of 3.7% and their weighted average term to maturity is 6.4 years.

{kind=link}

Camden currently pays a 3.26% dividend yield that is well covered by an Adjusted Funds from Operations ratio of just 64.49%. CPT currently trades at a blended P/FFO multiple of 17.40x which is a discount to their normal P/FFO of 20.06x. At iREIT, we rate Camden Property Trust a BUY.

{kind=link}

Equity Residential ( EQR ): S&P Credit Rating: A-

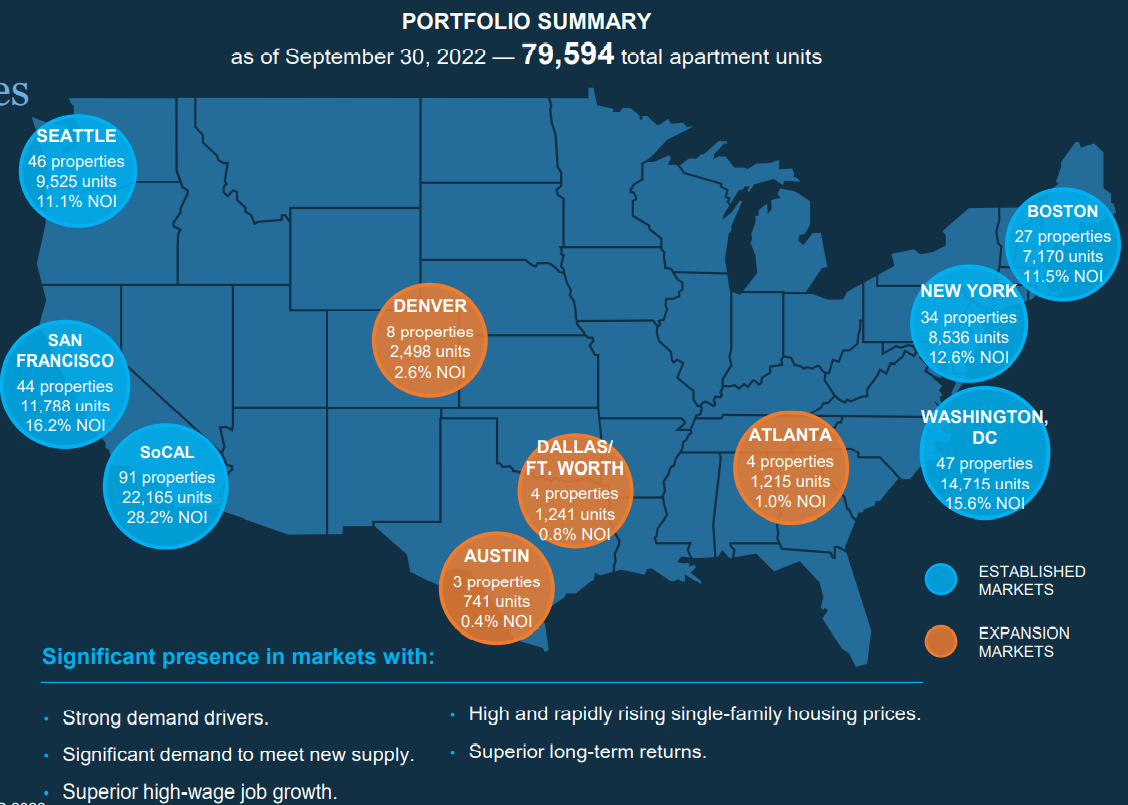

Equity Residential is one of the largest owner and operators of Class-A multifamily properties in the U.S. Currently, EQR has portfolio of 308 properties with 79,594 apartment units.

The REITs properties are concentrated in large coastal markets including Boston, New York, Washington, D.C., Seattle, San Francisco, and Southern California. More recently they have been expanding into Denver, Atlanta, Dallas, and Austin.

{kind=link}

Since their IPO in 1993, Equity Residential has delivered an 11.2% annual total shareholder return while growing the dividend at a 6.4% compound annual growth rate since 2011.

Funds from Operations in for 2022 are expected to come in at $3.53 per share, up from $2.99 in 2021, for an 18% year-over-year increase. Since 2018, EQR has had a blended FFO growth rate of 3.23% with an expected FFO growth rate of 7% in 2023.

EQR Investor Presentation

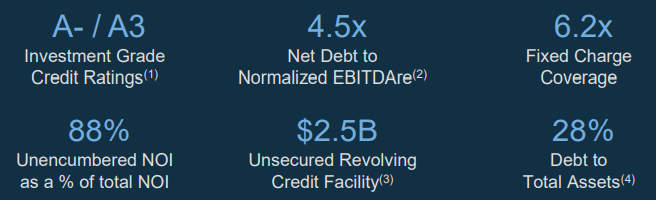

Equity Residential has excellent credit metrics, with a Net Debt to Normalized EBITDAre of 4.5x, a Debt to Total Assets of 28%, and a 6.2x Fixed Charge Coverage ratio. As of September 30, 2022, EQR had $2.3 billion in liquidity, with most of their $2.5 billion revolving credit facility available to them.

EQR Investor Presentation EQR Form 10-Q

{kind=link}

Equity Residential currently pays a dividend yield of 4.12% that is well covered by an AFFO payout ratio of 81.50%. EQR trades at a blended P/FFO of 17.14x which is a discount to their normal P/FFO ratio of 20.51x. At iREIT we rate Equity Residential a STRONG BUY.

{kind=link}

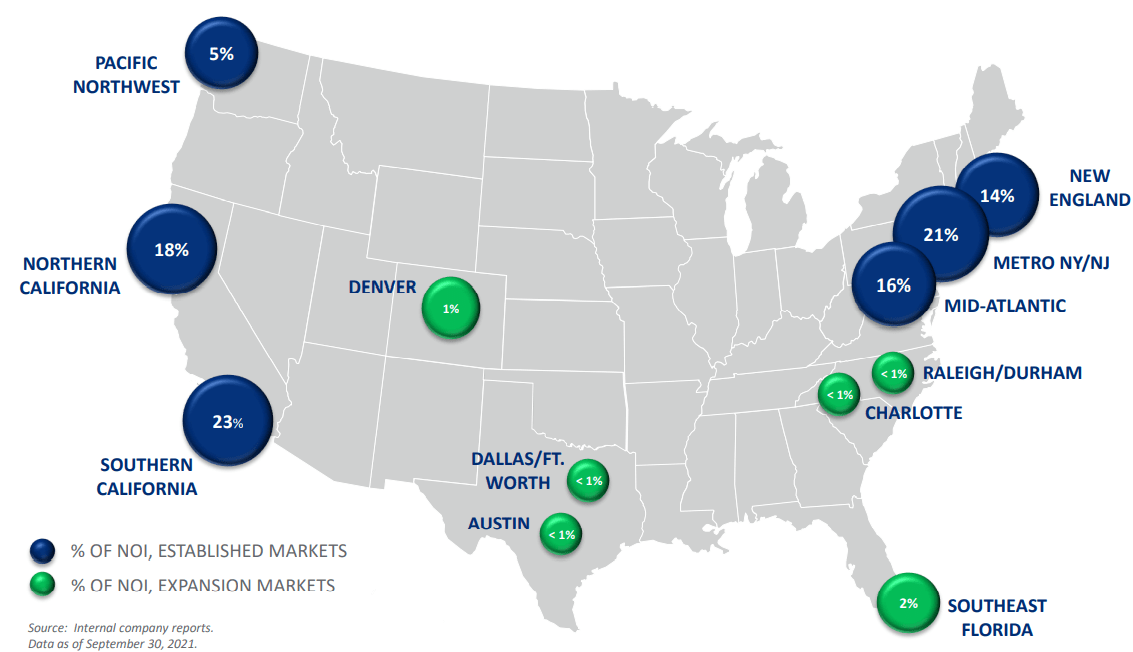

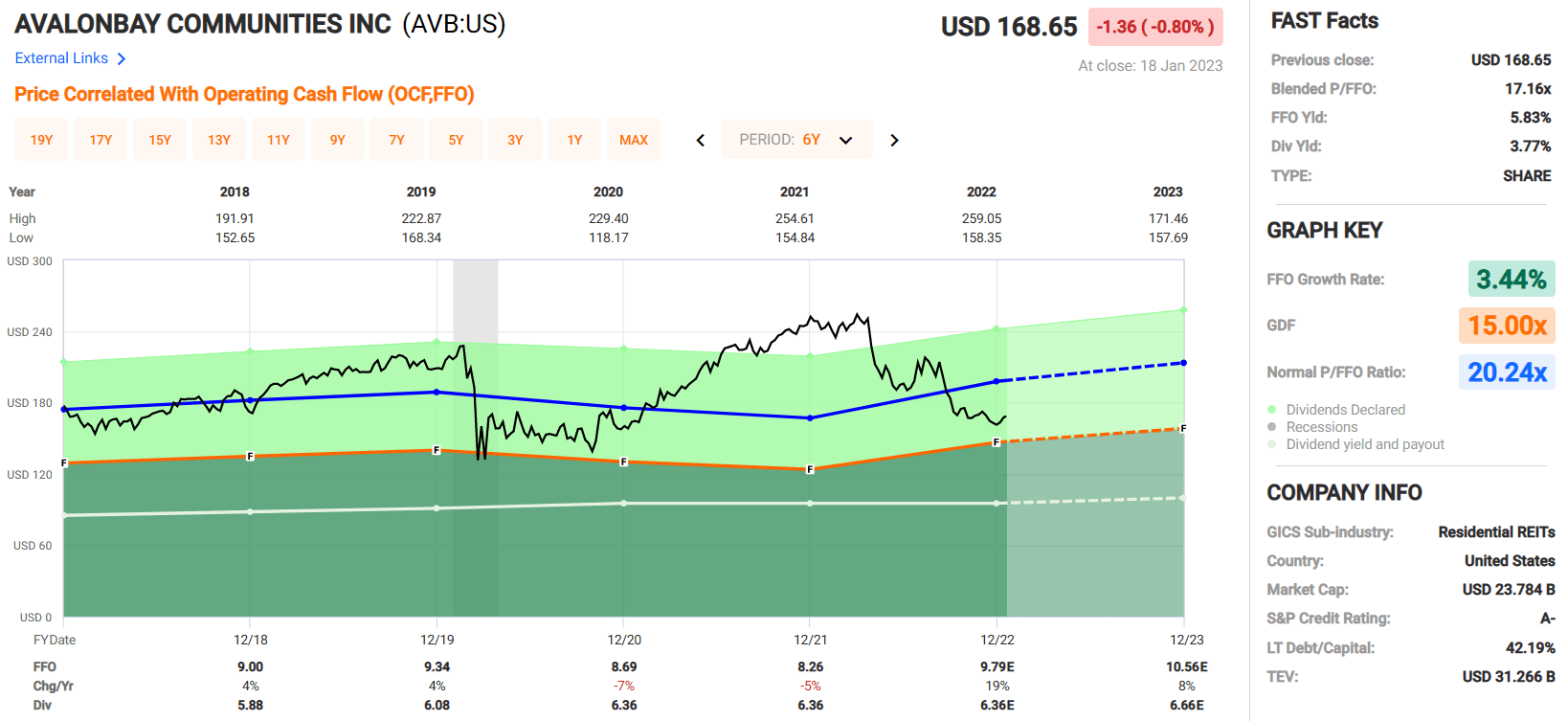

AvalonBay Communities, Inc. ( AVB ): S&P Credit Rating: A-

AvalonBay is a real estate investment trust that owns, manages, and develops multifamily communities mainly in New England, New York and New Jersey, the Mid-Atlantic, and California.

AVB focuses on regions that have employment growth in high wage sectors and areas with lower housing affordability. As of 3Q22, Avalon owned or had an ownership interest in 293 multifamily communities containing 88,405 apartment homes in 12 states.

{kind=link}

For 2022, analyst project AvalonBay's Funds from Operations to come in at $9.79 per share, which is up from $8.26 a share in 2021 for a year-over-year increase of 19%.

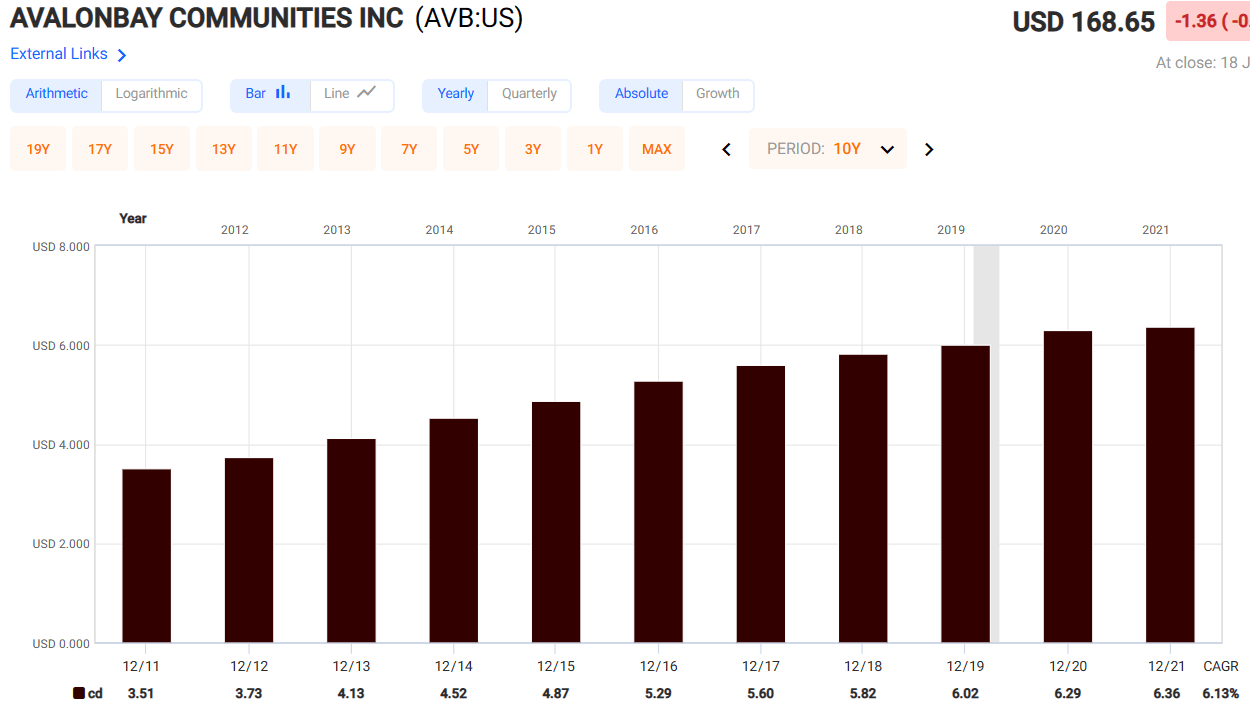

Since 2018, AVB has had a blended FFO growth rate of 3.44% with an expected 8% FFO increase in 2023. Over a 10 year period, AVB has been able to grow FFO at a rate of 6.29% while growing the dividend at a compound annual growth rate of 6.13%

{kind=link}

AvalonBay has solid debt metrics and liquidity. As of 3Q22, AVB had a Net Debt to Core EBITDAre of 4.6x, an Interest Coverage ratio of 6.9x, and a 95% unencumbered NOI. Their weighted average years to maturity stands at 8.1 years and they had $1.9 billion in liquidity as of 9/30/22.

AVB 3Q 2022 Earnings Release AVB Investor Presentation

{kind=link}

{kind=link}

AVB pays a dividend yield of 3.77% that is secure with an AFFO payout ratio of 71.14%. Currently, AVB is trading at a blended P/FFO of 17.16x, which compares favorably to its normal P/FFO multiple of 20.24x. At iREIT, we rate AvalonBay a STRONG BUY.

{kind=link}

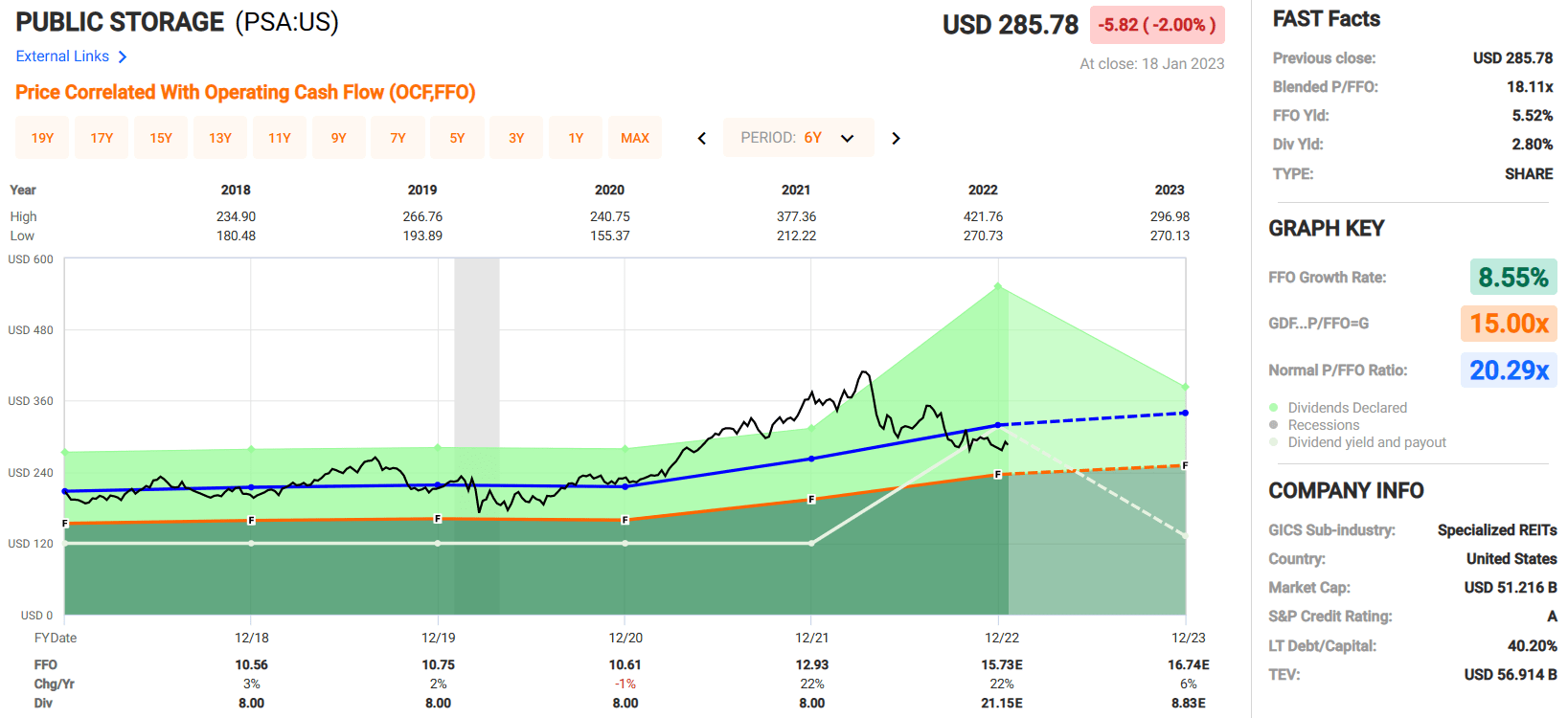

Public Storage ( PSA ): S&P Credit Rating: A

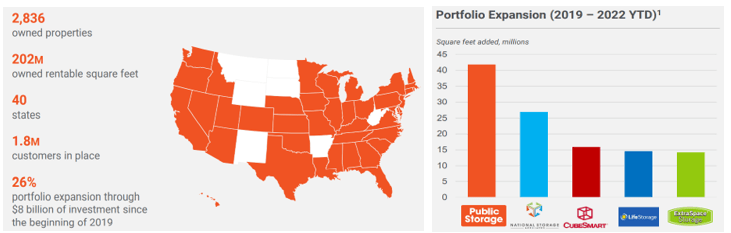

Public Storage is a real estate investment trust and is the largest owner, operator and developer of self-storage properties.

They serve almost 2 million customers with approximately 2,836 facilities located in 40 states across the U.S. Since 2019, PSA has invested $8.0 billion to expand its portfolio and currently owns 202 million rentable square feet of self-storage properties.

{kind=link}

The $8.0 billion in investments since 2019 has added 42 million square feet to the portfolio, expanding the portfolio size by 26%. Since 2019 PSA has pursued growth through investment much more aggressively than it direct peers, more than doubling the square feet added when compared to 3 out of 4 of its peers.

The increased investment since 2019 has started to materialize in accelerated growth in their Funds from Operations over the last 2 years.

PSA went from an FFO growth rate of 2% in 2019 to a growth rate of 22% in the years 2021 and 2022. FFO growth is expected to normalize in 2023 at a rate of 6% which is more in line with their long term average of around 8%.

{kind=link}

PSA's debt metrics are excellent, with a Debt to EBITDA of 2.2x, a Net Debt plus Preferred Equity to EBITDA of 3.3x, and a Fixed Charge Coverage ratio of 9.3x as of 3Q22.

PSA 3Q 2022 Financial Statement

{kind=link}

Since 2018 PSA has had a blended FFO growth rate of 8.55%, in line with their longer term average, and currently pays a dividend yield of 2.80%.

The AFFO payout ratio for 2022 is 155.63%, which would normally be a red flag, but this is only because PSA announced a one-time special dividend in 2022 of $13.15 per share.

Since 2011, their AFFO payout ratio's typical range is somewhere between 70-80%. Currently PSA trades at a blended P/FFO of 18.11x, which is a discount to their normal P/FFO of 20.29x. At iREIT, we rate Public Storage a BUY.

{kind=link}

I Pity The Fool That Doesn't Own These A-Rated REITs

Did you know that some of my followers call me Mr. T?

That shouldn't be a surprise since my last name is Thomas, right?

Well, from my lips to your ears,

"I pity the fool that don't own these A-rated REITs."

iREIT on Alpha

Stay tuned for my upcoming book, REITs For Dummies!

For further details see:

I Pity The Fool That Doesn't Own These A-Rated REITs