MORT - I Sold My Mortgage REITs

2023-10-02 08:05:00 ET

Summary

- I am bullish on REITs. But not all REITs.

- Mortgage REITs are a good example of that.

- I present 5 reasons why I tend to avoid mortgage REITs.

It has now been over 10 years since I made my first real estate investment trust ("REIT") investment.

It was actually a mortgage REIT ("mREIT") and its name was CYS Investments.

What attracted me to this REIT back then was its >10% dividend yield , which seemed to be sustainable.

Its lending strategy also seemed to be relatively safe and it had compelling growth prospects.

But like many other mortgage REITs ( MORT ), it still ended up turning into a value trap and my overall returns were rather disappointing compared to what I could have earned by owning some lower-yielding equity REITs ( VNQ ).

This sad story is a good representation of my typical experience investing in mortgage REIT.

The high yields offered by the sector have at times caught my interest but more often than not, I have later regretted being so greedy for income.

These days, I rarely ever buy mortgage REITs, and in today’s article, I am going to give you 5 reasons why.

Reason #1: Horrific Track Record

It turns out that it wasn’t just me who was investing in the wrong mREITs.

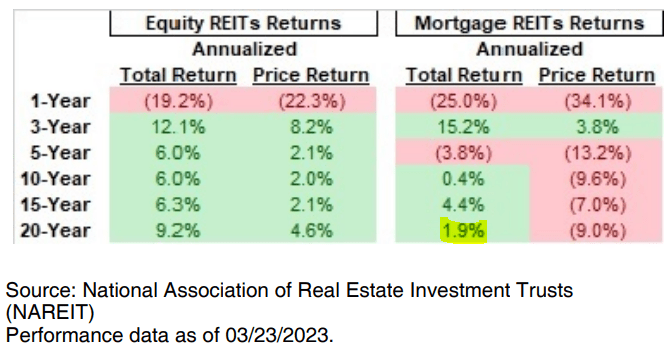

The whole sector has a very poor track record, earning just 2% average annual total returns over the past 20 years.

That’s 4x less than the returns of equity REITs:

{kind=link}

Investors earned high dividends, but this came at the cost of eroding share prices.

Why is that?

This brings us to the next reason.

Reason #2: Broken Business Model

The main issue with mortgage REITs is that they are too dependent on unpredictable macro factors such as the level of interest rates, their direction, and spreads.

They make leveraged bets that earn good returns for a while, but as the macro environment changes, they then suffer large losses.

This is exemplified by the historic dividend payments of mortgage REIT Annaly Capital Management ( NLY ):

Annaly Capital Management

They have consistently failed to predict the major macro turns and they have paid the price.

This makes their business unattractive to me. Some would go as far as to argue that their business is broken.

They are at the mercy of unpredictable factors that are out of their control and making matters worse is the high leverage of the sector.

Reason #3: Too Much Leverage

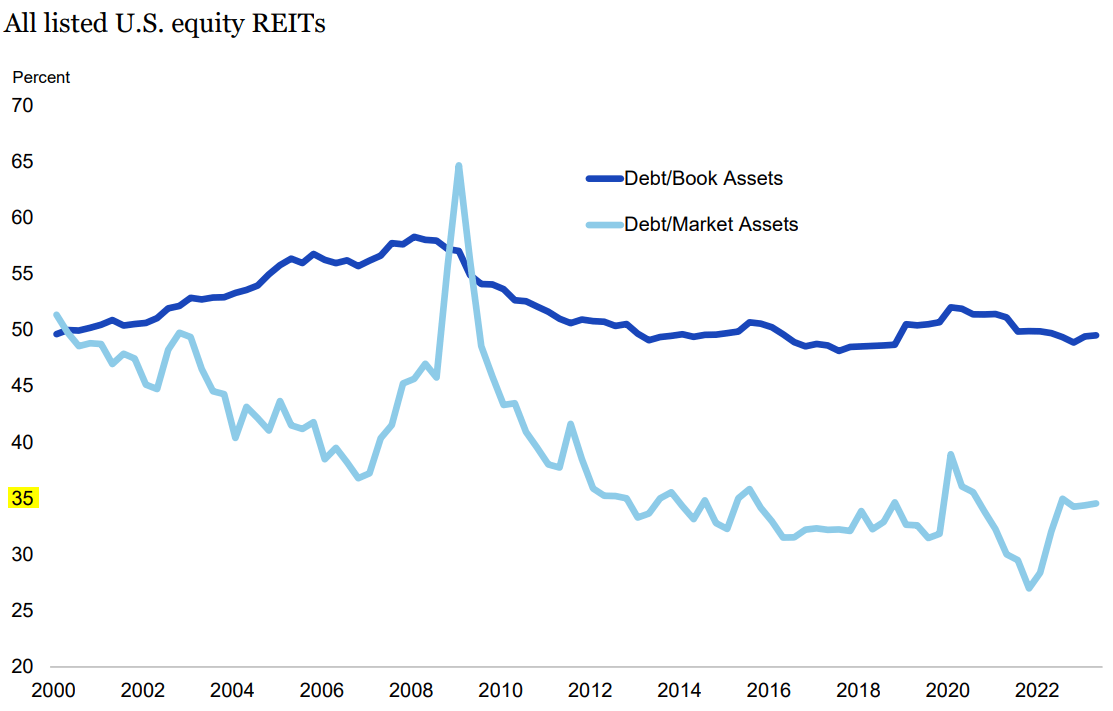

Today, most equity REITs use relatively little leverage.

Their balance sheets are the strongest they have ever been and it significantly reduces their risks in today’s rising interest rate environment:

{kind=link}

Mortgage REITs, on the other hand, use far more leverage, resulting in boom and bust cycles, and that makes them even less attractive to me.

Reason #4: Significant Conflicts of Interest

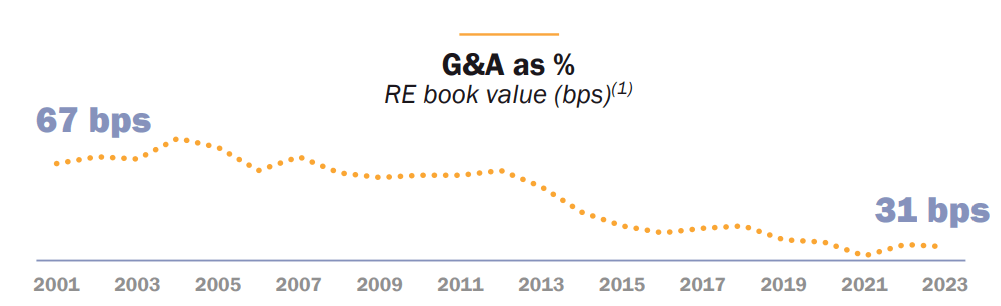

Today, most equity REITs are internally managed. This means that the management is hired as employees of the REIT and they then earn salaries that are tied to some key performance indicators.

This is the preferred management structure because it does a good job of aligning the interests of the manager and the shareholders. It also results in significant cost efficiencies as the REIT grows larger over time.

Realty Income ( O ) is a good example of that:

{kind=link}

But a lot of mortgage REITs are today still externally managed. This means that the management is outsourced to an outside management company that then takes care of everything in exchange for fees. Good examples include Blackstone Mortgage Trust ( BXMT ) and Starwood Property Trust ( STWD ).

This results in much greater conflicts of interest because the manager will typically be incentivized to grow the REIT as much as possible to generate more fees. Moreover, the manager will often also manage other vehicles, distracting their attention and resulting in further conflicts of interest.

If you can’t trust the management of a REIT, then you are better off staying away. This is unfortunately often the case with mortgage REITs.

Reason #5: Poor Overall Risk-to-Reward

So all in all, mortgage REITs offer high dividend yields, BUT:

- They are very dependent on unpredictable macro factors that are out of their control.

- They use too much leverage, leading to boom and bust cycles.

- Their management is often conflicted and expensive.

This explains why most of them have done so poorly over the long run, and since their business models haven’t changed, it is hard for me to be optimistic about their future.

Sure, today’s valuations are low and their dividend yields are high, but I would much rather buy equity REITs in most cases.

They are today also undervalued and their risk-to-reward is far better in my opinion.

For further details see:

I Sold My Mortgage REITs