WING - I've Shorted Wingstop As A Hedge To My Value Portfolio

2024-01-04 14:29:22 ET

Summary

- My value portfolio may be at risk of a near-term market correction.

- Rather than reducing the portfolio, I have chosen to hedge it with inverse bets on stocks I see as overvalued.

- WING is the first of these hedges.

- I discuss the rationale and portfolio considerations below.

At the beginning of 2023, I started building a value portfolio and have shared some entries here at Seeking Alpha. The portfolio is still under construction, but the recent market rise has me concerned about a possibly significant market pullback; so I feel it prudent to also add some value hedges to partially offset the potential downside of a general market move.

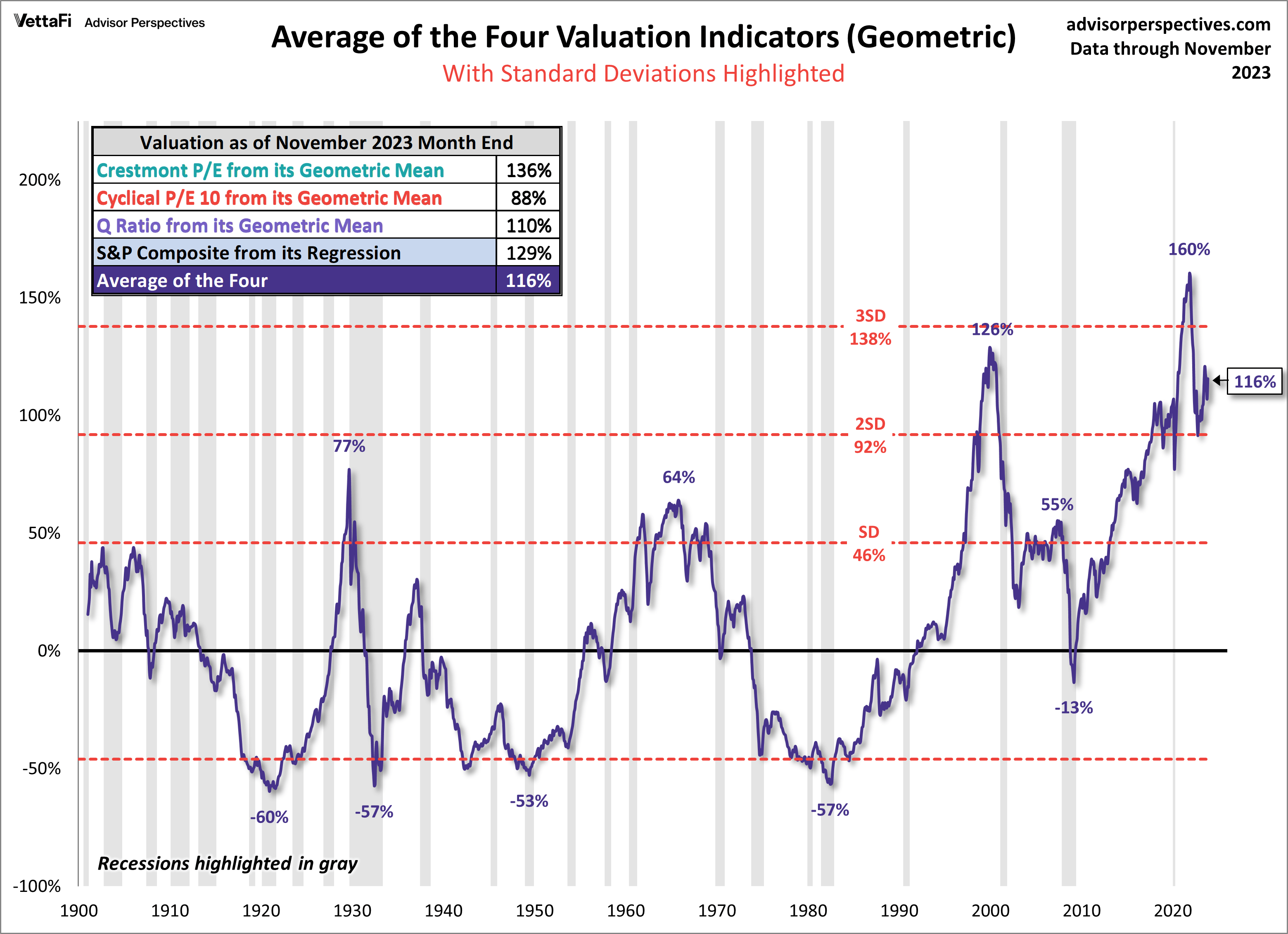

While it is only updated monthly or so, my favorite indicator to appraise market (over)valuation is the composite valuation index compiled by Advisor Perspectives:

{kind=link}

By this measure, we are at valuations only seen twice previously, both of which were followed by substantial downdrafts.

With that as a perspective, let me introduce my first hedge. Wingstop Inc. ( WING ) is an operator and franchisor of chicken wings, tenders, and sandwiches offered at about 2,000 global locations. The stock has had a phenomenal rise in industry-beating operating results.

bigcharts.com

{kind=link}

Growth Story

As can be seen from the above and from the most recent quarterly earnings , WING is a growth story, but as I discuss below, I think it's gotten way ahead of itself.

Key operating metrics for the fiscal third quarter 2023 compared to the fiscal third quarter 2022:

Thirteen Weeks Ended

Sep 30, 2023

Sep 24, 2022

Number of system-wide restaurants open at end of period

2,099

1,898

Number of domestic franchise restaurants open at end of period

1,791

1,631

Number of international franchise restaurants open at end of period

262

225

System-wide sales (in millions)

$ 885

$700

Domestic AUV (in thousands)

$ 1,755

$1,591

Domestic same-store sales growth

15.3 %

6.9 %

Company-owned domestic same-store sales growth

6.0 %

4.3 %

Net income (in thousands)

$ 19,511

$13,368

Adjusted net income (in thousands)

$ 20,499

$13,368

Adjusted EBITDA (in thousands)

$ 38,483

$28,155

The incredible -- historical and ongoing -- growth was highlighted on the most recent earnings call , including this introduction (my emphasis):

Our AUVs now average $1.8 million and we are on track for our 20th consecutive year of same-store sales growth. Wingstop continues to see double-digit transaction growth , a true sign of the underlying health and momentum of our brand. In fact, we exited the quarter with more momentum than when we started .

This growth we are seeing is consistent across all vintages of restaurants and our new restaurants are opening even stronger. We are achieving record levels of new guest acquisition across all channels. Our core guests continue to engage with us and we are seeing an increase in our average frequency.

[...]

This momentum has clearly continued into 2023. Throughout this year we have explained how these sales growth strategies that we are executing against our multiyear drivers, giving us confidence to increase AUVs well north of $2 million. We believe this was showcased in the third quarter as we lapped the launch of both Uber Eats and our Chicken Sandwich delivering 15.3% same-store sales growth. That was almost driven entirely by transactions .

There is no doubt that WING has executed impeccably and that it is still a growth story. Instead, the real question is, how much is that past and potential future growth worth? To me, the answer is best provided by looking at valuation metrics.

Valuation

As I often do, I begin my examination of valuation metrics by pulling up Seeking Alpha's valuation summary page .

{kind=link}

On almost every metric, WING trades at multiples of the sector median: 5X on forward P/E, 4X on forward EV/EBIT, 13X on forward P/S, etc. It has a negative book value per share vs. a P/B of 2X for its peers. Perhaps more telling about the meteoric stock price surge is that, despite being a substantially bigger company now, the current valuation metrics are higher than the 5-year average (e.g., 12% higher forward P/E, 19% higher on forward EV/EBIT, 23% higher on forward price sales, etc.). Now some might argue that the company's execution has de-risked the stock, and hence it trades at higher valuations, I could buy this argument if the stock were trading at slight premia to its peers, but when it trades at an order of magnitude greater multiples on some measures, I lean toward the argument that euphoria has resulted in extreme overvaluation.

To further illustrate this point, here's a chart showing the historical trend of a typical valuation metric.

Cash on Hand

As shown in its latest 10-Q filing, WING has plenty of cash on its balance sheet and should not be at risk for raising money. On the contrary, the company pays a small dividend and has a stock buyback program in place.

{kind=link}

On the other hand, the balance sheet also shows that total liabilities are substantially greater than total assets (hence the negative book value mentioned earlier). I personally don't think this matters much in the short term, but if we have a significant recession, WING may be at some risk, and it certainly won't be in a position to continue with its aggressive growth strategy.

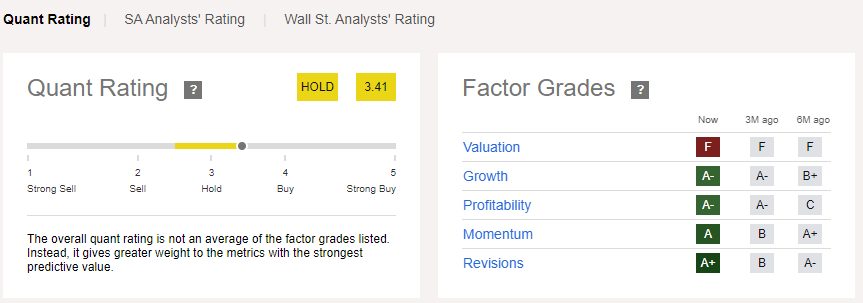

Quant Ratings

Seeking Alpha's quant ratings perfectly align with my take, which is that the company has executed very well and has seen a surge in its stock price which has led to "A" ratings in growth, profitability, momentum, and revisions; but the current valuation is so egregiously high that its rating is "F".

{kind=link}

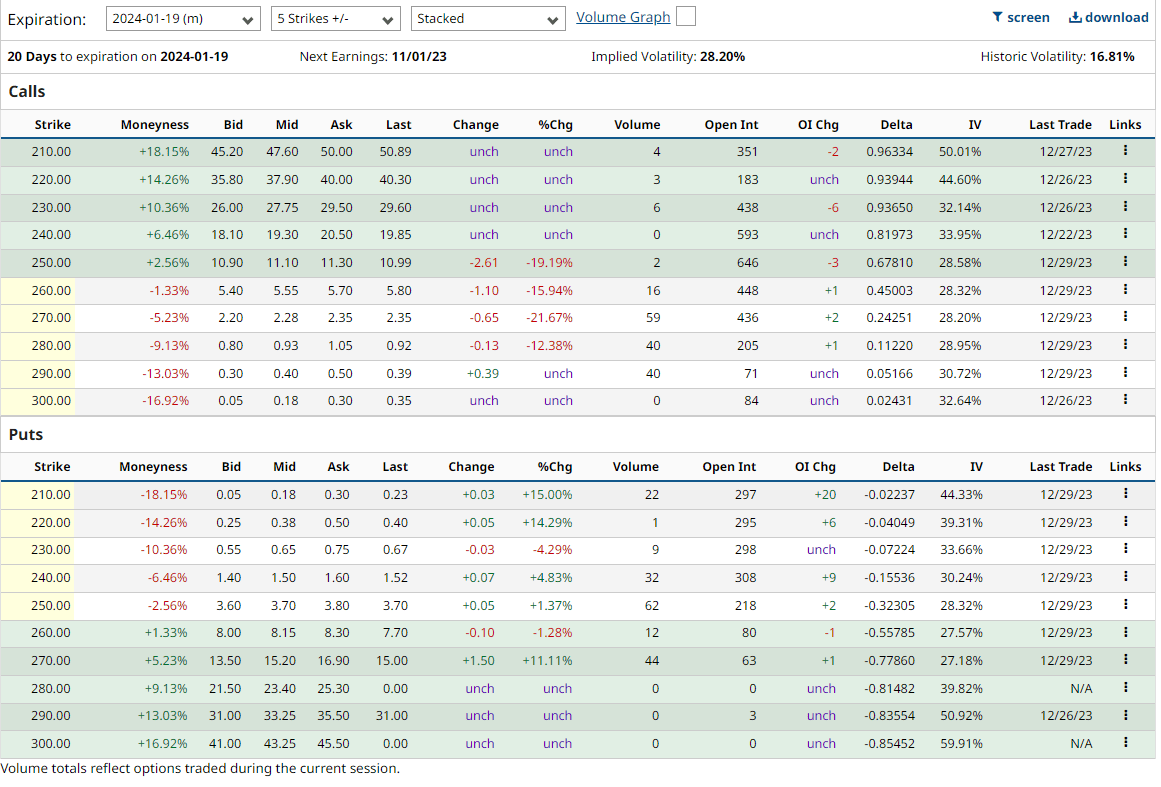

Options

WING trades liquid options with an implied volatility of about 30%. Thus, it is viable to use options strategies in putting on positions (though I personally haven't done so). Here are near the money strikes for Jan. 19, 2024:

{kind=link}

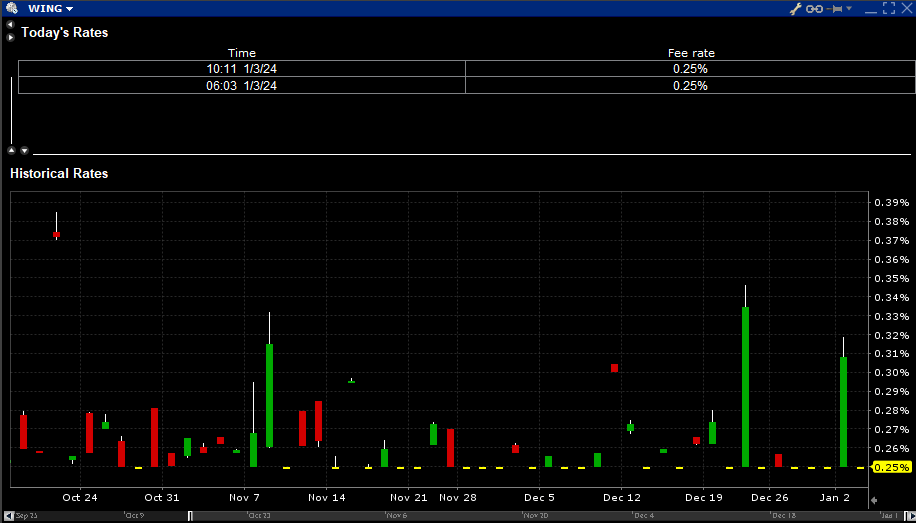

Cost to Borrow

WING has been a very easy borrow and currently has a borrowing cost of only 0.25% per year, so, unlike many shorts, there's little cost associated with shorting it.

{kind=link}

Hedge vs. Short or Portfolio Considerations

To emphasize, in this article, I'm not recommending an outright short of WING, but rather I'm short WING as a hedge against my value portfolio. I believe that over time value multiples revert to the mean and thus being long stocks with low valuation multiples will generate alpha.

However, since the overall market is currently near all-time valuation highs, I worry about the risk of an imminent major correction and its effect on the portfolio. To mitigate this risk, I could either reduce my long exposure (perhaps selling 25% of each of my value positions), or I could hedge the risk by shorting some high valuation stocks. Given the long-term bullish bias of stocks, and my confidence that over the long term, stocks revert to median valuation levels, I'm choosing to hedge my portfolio beginning with a short of WING.

Moreover, market "darlings" tend to fall faster than the general market at times of correction, so that's even more reason to prefer a short hedge to reducing overall exposure.

I'm still building both the long and short sides of this portfolio, but eventually, I'd like to have thirty 3% positions on the long side and about ten 6% positions on the short side. Ideally, the long side would remain about 90% invested with 10% cash, while the short side would be dynamically sized depending on the market's overall valuation (the 60% short position would likely be the largest, and it would tend to 0% as the market became fairly valued, and certainly when the market became undervalued).

Given the low cost to borrow and the dynamic nature of the short book in my portfolio, I've chosen to be short rather than buying puts on WING, but since the implied volatilities are quite low on WING, others might find that hedging via puts is the safer way to proceed.

Risks

Being short WING has the very real risk of the company continuing to execute and maintain its multiples. Remember, for example, that Domino's Pizza, Inc. ( DPZ ) was one of the best-performing stocks ever. This is why my position is small and is offset by a much larger long book. Moreover, as with all the positions in the value portfolio, I will review the situation and valuation metrics every few months and re-evaluate the position and its size.

For further details see:

I've Shorted Wingstop As A Hedge To My Value Portfolio