PBI - I Was Wrong About Pitney Bowes: Time To Sell Global Ecommerce!

2023-08-17 15:25:00 ET

Summary

- The best scenario for investors is for Pitney Bowes to sell the Global Ecommerce segment.

- A sale of the Global Ecommerce segment would result in the remaining company earning over $1.50 per share and growing at over 4% annually.

- At a 10x PE ratio the remaining company would be valued at over $15 per share.

- While the journey is uncertain depending upon the multiple paths, each path leads to the same eventual outcome.

- Steve Brill has the ability to positively change the future for Pitney Bowes in a shareholder-friendly way just as Bill Simon did for GameStop.

I had high hopes for Pitney Bowes ( PBI ). Under another CEO and management team, shares could have traded between $20 and $40 by now. Unfortunately, it has become apparent that the Global Ecommerce segment is an extremely valuable asset... in the hands of another management team. I believe that the best scenario for investors is for the Pitney Bowes Board of Directors to quickly come to the same conclusion that the segment needs to be sold immediately. Doing so will unlock significant value for Pitney Bowes shareholders, allow the company to significantly lower their cost of capital and interest payments, substantially increase profitability, and allow for investments into easy growth opportunities within the company's other business segments. A sale price of over $1 billion is definitely possible given the existing customer base, and significant investments in automation. There is no question that the capital expenditures that Pitney Bowes has made have materially increased the efficiency of the network over the last year.

This is not the article I wanted to write. I have been bullish on the Global Ecommerce segment and management's ability to turn it around for years. My analysis of the situation based on several years of working in the Pricing department of FedEx Services ( FDX ) was well-founded, but I just never anticipated such an epic failure to execute by the management team. As I noted in a previous article , I should have listened to my gut the moment that Marc Lautenbach started talking about "ingesting" packages into the postal network (quarter after quarter) instead of using the correct term of "injecting." It may seem minimal, but it absolutely foreshadowed what I believe is the complete lack of awareness that management had in regards to how to operate a logistics company.

With no turnaround in sight for the Global Ecommerce business (which actually lost more in 2022 than 2021) and with the company refinancing debt at a mind-blowing SFOR plus 6.9% (a total interest rate of over 12%), investors need the current Board of Directors to quickly come to the same conclusion!

In November, I highlighted how Pitney Bowes was the first activism target for Hestia Capital since their successful ( GME ) campaign. In 2020, Hestia won two board seats in a proxy contest against GameStop management which paved the way for Ryan Cohen to step-in and the rest is history. There is no question that a second activist always has it easier than the first activist... which brings us to the current situation with Pitney Bowes.

A few months ago, Hestia managed to win 4 out of 9 board seats at Pitney Bowes which has set-up a dream scenario for any activist looking to make a huge return in a short amount of time as the only reason that Lautenbach retained a seat was due to the votes of institutional, passive funds.

Ultimately there are three paths forward for the company, but to be clear - all paths lead to the same destination.

Path One: Steve Brill Chooses Loyalty to Shareholders Over Loyalty to Marc Lautenbach

This path is the most shareholder friendly as it involves no legal or proxy costs.

On March 2nd, 2023, Pitney Bowes announced the appointment of Steve Brill as an "independent" director. Brill retired from UPS in 2020 as the President of Corporate Strategy and this is his first board appointment.

This path forward is very straightforward. Brill must clearly see by now that the current management team's decision making is impaired due to how much time and effort they have spent on trying to make the Global Ecommerce segment a success. I understand the current management team's feelings. Nobody defended the decision to retain the Global Ecommerce segment more than I did. We all wanted it to be successful and making the decision to move on in the opposite direction is a very hard human mentality to overcome. This is precisely why investors need the Board of Directors (most of which were not part of the original decisions on Global Ecommerce) to step in and not only conclude that the segment must be sold, but also that it would only be logical to reconsider who would be the best option to lead the new company forward as CEO after the sale.

Brill must vote to put the Global Ecommerce segment up for sale and to begin the search for a new CEO. As someone who spent 33 years in the industry, there should be no one more qualified to come to this conclusion as an "independent" thinker. Failure to do so can only mean one thing: Steve Brill has decided to put his loyalty to Marc (for appointing him as an "independent" director) ahead of his loyalty to the shareholders.

And for what?

If Brill fails to act, paths two and three are a foregone conclusion. These paths will result in a completely new Board of Directors that are willing to put shareholders first. If that happens, it's my opinion that Brill, as a middle-aged white male will find it nearly impossible to serve on the Board of any future company ever again. This may sound harsh or politically incorrect, but I believe it's the cold harsh truth and it would be a mistake for investors not to consider this point. The pool for middle-aged white males is deep, and no company is going to want to appoint a candidate that was removed from his position after just one year on the job. There are just too many other alternatives. Therefore, good odds remain that Steve Brill can lead the change at Pitney Bowes much like Bill Simon did at GameStop in a nearly identical situation that also involved Hestia Capital.

Path Two: A New Activist Emerges

Path two is also straightforward.

In path two, a new activist emerges (similar to how Ryan Cohen emerged after Kurt Wolf / Hestia Capital won several board seats at GameStop). In this path, there are two possible scenarios.

Scenario One

Steve Brill votes with other members of the Board of Directors to appoint new Board members as recommended by whatever activist emerges which may include the removal of Marc Lautenbach as a Director. This would be the most shareholder-friendly outcome.

Furthermore, there is precedent, as this is precisely what happened at GameStop as mentioned earlier. Bill Simon, former CEO of Walmart, had a change of heart, sided with Hestia, and essentially allowed Ryan Cohen to commandeer GameStop.

Scenario Two

The current Board of Directors stand their ground, maintain their loyalty to a failed CEO, and decide to spend shareholders' money, again, in an attempt to save all of their jobs at the expense of shareholders.

Both of these scenarios lead to the same conclusion. In both scenarios, Marc Lautenbach exits the company and the new Board of Directors put the Global Ecommerce segment up for sale and save the company.

It is simply a matter of whether this outcome will be done with millions more of shareholders money spent on another proxy contest ( ~$11M was spent in the first 6 months of 2023 ), or if Brill (or another non-Hestia Director) will step-up and put shareholders first.

Path Three: Hestia Capital Wins Another Board Seat

If no new activist emerges, a shocking outcome in my opinion, then as far as I know there is nothing stopping Hestia Capital from winning additional seats in 2024. Unlike the situation with GameStop there is no cooperation agreement that was ever entered into or reported.

This outcome would be unfortunate, because it would mean that we would most definitely have to wait until 2024's annual shareholder meeting for the change necessary to move the company forward. I would assume that this outcome would also result in shareholder money being spent to fight Hestia from winning additional board seats.

However, the conclusion would be the same. There is little doubt that by 2024 Hestia would have the full support from the proxy companies to force even the passive shareholders like BlackRock and Vanguard to vote for all nine of Hestia's candidates - an outcome that would likely make it extremely difficult for some of the losing Directors to win seats at other companies in the future where they have no leg up in the area of Board diversity.

Sale of Global Ecommerce

Other Seeking Alpha authors were smarter than I as they wrote and came to the conclusion that the Global Ecommerce segment must be sold-off far before I did.

Pitney Bowes purchased Newgistics in 2017 for over $475 million. While Pitney Bowes management have been horrible operators of the Global Ecommerce segment it has not been for lack of investment. Per FactSet, from 2018 through 2022, Pitney Bowes has spent $742.5M on capital expenditures and I believe it's likely that the vast majority of those investments went towards the Global Ecommerce segment.

Therefore, while I lack the details necessary that only the due diligence of an acquiring firm could confirm, it would seem appropriate and conservative to expect at least $1 billion in the sale of the segment.

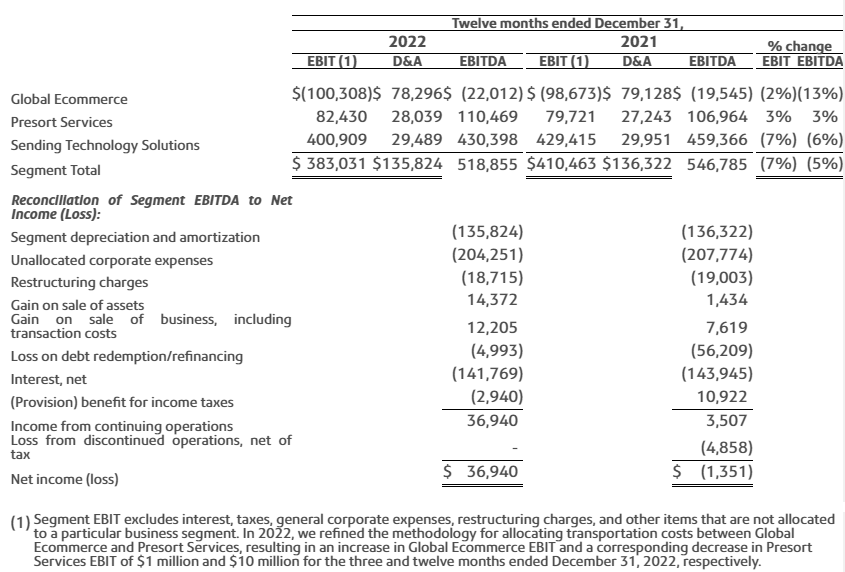

The image below from the 10-K details the profitability of different business segments through 2022. Of note, there are $204,251,000 in unallocated corporate expenses. I have never seen such a thing for a company as large as Pitney Bowes. How much of these unallocated costs are associated with the Global Ecommerce segment? One third? Half? We'll conservatively assume one third or approximately $68M.

Pitney Bowes Financials (Pitney Bowes 10-K)

{kind=link}

Excluding one-time items such as restructuring charges, gains on sales of assets, and losses on refinancing, net income in 2022 would have been $34.071M. Net income would have been $134.379M without the Global Ecommerce segment. Assuming one third of unallocated corporate expenses are related to Global Ecommerce would add an additional $68M to net income increasing the total to ~$202.5M in net income vs current market cap of ~$600M and current enterprise value of ~$2.5B.

A sale of the Global Ecommerce segment for $1B would be equivalent to the company receiving approximately $5.69 in cash per share, based on 175.695M outstanding shares.

How would the profitability of the company change if PBI used 100% of the proceeds to paydown debt?

At the end of 2022, PBI had an average interest rate of 7.5% with $2.2B in outstanding debt. However, only 65% of the debt had a fixed rate; therefore, the company expected to pay $170M to $180M in interest in 2023. Let's be incredibly conservative; however, and say that the $1B in debt paydown will only be at the 2022 average rate of 7.5%. This would result in savings of $75M annually.

We already discussed what net income would have looked like in 2022 without Global Ecommerce. If we now add the $75M in interest savings on top of the $202.5M we get to ~$275M a year. This is completely ignoring three key items. 1) The company would most likely prioritize the higher interest debt, 2) The company would almost certainly be able to refinance their remaining debt at materially lower rates which would further increase profitability, and 3) The lower cost of capital would increase the profitability of the Pitney Bowes bank.

Pitney Bowes would now generate $275M year with total debt of only $1.2B and net debt less than half that figure (as the company has over $500M in cash) before even considering that the Pitney Bowes bank debt is actually an asset.

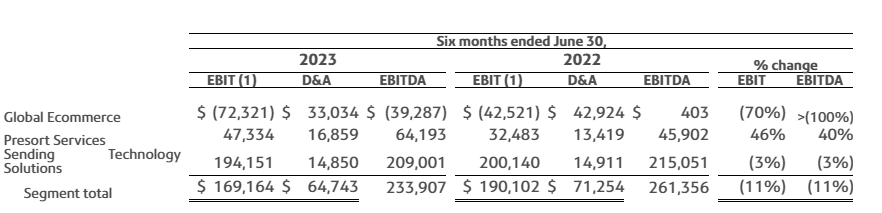

The most interesting development moving forward is that through the first six months of the year, the legacy businesses actually grew!

Pitney Bowes Financials (Pitney Bowes 10-Q)

{kind=link}

As the above graphic shows from the Pitney Bowes 10-Q Q2 earnings, the Presort and Sending Technology Solutions segments grew EBIT from $232.623M in the first 6 months of 2022 to $241.485M. The growth in Presort has been fantastic and there is no telling how much faster these segments, including the bank, could be growing if they were not constrained by the majority of the CapEx going towards Global Ecommerce.

With the sale of Global Ecommerce, Pitney Bowes would instantly transform into an incredibly profitable, growing, company with an extremely strong balance sheet. If desired, the remaining debt could easily be paid-off within 5 to 10 years without sacrificing investments in the remaining segments to increase their growth rates.

Risks

The biggest risk facing Pitney Bowes at this point is no change in strategic direction.

No new activist.

No change in heart from a majority of the current board members.

No change in the constitution of the board even with another proxy battle in 2024.

In my opinion, given how obvious the path forward has become, and since Hestia already controls 4 of 9 board seats, these risks seems extremely unlikely.

As I stated earlier, I have no idea what path is coming, but it will be one of the three and they all lead to the same destination.

Conclusion

No one is better equipped to make the recommendation to sell Global Ecommerce than DOMO Capital. In November of 2022, I wrote:

To be clear - we want nothing more than for PBI to retain the Global Ecommerce business and grow it into an entity that is generating hundreds of millions in EBIT a year. DOMO Capital is not looking for the unit to be sold off , especially after years of mismanagement.

However, If PBI can't generate positive EBIT in Q4, long-term investors need answers. Thankfully, with Hestia Capital involved, we have much greater confidence that the incompetent management of the global ecommerce unit will be resolved. If it cannot be resolved, then we would agree that the sale of the unit would unlock significant shareholder value.

It is clear that after the extremely disappointing fourth quarter as well as the equally disappointing first-half of 2023 that the time has come to sell the segment.

I was wrong.

Kurt Wolf was correct.

Other Seeking Alpha writers were also correct.

A sale of the Global Ecommerce segment should almost immediately re-value PBI over $10 per share as the capital structure would be massively de-levered, earning over $1.57 per share, while the current 3.8% growth rate of the legacy businesses through the first 6 months of 2023 could easily be accelerated with a more appropriate level of re-investment.

A multiple of 10x earnings in this scenario would be extremely conservative and yet would value shares over $15 per share.

While the path forward the company takes is unclear, the eventual destination seems obvious and leads to the same conclusion no matter which path is embarked upon.

The time to act to maximize shareholder value is now!

For further details see:

I Was Wrong About Pitney Bowes: Time To Sell Global Ecommerce!