OXLC - I Wouldn't Touch Oxford Lane Capital With A 10-Foot Pole

2023-10-23 11:06:43 ET

Summary

- Oxford Lane Capital operates as a fund that allocates capital to riskier prospects, primarily collateralized loan obligations (CLOs).

- The company has a high yield of 19.5% but has significantly underperformed the S&P 500 over the past ten years.

- Distributions have exceeded net investment income and realized gains, leading to the need for capital inflows from stock issuances to sustain the payouts.

Although I am not the kind of investor that prioritizes distributions, it is always nice to have the cash flow in if you do own shares of a company that does pay out a distribution. A company that is healthy and growing that elects to pay out some of its cash to shareholders is perfectly fine, and for those who are in retirement or approaching it, I can understand the appeal behind a hefty payout. But not every opportunity that boasts a large distribution should be taken seriously. In fact, the higher the yield, the more cautious investors should be. And this is because you could end up with a situation where the distribution is unsustainable.

Beware Oxford Lane Capital

One opportunity that many seem to like because of its massive payout is Oxford Lane Capital ( OXLC ). This is not a typical company, however. Rather, it operates as a fund that raises money on the open market and allocates that money toward riskier prospects. While this may sound foolish, in theory, it makes sense. By raising capital for cheap and allocating that capital to some riskier prospect, you can capture some sort of spread between the cost of the initial capital and the profits achieved by allocating that capital out. And by appropriately diversifying, you can virtually remove company-specific or investment-specific risk, dealing only with systemic risk.

{kind=link}

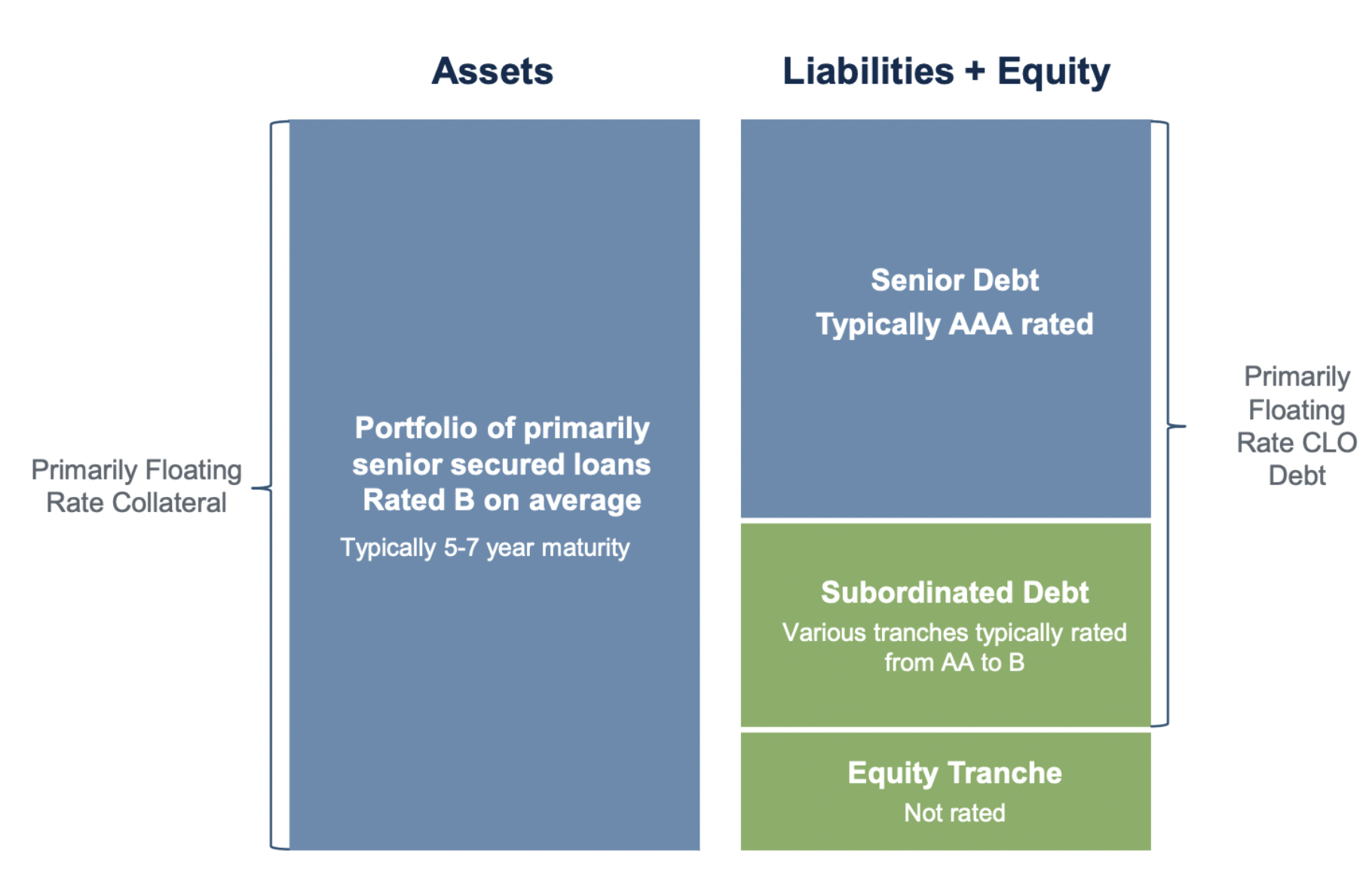

In the case of this particular prospect, management allocates the capital mostly to CLOs, also known as collateralized loan obligations. As I wrote about in a prior article regarding Eagle Point Credit ( ECC ), a CLO is essentially a pool of loans that is then divided up into different categories. Investors have the opportunity to buy into each of these categories. The highest, known as the senior debt category, gets paid back, with interest, before anybody else. Beneath that, you have subordinated debt. And at the very bottom, you have what is known as the equity tranche. This is the riskiest section of a CLO because it is only entitled to a return after everybody else above it has been paid. So if there were some sort of systemic collapse, it's the equity holder that would lose out first, even if some or all of the other parties could be paid.

In order to capture the greatest returns, Oxford Lane Capital focuses largely on the equity and junior debt categories of CLO investments that it makes. As of the end of March of this year, the portfolio that Oxford Lane Capital overseas allocated 95.9% of its assets toward CLO equity, with the remaining 4.1% in the form of CLO debt. So it truly is accepting incredible amounts of risk. Those who own shares have likely been quite happy in some respects. That's because this risky strategy has allowed the enterprise to pay out a significant amount of cash each year. In fact, the yield right now is 19.5%. That easily exceeds almost any other opportunity that's out there. Of course, management handles this risk by ensuring that funds are diversified appropriately.

{kind=link}

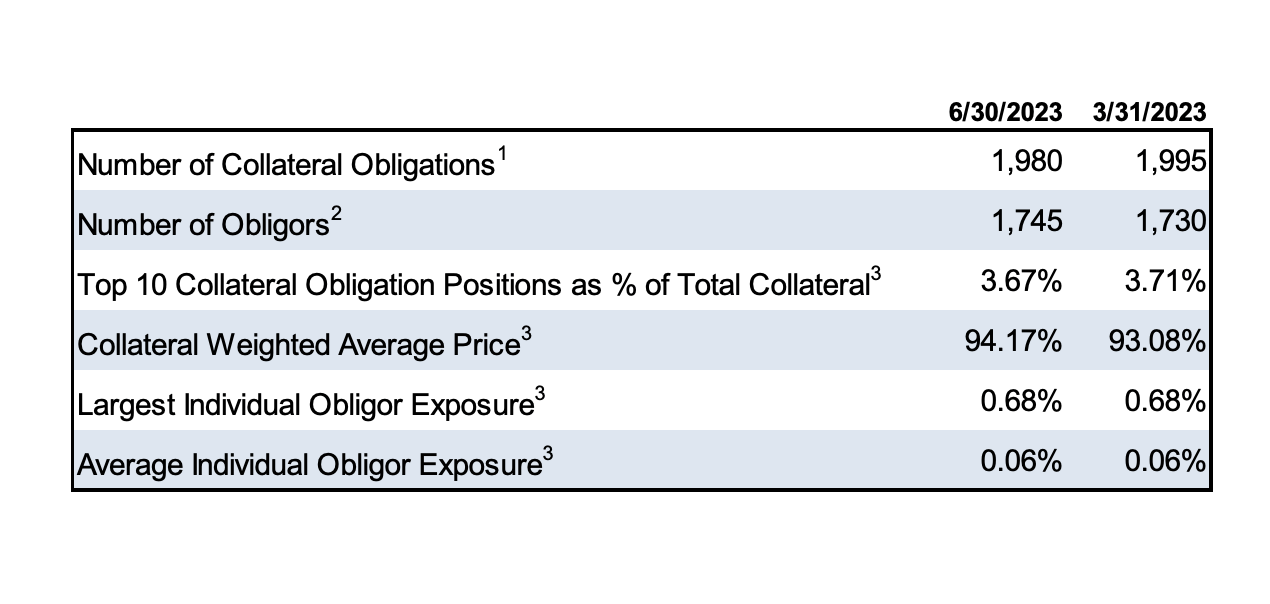

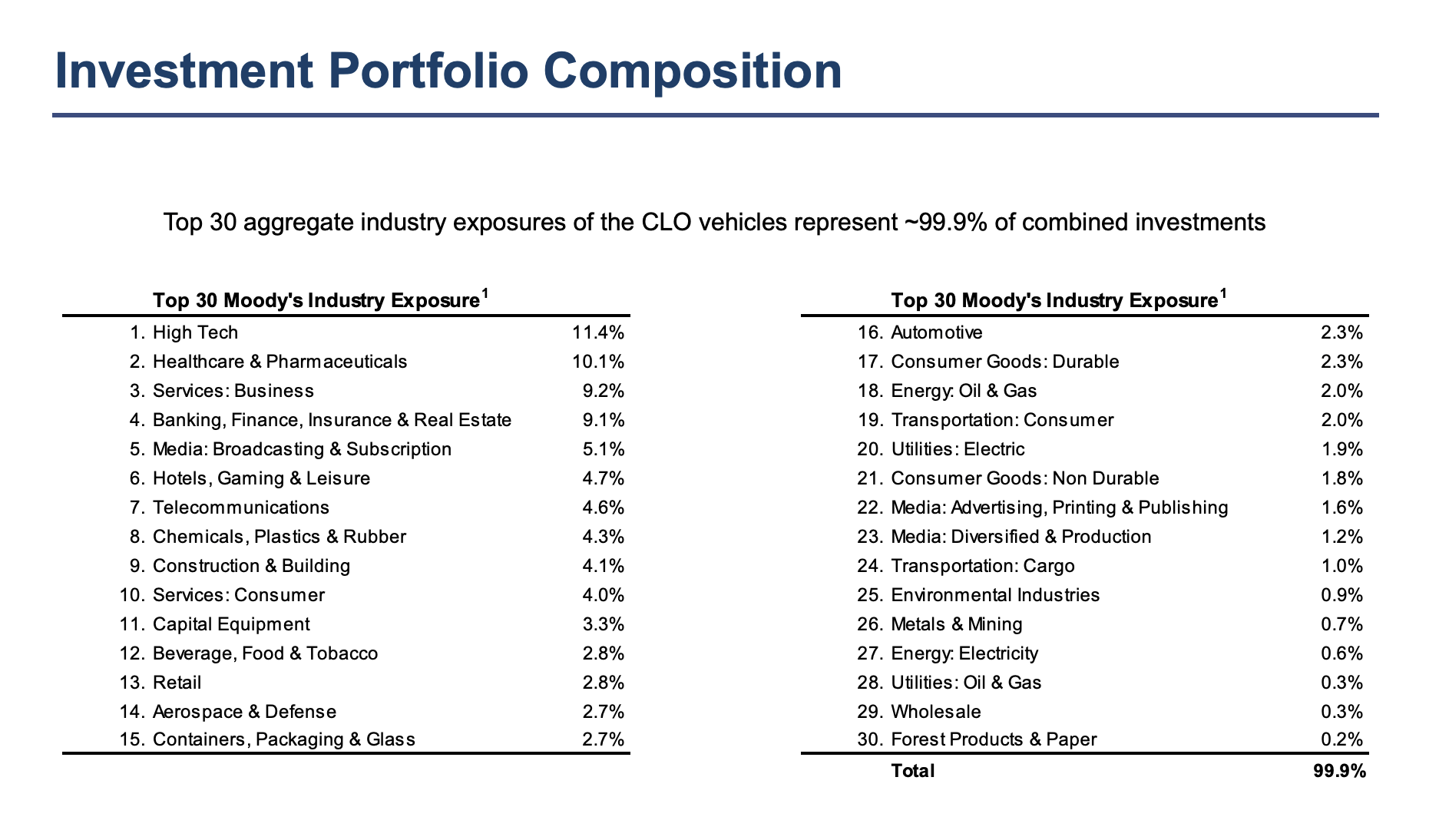

Diversification does come in multiple ways. For instance, it can come based on the number of holdings that are invested into. As of the end of the most recent quarter, the company's investments were allocated between 1,745 obligors spread across 236 investments between the company's CLO debt, CLO equity, and its warehouse equity and other investments, with the top 10 largest accounting for less than 3.7% of total holdings and the largest individual one amounting to 0.68% of holdings. The average individual one accounted for only 0.06% of holdings during that time. When it comes to industry-specific data, the firm is a bit more concentrated. Companies that it considers to be 'high tech' represent its largest exposure, totaling 11.4% of its invested assets. This is followed very closely by healthcare and pharmaceuticals at 10.1%. Service-oriented businesses are in third place at 9.2%. All combined, the five largest industries account for 44.9% of the company's investments at this time.

{kind=link}

This is all great. However, this doesn't mean that the company makes for a compelling prospect. There are two primary issues that I have with the firm. First and foremost is the fact that it has significantly underperformed the S&P 500. Over the past ten years, the S&P 500 has generated a return of 192.5%. That's with distributions included. By comparison, Oxford Lane Capital has achieved a total return of only 79.5%.

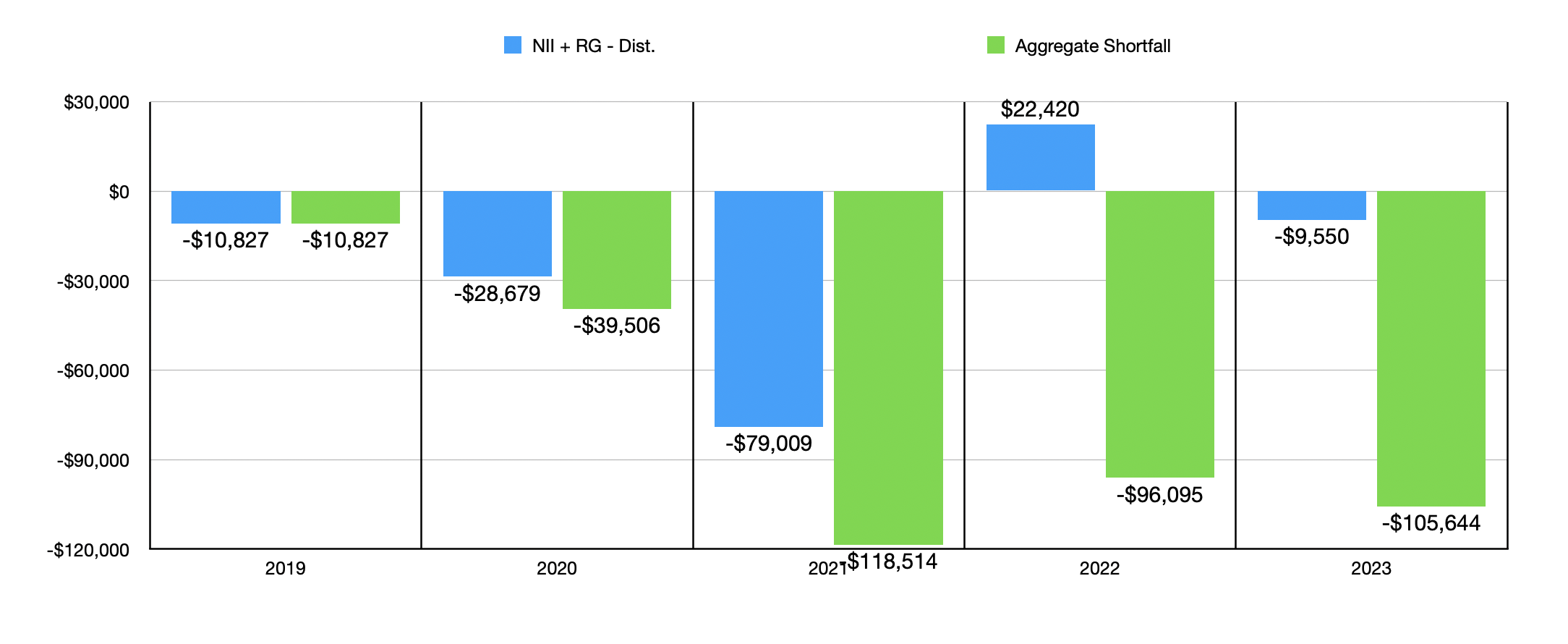

This may seem odd when you consider the hefty payout that the prospect offers. But that's where the picture gets rather ugly. For an opportunity like this, there really are only a few inputs and outputs that we need to look at in order to see if the distribution is sustainable. The first would be the net investment income. This is the income that the company brings in from its investments, minus any costs associated with operations. Next in line, we have net realized gains. When an investment matures or is exited, there is some real gain or loss experienced. If the combination of these two things are equal to or greater than the distributions, then you have a situation where the distribution is sustainable so long as this trend continues. But unfortunately, that is not the case. Looking at the past five completed fiscal years, we see that the shortfall in funding on this front has only grown significantly.

{kind=link}

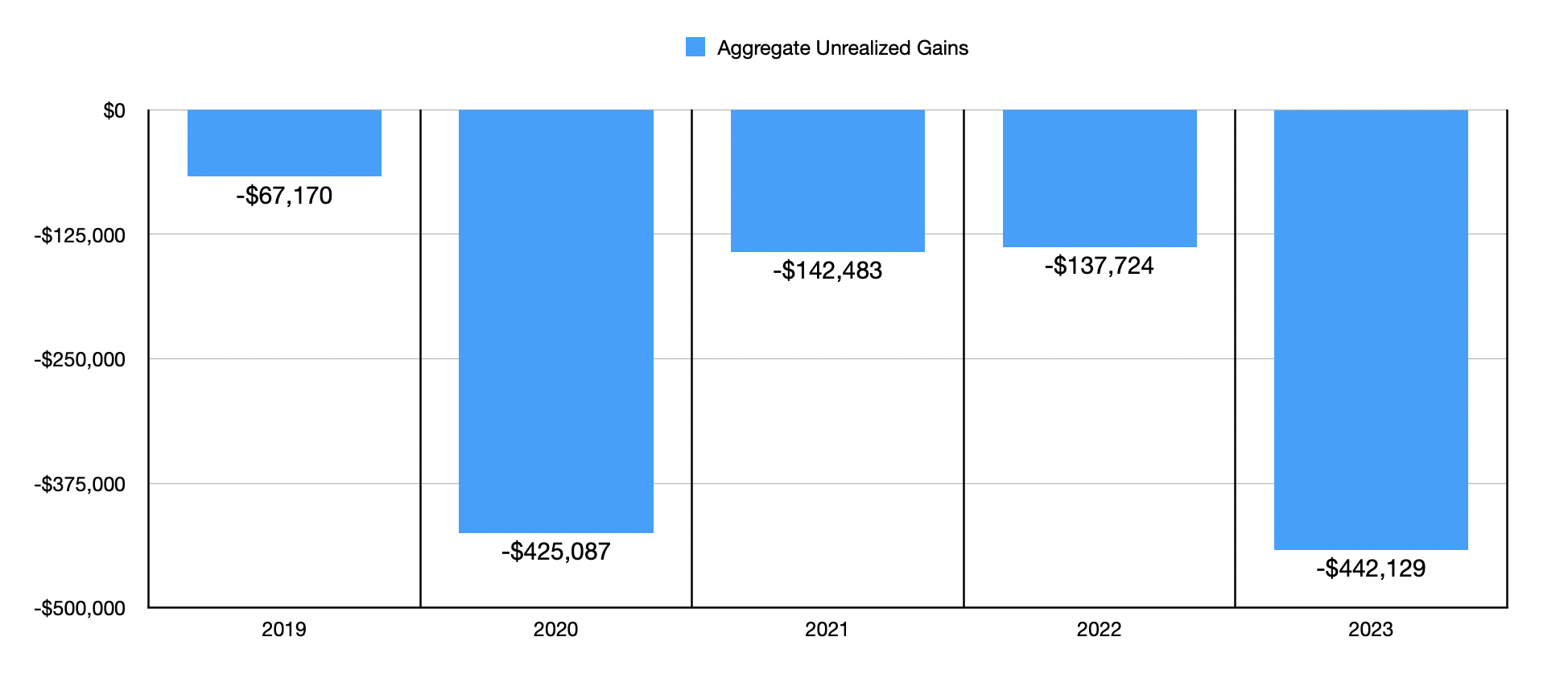

Between 2019 and 2023, distributions have exceeded the sum of net investment income and realized gains to the tune of $105.6 million. Now, a case could be made that unrealized gains should also be paid attention to. Unrealized gains are those that have not been sold, or exited otherwise, so they are not permanently locked in. But the problem with this argument is that unrealized gains have actually been negative to a rather significant degree over the same window of time. The aggregate total between 2019 and 2023 was negative to the tune of $442.1 million.

{kind=link}

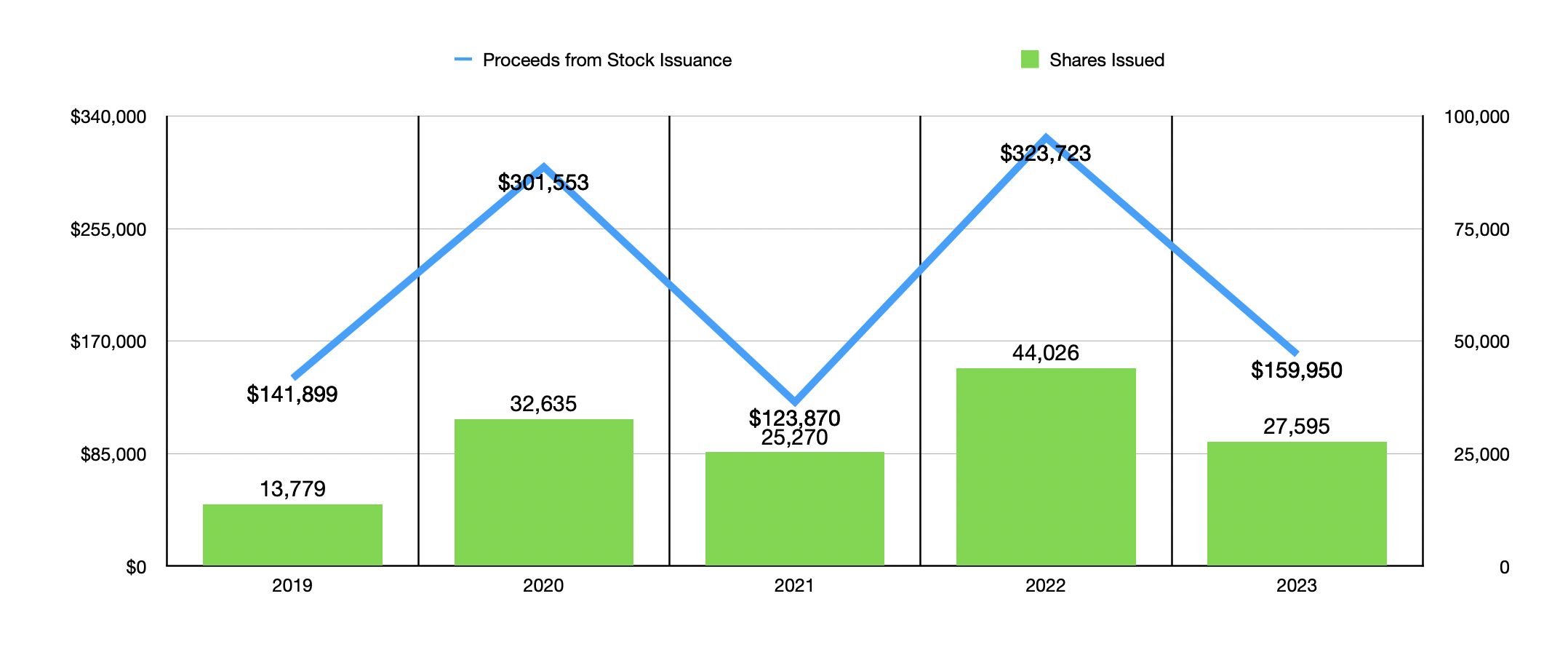

Where, then, has the company gotten its capital in order to grow and continue paying out the distribution? The answer lies in stock issuances. Between 2018 and 2020, the company has issued 143.3 million shares, bringing in $1.05 billion in capital. The allure of hefty yields has proven irresistible, especially when you consider that part of this window of time was when interest rates were still very low. But the problem with this is that, absent a change in the returns that it captures on its investments, and absent a change in distribution policy, Oxford Lane Capital can only pay out these hefty yields because of inflows of capital from other investors.

{kind=link}

Takeaway

Based on the data provided, Oxford Lane Capital is an interesting company. But it's not the kind of prospect that I would touch with a 10-foot pole. In the near term, it very well could go on to generate attractive returns for individual investors. But I would posit that it lacks the ability to keep paying out these distributions in perpetuity. Between that and the underperformance compared to the broader market, I do think a case could be made that there are definitely better prospects to be had out there. As such, I have decided to rate the enterprise a 'sell'.

For further details see:

I Wouldn't Touch Oxford Lane Capital With A 10-Foot Pole