IIIV - i3 Verticals: Growth Comes At A Price

2023-11-01 00:03:35 ET

Summary

- i3 Verticals builds and acquires software and payment solutions, primarily in the public sector and healthcare markets.

- The company has experienced significant growth in recurring SaaS revenue thanks to several acquisitions, but this has also caused dilution for shareholders.

- i3 Verticals has seen revenue growth, improved profitability and trades at attractive multiples, making the stock very appealing. However, high-interest rates and debt on the balance sheet pose some risks.

Investment Thesis

i3 Verticals ( IIIV ) builds, acquire and grows software and payment solutions in strategic vertical markets, primarily the public sector (e.g., municipalities for utility payments, states for auto registration billing) and healthcare. The company is growing at double digits and trades at attractive multiples, but we remain neutral as the current environment of high interest rates and aversion to tech stocks continues to put pressure in the stock.

IIIV's software and payment solutions incorporate specialized features tailored to fulfill the distinct needs their clients. Their payment technology seamlessly integrates with third-party business management systems used by their customers, ensuring both security and extensive reporting functionalities. This means that clients from various industries can easily incorporate IIIV's payment capabilities into their existing systems while maintaining data security and gaining access to detailed reporting tools.

Originally, IIIV was primarily recognized as a dedicated payment processing entity. However, in recent years, the company has adopted a software acquisition approach, in which they procure software assets and seamlessly integrate their payment engine into these acquired enterprises to drive organic expansion. This strategic move has enabled IIIV to swiftly transition towards a greater proportion of recurring SaaS revenue, marking a shift from being predominantly a "payments" company to becoming a "software" enterprise.

The company has made 48 acquisitions since becoming public in 2018. However, this growth has come with a price to shareholders. IIIV has funded most of their acquisitions with shares, which has caused massive dilution. Since becoming public, the stock is basically flat while the market cap increased almost 200%.

But how is the business performing today? In the first three quarters of their fiscal year, revenue grew 17.7% YoY to $273.8 million , and management expects revenue for the full fiscal year to be between $360 million and $380 million (+16.2% YoY at the midpoint). Moreover, annualized recurring revenue for the last quarter was $311.4 million, compared to $266.7 million a year ago, representing a period-to-period growth rate of 16.8%. Software and related services revenue as a percentage of total revenue was 50.3% for the latest quarter, compared to 48% a year ago and 42% two years ago.

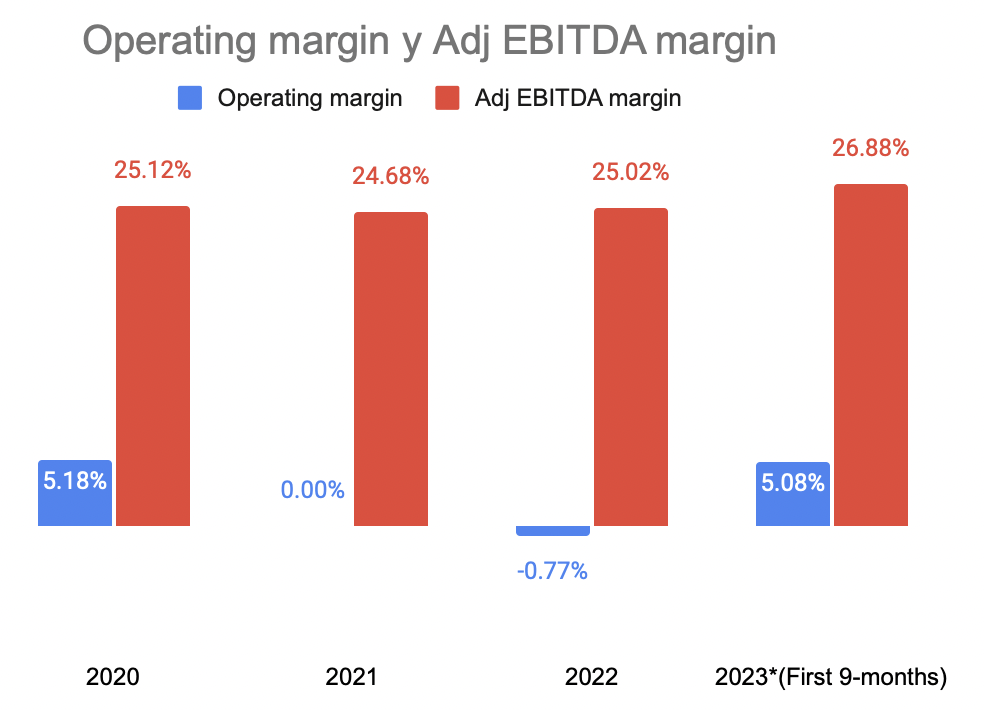

Income from operations was $13.9 million in the nine months ended June 30, versus a loss of $9.6 million the previous year. This represented a 5.08% margin. However, due to the rise in interest rates, interest expenses grew by 79% to $18.4 million, and the company recorded a net loss of $5.3 million.

Adjusted EBITDA was $73.6 million so far this year, up 27.3% YoY. This represented a 26.88% margin. They expect to finish the year with adj EBITDA between $97 million and $103 million, which at the mid-point would be a +27% margin. We will discuss this number is more detail later.

{kind=link}

At $18.18, IIIV has a market capitalization of $608 million. If we sum financial debt ($390 million) and subtract cash and equivalents ($5 million), we arrive at an enterprise value of $993 million. This means that the stock trades at 2.7x EV/Sales, 9.9x EV/Adj EBITDA (using 2023 guidance), and 17.3x P/FCF ((TTM)). These multiples are very attractive, especially for a company whose revenue is increasingly recurring. For comparison, Tyler Technologies (NYSE: TYL ), a public sector pure-play software enterprise, trades at 8.2x EV/Sales, 33x EV/EBITDA, and 37.8x P/FCF (all forward measures). If IIIV were to trade at, let's say, 4x EV/Sales, the stock should rise 80% from current levels.

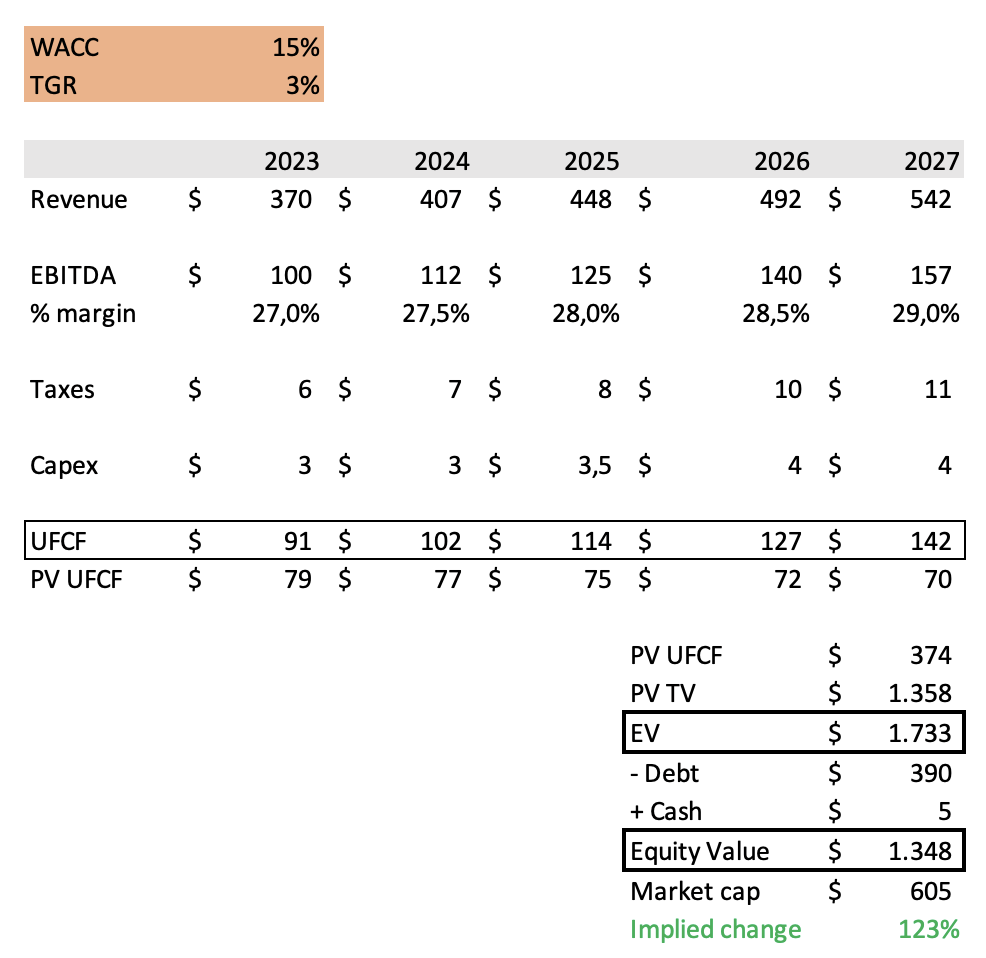

We also decided to do a DCF model. We assumed that revenue will grow at 10% for 5 years, EBITDA margins will expand by 0.50% per year, they will pay a 30% tax rate on EBIT and capex will remain more or less constant. We also assumed a WACC of 15% and a TGR of 3%.

{kind=link}

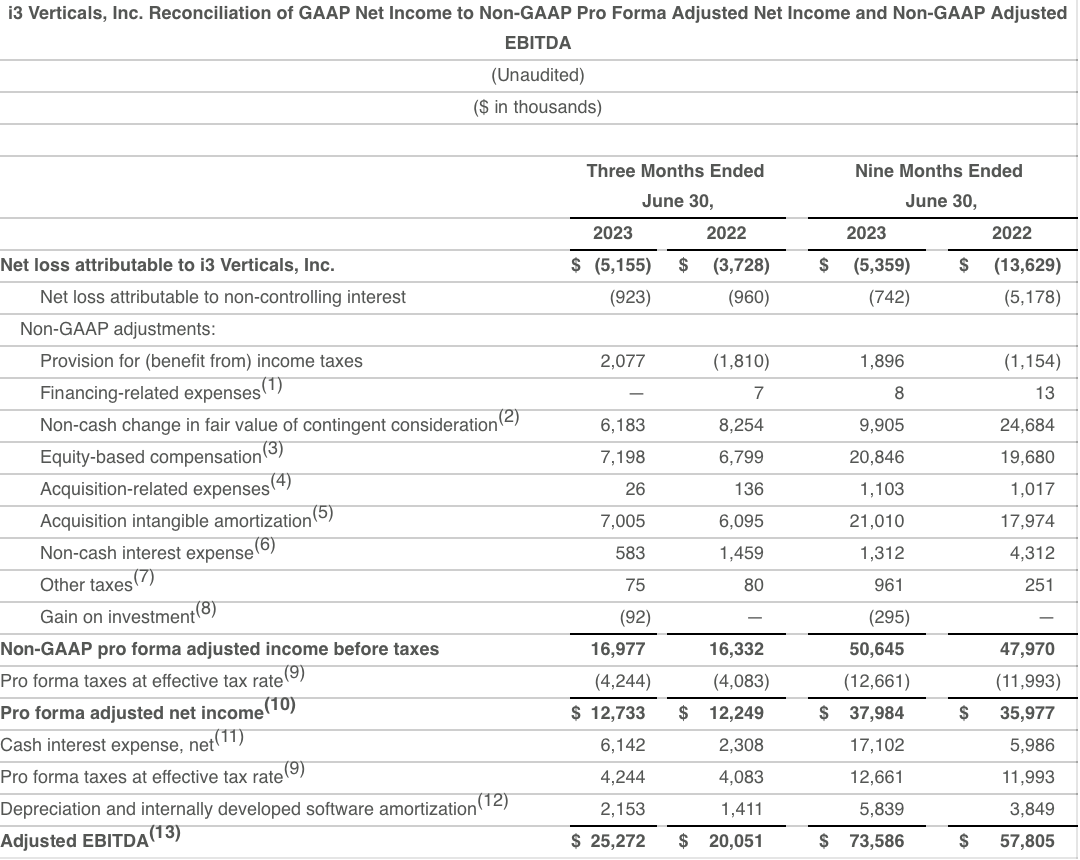

Wow! The equity looks very undervalued. Well, not so fast. The 27% EBITDA margin is adjusted, and it has a lot of adjustments. Here are all the cost the management adds back:

{kind=link}

Net loss magically goes from -$5 million to a profit of $39 million. I know some of the cost they add back are non-cash, like share based compensation, but they are a real cost to shareholders. The GAAP EBITDA margin is closer to 15%. If we use that margin, here is the DCF model updated:

{kind=link}

Overall, we believe that IIIV will continue to growth at mid-double digits for the coming years, fuel by acquisitions and synergies, while improving profitability. The stock seems fairly valued and it wouldn't surprise us to see it go higher. However, in the current market environment of high interest rates and aversion to tech stocks, we think fair value can quickly turned into overvalued. Since the stock is in a free fall, we remain neutral and patient for a better entry point under $15-$14 dollars per share, where we would have a nice margin of safety.

Risks

IIIV states very clearly that they pursue growth through acquisitions, and in this environment of high-interest rates, making acquisitions can be very expensive. This can result in more dilution or debt on the balance sheet, neither of which is good for shareholders.

Lastly, although the company has financed most of their acquisitions with share dilution, it does hold a sizable amount of debt on its balance sheet. The interest coverage ratio (EBIT/Interests) was 4.31x, and the total leverage ratio (Debt/EBITDA) was 4.00x at the end of the latest quarter. Their credit facility agreement requires them to maintain an interest coverage ratio of not less than 3.00x and a total leverage ratio of no more than 5.00x. Otherwise, the company could be seen in breach of its debt covenant and trigger a technical default.

For further details see:

i3 Verticals: Growth Comes At A Price