MGM - IAC: Asymmetric Investment At $42

Summary

- Struggles at Angi and Dotdash Meredith have caused IAC's share price to plummet ~65% during 2022.

- With much of its valuation covered by its stake in Angi and MGM, at its current share price, investors are paying very little for Dotdash, Turo, Care.com, and other assets.

- While some of IAC's holdings are performing poorly, a modest improvement could yield significant returns for shareholders.

- Even if business conditions remain weak, I see little downside in IAC shares at the current price.

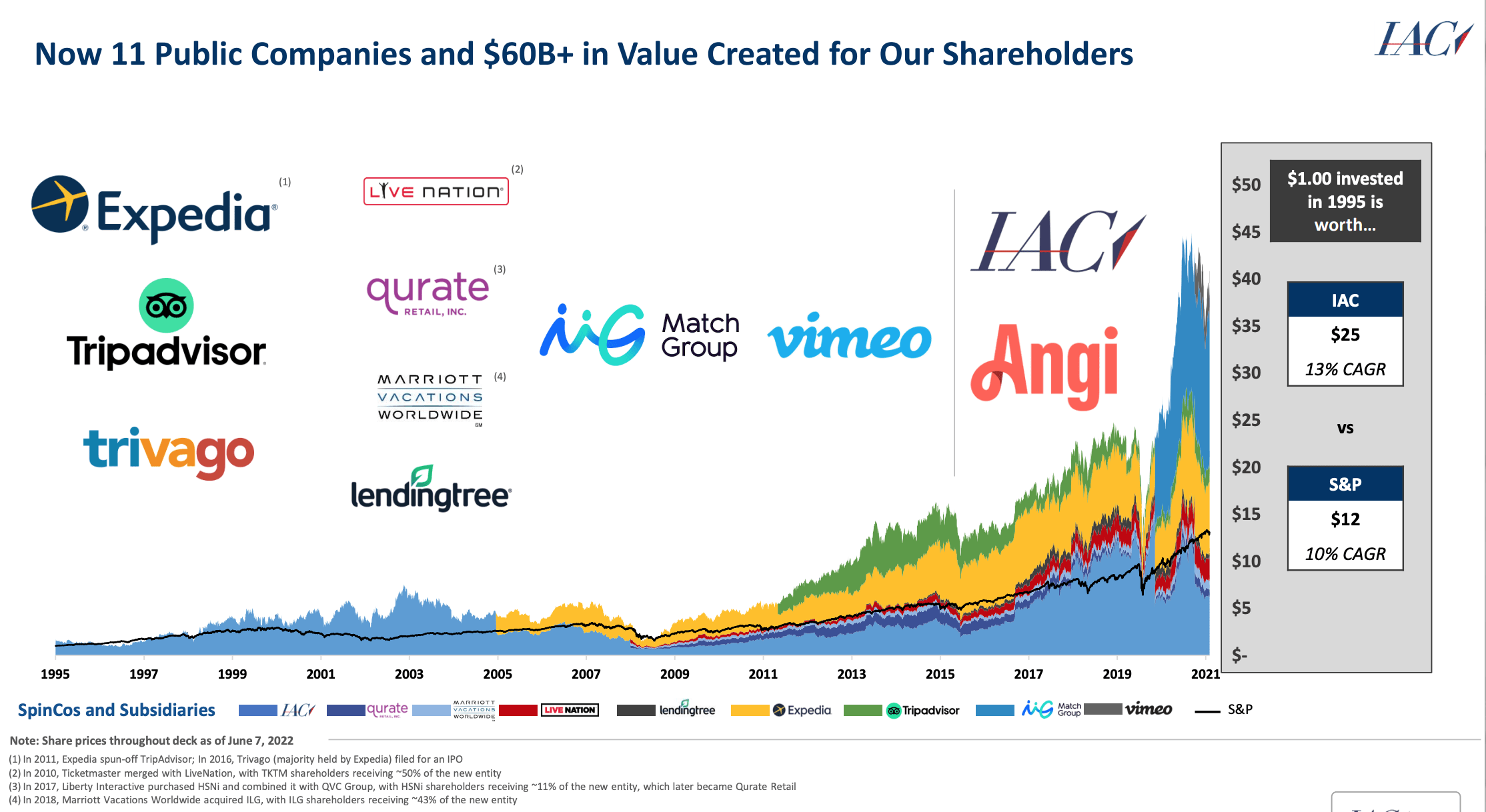

What a difference 24 months makes. Two years ago, IAC ( IAC ) management was revered as being the leading builders of online marketplaces with a multi-decade track record of developing several market-leading businesses and creating tremendous shareholder value (as shown below).

A Builder of Businesses (Investor Presentation)

{kind=link}

More recently, IAC has hit a rough patch which has caused its share price to plummet. Two of its largest businesses, Dotdash Meredith (Meredith was acquired in late 2021) and Angi ( ANGI ) are struggling and investors seem to have lost patience that the company can improve the fortunes of these two businesses. Similarly, investors are giving little-to-no credit for IAC's investments in Care.com and Turo, two leading marketplace businesses.

Should Dotdash Meredith or Angi start to show an improvement in results or if investors become more optimistic on Turo (which is producing record results), IAC shares could see shares more than double. If results continue to sputter, as I show below, I see little downside. Given what I believe to be an asymmetric situation, I've taken a long position in the stock.

Current results

IAC has two problem children - Angi and Dotdash Meredith:

- Angi has struggled since the pandemic created a shortage of home service professionals (leading to low fulfillment rates/poor customer service) and a bungled rebranding. Further, management estimates the mishandled rebranding of HomeAdvisor (which was merged into Angi) has cost the company $100 million in annual profits. While difficulties in rebranding are certainly disappointing, ultimately I believe this is the right strategy as it should allow for more efficient ad spend.

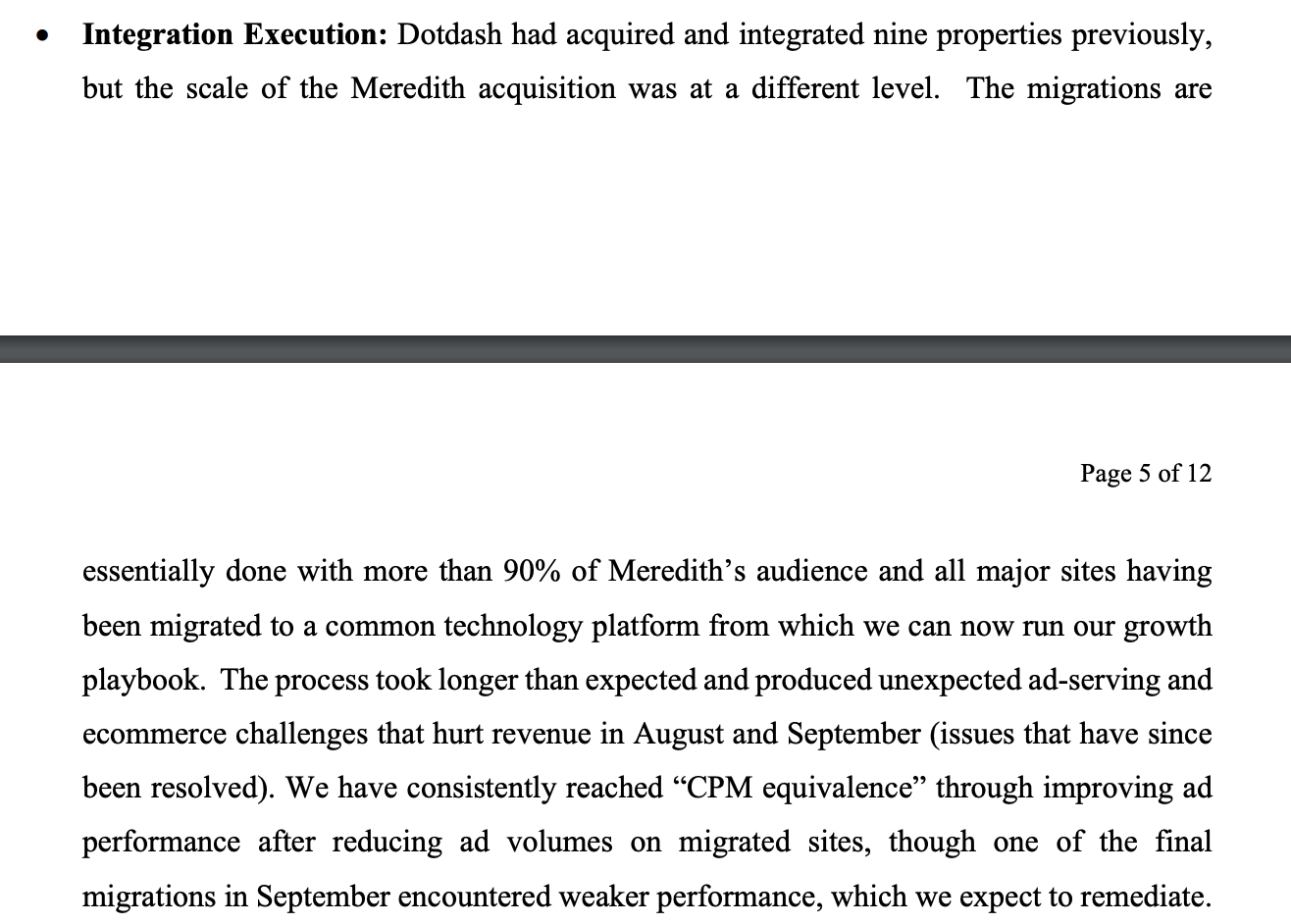

- Just over one year ago, IAC's Dotdash acquired Meredith for $2.7 billion in what has proven to be a poorly timed acquisition. Like Dotdash, Meredith is a publisher of content (both digital and magazines). The environment for advertising, particularly digital advertising, has been very difficult as clients have curtailed advertising spending amidst an expected slowdown in consumer spending. Further, the merger of Dotdash and Meredith has encountered operational difficulties (described below).

Discussion of Dotdash Meredith Execution Issues (IAC 3Q22 Shareholder Letter)

{kind=link}

While at the time of the acquisition, management expected the combined Dotdash Meredith to produce digital EBITDA of $450 million in 2023, operational setbacks and the difficult advertising environment suggest the business will produce less than $300 million in EBITDA in 2023.

Valuation

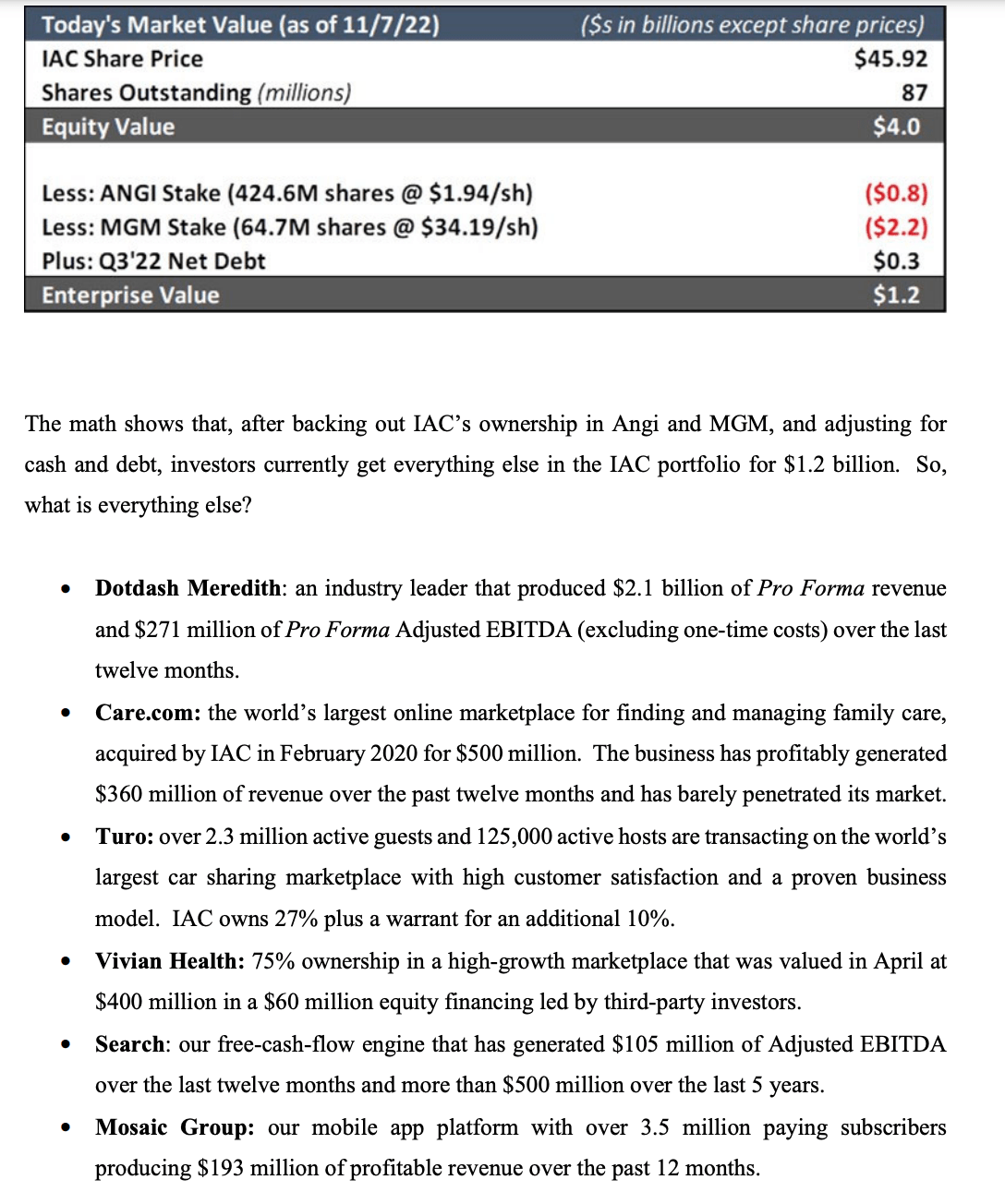

In its 3Q shareholder letter, management called out the extreme dislocation in IAC's share price. Subtracting out the stakes in the publicly listed holdings, Angi and gaming company MGM ( MGM ), at today's price ($42.50, down 7% from when IAC's 3Q letter was published) investors are buying Dotdash Meredith, Care.com, a 27% stake in car sharing company Turo and a collection of smaller assets for just under $1 billion.

IAC Valuation - Stub (3Q22 IAC Shareholder Letter)

{kind=link}

As for the two publicly traded holdings, at $34/share, I see gaming company MGM as being modestly undervalued at 9.5x current adjusted EBITDA with potential upside from a recovery in Macau and its online gaming business.

Last week I wrote a piece on SA, highlighting the upside potential in Angi. Should operating issues be resolved and financial results merely return to historical levels, this could add $15 per IAC share.

While Dotdash Meredith appears to have resolved the operational challenges which plagued the business during 3Q, the current advertising environment remains difficult. If we assume that the company can simply maintain trailing TTM adjusted EBITDA of $271 million and apply a 7x multiple to the business, this implies the business is worth $1.9 billion.

Taken together, in a modestly bullish scenario MGM, Angi, and Dotdash alone would be worth ~$60 to IAC shareholders (after deducting debt).

Beyond the big three, I think Care.com and Turo could add another $10-$15 to IAC's valuation. Care.com has grown revenue by ~70% from 2019 levels and is profitable. As the leading marketplace for managing family care (matches providers of elderly and childcare to households), the business should produce 20-30% EBITDA margins at scale. At a conservative 2-3x current revenue, the business would be worth another $8-$12 per IAC share.

While the market for IPOs has largely been dead in 2022, Turo's recently updated S1 shows improved revenue and profitability.

For further details see:

IAC: Asymmetric Investment At $42