BABWF - IAG: Robust Earnings Indicate Blue Skies Ahead (Rating Upgrade)

2023-08-03 15:59:25 ET

Summary

- British Airways owner International Consolidated Airlines Group S.A.'s half-year results were well-received last week, with a 6.7% increase in stock price, driven by increased revenues and improving margins as fuel prices cooled off.

- With strong forward bookings, the rest of 2023 looks good too. The company's debt is also more under control.

- Though liquidity is slightly wanting, it's not a big enough challenge to cloud the whole picture. International Consolidated Airlines Group's forward P/E looks attractive compared to peers as well, indicating upside to it.

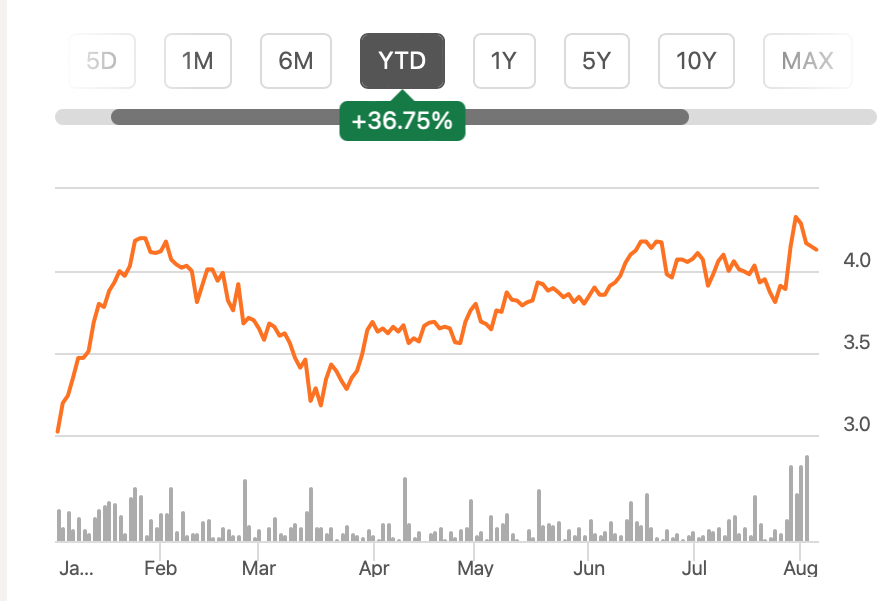

Since the last time, I wrote about the British Airways owner International Consolidated Airlines Group S.A. ( ICAGY , BABWF), also called IAG, in early February, its price has risen by only 4.2%. This is, of course, disappointing, considering that in January 2023 alone its price had more than doubled. But it’s not unexpected. Even then, my analysis showed that the price has run ahead of the fundamentals, which led me to give it a Hold rating.

{kind=link}

However, there is potentially a new catalyst in place. Its half-year (H1 2023) results were released at the end of last week. They were definitely well received by investors, going by the 6.7% increase in IAG’s price on the day, the biggest daily rise seen in 2023. So far, its price hasn't gone back to pre-result levels. The question, though is, can it sustain over time? Let’s find out.

Revenues up, improving margins

There’s a lot to like about IAG’s latest numbers . Here are a few key points that stood out for me:

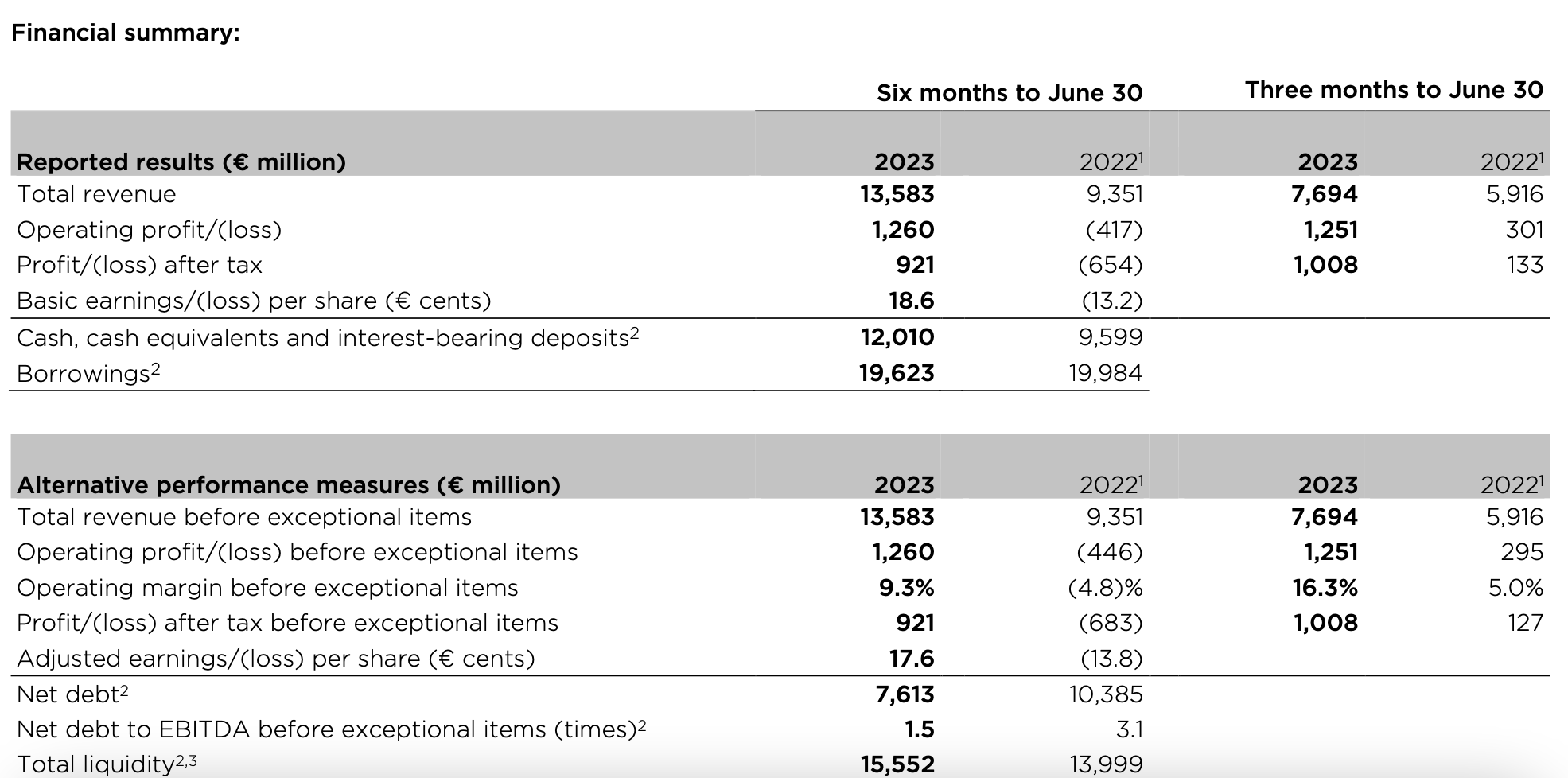

- Its revenues are up by 45% year-on-year (YoY), with 30.1% growth in the second quarter (Q2 2023), driven by increased passenger capacity, load factors and also higher yields per passenger. Leisure traffic, in particular, has been strong, though business travel is recovering at a slower pace.

- Operating expenses were up by a firm 26% during H1 2023, but there are signs of slowing down in costs in Q2 2023 when they rose relatively more moderately by 14.7%. Notably, the rise in fuel costs slowed down to single digits during the quarter, which is significant considering they account for a fourth of all costs. Lower jet fuel prices and more fuel-efficient aircrafts contributed to this development.

- IAG has shown both an operating profit and a net profit, in contrast with losses during the same time last year. It’s also encouraging to see an improvement in its margins in Q2 2023. The operating margin is now at 16.3%, while the net margin is at 13.1% compared to figures of 9.3% and 6.8% respectively for H1 2023.

- In terms of its alternative performance measures, IAG’s passenger capacity is now only 5.7% lower than it was pre-pandemic. The remaining drag is primarily because of a slow recovery in the Asia Pacific region, which isn’t surprising considering China’s COVID-19 restrictions until late last year. Notably, the passenger load factor at 84.1% in H1 2023, is actually higher by 1.1 percentage points compared to the same period in 2019.

{kind=link}

Better debt and liquidity position

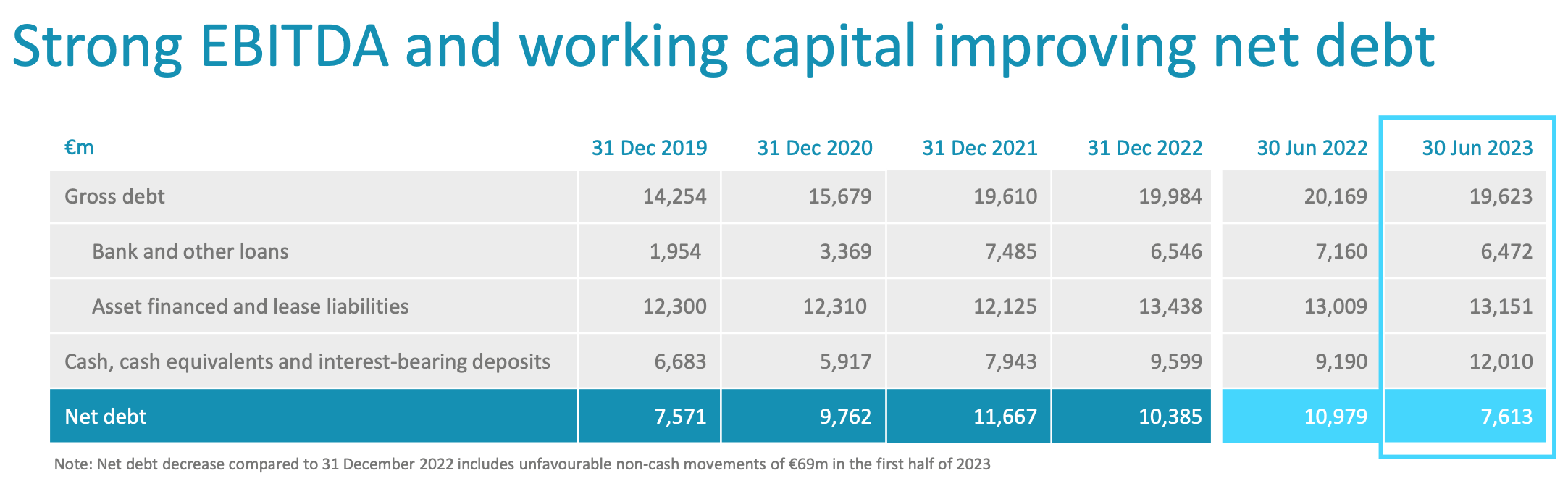

Its debt levels also look a whole lot better. The net debt- to-EBITDA before exceptional items halved to 1.5x from H1 2022. This followed a net debt reduction as liquidity improved due to higher profitability and forward bookings as well as lower gross loans. This is a huge improvement from the last time I checked and below the net debt to the EBITDA ceiling of 1.8x.

{kind=link}

However, I’m still marginally uncomfortable with its liquidity levels, with its working capital ratio at 0.76x, which indicates it doesn’t have enough to meet all its current obligations. That said, 48% of these liabilities are in the form of unearned revenue, which is presumably forward bookings. So, unless something goes very wrong, like lockdowns, it’s unlikely that IAG will be obliged to actually return them. Further, it has also historically had a low working capital ratio. Even in 2018, much before the pandemic, it was at 0.91x, which isn’t ideal. Still, the reason I’m a bit cautious about is that it’s even lower than historical levels right now.

Attractive market valuations and a positive outlook

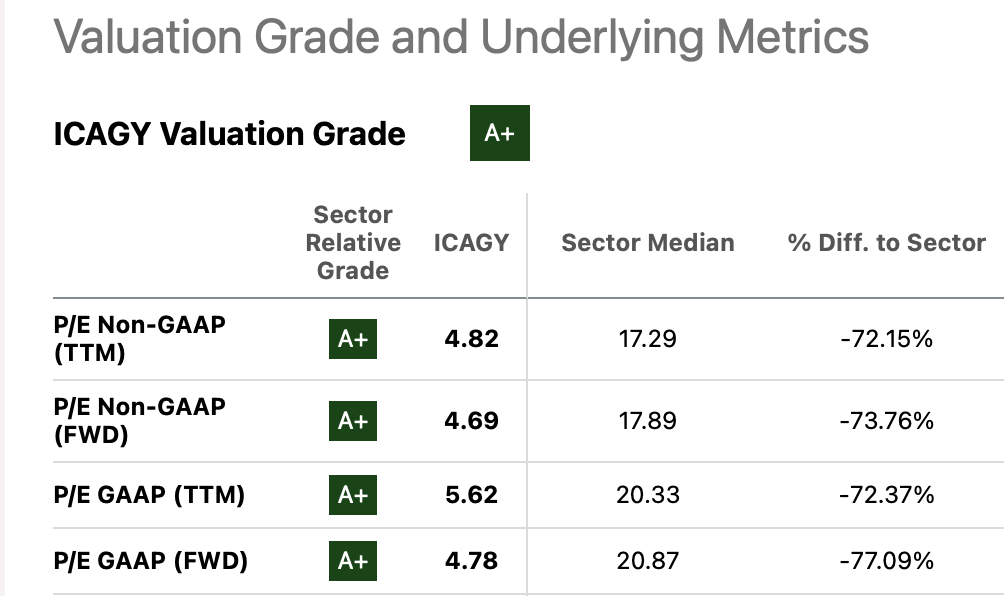

This doesn’t however detract from the overall attractiveness of the stock. All its price-to-earnings (P/E) ratios are way below those for the Industrials sector (see table below). In particular, I’d like to bring your attention to the forward P/Es. At 4.8x, the GAAP forward P/E has fallen significantly from its 42.9x levels the last I checked. On the other hand, the corresponding figure for Industrials has actually increased slightly over this time.

{kind=link}

It looks far less undervalued compared to peers like American Airlines Group ( AAL ) and Deutsche Lufthansa ( OTCQX: DLAKY ), which have forward GAAP P/Es of 5.3x and 6.3x, respectively. However, even these valuations for peers indicate on average a 20% upside for IAG right now.

I am even more convinced of the upside to the stock considering projections for the upcoming quarters and for the next year. After a big bump up in earnings per share [EPS] in 2023, they are expected to continue growing in 2024, as per analysts' estimates , bringing them quite close to pre-pandemic numbers.

The positive projections are also corroborated by IAG’s own outlook, at least for the remainder of the present year. It’s already 80% booked for the third quarter and 30% for the fourth quarter. It also expects capacity to be at 97% of pre-COVID-19 levels for the full year. Without giving any numerical profit guidance, it does say it expects “profit outperformance,” which in turn is seen as spilling over into generating “sustainable free cash flow this year” and a continued decline in net debt as well. In other words, all looks pretty good for the company.

What next?

Comparing now to early February, when I wrote about IAG, the big concerns on my mind have now been addressed. First, the recovery is no longer tentative, it's firmly underway. This is evident in revenue and profit growth and also the outlook for the year. In fact, by the end of next year, its earnings will be almost back to pre-pandemic levels.

Next, with growing profits, its net debt situation has improved and IAG expects it will improve even further by the end of this year. Sure, its balance sheet isn't a 100% perfect. Not with a sub-1x working capital ratio. But since it's skewed because of a high level of unearned revenues, at a time when the pandemic is well behind us, it's not a particular source of stress.

Also, International Consolidated Airlines Group S.A.s forward P/E ratio looks far more reasonable than the last time I checked. It is now competitive compared to the industrials sector and is even attractive compared with those of its closest peers. There is a clear upside to the stock even now. I’m upgrading it to Buy.

For further details see:

IAG: Robust Earnings Indicate Blue Skies Ahead (Rating Upgrade)