IAG - Iamgold: Nearing The Finish Line At Cote Gold

2023-08-11 18:38:17 ET

Summary

- Iamgold released its Q2 results this week, reporting a significant decline in production at costs well above the industry average.

- Unfortunately, this isn't expected to improve in H2 with costs tracking toward the high end of guidance and Cote not moving into commercial production for nearly a year.

- In this update, I'll look at where Iamgold's conservative fair value sits and if the stock is finally offering enough margin of safety to justify going long.

Q2 Production and Sales

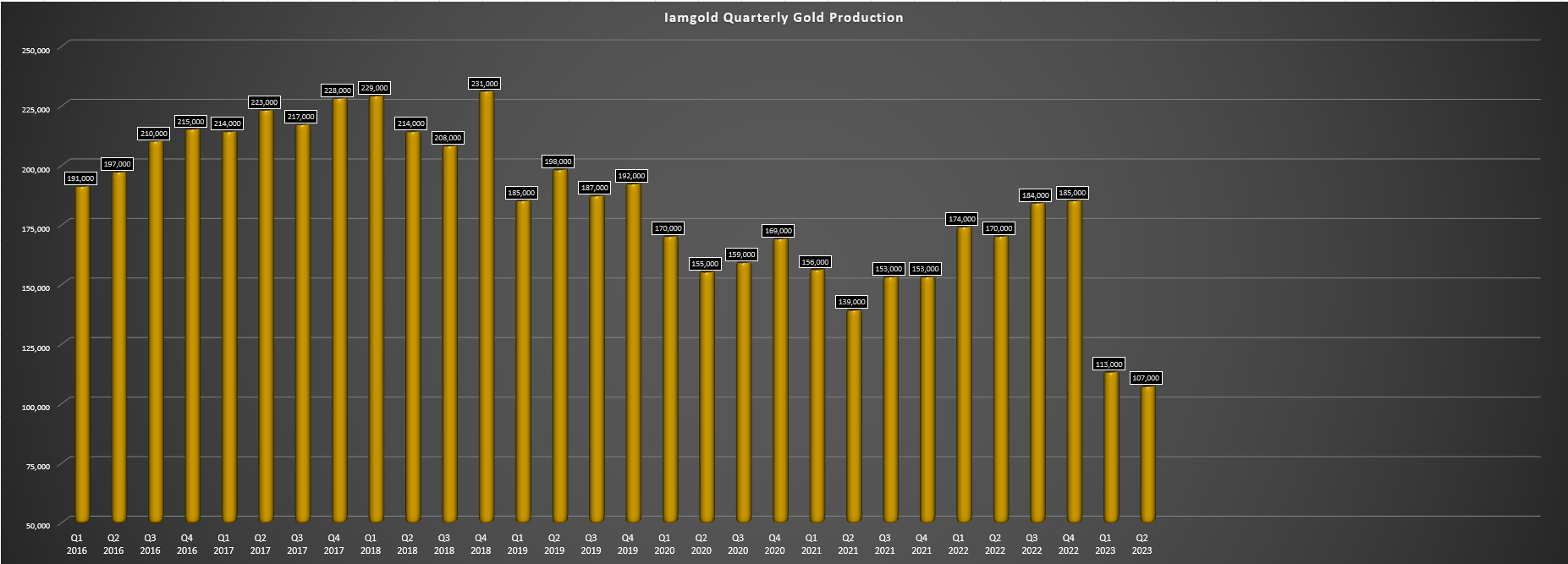

Iamgold (IAG) released its Q2 results this week, reporting quarterly attributable production of ~107,000 ounces of gold, a significant decline from the year-ago period (Q2 2022: ~170,000 ounces). This sharp decline in output was due to lapping tough comps at Essakane with a higher grade quarter (1.52 grams per tonne of gold) and lapping ~49,000 ounces of production from Rosebel, an asset that's since been sold to help fund Cote Gold construction without having to resort to share dilution. Unfortunately, this not only contributed to significantly lower output and revenue but also led to a sharp decline in all-in-sustaining cost margins despite the benefit of a higher average realized gold price ($1,973/oz).

Iamgold - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

As shown in the chart above, Iamgold has had one of the worst track records of production growth sector-wide (down from a peak of 800,000-plus ounces), which is even worse on a per-share basis when the share count has grown over 10% in the period from 2016 levels. Fortunately, some of the holes left relative to the prior production profile will be back-filled once Cote Gold heads into production, and this asset should pour its first gold within nine months. That said, Iamgold's ownership has dropped further after selling a stake to Sumitomo (with an option to buy this back at a later date), meaning that production will still be below FY2016 levels (~813,000 attributable ounces) during peak years of production from Cote. Meanwhile, Westwood and Essakane are staring down sub five-year mine lives, providing less visibility into what Iamgold's production profile looks like post-2027.

Iamgold - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

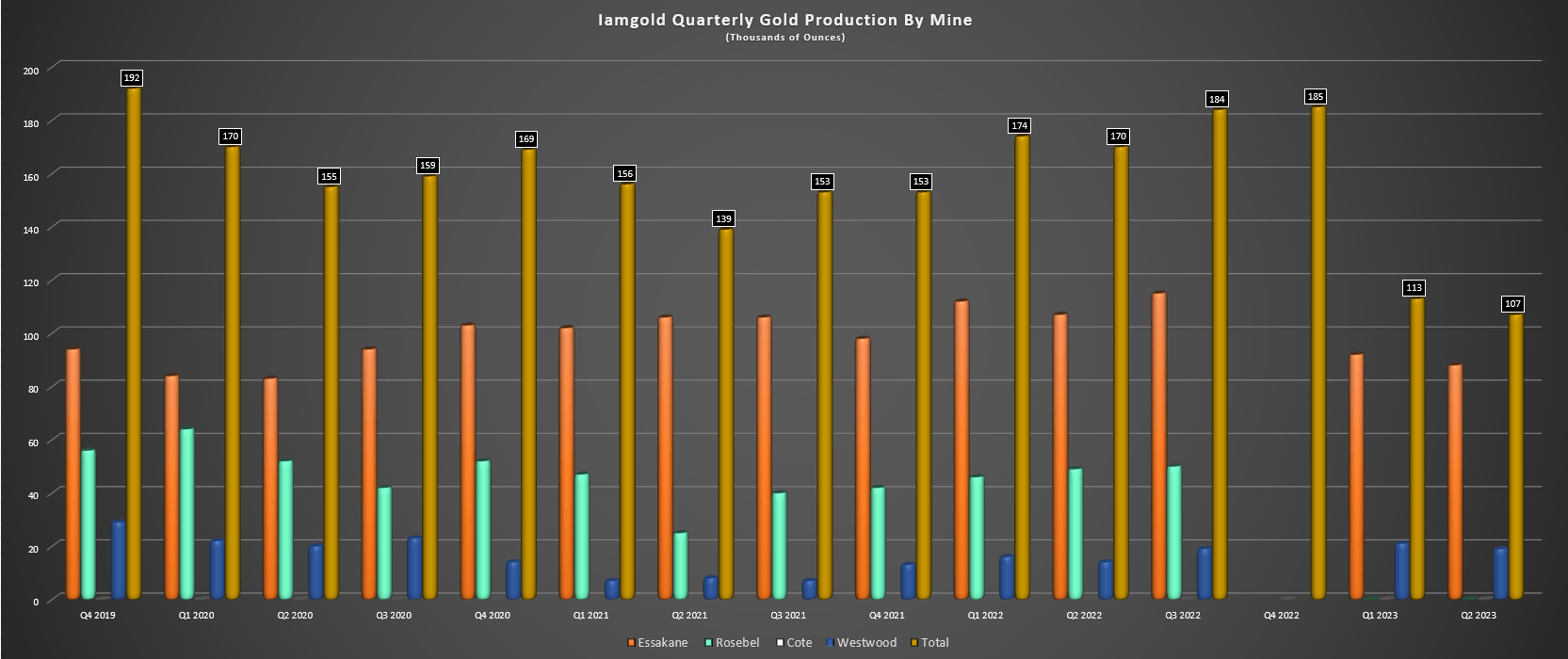

Taking a closer look at Iamgold's current operations, Essakane produced just ~88,000 attributable ounces in the period, down from ~107,000 ounces in the year-ago period. The decline in production was related to lower grades which offset the increased throughput in the period (~3.08 million tonnes), with grades declining due to the use of lower-grade stockpiles and initial ore from new mining phases. Meanwhile, recoveries slipped due to higher levels of graphitic carbon and sulfur from the new mining phases. The result was that all-in sustaining costs [AISC] at the asset spiked to $1,587/oz (Q2 2022: $1,124/oz), and Iamgold noted that consolidated all-in sustaining costs are now likely to come in near the top end of guidance, and above the expected midpoint of $1,662/oz, partially related to higher than planned sustaining capital expenditures in FY2023.

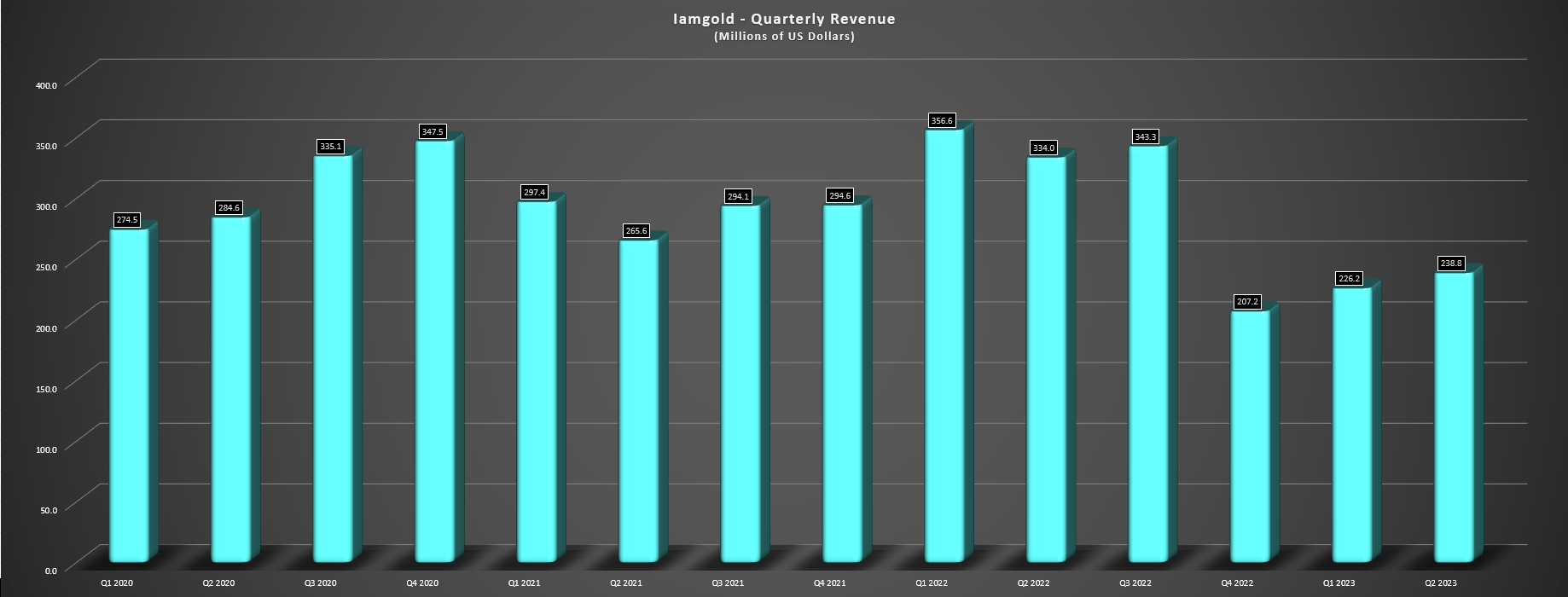

As for Westwood, production was ~19,000 ounces in the period, benefiting from higher-grade overall mill feed and increased underground tonnes mined. However, even with a better quarter with a 30%-plus increase in production year-over-year, this didn't really move the needle and could not pick up the slack from Essakane. The result was that quarterly revenue slid to $238.8 million from $334.0 million in Q2 2022 despite higher gold prices, with ~121,000 ounces sold at $1,973/oz in the period. Meanwhile, operating cash flow slid to $21.8 million before working capital, down from $93.9 million in Q2 2022. This was certainly disappointing, with Iamgold seeing lower revenue and cash flow year-over-year vs. many peers that have benefited from higher revenue, helped by the record average realized gold price.

Iamgold - Quarterly Revenue (Company Filings, Author's Chart)

{kind=link}

So, is there any positive news?

Iamgold does have a new CEO in Renaud Adams whose arrived at a timely point for the company to hopefully come in and sweep up some of the mess. In addition, Cote Gold is now 87% complete, 70% of the planned ~$3.0 billion capex (100% basis) has been spent, and Iamgold's cost to completion is covered by its available liquidity of ~$1.2 billion. This has helped to calm any worries about significant equity dilution to bring the asset into commercial production, and investors also are one year closer to having an exceptional operating asset in the portfolio which was no longer the case as of 2022 with the best years behind Rosebel (now sold) and Essakane already. Plus, the timing of the first production is coinciding with gold prices that seem to have a floor near $1,800/oz, with the delay in getting this asset into production paying off with near-record gold prices.

Costs and Margins

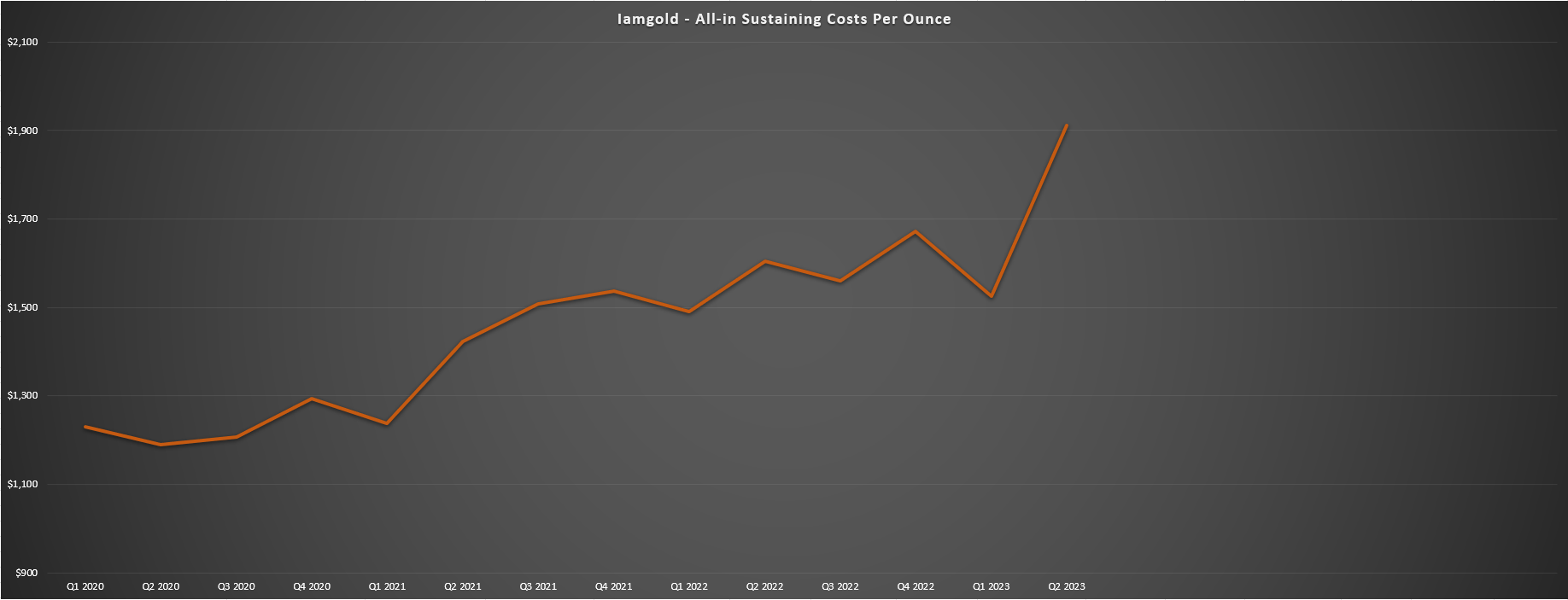

Unfortunately, there wasn't much to write home about from a cost standpoint, with Westwood remaining a small-scale operation at sub 20,000 ounces per quarter despite the benefit of higher underground and open-pit grades in the period. The result of this relatively low production profile and elevated sustaining capital was all-in sustaining costs came in at some of the worst levels sector-wide at $2,903/oz. And as noted, Essakane's costs were above the industry average at $1,587/oz, with Iamgold noting that the landed cost of fuel has increased due to measures taken to mitigate the "deteriorating" security situation in Burkina Faso. Meanwhile, heavy fuel oil has been substituted for higher-cost light fuel oil due to availability, impacting its processing costs. These are uniquely negative developments, with many peers calling out lower energy costs related to HFO and diesel in Q2, like B2Gold ( BTG ).

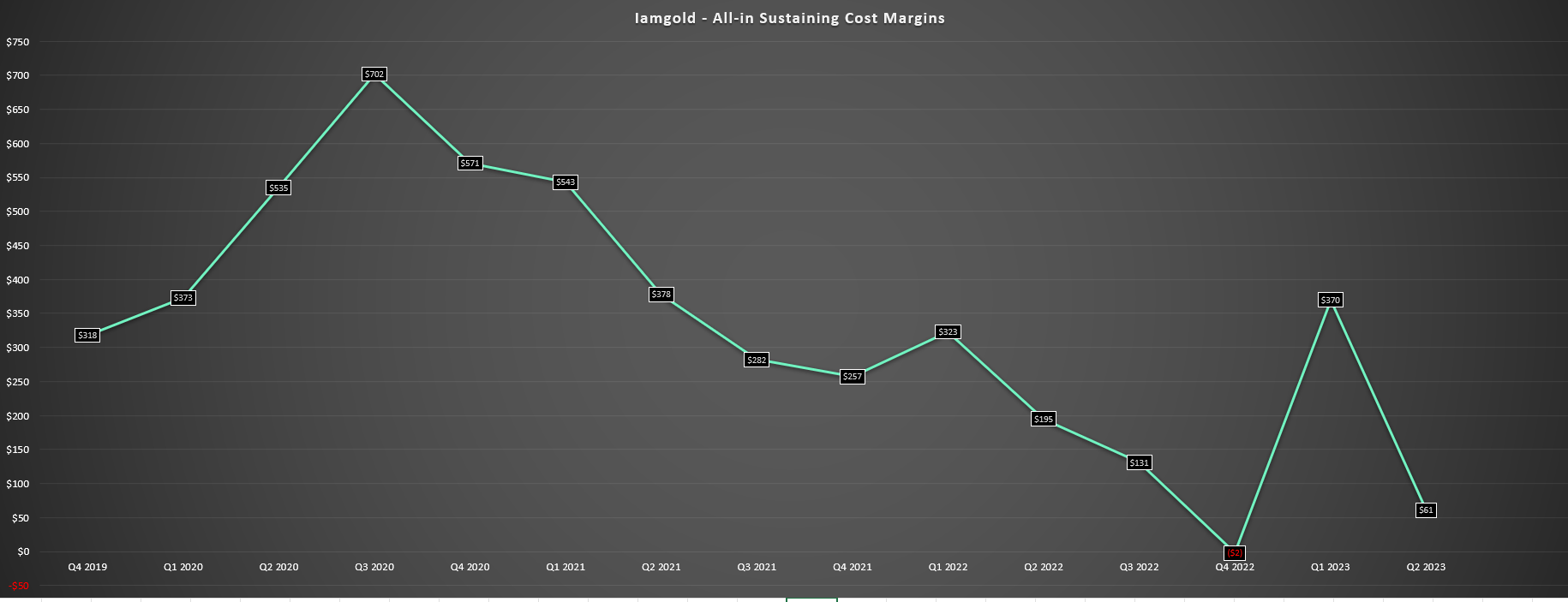

Given the higher costs at Essakane (fewer ounces sold and supply chain headwinds), all-in-sustaining costs hit a new high of $1,912/oz in the period, up from $1,604/oz in Q2 2022. This resulted in AISC margins plunging to $61/oz vs. $195/oz in the year-ago period. These are among the weakest margins sector-wide, and given that the security situation doesn't appear to be improving, it's hard to be optimistic about Essakane bringing costs below $1,500/oz going forward. Plus, while most miners benefited from improving margins on a year-over-year basis, Iamgold saw the opposite, and sentiment for West African miners is arguably worsening which might continue to weigh on Iamgold's stock until Cote has poured its first gold and can turn around its financial results and improve its jurisdictional profile from an operating standpoint.

Iamgold - All-in Sustaining Costs (Company Filings, Author's Chart) Iamgold - Quarterly AISC Margins (Company Filings, Author's Chart)

{kind=link}

{kind=link}

While the above figures are among the worst sector-wide, it's worth noting that Cote Gold will be a transformational asset for the company, with attributable production of ~290,000 ounces at sub $900/oz costs, a massive deviation from its current cost profile. So, while I was previously quite negative on Iamgold since 2020 as the stock was years away from seeing any major improvement in its cost profile with rising costs at all three of its assets, there's finally a light at the end of the tunnel for Iamgold which makes it worthy of consideration as a speculative bet if the stock can return to a more favorable valuation and provide a margin of safety. Let's take a look at the stock's valuation below:

Valuation

Based on ~490 million fully diluted shares and a share price of US$2.37, Iamgold trades at a market cap of ~$1.16 billion and an enterprise value of ~$1.44 billion. This may seem like a very reasonable valuation for a future ~700,000-ounce producer. However, although while Cote is a world-class asset, Essakane and Westwood are high-cost assets with relatively short mine lives, with just ~600,000 ounces of reserves at Westwood (year-end 2022), and barely ~2.0 million ounces of reserves at Essakane. And with Westwood's costs consistently coming in above $2,000/oz and a history of seismicity, it's difficult to assign any value to this Tier-1 jurisdiction asset. As for Essakane, the security situation in Burkina Faso is not improving, and even some West African-focused producers have divested what I otherwise thought to be relatively core assets, as evidenced by Endeavour Mining's ( OTCQX:EDVMF ) recent sale of Wahgnion and Boungou. In fact, Iamgold stated terrorist-related incidents have continued unabated in Burkina Faso (and the immediate region of the Essakane Mine) and this has affected supply chains, with higher costs to bring employees, contractors, supplies, and inventory to the mine site.

So, with a high-cost asset in a Tier-3 jurisdiction (Essakane), and an extremely high cost asset with a short mine life in Canada (Westwood), I would argue that Iamgold's true production profile over the next five years is ~300,000 ounces, which is its approximate share of Cote Gold in the first five years given that I don't expect the market to assign much of a multiple to its other two assets. And while this wouldn't be as negative if Iamgold had a solid development pipeline, the company sold off its other operating asset (Rosebel) and most of its development pipeline to fund Cote construction and avoid further equity dilution, meaning this is primarily a Cote story, with much less diversification given that Cote is the only significant future free cash flow generator in the portfolio. Plus, while Cote Gold is certainly a solid asset to have majority ownership of as a mid-tier producer, I see a more conservative fair value of $1.50 billion for Iamgold's ownership of Cote Gold (~56%), which includes upside from Gosselin.

Cote Gold TR & Iamgold News Release (Company Filings)

{kind=link}

Although this fair value estimate on attributable NPV (5%) and exploration upside at Cote Gold covers Iamgold's market cap, I think it's difficult to assign more than $450 million to Essakane and Westwood combined, which is offset by estimated corporate G&A of $450 million. Meanwhile, Iamgold has ~$250 million in net debt that also must be subtracted out from fair value (adjusting for deferred proceeds due by year-end from asset sales). Finally, I don't see any reason that Iamgold should trade at 1.0x P/NAV as a mid-tier producer with one exceptional asset and two high-cost assets with relatively short mine lives with one being in Burkina Faso. Instead, I think a 0.95x multiple is more conservative given the worsening security situation in Burkina Faso and rising costs at this asset (as a result). After adjusting for these items and this more conservative multiple, I see a fair value for Iamgold of ~$1.19 billion, translating to a fair value of US$2.43, pointing to just a 3% upside from current levels on a strictly P/NAV basis.

Iamgold - Year-To-Date Corporate G&A (Company Filings)

{kind=link}

Assuming we use a 70% weighting to P/NAV (0.95x multiple) and 30% weighting to P/CF (5.5x multiple) to derive Iamgold's fair value and estimates of operating cash flow of $0.93 per share (FY2024), this translates to a fair value of US$3.23. This fair value estimate suggests Iamgold could rebound to its previous highs reached in May if it were to trade at fair value and it points to a 36% upside from current levels. However, in a sector where the fundamentals have gone out the window and even the world's No. 2 gold producer is trading at less than 6.0x FY2024 cash flow per share estimates, I'm less confident in a rebound of this magnitude occurring before year-end. Plus, I require a minimum 40% discount to fair value to justify entering new positions in small-cap producers. If we apply this discount to Iamgold's estimated fair value of US$3.23, its low-risk buy zone doesn't come in until $1.95 or lower.

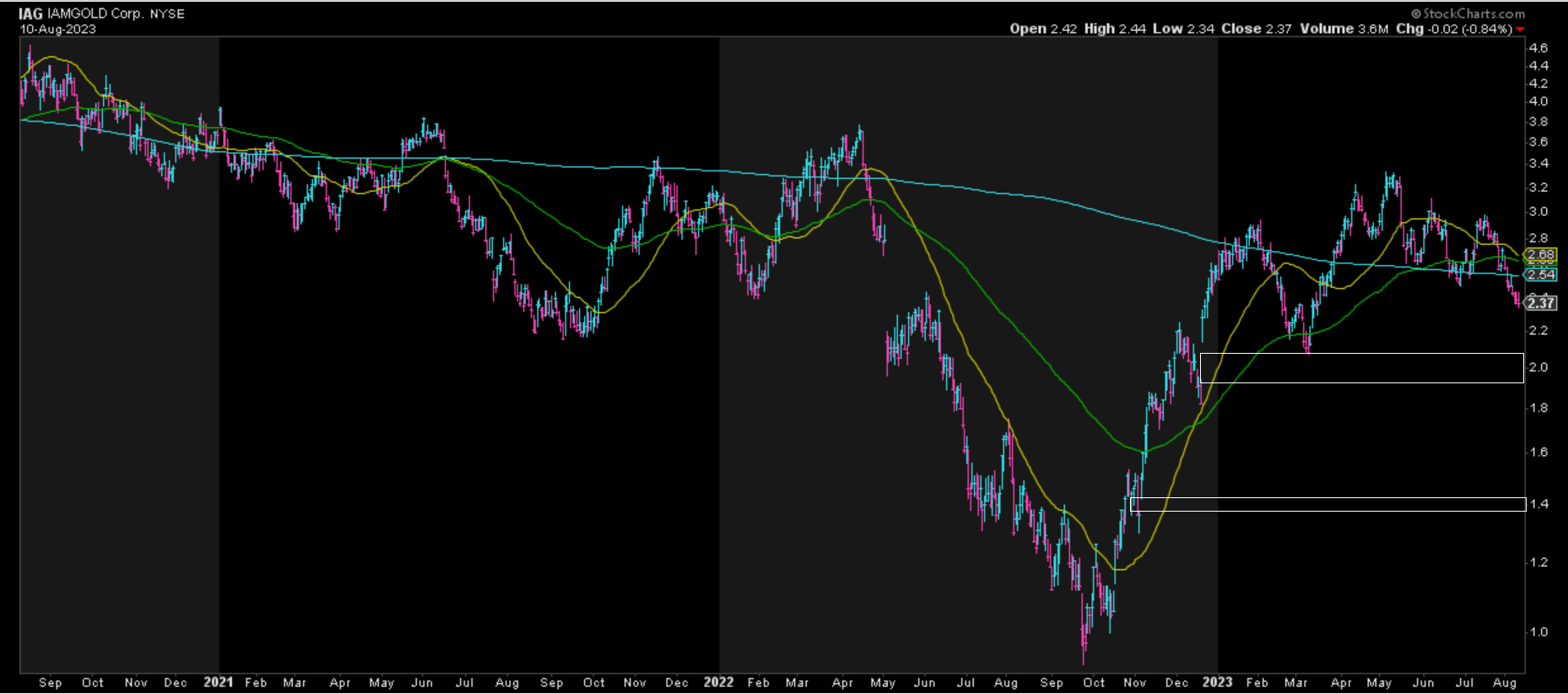

Obviously, Iamgold doesn't have to decline to US$1.95, and I could be wrong that further downside is likely. Still, with several higher-quality operators on sale with better track records that are buying back shares or paying shareholders to wait (attractive dividend yields), I continue to see better reward/risk setups elsewhere. Besides, the stock has multiple open gaps in its chart at US$1.39 and US$1.95 which is not ideal, making it tough to rule out a deeper correction to fill at least one of these gaps. Therefore, I don't see any reason to rush into the stock at current levels at US$2.37, especially with momentum recently flipping to the downside, with the stock set to see its shorter-term moving averages cross beneath its 200-day moving average over the next month if we don't see a sharp rebound in the stock immediately.

Iamgold - Daily Chart With Open Gaps (StockCharts.com)

{kind=link}

Summary

Iamgold has corrected over 25% from its highs after a period of strong outperformance, and while the stock is no longer fully valued where it was at its recent highs, I still don't see enough of a margin of safety at current levels. This is especially true when sentiment is worsening for West African gold producers and Iamgold has a substantial portion of its production profile and NAV tied to Essakane. On the positive side, Iamgold looks like it will be able to fund Cote Gold construction without any further equity dilution or royalty/stream sales on the asset, and the project is nearing the finish line. That said, I continue to see more attractive bets elsewhere in the sector, such as B2Gold which looks to have a conservative 50% upside to current levels and pays a ~5.4% dividend yield with a better development pipeline and a far better track record of creating shareholder value.

For further details see:

Iamgold: Nearing The Finish Line At Cote Gold